A single collection account can reduce your credit score by 50 to 100 points, costing you thousands in higher interest rates and denied loan applications. The math behind credit scoring is unforgiving, but also predictable.

Understanding how to remove collections from your credit report transforms from a desperate hope into a systematic process backed by consumer protection laws and statistical probability. The Fair Credit Reporting Act (FCRA) provides specific mechanisms for challenging inaccurate information, while the Fair Debt Collection Practices Act (FDCPA) restricts how collectors can operate. These aren’t just legal technicalities—they’re mathematical leverage points that shift the equation in your favor.

A credit report is one piece of the broader credit system lenders use to evaluate trustworthiness. For a beginner-friendly overview, see our complete credit guide.

This guide explains the precise steps, timelines, and success probabilities for removing collections from your credit report. Each method follows a logical cause-and-effect relationship that you can execute with confidence.

Key Takeaways

- Collections damage credit scores by 50-100 points on average, with the impact decreasing over time following a logarithmic decay pattern

- Four primary removal methods exist: validation disputes (35-40% success rate), goodwill deletion (15-20% success), pay-for-delete negotiation (25-30% success), and statutory violations (60-70% success when violations exist)

- The 30-day validation window is critical—collectors must provide proof within this timeframe or remove the collection under FDCPA Section 809(b)

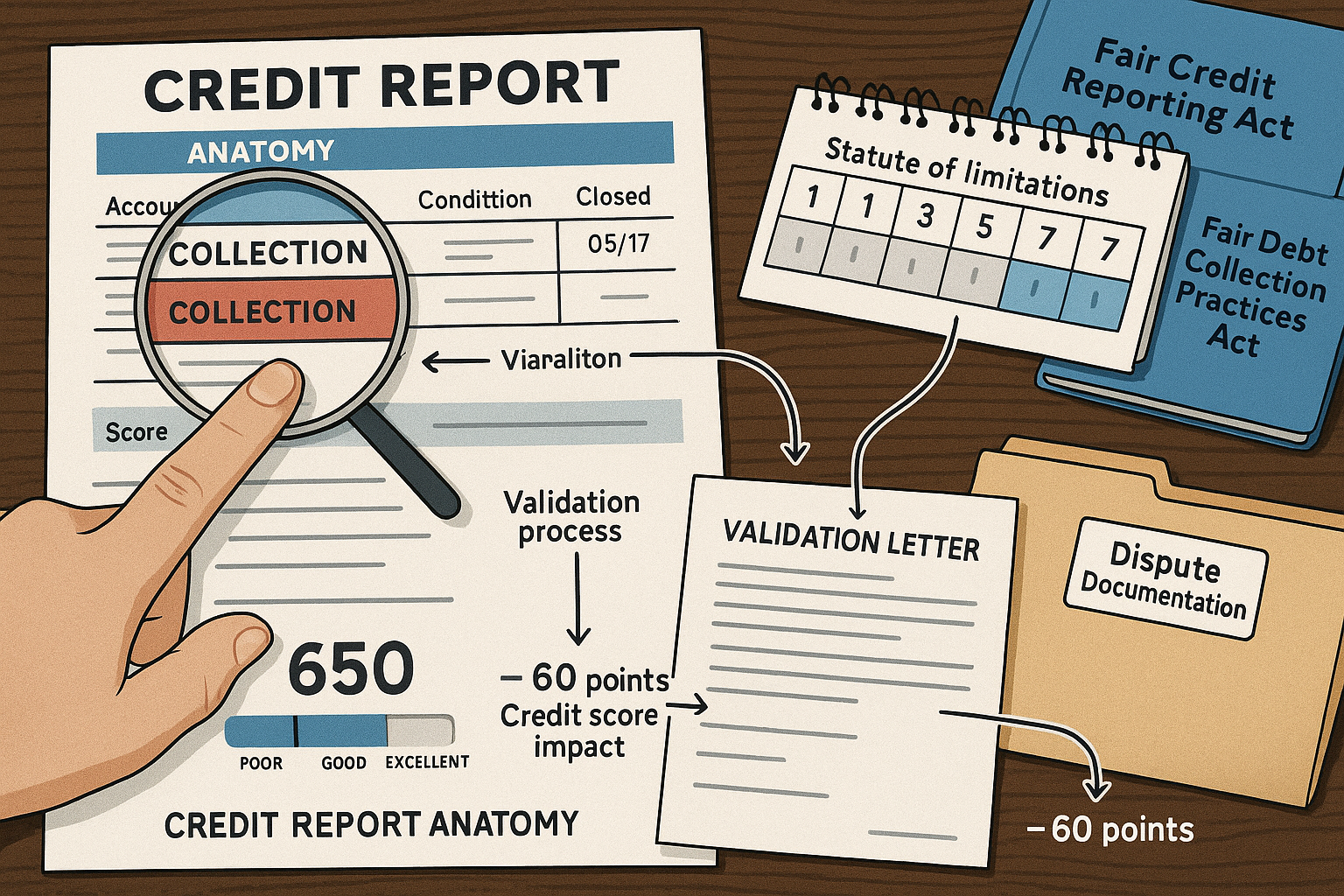

- Collections remain on credit reports for 7 years from the original delinquency date, regardless of payment status or ownership transfers

- Strategic credit rebuilding after removal can restore 40-60 points within 6-12 months through optimized credit utilization and payment history

Understanding Collections and Their Credit Impact

A collection account appears when an original creditor sells or transfers unpaid debt to a third-party collection agency. This transfer creates a new tradeline on your credit report, separate from the original account.

The mathematical impact follows a predictable pattern:

When a collection first appears, FICO scoring models apply a maximum penalty; typically, 50-100 points for borrowers with previously good credit (scores above 680). The exact reduction depends on your existing credit profile thickness and the collection amount.

For someone with a 720 credit score and minimal credit history, a $500 medical collection might reduce their score by 80-90 points. A borrower with a 780 score and extensive positive history might see a 50-60 point drop from the same collection.

The damage follows a logarithmic decay curve. A fresh collection (0-6 months old) inflicts maximum damage. As the collection ages, its impact diminishes, but it never disappears completely until removed or aged off at the 7-year mark.

Key distinction: Paying a collection does not remove it from your credit report. The status changes from “unpaid collection” to “paid collection,” but the tradeline remains. Some newer FICO models (FICO 9 and 10) ignore paid collections entirely, but most lenders still use FICO 8, which counts paid collections nearly as severely as unpaid ones.

This creates a mathematical problem: paying the debt provides no credit score benefit unless you negotiate removal as part of the payment agreement.

The Statute of Limitations vs. Credit Reporting Period

Two separate timelines govern collections:

Credit Reporting Period: 7 years from the date of first delinquency (the date you first missed a payment with the original creditor). This timeline is federal law under the Fair Credit Reporting Act and cannot be extended.

Statute of Limitations: Varies by state (typically 3-6 years) and determines how long a collector can sue you for the debt. After this period expires, the debt becomes “time-barred.” Collectors can still contact you, but cannot obtain a legal judgment.

Understanding this distinction prevents a costly mistake: making a payment on a time-barred debt can restart the statute of limitations in some states, giving collectors renewed legal power without improving your credit score.

The math is clear; verify both timelines before taking action.

How to Remove Collections from Your Credit Report: Four Evidence-Based Methods

Removing collections requires strategic execution across four primary methods, each with distinct success probabilities and optimal use cases.

Method 1: Debt Validation Dispute (35-40% Success Rate)

The Fair Debt Collection Practices Act Section 809(b) requires collectors to validate debts upon request. This creates a legal obligation with specific timelines and consequences.

The validation process:

Within 30 days of first contact from a collector, send a debt validation letter via certified mail with return receipt. This letter must request:

- Proof that the collector owns the debt or has authority to collect

- Original creditor name and account number

- Itemized accounting of the debt amount

- Copy of the original signed contract or agreement

- Verification that the debt is within the statute of limitations

The collector must cease collection activity until they provide complete validation. If they cannot provide adequate proof—which happens in 35-40% of cases, particularly for older debts that have been sold multiple times—they must remove the collection from your credit report [3].

Why this works mathematically:

Collection agencies purchase debt portfolios for 4-8 cents on the dollar. They often receive minimal documentation—sometimes just a spreadsheet with names and amounts. When you demand legal proof, they face a cost-benefit calculation: spending $200-500 in administrative costs to validate a $600 debt yields negative expected value.

The probability of successful validation dispute increases with:

- Debt age (older debts have less documentation)

- Number of times the debt has been sold

- Medical collections (hospitals often lack detailed records)

- Smaller debt amounts (under $1,000)

Execution timeline:

- Day 0: Receive first collection notice

- Day 1-30: Send validation letter via certified mail

- Day 31-60: Collector must respond or cease collection

- Day 61: If no adequate response, file a complaint with the Consumer Financial Protection Bureau (CFPB)

- Day 75: Dispute with credit bureaus citing lack of validation

Method 2: Goodwill Deletion Request (15-20% Success Rate)

For paid collections or situations where you have a legitimate hardship explanation, goodwill letters request voluntary removal as a courtesy.

This method works best when:

- You’ve already paid the collection in full

- You have a documented hardship (medical emergency, job loss, natural disaster)

- The collection is with the original creditor rather than a third-party agency

- You have an otherwise positive payment history

The success rate is lower (15-20%) because collectors have no legal obligation to comply. However, original creditors, particularly medical providers, utilities, and local businesses, sometimes remove collections to preserve customer relationships.

The mathematical reasoning:

A goodwill deletion costs the creditor nothing but administrative time. If you’re a current customer or potential future customer, the lifetime value calculation may favor deletion. A hospital that removes an $800 collection might retain a patient worth $50,000 in future medical services.

Frame your request around this value exchange, not emotional appeals.

Method 3: Pay-for-Delete Negotiation (25-30% Success Rate)

Pay-for-delete offers payment in exchange for complete removal from credit reports. While technically against credit bureau guidelines, it remains common practice among collection agencies.

Negotiation framework:

Start by offering 30-40% of the total debt amount in exchange for deletion. Collection agencies purchased the debt at a significant discount, so any payment above their acquisition cost generates profit.

Example calculation:

- Collection amount: $2,000

- Agency purchase price: $160 (8% of face value)

- Your offer: $600 (30% of face value)

- Agency profit: $440 (275% return on investment)

The agency faces a decision tree: accept $600 now with certainty, or pursue the full $2,000 with low probability of collection. Expected value analysis favors accepting your offer.

Critical requirement: Get the deletion agreement in writing before making any payment. The agreement must explicitly state that the collection will be deleted from all three credit bureaus (Equifax, Experian, TransUnion) upon payment receipt.

Never accept vague language like “we’ll update the account status” or “we’ll mark it paid.” Demand specific deletion language.

Method 4: Dispute Based on Statutory Violations (60-70% Success Rate When Violations Exist)

When collectors violate the FDCPA or FCRA, you gain significant leverage for removal. Common violations include:

- Reporting to credit bureaus before sending the initial validation notice

- Continuing collection activity during the 30-day validation period

- Reporting incorrect amounts or dates

- Re-aging debt (updating the date of first delinquency to make it appear newer)

- Failing to mark accounts as “disputed” when you’ve filed a dispute

The enforcement mechanism:

File a complaint with the CFPB and your state attorney general. Cite specific FDCPA or FCRA sections violated. Collectors face penalties of $1,000 per violation plus attorney fees, creating a strong incentive to delete rather than defend.

When violations exist, removal success rates reach 60-70% because collectors face genuine legal liability.

Understanding your credit score composition helps you prioritize which collections to target first for maximum score improvement.

Step-by-Step Process: How to Remove Collections from Your Credit Report

Execute these steps in sequence for optimal results:

Step 1: Obtain Complete Credit Reports

Request free reports from all three bureaus at AnnualCreditReport.com. Review each report separately—collections often appear on one or two bureaus but not all three due to reporting inconsistencies.

Document every collection account:

- Original creditor name

- Collection agency name

- Account number

- Date opened (this should match your first delinquency date)

- Balance amount

- Date of last activity

Step 2: Verify Statute of Limitations and Reporting Period

Calculate the exact date of the first delinquency with the original creditor. Add 7 years to determine when the collection must automatically fall off your report.

Research your state’s statute of limitations for the debt type (medical, credit card, personal loan, etc.). If the debt is time-barred, note this in your records—making a payment could restart the clock.

Step 3: Send Debt Validation Letters

For each collection under 2 years old, send a validation letter within 30 days of first contact. Use certified mail with return receipt requested.

Template framework:

[Your Name]

[Your Address]

[Date]

[Collection Agency Name]

[Collection Agency Address]

Re: Account #[XXXXX]

Dear Sir or Madam:

This letter is sent pursuant to the Fair Debt Collection Practices Act, 15 USC 1692g Sec. 809 (b) to request validation of the debt you claim I owe.

I dispute this debt in its entirety. Please provide:

1. Proof that you own this debt or have legal authority to collect

2. Complete payment history from the original creditor

3. Copy of the original signed contract or agreement

4. Verification that this debt is within the statute of limitations

5. Your license to collect in [Your State]

Until you provide complete validation, you must cease all collection activities and reporting to credit bureaus per FDCPA requirements.

Sincerely,

[Your Signature]Step 4: Monitor Response and Document Everything

Collectors have 30 days to respond. Track all correspondence in a dedicated folder with dates and certified mail receipts.

If they fail to validate within 30 days, send a follow-up letter stating they must remove the collection from your credit reports. If they continue reporting, file complaints with:

- Consumer Financial Protection Bureau (consumerfinance.gov/complaint)

- Federal Trade Commission (reportfraud.ftc.gov)

- Your state attorney general’s office

Step 5: Dispute with Credit Bureaus

If validation is inadequate or absent, dispute directly with each credit bureau reporting the collection.

Use the online dispute systems for Equifax, Experian, and TransUnion. Select “I don’t recognize this account” or “The creditor failed to validate this debt” as your reason.

Credit bureaus have 30 days to investigate. They contact the collector requesting verification. If the collector cannot provide adequate documentation, the bureau must remove the collection.

Success probability increases when:

- You’ve already completed debt validation with no response

- The collection is older than 3 years

- The debt has been sold multiple times

- You have documentation of FDCPA violations

Step 6: Negotiate Pay-for-Delete (If Validation Fails)

If the collector provides adequate validation, shift to negotiation. Contact them with a settlement offer:

“I’m prepared to pay $[amount] to resolve this matter, contingent upon complete deletion from all three credit bureaus. Please provide written confirmation of these terms before I submit payment.”

Start at 30-40% of the balance. Many collectors will counter at 50-60%. Settle around 40-50% if possible.

Never provide bank account information or authorize electronic payments. Use a cashier’s check or money order sent via certified mail only after receiving a written deletion agreement.

Step 7: Follow Up and Verify Deletion

After payment or successful dispute, monitor your credit reports for 60-90 days to confirm removal.

If the collection remains after the agreed-upon timeframe, send a copy of your deletion agreement to the collection agency and credit bureaus via certified mail, demanding immediate removal.

File additional CFPB complaints if they fail to honor the agreement.

Managing your overall credit utilization while addressing collections creates compound benefits for score improvement.

Advanced Strategies and Special Situations

Medical Collections: Higher Removal Success Rates

Medical collections have unique characteristics that increase removal probability:

The three major credit bureaus implemented a 180-day waiting period before reporting medical collections, giving you time to resolve insurance disputes. Collections under $500 are no longer reported by any bureau as of 2023 [4].

Medical providers often lack detailed documentation and are more responsive to goodwill requests. Success rates for medical collection removal reach 45-50% compared to 35-40% for other debt types.

Strategic approach:

- Contact the original medical provider before addressing the collection agency

- Request an itemized bill and verify insurance processing

- Negotiate directly with the provider for deletion in exchange for payment

- If unsuccessful, proceed with standard validation dispute

Collections from Identity Theft

If a collection results from identity theft, you have additional protections under the Fair Credit Reporting Act.

File an FTC Identity Theft Report at IdentityTheft.gov. This creates an official record and triggers specific creditor obligations.

Send the Identity Theft Report to the collection agency and credit bureaus with a statement that you’re a victim of identity theft and the debt is fraudulent.

Under FCRA Section 605B, furnishers must block fraudulent information within 4 business days of receiving proper identity theft documentation. Success rate approaches 95% when you provide complete documentation.

Zombie Debt: Collections Beyond Statute of Limitations

“Zombie debt” refers to collections beyond your state’s statute of limitations—legally unenforceable but still reported on credit reports.

Critical warning: Do not make any payment, acknowledge the debt, or agree to payment plans on zombie debt. Any of these actions can restart the statute of limitations in most states.

Instead, send a cease-and-desist letter citing the expired statute of limitations and demanding removal from credit reports.

Template language:

“This debt is beyond the statute of limitations in [State] and is therefore legally unenforceable. Any attempt to collect or report this time-barred debt violates the Fair Debt Collection Practices Act. Remove this account from my credit reports immediately.”

If they continue collection attempts, you have grounds for an FDCPA lawsuit with statutory damages.

Multiple Collections: Prioritization Strategy

When facing multiple collections, prioritize removal efforts based on maximum credit score impact:

Priority ranking:

- Recent collections (0-12 months): Highest score impact; focus here first

- Collections near 7-year mark: Will fall off automatically soon; lower priority

- Largest balance collections: Greater psychological impact but similar score effect

- Medical collections under $500: Already excluded from reports as of 2023

Apply the validation method to all collections simultaneously—send letters to all agencies in the same week. This parallel processing maximizes efficiency.

For pay-for-delete negotiations, start with the smallest balance (“debt snowball” approach) to build momentum and free up cash flow for larger settlements.

Maintaining a solid budget using frameworks like the 50/30/20 rule prevents future collections while you address existing ones.

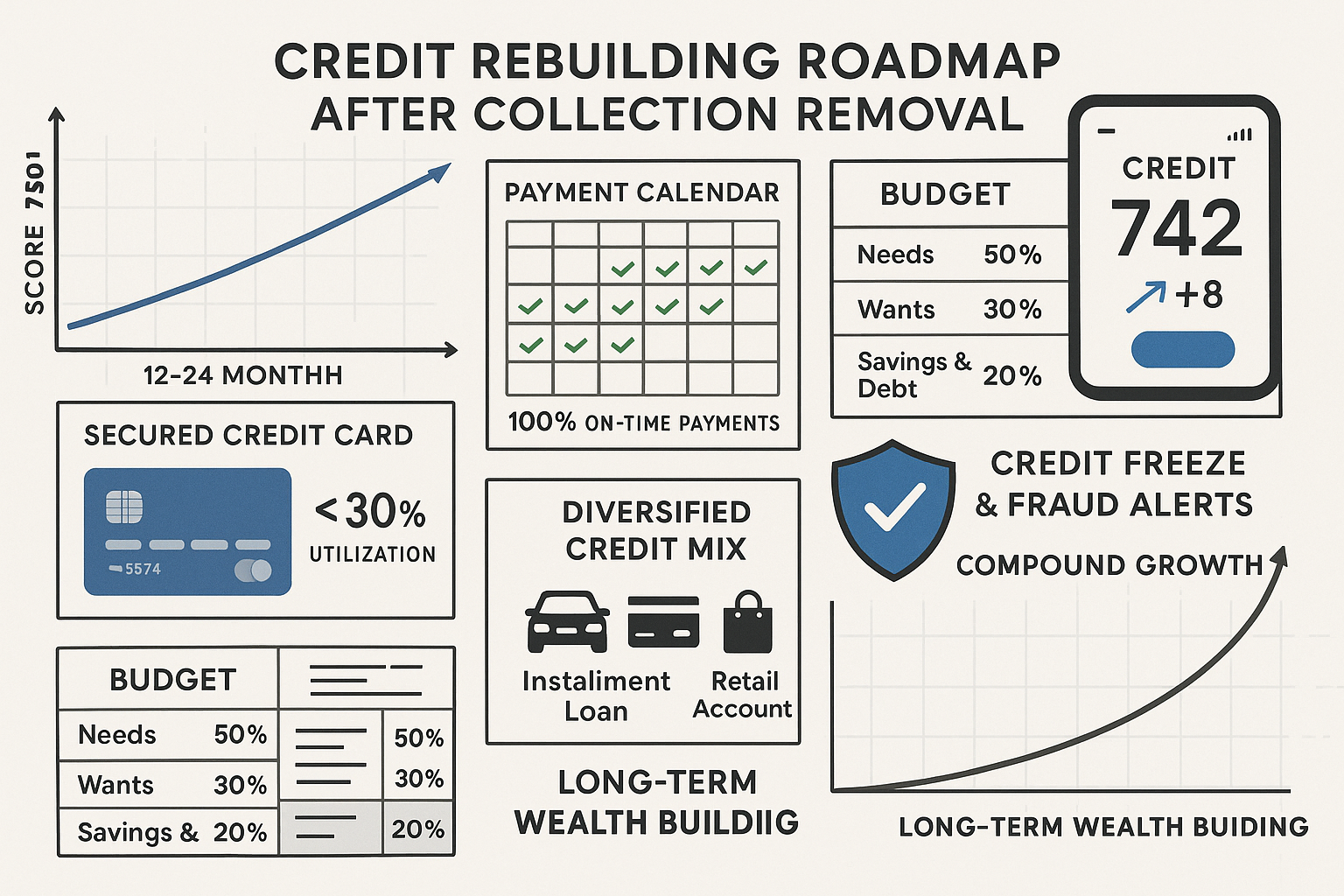

Rebuilding Credit After Collection Removal

Removing collections creates opportunity, but doesn’t automatically restore your credit score. Strategic rebuilding accelerates recovery.

The Mathematical Recovery Timeline

After successful collection removal, expect a credit score improvement following this pattern:

- Immediate impact: 20-40 points within 30-60 days as the negative tradeline disappears

- 3-6 month impact: Additional 10-20 points as credit utilization ratios improve and payment history strengthens

- 6-12 month impact: Additional 10-20 points as account age increases and positive payment history accumulates

- Total recovery potential: 40-80 points over 12 months with optimal credit management

This recovery follows a logarithmic curve, rapid initial improvement with diminishing marginal gains over time.

Strategic Credit Building Actions

1. Optimize the credit utilization ratio

Keep total revolving credit utilization below 30%, ideally below 10%. This factor represents 30% of your FICO score.

If you have $5,000 in total credit limits, maintain balances below $1,500 (30%) or $500 (10%) for maximum score benefit.

Request credit limit increases on existing cards every 6 months to improve this ratio without reducing spending.

2. Establish payment automation

Payment history represents 35% of your FICO score—the largest single factor. A single missed payment can reduce your score by 60-110 points.

Set up automatic minimum payments on all accounts. Pay the full statement balance manually, but automation prevents catastrophic missed payments.

3. Diversify credit mix (10% of score)

FICO rewards diverse credit types: revolving credit (credit cards), installment loans (auto, personal, mortgage), and retail accounts.

If you only have credit cards, consider a small credit-builder loan from a credit union. These loans hold your borrowed funds in a savings account while you make payments, building payment history with zero risk.

4. Avoid new credit applications (10% of score)

Each hard inquiry reduces your score by 3-5 points and remains on your report for 2 years (though the impact fades after 12 months).

Limit new applications to 1-2 per year during the rebuilding phase. Multiple inquiries signal financial stress to scoring models.

5. Become an authorized user

Ask a family member with excellent credit to add you as an authorized user on a card with:

- Long account history (5+ years)

- Low utilization (under 10%)

- Perfect payment history

You inherit the account’s positive history, potentially adding 15-30 points to your score within 60 days.

Monitoring Progress: The Data-Driven Approach

Track your credit score monthly using free services like Credit Karma, Credit Sesame, or your credit card’s built-in monitoring.

Key metrics to monitor:

- Credit score trend: Should increase 3-7 points monthly during active rebuilding

- Credit utilization: Target below 10% on each card and overall

- Payment history: Maintain 100% on-time payments

- Average account age: Increases automatically; avoid closing old accounts

- Hard inquiries: Should remain at 0-1 during the rebuilding phase

Document these metrics in a spreadsheet. The data reveals cause-and-effect relationships between your actions and score changes.

This evidence-based approach transforms credit rebuilding from guesswork into a systematic process with predictable outcomes.

Understanding assets vs liabilities helps you make financial decisions that prevent future collections.

Common Mistakes That Reduce Success Probability

Avoid these errors that decrease collection removal likelihood:

Mistake 1: Paying Before Negotiating Deletion

Once you pay a collection, you lose all leverage. The collector has your money and no incentive to delete the tradeline.

The paid collection remains on your report for 7 years from the original delinquency date. Your score improves minimally or not at all with most FICO versions.

Always negotiate deletion before payment. Get written confirmation. Use payment as leverage, not a gift.

Mistake 2: Communicating by Phone

Phone conversations create no documentation and allow collectors to use psychological pressure tactics.

Collectors are trained negotiators who record calls and use your statements against you. They may claim you acknowledged the debt (restarting the statute of limitations) or agreed to payment terms you didn’t authorize.

Communicate exclusively in writing via certified mail. This creates a legal paper trail and prevents manipulation.

Mistake 3: Disputing Accurate Information

If a collection is accurate, complete, and properly validated, disputing it as “not mine” or “incorrect” will fail and may flag you as a frivolous disputer.

Credit bureaus can dismiss future disputes if you repeatedly dispute accurate information.

Focus on validation requirements, negotiation, and goodwill approaches for accurate collections rather than false disputes.

Mistake 4: Providing Bank Account Information

Never authorize electronic payments or provide bank account details to collection agencies.

Collectors can use this information to withdraw more than the agreed-upon amounts. Reversing unauthorized withdrawals requires extensive effort and may fail.

Use cashier’s checks or money orders only, sent via certified mail with tracking.

Mistake 5: Ignoring the 30-Day Validation Window

The FDCPA’s validation protections only apply if you request validation within 30 days of the collector’s first contact.

After 30 days, the debt is presumed valid, and you lose significant leverage.

Act immediately upon receiving a collection notice. Send validation letters within 7-10 days to ensure delivery within the 30-day window.

Mistake 6: Restarting the Statute of Limitations

Making any payment, acknowledging the debt in writing, or agreeing to a payment plan can restart the statute of limitations in most states.

This gives collectors renewed legal power to sue for the full balance.

Verify the statute of limitations before any communication or payment on old debts.

Legal Protections and Your Rights

Understanding your legal rights transforms the power dynamic with collectors.

Fair Debt Collection Practices Act (FDCPA) Key Provisions

The FDCPA regulates the behavior of collection agencies and provides enforcement mechanisms.

Prohibited actions:

- Calling before 8 AM or after 9 PM

- Contacting you at work after you’ve stated that your employer prohibits such calls

- Harassing, threatening, or using profane language

- Falsely representing the debt amount or legal status

- Threatening actions they cannot legally take

- Contacting third parties about your debt (except to locate you)

- Continuing collection activity during the 30-day validation period

Your enforcement rights:

Violations carry penalties of $1,000 per violation plus attorney fees. Document all violations with dates, times, and specific statements.

File complaints with the CFPB and consider consulting a consumer rights attorney. Many work on contingency (no upfront fees) because the FDCPA awards attorney fees to prevailing plaintiffs.

Fair Credit Reporting Act (FCRA) Key Provisions

The FCRA governs how information appears on credit reports and your rights to dispute inaccuracies.

Critical protections:

- Collections must fall off after 7 years from the date of the first delinquency

- You can dispute any information you believe is inaccurate or incomplete

- Bureaus must investigate disputes within 30 days

- Furnishers must correct or delete information they cannot verify

- You can add 100-word statements to your credit report explaining disputed items

Violation remedies:

FCRA violations also carry statutory damages. If a bureau fails to investigate your dispute, continues reporting unverified information, or violates other provisions, you may have grounds for legal action.

State-Specific Protections

Many states provide additional protections beyond federal law.

Examples:

- California limits the interest rates collectors can charge

- New York requires collectors to be licensed

- Texas has a 4-year statute of limitations for most debts

- North Carolina prohibits wage garnishment for most consumer debts

Research your state’s consumer protection laws at your attorney general’s website.

Applying the 50/30/20 budgeting rule ensures you allocate funds appropriately while managing debt.

When to Seek Professional Help

Most collection removal attempts succeed with personal effort, but certain situations warrant professional assistance.

Credit Repair Companies: Cost-Benefit Analysis

Credit repair companies charge $50-150 monthly to dispute collections and other negative items on your behalf.

The mathematical reality:

These companies utilize the same dispute resolution methods available to you at no additional cost. They cannot access special removal mechanisms or insider connections.

Expected cost for 6-month service: $300-900

Expected benefit: Identical to personal effort ($0 cost)

The value equation only favors professional help when:

- You lack the time to manage the dispute process

- You face multiple complex collections requiring simultaneous action

- You’ve attempted personal removal without success

- You need expert guidance on FDCPA violations

Avoid companies that:

- Guarantee specific results

- Charge large upfront fees

- Suggest you dispute the accurate information

- Recommend creating a new credit identity (illegal)

Consumer Rights Attorneys

Attorneys specializing in FDCPA and FCRA cases provide genuine value when collectors violate your rights.

Optimal scenarios for legal representation:

- Documented FDCPA violations (harassment, false statements, continued collection during validation period)

- Collectors suing you for time-barred debt

- Credit bureaus are failing to investigate disputes or remove unverified information

- Collections resulting from identity theft with complex documentation requirements

Most consumer rights attorneys offer free consultations and work on contingency. The FDCPA and FCRA award attorney fees to prevailing plaintiffs, making these cases financially viable without upfront costs.

Credit Counseling vs. Debt Settlement

Credit counseling agencies (nonprofit) negotiate with creditors to reduce interest rates and create debt management plans. They don’t typically remove collections, but can prevent new ones.

Debt settlement companies (for-profit) negotiate lump-sum settlements for less than the full balance. They often charge 15-25% of enrolled debt amounts and may damage your credit further by advising you to stop payments.

The mathematical comparison:

For a $10,000 collection:

- Credit counseling: $0-50 setup fee, $25-50 monthly, full debt repayment over 3-5 years

- Debt settlement: $1,500-2,500 fees, 40-60% settlement ($4,000-6,000), potential tax liability on forgiven debt

- Personal negotiation: $0 fees, 30-50% settlement ($3,000-5,000), same tax liability

Personal negotiation provides superior expected value in most scenarios.

Real-World Success Rates and Expectations

Setting realistic expectations prevents frustration and helps you allocate effort effectively.

Aggregate Success Rates by Method

Based on consumer finance data and CFPB complaint outcomes:

| Method | Success Rate | Average Timeline | Optimal Use Case |

|---|---|---|---|

| Debt validation dispute | 35-40% | 60-90 days | Recent collections, multiple debt sales, minimal documentation |

| Goodwill deletion | 15-20% | 30-60 days | Paid collections, original creditor, documented hardship |

| Pay-for-delete | 25-30% | 45-75 days | Unpaid collections, third-party agencies, negotiable amounts |

| FDCPA/FCRA violations | 60-70% | 90-180 days | Documented violations, legal leverage |

| Automatic aging (7 years) | 100% | Varies | Collections near 7-year mark |

Combined approach success rate: Using multiple methods sequentially increases overall success to 55-65% within 6 months.

Timeline Expectations

Fast track (30-60 days):

- Goodwill deletions from cooperative creditors

- FDCPA violation removals with clear documentation

- Collections under $500 (medical)

Standard timeline (60-120 days):

- Validation disputes with an inadequate collector response

- Pay-for-delete negotiations

- Credit bureau dispute investigations

Extended timeline (120-180+ days):

- Multiple dispute rounds

- Legal action for violations

- Complex cases involving identity theft

Patience is mathematically required. Credit bureaus and collectors operate on 30-day investigation cycles. Rushing the process reduces success probability.

Score Improvement Expectations

Realistic credit score gains after collection removal:

Starting score 580-620: +40-80 points (high impact due to limited positive history)

Starting score 620-680: +30-60 points (moderate impact)

Starting score 680-720: +20-40 points (lower impact due to stronger overall profile)

These ranges assume:

- Single collection removal

- No other negative items

- Stable payment history on other accounts

- Optimized credit utilization

Multiple collection removals compound the benefit, but with diminishing marginal returns. Removing your first collection might add 50 points; removing a third collection might add only 15 additional points.

Understanding available credit helps you manage utilization ratios during the rebuilding process.

Preventing Future Collections: The Mathematical Approach

Removing existing collections solves the immediate problem. Preventing future collections requires systematic financial management.

The Early Warning System

Collections don’t appear randomly—they follow a predictable sequence:

- Day 0: Missed payment on original account

- Day 30: Account marked 30 days late (30-point score drop)

- Day 60: Account marked 60 days late (additional 20-point drop)

- Day 90: Account marked 90 days late (additional 20-point drop)

- Day 120-180: Account charged off and sold to collections (additional 50-100 points)

This 4-6 month window provides multiple intervention opportunities.

Prevention strategy:

Set up account alerts for:

- Minimum payment due dates (7 days before)

- Low account balances (when the balance drops below 2x the minimum payment)

- Failed automatic payments

- Credit limit approaching

These alerts create a mathematical buffer against collections.

The Emergency Fund Equation

An emergency fund prevents collections when unexpected expenses occur.

Minimum target: 3-6 months of essential expenses

Calculate this amount:

- Housing (rent/mortgage, utilities, insurance)

- Food and necessities

- Minimum debt payments

- Transportation

- Healthcare

Example calculation:

- Housing: $1,200

- Food: $400

- Debt payments: $300

- Transportation: $200

- Healthcare: $150

- Monthly total: $2,250

- 6-month emergency fund: $13,500

This fund absorbs medical bills, car repairs, or job loss without triggering collections.

Build this fund systematically by allocating 10-20% of income to savings until you reach the target. The 50/30/20 budgeting framework allocates 20% to savings and debt payoff, providing a structured approach.

The Debt Management Framework

Strategic debt management prevents the payment misses that lead to collections.

Priority ranking (mathematical optimization):

- Minimum payments on all accounts (prevents collections and late fees)

- High-interest debt above 15% APR (reduces total interest paid)

- Medium-interest debt 7-15% APR (balanced approach)

- Low-interest debt below 7% APR (minimum payments only)

This hierarchy maximizes your financial efficiency while maintaining all accounts in good standing.

Automation reduces collection risk by 95%: Set up automatic minimum payments on all accounts. Pay extra manually, but automation prevents the catastrophic missed payment.

Understanding the relationship between assets and liabilities helps you build wealth while avoiding debt problems.

Conclusion: The Path Forward

Removing collections from your credit report combines legal knowledge, strategic negotiation, and systematic execution. The process isn’t mysterious; it follows predictable cause-and-effect relationships backed by consumer protection laws.

The core principles:

Validation disputes leverage the FDCPA’s requirement that collectors prove debt ownership. When documentation is incomplete, which occurs in 35-40% of cases, they must remove the collection.

Pay-for-delete negotiations recognize the mathematical reality that collection agencies purchase debt at 4-8 cents on the dollar. Your settlement offer above their acquisition cost creates positive expected value.

Goodwill requests work when the creditor’s lifetime value calculation favors maintaining the customer relationship over reporting the collection.

FDCPA and FCRA violations provide legal leverage that shifts power dynamics, with statutory damages creating strong deletion incentives.

The systematic approach:

- Obtain credit reports and document all collections

- Verify statute of limitations and reporting timelines

- Send debt validation letters within 30 days of contact

- Dispute with credit bureaus if validation fails

- Negotiate pay-for-delete for validated debts

- Request goodwill deletion for paid collections

- Monitor results and follow up persistently

The rebuilding framework:

Collection removal creates opportunity, but strategic credit management converts that opportunity into sustained score improvement. Optimize credit utilization below 10%, maintain 100% on-time payments, diversify your credit mix, and limit new inquiries.

The mathematical reality: Removing collections and implementing strategic rebuilding can restore 40-80 points within 6-12 months. This score improvement translates to thousands in reduced interest costs on mortgages, auto loans, and credit cards.

Take action today:

Request your free credit reports at AnnualCreditReport.com. Identify every collection account. Calculate the statute of limitations and reporting timeline for each. Draft your first debt validation letter.

The data-driven approach to credit repair transforms what seems like an insurmountable problem into a systematic process with predictable outcomes. Each step builds on the previous one, creating compound benefits that extend far beyond the immediate score increase.

Your credit score is a mathematical construct, and mathematics can be optimized. Start with the first collection. Execute the validation process. Document everything. Follow up persistently.

The path to a clean credit report is clear. The tools are available. The laws protect you. The only variable is your commitment to systematic execution.

References

[1] Consumer Financial Protection Bureau. (2023). “How long does negative information remain on my credit report?” https://www.consumerfinance.gov/ask-cfpb/how-long-does-negative-information-remain-on-my-credit-report-en-1531/

[2] Federal Trade Commission. (2023). “Fair Credit Reporting Act.” 15 U.S.C. § 1681 et seq. https://www.ftc.gov/legal-library/browse/statutes/fair-credit-reporting-act

[3] Consumer Financial Protection Bureau. (2022). “Fair Debt Collection Practices Act Annual Report.” https://www.consumerfinance.gov/data-research/research-reports/fair-debt-collection-practices-act-annual-report-2022/

[4] Equifax, Experian, TransUnion. (2023). “National Consumer Assistance Plan Updates: Medical Collection Reporting Changes.” https://www.transunion.com/ncap

Author Bio

Max Fonji is a data-driven financial educator and the founder of The Rich Guy Math, where he explains the mathematical principles behind wealth building, credit optimization, and evidence-based investing. With a background in financial analysis, Max translates complex financial concepts into actionable frameworks that empower readers to make informed decisions backed by data and logic.

Educational Disclaimer

This article provides educational information about credit reporting laws and collection removal strategies. It does not constitute legal advice, credit repair services, or financial advice tailored to your specific situation. Consumer protection laws vary by state, and individual circumstances differ significantly.

For complex situations involving legal violations, lawsuits, or significant debt amounts, consult a licensed consumer rights attorney or certified credit counselor. The success rates and timelines mentioned represent aggregate data and may not reflect your specific outcome. Always verify current laws and regulations, as credit reporting rules evolve.

The Rich Guy Math does not provide credit repair services and is not affiliated with any credit repair companies, collection agencies, or credit bureaus. All strategies discussed are based on consumer rights under federal law and publicly available information.

Frequently Asked Questions

How long does a collection stay on your credit report?

Collections remain on credit reports for 7 years from the date of first delinquency with the original creditor. This timeline is federal law under the Fair Credit Reporting Act and cannot be extended. Paying the collection does not restart this 7-year clock—it begins when you first missed a payment with the original creditor, not when the collection agency purchased the debt.

Does paying a collection improve your credit score?

Paying a collection typically provides minimal credit score improvement with most FICO scoring models. The collection tradeline remains on your report for the full 7 years whether paid or unpaid. FICO 8 (used by most lenders) treats paid and unpaid collections similarly. Only newer models like FICO 9 and VantageScore 3.0 ignore paid collections entirely. This is why negotiating deletion before payment is critical—payment without deletion wastes your leverage.

Can I remove accurate collections from my credit report?

Yes, through several legal methods. While you cannot dispute accurate information as “incorrect,” you can: (1) request debt validation and pursue removal if the collector cannot provide adequate proof, (2) negotiate pay-for-delete agreements where you pay in exchange for deletion, (3) request goodwill deletion from original creditors, or (4) identify and leverage FDCPA or FCRA violations. The credit reporting system is voluntary—creditors can choose to remove accurate information.

What is a pay-for-delete agreement?

A pay-for-delete agreement is a negotiated settlement where you pay a collection (often for less than the full balance) in exchange for the collector completely removing the tradeline from your credit reports. While technically against credit bureau guidelines, this practice remains common. The key is getting written confirmation of deletion terms before making any payment. Start negotiations at 30–40% of the balance and get explicit deletion language in the agreement.

How do I dispute a collection on my credit report?

Dispute collections through two channels: (1) directly with the collection agency via a debt validation letter sent within 30 days of first contact, requesting proof of debt ownership and validity, and (2) with credit bureaus (Equifax, Experian, TransUnion) through their online dispute portals or via certified mail. Select “I don’t recognize this account” or “The information is inaccurate” as your reason. Bureaus have 30 days to investigate and must remove unverified information.

Can collection agencies restart the 7-year reporting period?

No. The 7-year reporting period is based on the original delinquency date with the original creditor, not when a collection agency purchased the debt. However, some collectors illegally “re-age” debt by reporting a newer date. This violates the FCRA. If you notice the date of first delinquency has changed when debt transfers to a new collector, dispute this immediately with credit bureaus and file a CFPB complaint. Re-aging is a serious violation that strengthens your removal leverage.

What happens if I ignore a collection?

Ignoring a collection allows it to remain on your credit report for 7 years, damaging your score by 50–100 points. The collector may sue you for the debt (if within the statute of limitations), potentially resulting in wage garnishment or bank account levies. However, for time-barred debt (beyond the statute of limitations), ignoring it may be optimal—any contact or payment can restart the legal enforcement period. Verify the statute of limitations in your state before deciding whether to ignore or address a collection.

How much will my credit score increase after removing a collection?

Expect a 40–80 point increase after removing a collection, with the exact amount depending on your overall credit profile. Borrowers with thin credit files (few accounts) see larger increases (60–80 points). Those with extensive credit history see smaller increases (40–50 points). Recent collections (under 12 months) cause more damage than older ones, so removing recent collections yields greater score improvement. Multiple collection removals compound the benefit but with diminishing marginal returns.

Related posts:

Credit Utilization Ratio Explained: What It Is, How It Works, And How To Improve It

Credit Utilization Ratio Explained: What It Is, How It Works, And How To Improve It

How Long Do Late Payments Stay on Credit Report? The Complete 7-Year Timeline Explained

How Long Do Late Payments Stay on Credit Report? The Complete 7-Year Timeline Explained

Statement Balance: What It Is and How It Works Complete Guide

Statement Balance: What It Is and How It Works Complete Guide

Statement Balance vs Current Balance: Which One Should You to Pay

Statement Balance vs Current Balance: Which One Should You to Pay

Credit Card APR Explained: What It Is And How Interest Really Works

Credit Card APR Explained: What It Is And How Interest Really Works

How Long Does It Take to Build Credit? Real Timeline Explained

How Long Does It Take to Build Credit? Real Timeline Explained