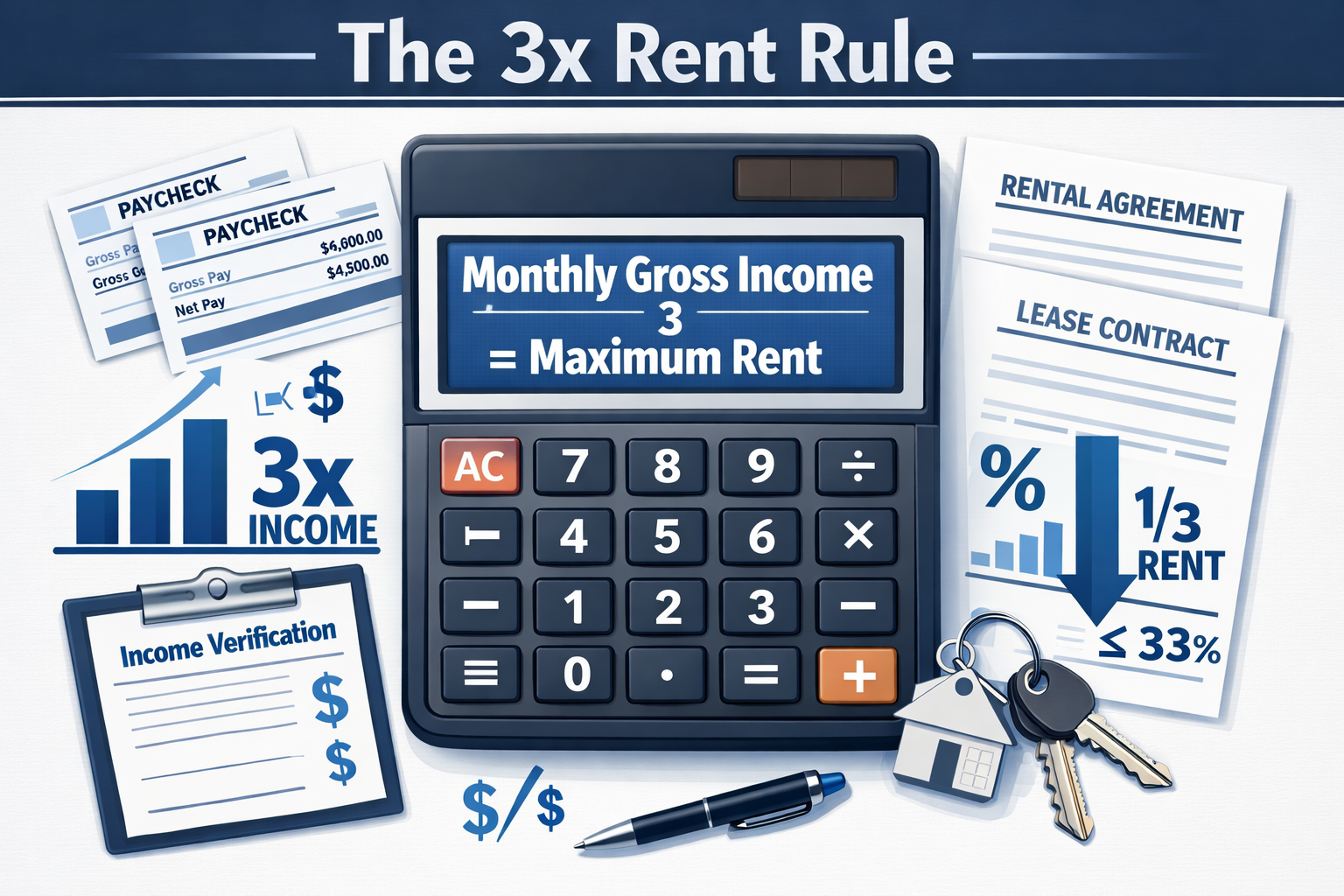

The 3x rent rule is a housing affordability guideline stating that your monthly gross income should be at least three times your monthly rent. Landlords use this screening tool to assess whether prospective tenants can comfortably afford rent payments without defaulting.

This rule serves as a quick risk management filter in the rental market. Property owners apply it to minimize financial risk and ensure consistent rent collection. For renters, understanding this calculation helps set realistic housing budgets before apartment hunting begins.

This article breaks down the math behind the 3x rent rule, explains when it works (and when it doesn’t), and provides practical alternatives for better budgeting and financial planning.

Key Takeaways

- The 3x rent rule requires the monthly gross income to be at least 3x the monthly rent amount.

- Landlords use this formula as a screening tool to reduce rent default risk

- The calculation uses gross income (before taxes), not net take-home pay

- High-debt borrowers and freelancers often struggle to meet this threshold

- Better alternatives include the 50/30/20 rule and a comprehensive cash flow analysis

What Is the 3x Rent Rule?

The 3x rent rule is a financial screening standard used primarily by landlords and property managers. It establishes a minimum income requirement for rental applicants.

The formula:

Monthly Gross Income ÷ 3 = Maximum Affordable Rent

Or inversely:

Monthly Rent × 3 = Minimum Required Income

Gross income refers to total earnings before taxes, retirement contributions, health insurance, or other deductions. This differs from net income, which represents actual take-home pay after all withholdings.

For example, if a paycheck shows $5,000 gross and $3,800 net, the 3x rent rule uses the $5,000 figure.

Quick summary:

- Uses gross (pre-tax) income

- Applies to monthly rent only (excludes utilities)

- Serves as a minimum threshold, not a maximum budget

- Functions as a landlord screening tool, not personal financial advice

Why Landlords Use the 3x Rent Rule

Property owners rely on the 3x rent rule to protect their investment and maintain cash flow stability. The logic centers on risk management and default prevention.

Core reasons landlords apply this standard:

- Income stability screening — Ensures tenants have sufficient buffer income to cover rent plus other living expenses

- Default risk reduction — Applicants earning less than 3x rent show a higher statistical probability of late or missed payments

- Property management standards — Many property management companies enforce this rule as company policy across all units

- Lender requirements — Mortgage lenders and investors often require landlords to maintain minimum tenant income ratios.

- Legal protection — Consistent application of objective income standards helps avoid discrimination claims

The rule assumes that dedicating more than 33% of gross income to rent creates financial strain. This threshold leaves room for taxes, debt payments, groceries, transportation, healthcare, and savings.

From a landlord’s perspective, a tenant spending 40-50% of gross income on rent becomes a higher-risk liability. One unexpected expense (car repair, medical bill) could force them to choose between rent and other necessities.

The 3x rent rule provides a simple, objective screening metric that requires minimal calculation and applies uniformly across applicants.

How to Calculate the 3x Rent Rule (Step-by-Step)

The calculation process involves three straightforward steps. Both renters and landlords can apply this formula in under 60 seconds.

Step 1 — Find Your Gross Monthly Income

Identify total monthly earnings before any deductions:

- Salary employees: Annual salary ÷ 12

- Hourly workers: Hourly rate × hours per week × 52 ÷ 12

- Multiple income sources: Add all gross income streams together

Include bonuses, commissions, and overtime only if guaranteed or documented over 12+ months.

Step 2 — Divide By Three

Take the gross monthly income figure and divide by 3:

Gross Monthly Income ÷ 3 = Maximum Rent Budget

This result represents the highest rent amount that meets the 3x standard.

Step 3 — Compare to Target Rent

Match your calculated maximum against actual rental listings:

- If target rent ≤ your calculated max → You meet the requirement

- If target rent > your calculated max → You fail the screening

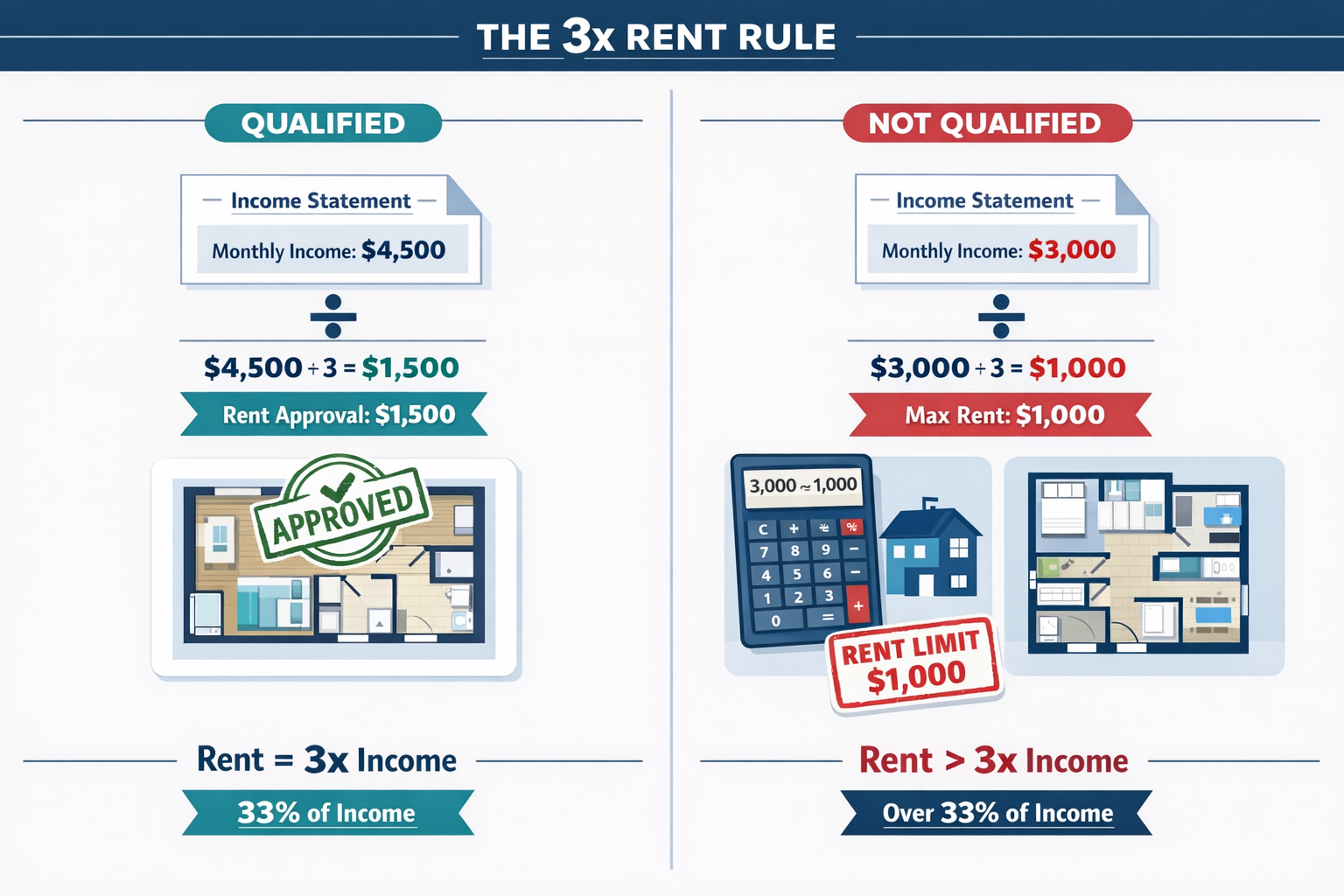

Example 1: $4,500 Monthly Income

Scenario: Sarah earns $54,000 annually as a marketing coordinator.

- Annual salary: $54,000

- Monthly gross income: $54,000 ÷ 12 = $4,500

- Maximum rent: $4,500 ÷ 3 = $1,500

Result: Sarah qualifies for apartments priced at $1,500/month or less. A $1,600 apartment would likely trigger automatic rejection unless she provides a co-signer.

Example 2: $3,000 Monthly Income

Scenario: James works part-time, earning $18/hour, 40 hours weekly.

- Hourly calculation: $18 × 40 × 52 = $37,440 annually

- Monthly gross income: $37,440 ÷ 12 = $3,120

- Maximum rent: $3,120 ÷ 3 = $1,040

Result: James meets the 3x standard for rentals priced at $1,040 or below. A $1,200 apartment exceeds his qualifying threshold by $160/month.

Understanding these calculations helps renters set realistic housing budgets before beginning apartment searches. It also prevents wasted application fees on properties where income disqualifies approval.

For more guidance on creating a comprehensive spending plan, explore the 50/30/20 rule budgeting framework.

Is the 3x Rent Rule Accurate for Real Life?

The 3x rent rule provides a useful baseline but fails to account for individual financial complexity. Real-world budgets involve variables that a simple income-to-rent ratio cannot capture.

Major limitations:

High Debt Payments

The formula ignores existing debt obligations:

- Student loans — A borrower with $800/month in student loan payments has significantly less disposable income than someone debt-free at the same gross income

- Credit card debt — Minimum payments of $300-500/month reduce actual housing affordability

- Auto loans — Car payments of $400-600/month shrink available cash flow

Someone earning $4,500/month with $1,200 in debt payments has only $3,300 remaining before rent. A $1,500 rent (which meets the 3x rule) would consume 45% of post-debt income, a dangerous financial position.

High Cost-of-Living Cities

Geographic location dramatically impacts housing affordability:

- San Francisco, New York, Boston — Median rents often exceed what 3x income allows for average earners

- State and local taxes — High-tax states reduce net income more than the gross calculation suggests

- Regional expenses — Transportation, food, and healthcare costs vary by 30-50% between markets

A $75,000 salary in Des Moines provides far more purchasing power than the same income in Manhattan, yet the 3x rule treats them identically.

Childcare Expenses

Families with young children face substantial additional costs:

- Daycare — $800-2,000/month per child in many markets

- After-school care — $300-600/month

- Healthcare — Family insurance premiums and out-of-pocket costs

These expenses can equal or exceed rent itself, making the 3x rule dangerously inadequate for parents.

Why It’s a Baseline, Not a Financial Plan

The 3x rent rule serves as a minimum screening threshold for landlords, not a personalized affordability assessment. It answers one question: “Can this applicant likely pay rent?” It does not answer: “Should this person rent here, given their complete financial picture?”

Renters should view passing the 3x test as a starting point, then apply more comprehensive budgeting methods to determine true affordability. For a broader financial framework, review budgeting fundamentals.

3x Rent Rule vs 30% Housing Rule

Two common housing affordability guidelines often create confusion. While related, they serve different purposes and produce different results.

| Metric | 3x Rent Rule | 30% Housing Rule |

|---|---|---|

| Income Type | Gross income (pre-tax) | Gross or net income (varies) |

| Primary Users | Landlords, property managers | Financial planners, budget advisors |

| Purpose | Tenant screening | Personal affordability planning |

| Calculation | Income ÷ 3 = max rent | Income × 0.30 = max housing cost |

| Includes Utilities | No (rent only) | Yes (total housing costs) |

| Flexibility | Rigid screening standard | Flexible guideline |

| Best For | Rental application approval | Comprehensive budget planning |

How They Overlap

Both rules target roughly the same affordability range:

- 3x rent rule: Rent should not exceed 33.3% of gross income

- 30% housing rule: Total housing costs should not exceed 30% of gross income

The 3x rule calculates from the rent side (rent × 3 = income), while the 30% rule calculates from the income side (income × 0.30 = housing budget).

Key Differences

Scope of costs:

The 30% rule typically includes utilities, renters’ insurance, and parking fees. The 3x rent rule considers base rent only. This makes the 30% rule more conservative and realistic for actual monthly expenses.

Flexibility:

Landlords enforce the 3x rule as a pass/fail screening test. The 30% rule functions as personal guidance; you can choose to spend 25% or 35% based on priorities and circumstances.

Income definition:

The 3x rule always uses gross income. Budget planners sometimes apply the 30% rule to net (take-home) income for more accurate cash flow planning.

Which Should You Use?

- For rental applications: Meet the 3x rent rule requirement

- For personal budgeting: Apply the 30% rule to total housing costs using net income

Combining both approaches provides the clearest picture. Pass the landlord’s 3x test, then verify the apartment fits within your 30% total housing budget.

When the 3x Rent Rule Doesn’t Work

Certain income types and financial situations make the 3x rent rule impractical or misleading. Landlords may require additional documentation or alternative verification methods.

Freelancers and Self-Employed Workers

Independent contractors face unique challenges:

- Income volatility — Monthly earnings fluctuate significantly

- Tax deductions — Business expenses reduce taxable income but don’t reflect actual cash flow

- Irregular payment schedules — Large payments followed by dry months create documentation problems

Solution: Provide 12-24 months of bank statements or tax returns showing average monthly income. Some landlords calculate annual income ÷ 12 for qualification purposes.

Commission-Based Income

Salespeople and commission earners experience similar issues:

- Seasonal variations — Strong quarters followed by slow periods

- Unpredictable timing — Commission checks may lag sales by 30-90 days

- Base salary confusion — Low base salary fails 3x test despite high total compensation

Solution: Submit year-to-date earnings statements and the previous year’s W-2 to demonstrate income stability over time.

High Tax States

Geographic location affects net income substantially:

- California, New York, and New Jersey — State income tax rates of 8-13% reduce take-home pay

- FICA and federal taxes — Additional 20-30% withholding

- Total tax burden — Combined taxes can consume 40-50% of gross income

Someone earning $6,000 gross in California may net only $3,600 after all taxes. A $2,000 rent (which passes the 3x test) actually consumes 56% of net income—financially unsustainable.

Solution: Calculate affordability using net income and the 30% rule instead of relying solely on the 3x gross income standard.

High Debt-to-Income Ratios

Borrowers with substantial debt obligations face affordability gaps:

- Student loans — $500-1,000/month payments

- Auto loans — $400-600/month

- Credit cards — $200-500/month minimum payments

- Personal loans — Variable amounts

The total debt-to-income (DTI) ratio provides better affordability insight than rent-to-income alone. Lenders typically prefer total DTI below 43%, meaning all debt payments plus rent should not exceed 43% of gross income.

For a deeper understanding of debt management, review comprehensive guides on managing debt obligations.

When to Request Exceptions

Applicants who fail the 3x test but possess strong financial profiles can negotiate:

- Large savings accounts — 6-12 months of rent in liquid savings

- Excellent credit scores — 750+ FICO score demonstrates payment reliability

- Co-signers — Parent or guarantor with qualifying income

- Larger security deposit — Offer 2-3 months rent upfront to offset risk

Landlords have discretion to waive or modify income requirements for applicants who demonstrate financial responsibility through alternative means.

Better Alternatives to the 3x Rent Rule

More sophisticated budgeting methods provide clearer affordability pictures than simple income ratios. These frameworks account for complete financial circumstances.

50/30/20 Budget Rule

This evidence-based framework divides after-tax income into three categories:

- 50% — Needs (housing, utilities, groceries, insurance, minimum debt payments)

- 30% — Wants (dining out, entertainment, hobbies, subscriptions)

- 20% — Savings (emergency fund, retirement, debt payoff beyond minimums)

Housing falls within the 50% “needs” category, meaning rent plus utilities should consume no more than 50% of net income (ideally closer to 30-35% to leave room for other necessities).

This method forces consideration of total financial obligations rather than focusing on rent in isolation.

Learn the complete framework at 50/30/20 rule budgeting.

Zero-Based Budgeting

This approach assigns every dollar of income to a specific purpose:

- List total monthly net income

- Allocate to categories until reaching zero (income – expenses = 0)

- Prioritize essentials first (housing, food, transportation)

- Assign remaining funds to savings, debt payoff, and discretionary spending

Zero-based budgeting reveals exactly how much remains for rent after accounting for all other financial obligations. It prevents the oversimplification of income-to-rent ratios.

See our complete framework of the zero-based budgeting guide.

Comprehensive Cash Flow Analysis

The most accurate affordability assessment examines the complete monthly cash flow:

Step 1: Calculate total monthly net income (after all taxes and deductions)

Step 2: List all fixed expenses:

- Debt payments (student loans, auto, credit cards)

- Insurance (health, auto, renters)

- Subscriptions and memberships

- Childcare

Step 3: Estimate variable expenses:

- Groceries

- Transportation and fuel

- Healthcare and medications

- Personal care

Step 4: Set savings targets:

- Emergency fund contribution

- Retirement savings

- Short-term goals

Step 5: Calculate the remaining amount available for housing:

Net Income – (Fixed + Variable + Savings) = Maximum Affordable Rent

This method produces the most accurate affordability figure because it accounts for actual financial reality rather than theoretical income ratios.

The 28/36 Rule (Mortgage Industry Standard)

While designed for homebuyers, this rule offers useful guidance:

- 28% rule — Housing costs should not exceed 28% of gross monthly income

- 36% rule — Total debt payments (housing + all other debt) should not exceed 36% of gross income

Renters can apply the same logic: if rent plus debt payments exceed 36% of gross income, financial stress becomes likely.

For additional budgeting resources and calculators, visit the budgeting and saving hub.

Should You Follow the 3x Rent Rule?

The answer depends on individual financial circumstances, income stability, and debt obligations. The 3x rent rule works well as a screening baseline, but should not replace comprehensive financial planning.

Good Fit If:

You have a stable, predictable income

- Salaried employees with consistent paychecks

- Government or corporate positions with minimal layoff risk

- Established career with a reliable income history

You carry low or no debt

- No student loans or auto loans

- Credit cards are paid in full monthly

- Minimal financial obligations beyond basic living expenses

You live in moderate cost-of-living areas

- Rent prices align with local median incomes

- Utilities and transportation costs remain reasonable

- Healthcare and childcare expenses stay manageable

You maintain healthy savings

- 3-6 months emergency fund already established

- Consistent retirement contributions

- Financial cushion for unexpected expenses

You have minimal dependents

- Single or dual-income household without children

- No elderly parent care responsibilities

- Limited family financial obligations

Bad Fit If:

You carry high-interest debt

- Credit card balances with 18-25% APR

- Personal loans are consuming a significant portion of the monthly income

- Debt payments exceeding $500/month

You have low or unstable savings

- Less than $1,000 in emergency fund

- No retirement contributions

- Living paycheck-to-paycheck despite meeting 3x test

You earn an irregular income

- Freelance or gig economy work

- Commission-based sales positions

- Seasonal employment with income gaps

You face high regional costs

- Major metropolitan areas (NYC, SF, LA, Boston)

- States with high income tax rates

- Areas with expensive healthcare or childcare

You support dependents

- Children requiring daycare or after-school care

- Elderly parents needing financial assistance

- Family members relying on your income

Practical Advice

Before committing to rent based solely on the 3x rule:

- Calculate total housing costs — Include utilities, renter’s insurance, parking, and any mandatory fees

- Review complete monthly expenses — Account for debt, groceries, transportation, healthcare, and savings

- Apply the 50/30/20 framework — Ensure housing fits within the 50% “needs” category of net income

- Maintain emergency reserves — Keep 3-6 months of expenses in liquid savings before signing a lease

- Consider future changes — Evaluate whether you can afford rent if income decreases or expenses increase

The 3x rent rule helps you qualify for an apartment. Comprehensive budgeting helps you afford it comfortably without financial stress.

For additional financial planning tools, explore The Rich Guy Math calculators for data-driven insights into budgeting, saving, and wealth building.

Interactive 3x Rent Rule Calculator

Rent as % of Income: 0%

Conclusion

The 3x rent rule establishes a simple affordability threshold: monthly gross income should equal at least three times the monthly rent. Landlords apply this standard to screen tenants and reduce default risk.

When to use it: The rule works effectively for salaried employees with stable income, low debt, and moderate cost-of-living expenses. It provides a quick qualification benchmark for rental applications.

When not to rely on it alone: High debt loads, irregular income, expensive geographic markets, and dependent care responsibilities all limit the rule’s accuracy. These situations require more comprehensive cash flow analysis.

Better approach: Combine the 3x rent rule with the 50/30/20 budgeting framework, total debt-to-income calculations, and complete monthly expense tracking. This multi-factor assessment produces realistic affordability figures that account for your complete financial picture.

The math behind money reveals that housing affordability extends far beyond simple income ratios. True financial stability requires understanding how rent fits within total cash flow, savings goals, and long-term wealth-building strategies.

For more evidence-based financial planning resources, explore the complete budgeting and saving guide and discover how data-driven insights build lasting financial security.

Disclaimer

This article provides educational information about the 3x rent rule and housing affordability calculations. It does not constitute financial advice, legal guidance, or professional consultation.

Individual financial circumstances vary significantly. Readers should evaluate their complete financial situation—including debt obligations, savings, dependents, and regional cost-of-living factors—before making decisions about housing.

Landlord requirements and rental application standards differ by property, management company, state, and local jurisdiction. Some landlords may apply stricter or more flexible income requirements than the 3x standard described here.

Consult qualified financial advisors, housing counselors, or legal professionals for personalized guidance regarding rental agreements, lease terms, and housing affordability specific to your situation.

The Rich Guy Math provides data-driven financial education to improve financial literacy and understanding. All calculations, examples, and recommendations serve educational purposes only.

Author Bio

Max Fonji is the founder of The Rich Guy Math, a financial education platform that explains the math behind money through data-driven analysis and evidence-based insights.

With expertise in financial modeling, investment analysis, and personal finance optimization, Max translates complex financial concepts into clear, actionable guidance for beginner and intermediate investors.

The Rich Guy Math focuses on teaching fundamental principles of wealth building, risk management, and financial decision-making through logical frameworks and quantitative analysis.

Learn more about evidence-based financial education at The Rich Guy Math.

References

[1] U.S. Department of Housing and Urban Development. (2024). “Affordability Standards and Housing Cost Burden.” HUD.gov. https://www.hud.gov

[2] Consumer Financial Protection Bureau. (2024). “Renting and Tenant Rights.” ConsumerFinance.gov. https://www.consumerfinance.gov

[3] National Multifamily Housing Council. (2024). “Income Verification Standards for Rental Housing.” NMHC.org. https://www.nmhc.org

[4] Federal Reserve Board. (2024). “Report on the Economic Well-Being of U.S. Households.” FederalReserve.gov. https://www.federalreserve.gov

[5] U.S. Census Bureau. (2024). “Median Gross Rent and Housing Costs.” Census.gov. https://www.census.gov

Frequently Asked Questions

Does the 3x rent rule use gross income or net income?

The 3x rent rule uses gross income (pre-tax earnings before any deductions). Landlords calculate based on total income shown on pay stubs or tax returns, not take-home pay. For example, if you earn $5,000 gross but net $3,800 after taxes, the calculation uses the $5,000 figure.

Is the 3x rent rule required by law?

No. The 3x rent rule is a voluntary screening standard used by landlords and property management companies. No federal or state law requires this specific income threshold. Landlords may set their own criteria as long as they apply them consistently and comply with Fair Housing laws.

Can landlords deny applications based on the 3x rent rule?

Yes. Landlords can legally deny rental applications if applicants fail to meet income requirements, provided the rule is applied uniformly to all applicants. Denials cannot be based on protected characteristics such as race, religion, disability, or familial status.

Does the 3x rent rule apply when renting with roommates?

This depends on the landlord’s policy. Some landlords evaluate combined household income, while others require each individual applicant to meet the 3x rent standard independently. Always confirm the policy before submitting an application.

What if I earn tips, bonuses, or overtime—does that count toward the 3x rule?

Yes, if the income is consistent and well-documented. Landlords typically require at least 12 months of history through tax returns, year-to-date pay stubs, or employer verification. One-time bonuses or irregular overtime usually do not count unless contractually guaranteed.

Can I use a co-signer if I don’t meet the 3x rent requirement?

Yes. Many landlords allow a co-signer or guarantor who agrees to cover rent if you default. Co-signers often must earn 5–6x the monthly rent and have strong credit. This option is common for students, recent graduates, or individuals with temporarily lower income.