Picture this: You’ve just delivered a product or service to a customer, sent them an invoice, and now you’re waiting for payment. That money they owe you? That’s accounts receivable in action. It’s the lifeblood of cash flow for countless businesses, yet it’s one of the most misunderstood aspects of financial management. Whether you’re an aspiring entrepreneur, a small business owner, or simply curious about how companies manage their money, understanding accounts receivable is absolutely essential for financial success.

In simple terms, accounts receivable means the money customers owe to a business for goods or services already delivered but not yet paid for. Think of it as an IOU from your customers; it’s an asset on your balance sheet, representing future cash that should flow into your business. Investopedia – Accounts Receivable

TL;DR

Accounts receivable (AR) is the money owed to a business by customers who purchased goods or services on credit—it’s listed as a current asset on the balance sheet.

Effective AR management directly impacts cash flow, working capital, and overall business health; delayed collections can strangle even profitable companies.

The accounts receivable turnover ratio measures how efficiently a company collects payments, calculated as Net Credit Sales ÷ Average Accounts Receivable.

Common AR challenges include late payments, bad debts, and cash flow gaps—but proper credit policies, invoicing systems, and collection strategies can minimize these risks.

Automation and technology are transforming AR management in 2025, making it easier for businesses to track, collect, and optimize their receivables.

What Is Accounts Receivable? The Complete Definition

Accounts receivable represent the outstanding invoices a company has or the money clients owe the company for goods or services rendered. In accounting terms, AR is classified as a current asset on the balance sheet because it’s expected to be converted into cash within one year (or one business cycle).

Here’s the key distinction: When a business sells something on credit—meaning the customer doesn’t pay immediately—the transaction creates an account receivable. The business has provided value but hasn’t received cash yet. This is different from a cash sale, where money changes hands immediately.

The Accounting Entry for Accounts Receivable

When a credit sale occurs, the accounting entry looks like this:

Debit: Accounts Receivable

Credit: Revenue (or Sales)

When the customer pays:

Debit: Cash

Credit: Accounts Receivable

This double-entry bookkeeping ensures that your financial statements accurately reflect both what you’ve earned (revenue) and what you’re owed (accounts receivable).

Why Accounts Receivable Matters

Understanding AR is crucial because:

It affects cash flow – Revenue on paper doesn’t pay bills; actual cash does

It represents working capital – Money tied up in AR can’t be used for operations

It impacts business valuation – Investors and lenders scrutinize AR quality

It reveals customer relationships – Payment patterns indicate customer satisfaction and reliability

Just as investors need to understand market dynamics and financial principles to make smart decisions, business owners must master accounts receivable to maintain healthy finances.

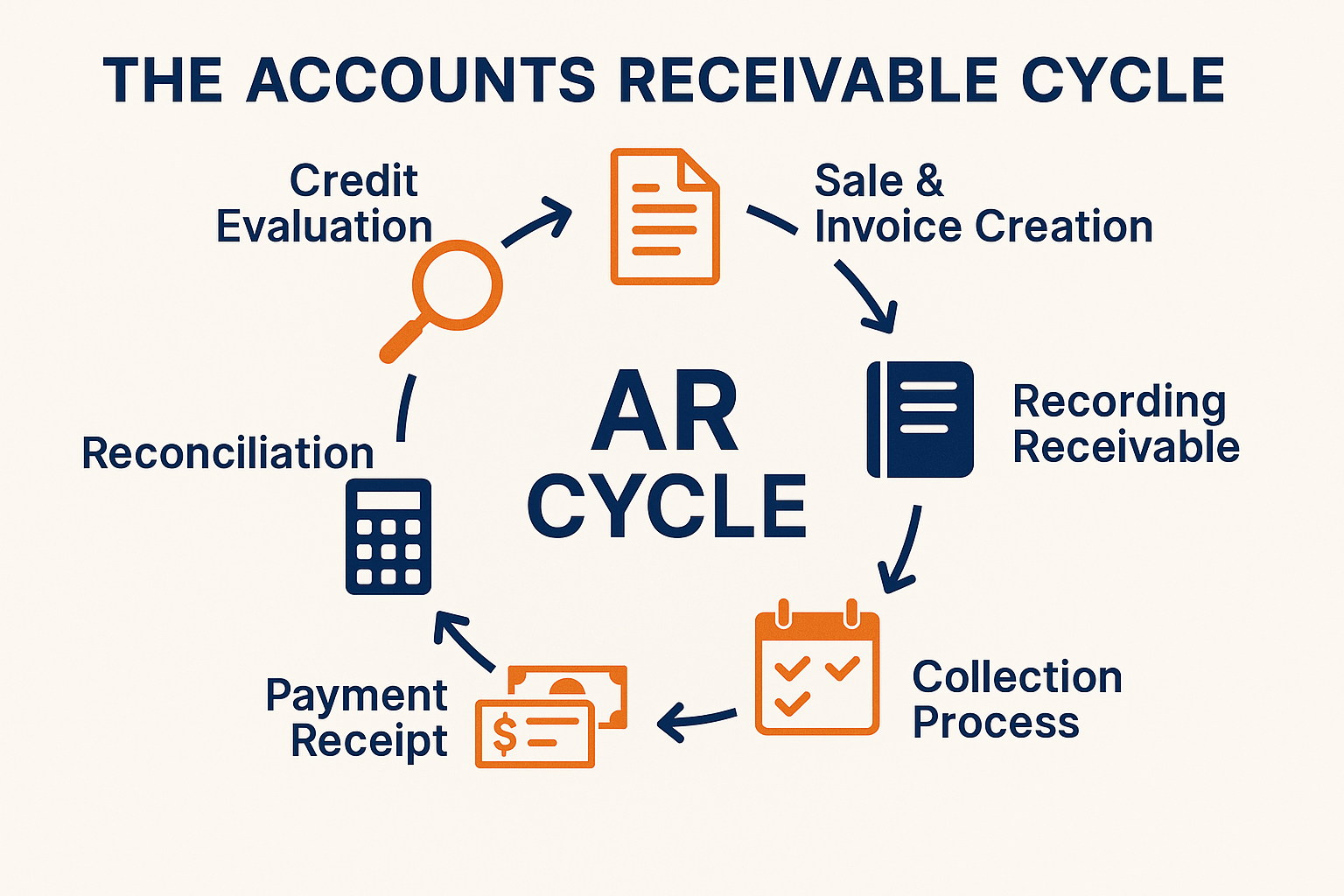

How Accounts Receivable Works: The Complete Cycle

The accounts receivable cycle (also called the credit-to-cash cycle) includes several distinct stages:

1. Credit Evaluation

Before extending credit, businesses should evaluate a customer’s creditworthiness. This might include:

- Checking credit scores and reports

- Reviewing payment history with other vendors

- Setting appropriate credit limits

- Establishing payment terms (Net 30, Net 60, etc.)

2. Sale and Invoice Creation

When a sale occurs on credit:

- The business delivers goods or services

- An invoice is generated with clear payment terms

- The invoice details the amount due, due date, and payment methods

- The transaction is recorded in the accounting system

3. Recording the Receivable

The accounting department records the transaction:

- AR increases (debit)

- Revenue increases (credit)

- The customer account is updated

4. Collection Process

The business actively manages collection through:

- Sending payment reminders before the due date

- Following up on overdue accounts

- Offering early payment discounts

- Escalating collection efforts for delinquent accounts

5. Payment Receipt

When payment arrives:

- Cash increases (debit)

- AR decreases (credit)

- The customer’s account balance is cleared

6. Reconciliation and Reporting

Regular AR management includes:

- Aging reports to track outstanding invoices

- Reconciliation with customer statements

- Analysis of collection efficiency

- Identification of bad debt risks

Real-World Examples of Accounts Receivable

Let’s look at practical examples across different industries:

Example 1: Retail Supplier (B2B)

Scenario: ABC Wholesale supplies inventory to retail stores.

- January 5: ABC ships $50,000 worth of products to Retail Store XYZ with Net 30 terms

- January 5: ABC records a $50,000 accounts receivable

- February 4: Retail Store XYZ pays the $50,000

- February 4: ABC converts the receivable to cash

Impact: For 30 days, ABC had $50,000 tied up in AR, affecting their working capital.

Example 2: Freelance Consultant (Services)

Scenario: Sarah is a marketing consultant.

- March 1: Sarah completes a $5,000 project for a client

- March 1: Sarah sends an invoice with Net 15 terms

- March 1: Sarah records $5,000 in accounts receivable

- March 16: Client pays $5,000

- March 16: Sarah’s AR decreases, cash increases

Impact: Sarah’s cash flow depends on timely collection—delayed payments could prevent her from paying her own bills.

Example 3: Manufacturing Company

Scenario: TechParts Manufacturing produces components.

- Quarter 1: TechParts ships $2 million in parts to various customers

- Average payment terms: Net 45

- Collection rate: 95% within 60 days, 5% requires additional follow-up

- End of Quarter 1: AR balance shows $1.8 million outstanding

Impact: TechParts must carefully manage this $1.8 million in AR to ensure sufficient cash flow for operations, payroll, and inventory purchases.

Example 4: Software-as-a-Service (SaaS) Company

Scenario: CloudSoft charges annual subscriptions.

- January 1: Customer signs a $12,000 annual contract

- January 1: CloudSoft invoices the full amount with Net 30 terms

- January 1: CloudSoft records $12,000 AR (but recognizes revenue monthly)

- January 30: Customer pays $12,000

- January 30: AR is cleared

Impact: Even though CloudSoft received $12,000 cash, they must recognize revenue over 12 months ($1,000/month) according to accounting standards.

The Accounts Receivable Formula and Key Metrics

Basic AR Balance

The accounts receivable balance at any point equals:

Beginning AR + Credit Sales – Collections – Write-offs = Ending AR

Accounts Receivable Turnover Ratio

This critical metric measures how efficiently a company collects its receivables.

Formula:

AR Turnover Ratio = Net Credit Sales ÷ Average Accounts Receivable

Where:

- Net Credit Sales = Total credit sales minus returns and allowances

- Average Accounts Receivable = (Beginning AR + Ending AR) ÷ 2

Example:

- Annual credit sales: $1,200,000

- Beginning AR: $150,000

- Ending AR: $170,000

- Average AR: ($150,000 + $170,000) ÷ 2 = $160,000

AR Turnover = $1,200,000 ÷ $160,000 = 7.5 times per year

Interpretation: A higher turnover ratio usually indicates efficient collection and quality receivables. The company collects its average receivables 7.5 times annually.

Days Sales Outstanding (DSO)

DSO indicates the average number of days it takes to collect payment.

Formula:

DSO = (Accounts Receivable ÷ Net Credit Sales) × Number of Days

Or alternatively:

DSO = 365 ÷ AR Turnover Ratio

Using our previous example:

DSO = 365 ÷ 7.5 = 48.7 days

Interpretation: On average, it takes about 49 days to collect payment after a sale. Compare this to your payment terms (e.g., Net 30) to assess collection efficiency.

Collection Effectiveness Index (CEI)

This metric measures the effectiveness of collection efforts.

Formula:

CEI = [(Beginning AR + Credit Sales – Ending AR) ÷ (Beginning AR + Credit Sales – Current AR)] × 100

A CEI of 100% means perfect collection; anything above 70% is generally considered good. FASB – Accounting Standards

Accounts Receivable vs Accounts Payable: Understanding the Difference

| Aspect | Accounts Receivable (AR) | Accounts Payable (AP) |

|---|---|---|

| Definition | Money customers owe you | Money you owe suppliers |

| Classification | Current Asset | Current Liability |

| Impact on Cash | Future cash inflow | Future cash outflow |

| Goal | Collect quickly | Pay strategically (not too early, not too late) |

| Affects | Revenue recognition | Expense recognition |

| Management Focus | Credit policies, collection | Payment terms, vendor relationships |

Key Insight: Successful businesses manage both sides of this equation. Just as you want customers to pay quickly Accounts Receivable(AR), suppliers want you to pay promptly for Accounts Payable(AP). Balancing both optimizes cash flow and maintains healthy business relationships. See our full guide on Accounts Receivable vs Accounts Payable.

Understanding financial flows is similar to grasping how market emotions affect investment decisions—both require strategic thinking and emotional discipline.

The Accounts Receivable Aging Report: Your Collection Roadmap

An AR aging report (or aging schedule) categorizes outstanding receivables by how long they’ve been unpaid. This is one of the most powerful tools for AR management.

Sample AR Aging Report

| Customer | Current (0-30 days) | 31-60 days | 61-90 days | Over 90 days | Total AR |

|---|---|---|---|---|---|

| Customer A | $5,000 | $2,000 | $0 | $0 | $7,000 |

| Customer B | $3,000 | $0 | $1,500 | $500 | $5,000 |

| Customer C | $10,000 | $0 | $0 | $0 | $10,000 |

| Customer D | $0 | $4,000 | $2,000 | $3,000 | $9,000 |

| Total | $18,000 | $6,000 | $3,500 | $3,500 | $31,000 |

| % of Total | 58% | 19% | 11% | 11% | 100% |

How to Use the Aging Report

Identify problem accounts – Customer D has $5,000 over 60 days old (red flag)

Prioritize collection efforts – Focus on older receivables first

Assess bad debt risk – Receivables over 90 days have higher default risk

Evaluate credit policies – High percentages in older categories suggest policy problems

Forecast cash flow – Current receivables are more likely to convert to cash soon

Best Practice: Review your AR aging report weekly or at a minimum monthly. The older a receivable gets, the less likely you’ll collect it.

Advantages and Limitations of Accounts Receivable

Advantages

1. Competitive Advantage

Offering credit terms attracts customers who can’t or prefer not to pay immediately. Many B2B transactions require credit to remain competitive.

2. Increased Sales

Credit sales typically generate higher revenue than cash-only policies. Customers buy more when they can pay later.

3. Customer Loyalty

Flexible payment terms build stronger customer relationships and repeat business.

4. Asset Value

AR represents a tangible asset that can be used as collateral for loans or sold (factored) for immediate cash.

5. Revenue Recognition

Under accrual accounting, AR allows businesses to recognize revenue when earned, not just when cash is received, providing a clearer picture of business performance.

Limitations and Risks

1. Cash Flow Strain

High AR means cash is tied up, potentially creating liquidity problems. You might be profitable on paper, but unable to pay bills.

2. Bad Debt Risk

Some customers will never pay. According to industry data, typical bad debt rates range from 1-3% of credit sales, but can be much higher in certain industries.

3. Collection Costs

Managing AR requires time, staff, systems, and sometimes legal action—all of which cost money.

4. Opportunity Cost

Money tied up in AR can’t be invested elsewhere. This is similar to how passive income strategies require initial capital deployment.

5. Administrative Burden

Tracking invoices, following up with customers, reconciling payments, and managing disputes requires significant resources.

6. Customer Relationship Strain

Aggressive collection tactics can damage relationships with valuable customers.

How to Manage Accounts Receivable Effectively

Effective AR management is crucial for business survival and growth. Here are proven strategies:

1. Establish Clear Credit Policies

Before extending credit:

- Conduct credit checks on new customers

- Set appropriate credit limits based on risk assessment

- Define clear payment terms (Net 15, Net 30, etc.)

- Document policies in writing

- Require credit applications for larger accounts

Example Credit Policy Components:

- Maximum credit limit: $10,000 for new customers

- Payment terms: Net 30 for established customers, prepayment for new customers

- Late payment penalty: 1.5% per month on overdue balances

- Credit review: Annual review of all accounts over $5,000

2. Invoice Promptly and Accurately

Best practices:

- Send invoices immediately after delivery

- Include all necessary details (invoice number, date, itemized charges, payment terms, due date)

- Provide multiple payment options (check, ACH, credit card, online portal)

- Use professional, clear invoice templates

- Ensure accuracy to avoid disputes that delay payment

Pro Tip: Invoices sent within 24 hours of delivery are paid 30% faster on average than those sent after a week.

3. Offer Early Payment Incentives

Discount terms encourage faster payment:

- 2/10 Net 30 – 2% discount if paid within 10 days, full amount due in 30 days

- 1/15 Net 45 – 1% discount if paid within 15 days, full amount due in 45 days

Example:

- Invoice amount: $10,000

- Terms: 2/10 Net 30

- If paid in 10 days: Customer pays $9,800

- If paid in 30 days: Customer pays $10,000

Analysis: You’re essentially paying $200 to get your money 20 days earlier. The annualized cost of this discount is approximately 36%, but it may be worth it for improved cash flow.

4. Implement Systematic Follow-Up

Collection timeline:

- Day 0 (Invoice sent): Send invoice with payment instructions

- Day 7: Send a friendly reminder email

- Day 20: Send second reminder (10 days before due date)

- Day 30 (Due date): Send payment due notice

- Day 35: Phone call to customer

- Day 45: Formal collection letter

- Day 60: Final notice before escalation

- Day 75: Consider a collection agency or legal action

Communication Best Practices:

- Start friendly and become firmer over time

- Always maintain professionalism

- Document all communication

- Offer payment plans when appropriate

5. Use Technology and Automation

Modern AR software can:

- Automate invoice generation and delivery

- Send automatic payment reminders

- Provide real-time AR dashboards

- Generate aging reports instantly

- Integrate with accounting systems

- Accept online payments

- Track collection activities

- Predict payment patterns using AI

Popular AR Management Tools (2025):

- QuickBooks Online

- FreshBooks

- Zoho Books

- Bill.com

- Stripe Billing

- Fundbox

6. Monitor Key Metrics Regularly

Track these metrics monthly:

- AR Turnover Ratio – Are collections improving or declining?

- Days Sales Outstanding (DSO) – Is the collection period lengthening?

- Collection Effectiveness Index – How effective are collection efforts?

- Bad Debt Percentage – What percentage of sales becomes uncollectible?

- AR Aging Distribution – What percentage falls in each aging bucket?

7. Address Disputes Quickly

Payment disputes are a major cause of delayed collections:

- Investigate disputes immediately

- Communicate with customers to understand issues

- Resolve legitimate problems quickly

- Separate disputed amounts from undisputed amounts

- Request payment of undisputed portions while resolving issues

8. Know When to Write Off Bad Debt

Despite best efforts, some receivables become uncollectible:

Indicators of uncollectible debt:

- Customer declares bankruptcy

- The customer goes out of business

- The receivable is over 120-180 days old with no response

- Collection costs exceed the receivable amount

- Legal action is unsuccessful

Accounting entry for write-off:

Debit: Bad Debt Expense

Credit: Accounts Receivable

This removes the uncollectible amount from AR and recognizes the loss.

Accounts Receivable Financing: Converting AR to Cash

When businesses need immediate cash, they can leverage their accounts receivable through various financing methods:

1. AR Factoring

How it works:

- You sell your invoices to a factoring company at a discount

- The factor pays you 70-90% immediately

- The factor collects payment from your customer

- You receive the remaining balance minus fees (typically 1-5%)

Example:

- Invoice value: $100,000

- Advance rate: 80%

- Factor fee: 3%

- You receive immediately: $80,000

- Customer pays factor: $100,000

- You receive later: $17,000 (remaining 20% minus $3,000 fee)

- Total received: $97,000

Pros: Quick cash, factor handles collections

Cons: Expensive, customers know you factored (may signal financial distress)

2. AR Financing (Asset-Based Lending)

How it works:

- You borrow money using AR as collateral

- You retain ownership of receivables

- You handle collections

- Repay the loan as customers pay

Example:

- AR balance: $500,000

- Loan-to-value: 80%

- You can borrow: $400,000

- Interest rate: 8-12% annually

Pros: Less expensive than factoring, you maintain customer relationships

Cons: You’re responsible for collections, which requires ongoing reporting

3. Invoice Discounting

Similar to factoring, but:

- Your customers don’t know you’ve borrowed against receivables

- You maintain collection responsibility

- Typically used by larger, more established businesses

Common Accounts Receivable Mistakes to Avoid

1: No Credit Policy

Problem: Extending credit to anyone without evaluation

Solution: Implement a formal credit approval process

2: Inconsistent Follow-Up

Problem: Only contacting customers when you need cash

Solution: Systematic, scheduled collection of communications

3: Poor Invoice Practices

Problem: Delayed, incomplete, or inaccurate invoices

Solution: Automated, immediate, detailed invoicing

4: Ignoring Aging Reports

Problem: Not reviewing AR aging regularly

Solution: Weekly or monthly aging report reviews with action plans

5: Being Too Lenient

Problem: Allowing customers to consistently pay late without consequences

Solution: Enforce late fees, adjust credit terms, or require prepayment

6: No Documentation

Problem: Verbal agreements without written confirmation

Solution: Document all terms, communications, and agreements

7: Waiting Too Long to Act

Problem: Letting receivables age beyond 90 days before escalating

Solution: Progressive collection process with a clear escalation timeline

Just as avoiding common investment mistakes is crucial for financial success, avoiding AR management errors protects business cash flow.

Accounts Receivable in Different Business Types

Small Businesses and Startups

Challenges:

- Limited resources for credit checking

- Cash flow sensitivity

- Personal relationships with customers make collections awkward

Strategies:

- Start with stricter terms (Net 15 or prepayment)

- Use simple AR software

- Offer discounts for immediate payment

- Consider requiring deposits for large orders

Medium-Sized Businesses

Challenges:

- A growing customer base requires more sophisticated systems

- Balancing growth with cash flow

- Need for dedicated AR staff

Strategies:

- Implement comprehensive AR software

- Hire a dedicated collections specialist

- Develop tiered credit policies

- Regular AR metrics reporting

Large Enterprises

Challenges:

- Managing thousands of customer accounts

- Complex payment terms and contracts

- International transactions with currency issues

Strategies:

- Enterprise AR management systems

- Dedicated AR department

- Automated workflows and AI-powered predictions

- Global payment processing capabilities

Service Businesses

Unique considerations:

- No physical product to repossess

- Revenue recognition can be complex (especially for long-term contracts)

- Progress billing for long projects

Best practices:

- Milestone-based invoicing

- Retainer agreements

- Clear scope documentation to prevent disputes

Product-Based Businesses

Unique considerations:

- Inventory management tied to AR

- Potential for returns affecting AR

- Seasonal fluctuations

Best practices:

- Align inventory purchases with expected collections

- Clear return policies

- Seasonal credit term adjustments

The Impact of Accounts Receivable on Financial Statements

Balance Sheet Impact

Assets Section:

Current Assets:

Cash: $50,000

Accounts Receivable: $75,000

Less: Allowance for Doubtful Accounts: ($3,000)

Net Accounts Receivable: $72,000

Inventory: $40,000

Total Current Assets: $162,000Key points:

- AR is listed as a current asset

- The allowance for doubtful accounts reduces AR to its net realizable value

- High AR relative to cash can signal liquidity issues

Income Statement Impact

Revenue Recognition:

Revenue: $500,000

Less: Sales Returns and Allowances: ($10,000)

Net Revenue: $490,000

Operating Expenses:

Bad Debt Expense: $5,000Key points:

- Revenue is recognized when earned (accrual basis), creating AR

- Bad debt expense represents estimated uncollectible receivables

- This expense reduces net income

Cash Flow Statement Impact

Operating Activities Section:

Net Income: $50,000

Adjustments:

Increase in Accounts Receivable: ($20,000)

Bad Debt Expense: $5,000

Cash from Operating Activities: $35,000Key points:

- An increase in AR reduces cash from operations (cash not yet received)

- A decrease in AR increases cash from operations (collections)

- This is why profitable companies can still have cash flow problems

Understanding these financial statement relationships is as important as understanding how different factors move markets when analyzing investments.

Technology Trends in Accounts Receivable Management (2025)

1. Artificial Intelligence and Machine Learning

Applications:

- Predicting which customers will pay late

- Optimizing collection strategies for different customer segments

- Automating invoice matching and reconciliation

- Detecting fraud and duplicate payments

Example: AI can analyze payment patterns and alert you that Customer X, who usually pays in 30 days, is likely to pay late this month based on recent behavior changes.

2. Blockchain for AR

Benefits:

- Immutable transaction records

- Smart contracts that auto-execute payment terms

- Reduced dispute resolution time

- Enhanced transparency in B2B transactions

3. Automated Payment Reminders

Features:

- Personalized reminder schedules based on customer behavior

- Multi-channel reminders (email, SMS, phone)

- Automatic escalation for overdue accounts

- Integration with customer communication preferences

4. Real-Time AR Dashboards

Capabilities:

- Live AR balance and aging

- Collection performance metrics

- Customer payment trends

- Cash flow forecasting

- Mobile access for on-the-go management

5. Electronic Invoicing and Payment

Advantages:

- Instant invoice delivery

- Multiple payment options (ACH, credit card, digital wallets)

- Automatic payment confirmation

- Reduced manual processing

- Lower costs compared to paper invoicing

Statistics: Electronic invoices are paid 2-3 times faster than paper invoices on average.

6. Integration with ERP and CRM Systems

Benefits:

- Unified customer view (sales, service, and payment history)

- Automated workflows from sale to collection

- Better customer segmentation

- Improved forecasting

Accounts Receivable Best Practices Checklist

Use this checklist to optimize your AR management:

Before the Sale ✓

- [ ] Credit policy is documented and current

- [ ] New customer credit check completed

- [ ] Credit limit established

- [ ] Payment terms clearly communicated

- [ ] Customer has signed the credit agreement

At the Time of Sale ✓

- [ ] Invoice created immediately

- [ ] All invoice details are accurate

- [ ] Payment terms clearly stated

- [ ] Multiple payment options provided

- [ ] Invoice sent within 24 hours

During the Collection Period ✓

- [ ] Payment reminders scheduled

- [ ] AR aging report reviewed weekly/monthly

- [ ] Key metrics tracked and analyzed

- [ ] Overdue accounts contacted promptly

- [ ] Disputes addressed immediately

Ongoing Management ✓

- [ ] AR software is up-to-date

- [ ] Staff trained on collection procedures

- [ ] Customer payment patterns analyzed

- [ ] Credit policies reviewed annually

- [ ] Bad debt provisions are adequate

Escalation Procedures ✓

- [ ] Clear escalation timeline defined

- [ ] Collection agency relationships established

- [ ] Legal resources identified

- [ ] Write-off procedures documented

- [ ] Lessons learned incorporated into policy

📊 AR Performance Calculator

Calculate Days Sales Outstanding (DSO) and AR Turnover Ratio

Total credit sales for the year (exclude cash sales)

AR balance at the start of the period

AR balance at the end of the period

Typical credit terms you offer (e.g., Net 30 = 30 days)

Your AR Performance Metrics

Real-World Case Study: AR Management Transformation

Company Background

TechSupply Inc. is a mid-sized distributor of technology components with annual revenue of $15 million.

The Problem (2023)

- Average DSO: 68 days (payment terms: Net 30)

- AR Turnover: 5.4x annually

- Bad debt rate: 4.2% of sales

- Cash flow: Consistently tight, requiring a line of credit

- Collection process: Manual, inconsistent follow-up

The Transformation (2024)

Step 1: Credit Policy Overhaul

- Implemented formal credit application for all new customers

- Established tiered credit limits based on credit scores

- Required prepayment for customers with poor payment history

Step 2: Technology Implementation

- Adopted cloud-based AR management software

- Automated invoice delivery and payment reminders

- Integrated online payment portal

Step 3: Process Improvements

- Hired a dedicated collections specialist

- Created a systematic follow-up schedule

- Implemented early payment discount (2/10 Net 30)

- Weekly AR aging report reviews with action plans

Step 4: Customer Communication

- Sent friendly payment reminders 7 days before the due date

- Made courtesy calls on day 35 for overdue accounts

- Offered payment plans for customers experiencing difficulties

The Results (2025)

- Average DSO: 42 days (38% improvement)

- AR Turnover: 8.7x annually (61% improvement)

- Bad debt rate: 1.8% of sales (57% reduction)

- Cash flow: Eliminated the need for a credit line

- Customer satisfaction: Improved (clearer communication)

Financial Impact:

- Freed up approximately $850,000 in working capital

- Reduced bad debt expense by $360,000 annually

- Eliminated $45,000 in annual credit line interest

- Total annual benefit: ~$450,000+

Key Takeaway: Strategic AR management isn’t just about collecting money—it’s about optimizing the entire credit-to-cash cycle to improve financial health and business relationships. SEC – Understanding Financial Statements

Accounts Receivable and Your Personal Finances

While AR is primarily a business concept, the principles apply to personal financial management:

Personal “Accounts Receivable”

Examples:

- Money, friends, or family owe you

- Security deposits you’ll get back

- Tax refunds owed to you

- Insurance claim payments

- Freelance work invoiced but not paid

Lessons from AR for Personal Finance

1. Document Everything

Just as businesses document credit sales, they document personal loans with written agreements specifying amounts and repayment terms.

2. Follow Up Systematically

Don’t be afraid to send polite reminders about money owed to you—it’s your money.

3. Consider the Opportunity Cost

Money owed to you is money you can’t invest. This is similar to how passive income strategies require available capital.

4. Know When to Write It Off

Sometimes, pursuing a small amount costs more (in time and relationship damage) than it’s worth. Know when to let it go.

5. Be Strategic About “Credit Terms”

If lending money to others, consider requiring partial upfront payment or setting clear, short repayment periods.

The Connection Between AR and Investment Analysis

For investors evaluating companies, accounts receivable provides valuable insights:

What to Look For

1. AR Turnover Trends

Declining turnover may indicate:

- Weakening sales quality

- Customer financial problems

- Aggressive revenue recognition

- Collection difficulties

2. AR Growth vs. Revenue Growth

If AR grows faster than revenue, it suggests:

- Longer collection periods

- Potential revenue quality issues

- Possible channel stuffing (forcing sales)

3. Days Sales Outstanding

Compare DSO to:

- The company’s stated payment terms

- Industry averages

- Historical company performance

- Competitors’ DSO

4. Allowance for Doubtful Accounts

- Is it adequate based on AR aging?

- Has it changed significantly?

- Compared to industry norms

5. AR Concentration

- Are receivables concentrated in a few customers?

- What’s the risk if a major customer defaults?

Red Flags for Investors

Rapidly increasing AR relative to sales

Declining AR turnover over multiple quarters

Inadequate allowance for doubtful accounts

High concentration in a few customers

Frequent changes in accounting policies related to AR

Understanding these metrics helps investors make informed decisions, similar to understanding why stocks move and market fundamentals.

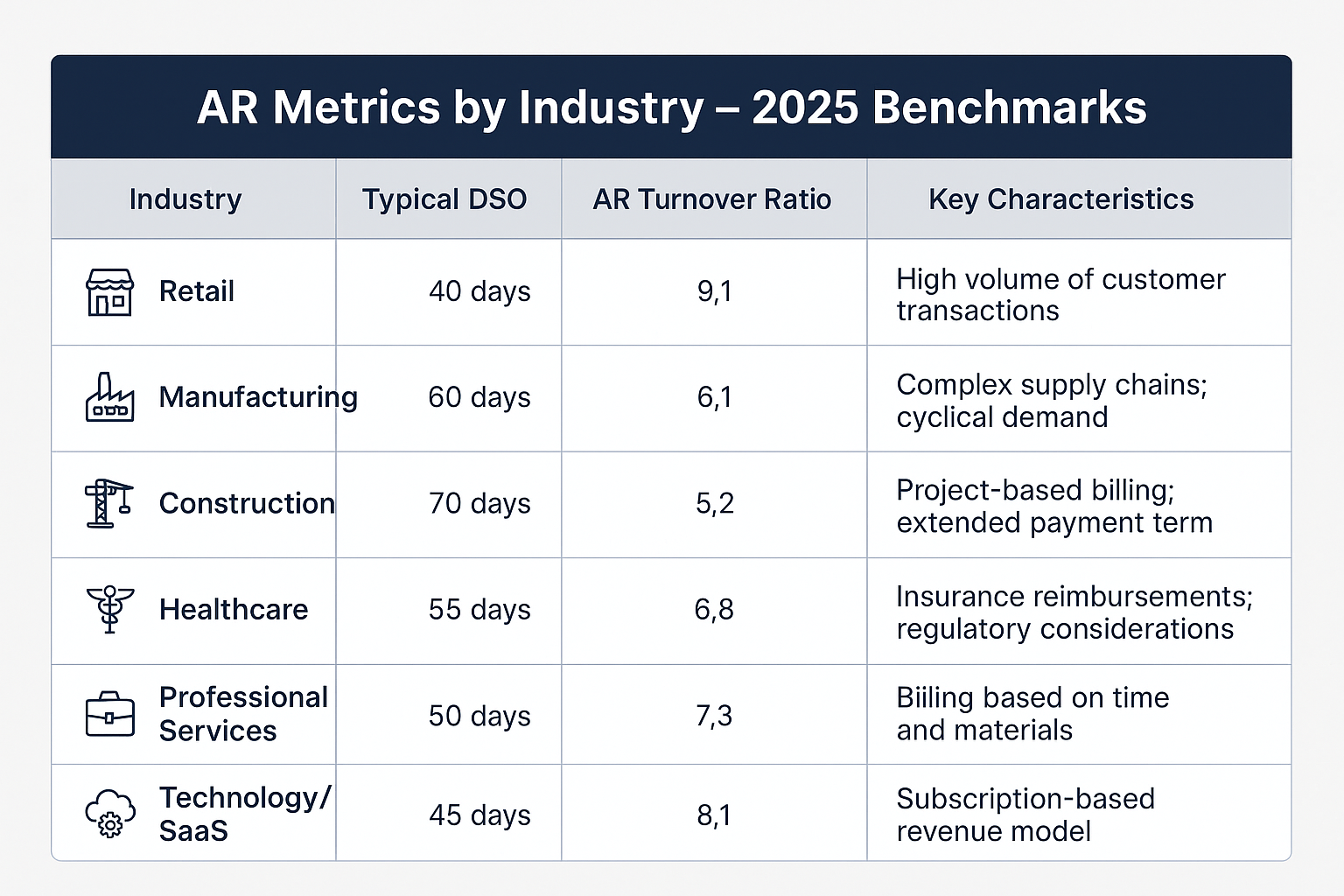

Industry-Specific AR Benchmarks

Different industries have vastly different AR characteristics:

| Industry | Typical DSO | Typical AR Turnover | Notes |

|---|---|---|---|

| Retail | 5-15 days | 24-73x | Mostly cash/credit card sales |

| Manufacturing | 45-60 days | 6-8x | B2B sales with standard terms |

| Construction | 60-90 days | 4-6x | Project-based, progress billing |

| Healthcare | 45-70 days | 5-8x | Insurance reimbursement delays |

| Professional Services | 30-60 days | 6-12x | Varies by service type |

| Wholesale/Distribution | 35-50 days | 7-10x | B2B with competitive terms |

| Technology/SaaS | 30-45 days | 8-12x | Subscription models improving |

Important: Always compare your metrics to your specific industry and company size, not universal benchmarks.

The Future of Accounts Receivable Management

Emerging Trends

1. Embedded Finance

AR management is integrated directly into sales and ERP platforms, creating seamless workflows from quote to collection.

2. Predictive Analytics

AI predicts payment dates with high accuracy, allowing better cash flow forecasting and proactive collection strategies.

3. Instant Payments

Real-time payment networks (like FedNow in the US) enable instant B2B payments, potentially reducing DSO to near-zero.

4. Tokenization and Digital Assets

AR is represented as digital tokens that can be easily traded, sold, or used as collateral in decentralized finance (DeFi) platforms.

5. Automated Dispute Resolution

AI-powered systems automatically identify, categorize, and resolve common invoice disputes without human intervention.

6. Dynamic Discounting

Flexible early payment discounts that adjust based on the payer’s cash position and the seller’s working capital needs.

Skills for AR Professionals in 2025

To succeed in AR management, develop:

- Data analytics – Understanding metrics and trends

- Technology proficiency – Working with modern AR software

- Communication skills – Professional, effective collection conversations

- Negotiation abilities – Structuring payment plans and resolving disputes

- Financial acumen – Understanding cash flow and working capital

- Customer service mindset – Balancing collection with relationship management

Conclusion: Mastering Accounts Receivable for Business Success

Accounts receivable isn’t just an accounting concept—it’s a critical driver of business success that directly impacts cash flow, growth potential, and financial stability. In simple terms, accounts receivable means the money customers owe you for goods or services already delivered—and how well you manage it can make or break your business.

Key Principles to Remember

Revenue isn’t cash – Profitable on paper doesn’t mean liquid in reality

Speed matters – The faster you collect, the healthier your cash flow

Prevention beats cure – Strong credit policies prevent collection problems

Measurement drives improvement – Track DSO, turnover, and aging religiously

Technology is your friend – Automation dramatically improves efficiency

Balance is essential – Strict enough to get paid, flexible enough to retain customers

Your Action Plan: Next Steps

Whether you’re a business owner, financial professional, or aspiring entrepreneur, here’s what to do next:

Step 1: Assess Your Current State

- Calculate your current DSO and AR turnover

- Review your AR aging report

- Identify your biggest collection challenges

Step 2: Establish or Update Policies

- Document clear credit policies

- Define payment terms and conditions

- Create systematic collection procedures

Step 3: Implement Technology

- Research AR management software appropriate for your size

- Automate invoice delivery and payment reminders

- Set up online payment options

Step 4: Train Your Team

- Ensure everyone understands the importance

- Train staff on collection best practices

- Establish accountability for AR metrics

Step 5: Monitor and Optimize

- Review AR metrics monthly

- Compare to industry benchmarks

- Continuously refine processes based on data

Step 6: Learn Continuously

Stay informed about financial management principles through resources like smart financial strategies, and continue building your business acumen.

The Bottom Line

Effective accounts receivable management transforms paper profits into actual cash, enabling you to pay bills, invest in growth, and build a sustainable business. It requires attention, discipline, and the right systems—but the payoff in improved cash flow, reduced bad debts, and stronger customer relationships is absolutely worth it.

Remember: Every dollar in accounts receivable is a dollar you’ve earned but can’t yet spend. The faster you convert those receivables to cash, the more financial flexibility and growth potential you create.

Start implementing these AR best practices today, and watch your cash flow—and your business—thrive in 2025 and beyond.

FAQ: Accounts Receivable

A good AR turnover ratio varies by industry, but generally, a ratio between 7 and 10 is considered healthy for most businesses. This means the company collects its average receivables 7-10 times per year. Higher ratios indicate efficient collection, while lower ratios may signal collection problems or overly generous credit terms. Always compare your ratio to industry benchmarks for meaningful analysis.

The allowance for doubtful accounts estimates uncollectible receivables. Two common methods are: (1) Percentage of sales method – apply a historical bad debt percentage to current credit sales (e.g., if 2% historically default, allowance = credit sales × 2%), and (2) Aging method – apply increasing percentages to older receivables (e.g., 1% for current, 5% for 31-60 days, 20% for 61-90 days, 50% for over 90 days). The aging method is generally more accurate

Accounts receivable are definitely current assets on the balance sheet. It represents money owed to the company, which is a resource with future economic value. The opposite—money the company owes to others—is accounts payable, which is a current liability. This distinction is fundamental to understanding financial statements.

When a customer pays their invoice, the accounts receivable balance decreases, and cash increases by the same amount. The accounting entry is: Debit Cash, Credit Accounts Receivable. This converts the receivable asset into cash, improving the company’s liquidity. The customer’s individual account balance also goes to zero.

Yes, accounts receivable can be sold through a process called factoring. A factoring company purchases your invoices at a discount (typically 70-97% of face value) and assumes responsibility for collection. This provides immediate cash but at a cost. Alternatively, AR can be used as collateral for asset-based loans, where you retain ownership while borrowing against the receivables.

Accounts receivable arise from normal business operations (selling goods/services on credit) and are typically due within 30-90 days with no formal written agreement. Notes receivable are formal written promises to pay a specific amount by a specific date, often with interest, typically for longer periods (over 90 days). Notes receivable are more legally binding and often involve larger amounts.

Accounts receivable directly impacts cash flow because it represents revenue earned but cash not yet received. When AR increases, cash flow from operations decreases (even if net income is high) because more money is tied up in receivables. When AR decreases (collections exceed new credit sales), cash flow improves. This is why profitable companies can still face cash shortages—high AR means “paper profits” without actual cash.

Disclaimer

This article is for educational purposes only and does not constitute financial, accounting, or legal advice. Accounts receivable management practices should be tailored to your specific business circumstances, industry, and jurisdiction. Consult with qualified accounting professionals, financial advisors, and legal counsel before implementing significant changes to credit policies or collection practices. Tax treatment of accounts receivable and bad debt varies by location and business structure—seek professional tax advice for your situation.

About the Author

Written by Max Fonji — with a decade of experience in financial education and business strategy, Max is your go-to source for clear, data-backed insights on personal finance, investing, and business management. Through TheRichGuyMath.com, Max helps thousands of readers build wealth through informed financial decisions and smart business practices. Learn more about building wealth through dividend investing and other proven strategies on our blog.

Related posts:

What Is SmartPass? Raptor Digital Hall Pass Explained for K-12 Schools

What Is SmartPass? Raptor Digital Hall Pass Explained for K-12 Schools

What Is the 3x Rent Rule & How to Calculate It (With Examples)

What Is the 3x Rent Rule & How to Calculate It (With Examples)

Types of Income: A Complete Guide to Earning and Growing Wealth

Types of Income: A Complete Guide to Earning and Growing Wealth

Tax Filing: A Clear, Step-by-Step Guide for Stress-Free Taxes

Tax Filing: A Clear, Step-by-Step Guide for Stress-Free Taxes

Return on Assets (ROA): Definition, Formula & How to Improve It

Return on Assets (ROA): Definition, Formula & How to Improve It

How to Save Money Fast: A Smart Savings Plan That Actually Works

How to Save Money Fast: A Smart Savings Plan That Actually Works