Picture this: It’s Monday morning, and your alarm blares at 6:30 AM. You drag yourself out of bed, shower, grab coffee, and head to work. Eight hours later, you clock out and head home. Two weeks later, a paycheck hits your bank account. That, my friend, is active income in action, the most common way people earn money, yet one of the least understood concepts in personal finance.

Here’s the thing: 95% of Americans rely primarily on active income to pay their bills, fund their dreams, and build their lives. But what exactly is it? How does it differ from passive income? And most importantly, how can you maximize what you’re earning right now while setting yourself up for financial freedom down the road?

Whether you’re punching a time clock, running a small business, or freelancing from your couch, understanding active income is the first step toward taking control of your financial future. Let’s dive in.

Key Takeaways

- Active income requires your direct time and effort to generate money, think salaries, hourly wages, commissions, and freelance work

- You trade time for money with active income, meaning your earning potential is limited by the hours in a day

- Most people start with active income before transitioning to passive income streams for long-term wealth building

- You can increase active income through skill development, negotiation, side hustles, and career advancement

- Active income is taxed at higher rates than passive income in most tax systems, making tax strategy important

What Is Active Income? The Complete Definition

Active income is money you earn in direct exchange for your time, labor, skills, or services. It’s called “active” because you must actively participate in the work to receive payment. The moment you stop working, the income stops flowing. As Investopedia explains, passive income typically comes from investments or ventures that require minimal ongoing effort after the initial setup.

Think of it like a water faucet, when you turn it on (work), water flows (money comes in). When you turn it off (stop working), the water stops. Simple, right?

The Core Characteristics of Active Income

Active income has several defining features:

- Direct time-for-money exchange – You work an hour, you get paid for an hour

- Immediate participation required – Someone else can’t easily do the work for you

- Linear earning potential – More hours = more money, but there’s a ceiling

- Stops when you stop – No work = no paycheck

- Primary income source – For most people, this is their main financial lifeline

According to the Bureau of Labor Statistics, the median weekly earnings for full-time wage and salary workers in the United States were $1,145 in the fourth quarter of 2024, all active income.

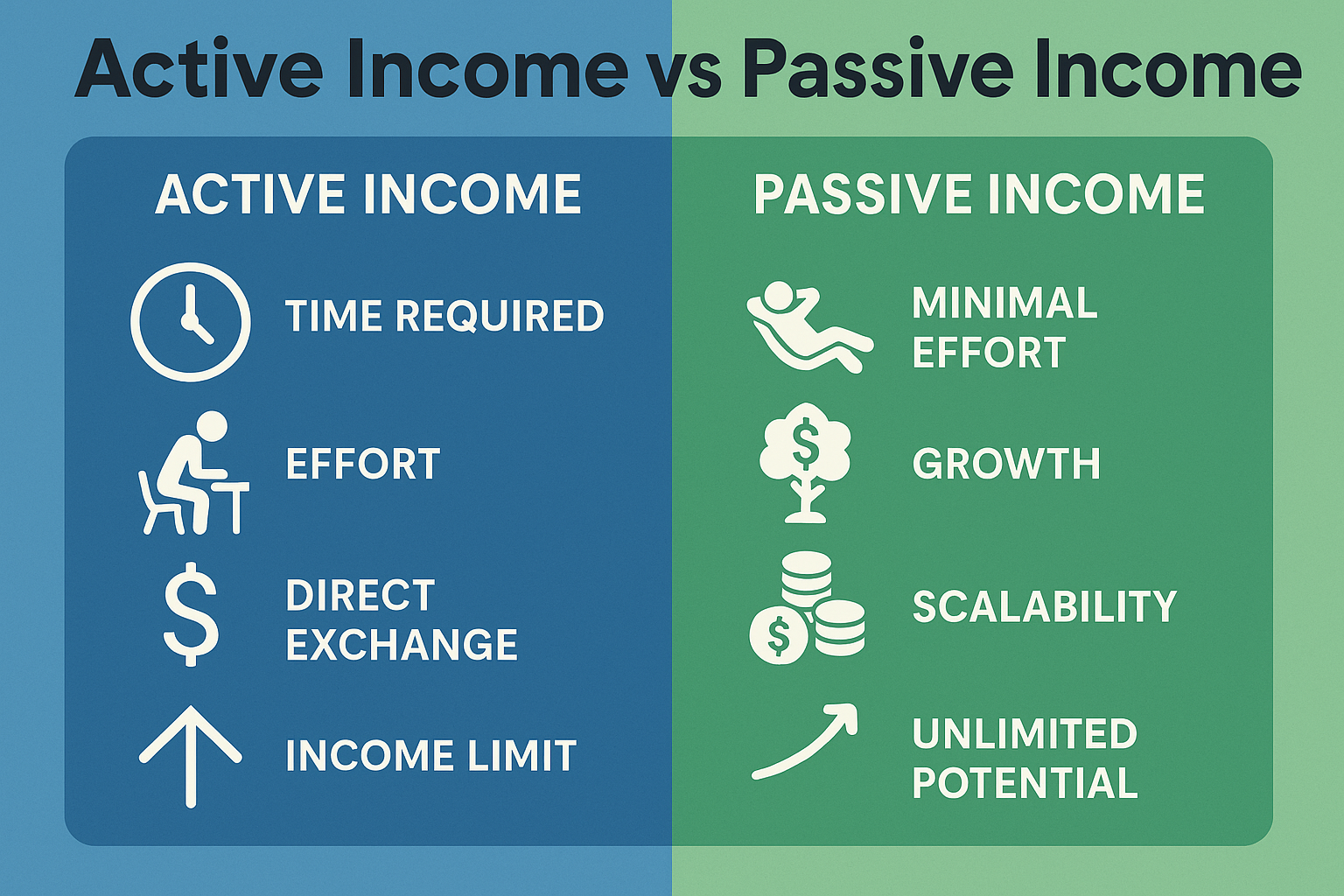

Active Income vs Passive Income: What’s the Difference?

The distinction between active and passive income is crucial for anyone serious about building wealth. Here’s how they stack up Active vs Passive Income:

| Feature | Active Income | Passive Income |

|---|---|---|

| Effort Required | Continuous, direct involvement | Upfront work, then minimal maintenance |

| Time Commitment | Trading hours for dollars | Earning while you sleep |

| Scalability | Often, lower capital gains rates | Highly scalable |

| Examples | Salary, hourly wages, commissions | Rental income, dividends, royalties |

| Stability | Generally predictable | Can fluctuate |

| Tax Treatment | Higher ordinary income rates | Often lower capital gains rates |

| Risk Level | Lower (steady paycheck) | Higher (requires investment) |

While active income pays the bills today, passive income builds wealth for tomorrow. The smartest financial strategy? Use your active income to fund passive income investments that eventually replace your need to work.

Many successful investors begin earning passive income through dividend investing, utilizing their active income to purchase high-dividend stocks that generate cash flow over time.

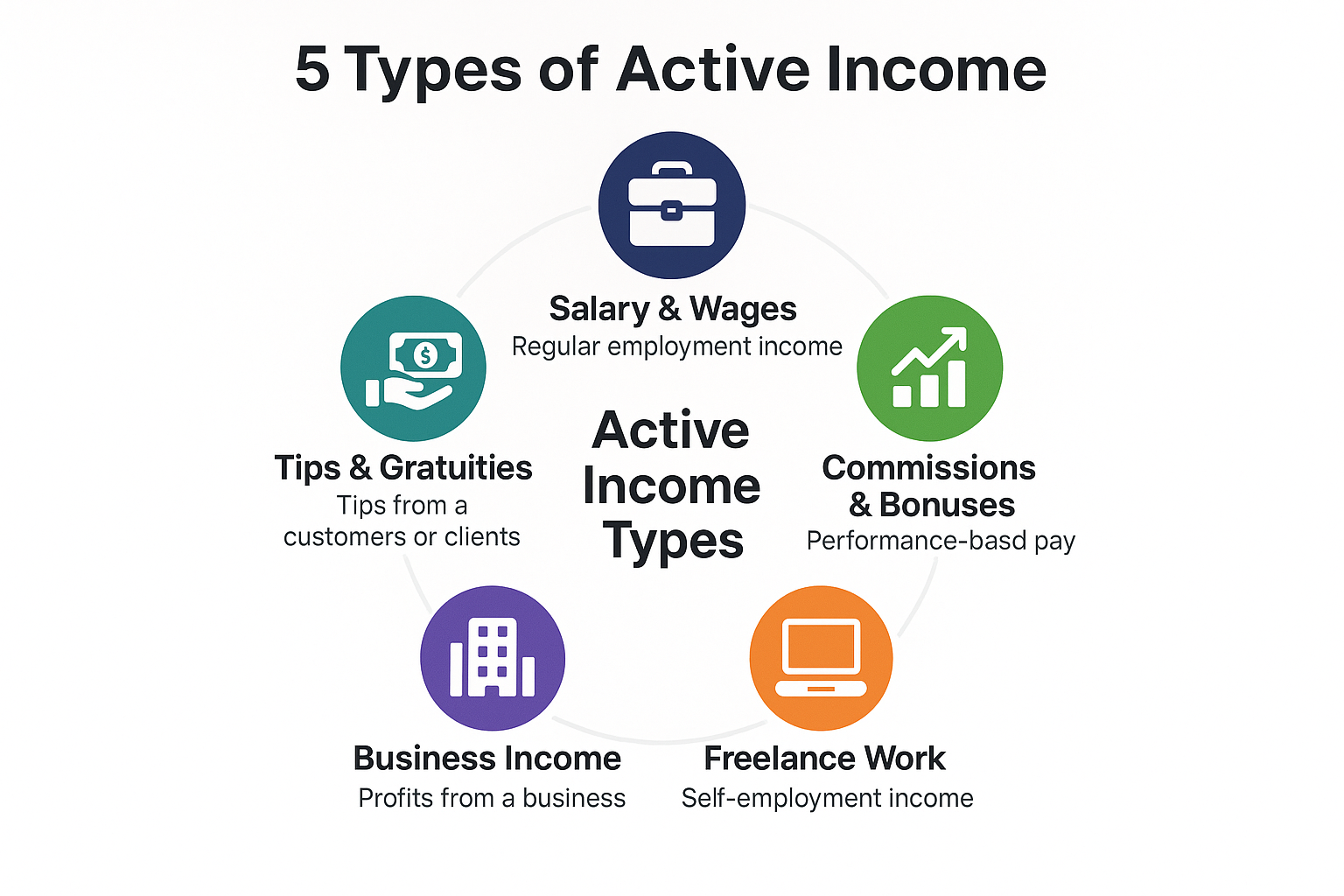

Common Types of Active Income (With Real Examples)

Active income comes in many flavors. Let’s break down the most common types:

1. Salary and Wages

This is the bread and butter of active income, a fixed amount paid regularly for your work.

Examples:

- Sarah, the Marketing Manager, earns $75,000 annually working for a tech company

- James, the Retail Associate: Makes $16/hour at a local bookstore

- Dr. Chen, the Dentist, receives a $180,000 salary at a dental practice

Pros: Predictable, stable, often includes benefits

Cons: Limited flexibility, capped earning potential

2. Commissions and Bonuses

Performance-based compensation that rewards results.

Examples:

- Mike, the Real Estate Agent: Earns 3% commission on each home sale

- Lisa, the Sales Rep: Gets a $50,000 base salary plus 10% commission on sales

- Tom, the Investment Banker: Receives a $200,000 bonus based on deals closed

Pros: Unlimited earning potential, motivating

Cons: Unpredictable, income can fluctuate wildly

3. Freelance and Contract Work

Self-employed professionals trading specialized skills for project-based pay.

Examples:

- Emma, the Graphic Designer: Charges $75/hour for logo design work

- Carlos, the Web Developer: Earns $5,000 per website build

- Rachel, the Copywriter: Gets paid $500 per blog article

Pros: Flexibility, control over rates, diverse projects

Cons: No benefits, irregular income, must find own clients

4. Business Income (Active)

Money earned from actively running a business where your involvement is essential.

Examples:

- David, the Restaurant Owner: Manages operations daily, earns $120,000/year

- Maria, the Consultant: Runs a one-person consulting firm, billing $200/hour

- The Johnson Family: Operates a family farm, earning $85,000 annually

Pros: Higher earning potential, tax advantages, building equity

Cons: Long hours, high stress, significant responsibility

5. Tips and Gratuities

Service-based income is dependent on customer satisfaction.

Examples:

- Jessica, the Server: Makes $15/hour plus $150-300 in tips per shift

- Andre, the Uber Driver: Earns ride fares plus customer tips

- Sophia, the Hair Stylist: Receives 15-20% tips on services

Pros: Can significantly boost base pay, immediate cash

Cons: Unpredictable, dependent on customer generosity

Why Active Income Matters (Even If You’re Building Passive Income)

Here’s something most personal finance gurus won’t tell you: active income isn’t the enemy. In fact, it’s your most powerful wealth-building tool when you’re starting.

The Foundation of Financial Growth

Active income serves as:

- Your seed money for investments

- The safety net while building passive streams

- Skill development that increases your market value

- Immediate cash flow to cover living expenses

Think of active income as the engine that powers your journey to financial independence. Without it, you have no fuel to invest in the stock market, real estate, or business ventures.

A Real-Life Story: From Paycheck to Portfolio

Meet Alex, a software engineer who earned $95,000 in active income in 2020. Instead of lifestyle inflation, Alex lived on $60,000 and invested the remaining $35,000 into dividend-paying stocks and index funds.

By 2025, Alex’s portfolio is expected to generate $8,500 annually in passive income, representing nearly 9% of the original active income. That’s not retirement money yet, but it’s a solid foundation built entirely from maximizing active income.

Understanding why you should invest your active income rather than just spending it is crucial for long-term wealth building.

How to Earn More Active Income: 7 Proven Strategies

Ready to boost your active income? Here are actionable strategies that actually work:

1. Develop High-Value Skills

The fastest way to increase active income is to become more valuable in the marketplace.

Action steps:

- Learn in-demand technical skills (coding, data analysis, digital marketing)

- Get professional certifications in your field

- Master soft skills like negotiation and communication

- Stay current with industry trends

Real example: Jennifer learned SQL and Python through online courses while working as a business analyst. Within 18 months, she negotiated a $25,000 raise.

2. Negotiate Your Salary

Most people leave thousands on the table by not negotiating.

Action steps:

- Research market rates for your position

- Document your achievements and value

- Practice your pitch

- Ask confidently during reviews or job offers

Statistics: According to salary.com, people who negotiate their salary can earn $1 million more over their lifetime compared to those who don’t.

3. Start a Side Hustle

Turn your spare time into extra income.

Popular side hustles for 2025:

- Freelance writing or design ($25-100/hour)

- Online tutoring ($20-60/hour)

- E-commerce or dropshipping (variable)

- Consulting in your expertise ($100-300/hour)

- Content creation (YouTube, podcasting)

Pro tip: Choose a side hustle that builds skills transferable to your main career or that could eventually become passive.

4. Pursue Performance-Based Roles

Switch to positions where exceptional performance equals exceptional pay.

High-commission fields:

- Sales (especially B2B, tech, or medical)

- Real estate

- Financial services

- Insurance

Consideration: Higher earning potential comes with less stability; make sure you have an emergency fund first.

5. Climb the Career Ladder

Strategic career advancement remains one of the most reliable ways to increase active income.

Action steps:

- Seek leadership opportunities

- Take on high-visibility projects

- Build relationships with decision-makers

- Consider strategic job changes every 2-3 years

Data point: Employees who stay at companies longer than two years get paid 50% less over their lifetime, according to Forbes.

6. Become an Expert

Position yourself as a go-to authority in your niche.

How to build expertise:

- Publish articles or blog posts

- Speak at industry events

- Create educational content

- Build a professional brand online

Real example: Marcus, a cybersecurity professional, started writing LinkedIn articles about data protection. Within two years, he was getting speaking invitations and consulting offers at $300/hour.

7. Leverage Geographic Arbitrage

Work remotely for high-paying markets while living in lower-cost areas.

Modern opportunities:

- Remote positions for companies in expensive cities

- International freelancing (earning in USD/EUR, spending in lower-cost currencies)

- Digital nomad lifestyle

Example: Priya works remotely for a San Francisco tech company ($130,000 salary) while living in Austin, Texas, where her cost of living is 40% lower.

The Tax Side of Active Income (What You Need to Know)

Here’s the not-so-fun part: active income is typically taxed at the highest rates.

Understanding Tax Brackets

In 2025, federal income tax rates range from 10% to 37% for ordinary income. Your active income falls into these brackets:

- 10%: Up to $11,600 (single)

- 12%: $11,601 to $47,150

- 22%: $47,151 to $100,525

- 24%: $100,526 to $191,950

- 32%: $191,951 to $243,725

- 35%: $243,726 to $609,350

- 37%: Over $609,350

Plus, you’ll pay:

- Social Security tax: 6.2% (up to $168,600 in 2025)

- Medicare tax: 1.45% (all income)

- Additional Medicare tax: 0.9% (income over $200,000)

Tax-Optimization Strategies

Smart moves to reduce your tax burden:

- Maximize retirement contributions – 401(k), IRA contributions reduce taxable income

- Use HSAs – Triple tax advantage for healthcare expenses

- Take advantage of deductions – Standard or itemized, whichever is higher

- Consider tax-loss harvesting – Offset investment gains with losses

- Explore business deductions – If self-employed or side hustling

Important note: While active income is taxed heavily, smart investment strategies can help you transition some of that money into lower-taxed passive income over time.

The Active Income Trap (And How to Avoid It)

Here’s the harsh truth: relying solely on active income is risky.

Why It’s a Trap

- Limited by time – Only 24 hours in a day

- No income if you can’t work – Illness, injury, or layoff = no paycheck

- Retirement challenge – Active income stops when you stop working

- Lifestyle inflation – More active income often leads to more spending

- No leverage – You can’t scale yourself

The Solution: The Income Diversification Strategy

The 70-20-10 Rule:

- 70% of active income covers living expenses

- 20% goes to building passive income investments

- 10% funds for emergency savings and skill development

This approach uses your active income as the foundation while systematically building income streams that don’t require your constant presence.

Many successful wealth builders use their active income to invest in opportunities that appreciate over time. Understanding why the stock market goes up helps you make smarter investment decisions with your active income.

Active Income in Different Life Stages

Your relationship with active income evolves throughout your life:

Early Career (20s-30s)

Focus: Maximize earning potential and skill development

- Invest heavily in education and skills

- Take calculated career risks

- Build an emergency fund

- Start investing early (even small amounts)

Mid-Career (40s-50s)

Focus: Peak earning years and wealth acceleration

- Maximize active income through expertise

- Aggressively build passive income streams

- Increase investment contributions

- Consider entrepreneurship or consulting

Pre-Retirement (60s+)

Focus: Transition from active to passive income

- Reduce reliance on active income

- Live primarily on passive income and investments

- Consider part-time or passion projects

- Optimize Social Security timing

Common Mistakes People Make With Active Income

Avoid these costly errors:

1: Not Tracking Where It Goes

Solution: Use budgeting apps to monitor every dollar

2: Lifestyle Inflation

Solution: Increase savings rate as income grows

Mistake #3: Ignoring Tax Optimization

Solution: Work with a tax professional or use tax software effectively

4: Not Investing in Yourself

Solution: Allocate 10% of income to skill development

Mistake #5: Putting All Eggs in One Basket

Solution: Build multiple income streams early

Many people also make critical mistakes when they start investing. Learning about why people lose money in the stock market and understanding the cycle of market emotions can help you avoid common pitfalls.

💰 Active Income Calculator

Calculate your total active income and see how it breaks down

Primary Income Source

Additional Active Income

Building Your Active Income Action Plan

Now that you understand active income inside and out, it’s time to create your personalized strategy. Here’s a step-by-step framework:

Step 1: Audit Your Current Active Income

Take inventory of all your active income sources:

- Primary job salary/wages

- Side hustle earnings

- Freelance projects

- Commission or bonus income

- Any other work-for-pay activities

Calculate your effective hourly rate by dividing total annual active income by total hours worked. This number reveals your true earning power.

Step 2: Identify Growth Opportunities

Ask yourself:

- Which skills could I develop to earn 20-50% more?

- Am I being paid fairly for my market value?

- What side income could I start with skills I already have?

- Where could I add value that others would pay for?

Step 3: Set Specific Income Goals

Use the SMART framework:

- Specific: “Increase active income by $15,000 annually”

- Measurable: Track monthly progress

- Achievable: Based on a realistic skill development timeline

- Relevant: Aligned with your life goals

- Time-bound: “Within 18 months”

Step 4: Create Your Skill Development Plan

Invest in yourself systematically:

- Monthly: Read industry publications, take online courses

- Quarterly: Attend workshops or conferences

- Annually: Pursue certifications or advanced training

Remember: every dollar invested in skill development can return 10-100x in increased active income over your career.

Step 5: Transition Strategy to Passive Income

The ultimate goal isn’t just more active income, it’s financial freedom. Here’s how to bridge the gap:

The Wealth Acceleration Formula:

- Maximize active income (years 1-5)

- Live below your means (maintain lifestyle discipline)

- Invest the difference (build passive income streams)

- Reinvest passive income (compound growth)

- Achieve financial independence (passive income > expenses)

For those ready to start building wealth beyond active income, exploring various investment opportunities can provide the foundation for long-term financial security.

Active Income Success Stories: Real People, Real Results

Story #1: The Corporate Climber

Background: Kevin worked as a mid-level accountant earning $68,000 in 2020.

Strategy:

- Earned CPA certification while working full-time

- Volunteered for high-visibility projects

- Networked with senior leadership

- Changed companies strategically twice

Result: By 2025, Kevin’s active income reached $125,000, an 84% increase in five years.

Key lesson: Strategic career moves and credentials beat loyalty to a single employer.

Story #2: The Side Hustle Queen

Background: Melissa, a teacher earning $52,000, wanted to pay off student loans faster.

Strategy:

- Started tutoring online ($40/hour)

- Created educational resources on Teachers Pay Teachers

- Offered curriculum consulting on weekends

- Scaled to 15 hours/week of side work

Result: Added $28,000 in annual active income while keeping her teaching job.

Key lesson: Your existing skills are valuable—find people who will pay for them.

Story #3: The Freelance Transition

Background: Omar worked in corporate marketing for $85,000 but hated the commute and office politics.

Strategy:

- Built freelance client base while employed (evenings/weekends)

- Saved 12 months of expenses as a safety net

- Left corporate job when freelance income hit $7,000/month

- Raised rates 40% over two years

Result: Now earns $140,000 annually with complete schedule flexibility.

Key lesson: Transition gradually and build your safety net before leaping.

The Psychology of Active Income: Mindset Matters

Your relationship with active income is deeply psychological. Here’s how to develop a healthy mindset:

Avoid the “Just a Job” Trap

Even if you’re building toward passive income, treating your active income source as “just a job” is a mistake. Your current work is funding your future freedom, respect it, optimize it, and extract maximum value from it.

Embrace the Exchange

Active income isn’t exploitation, it’s a voluntary exchange of value. You provide skills, time, and effort; your employer or clients provide money. When you view it this way, you can:

- Negotiate from a position of strength

- Seek win-win arrangements

- Leave situations that aren’t mutually beneficial

Develop an Abundance Mindset

Scarcity thinking: “I’m lucky to have any job.”

Abundance thinking: “I create value, and multiple opportunities exist for me”.

The abundance mindset doesn’t mean being ungrateful; it means recognizing your worth and pursuing opportunities that reflect it.

Active Income in the Gig Economy (2025 Edition)

The nature of active income has transformed dramatically. The gig economy now represents over 36% of the U.S. workforce, according to recent data.

Popular Gig Economy Active Income Sources

High-earning opportunities:

- Specialized consulting: $100-500/hour

- Technical freelancing: $75-200/hour (web dev, design, data science)

- Professional services: $50-150/hour (bookkeeping, legal, marketing)

Flexible income options:

- Rideshare driving: $15-30/hour (after expenses)

- Food delivery: $12-25/hour

- Task-based work: $15-40/hour (TaskRabbit, Handy)

Creative income streams:

- Content creation: Variable (YouTube, TikTok, blogging)

- Online teaching: $20-60/hour

- Virtual assistance: $15-35/hour

Pros and Cons of Gig Active Income

Advantages:

- ✅ Flexibility in schedule

- ✅ Multiple income sources

- ✅ Low barrier to entry

- ✅ Test different opportunities

Disadvantages:

- No benefits (health insurance, retirement)

- Income volatility

- Self-employment taxes

- No paid time off

When to Reduce Active Income (Yes, Really)

Here’s a counterintuitive truth: there comes a point where reducing active income makes sense.

The Crossover Point

This happens when:

- Your passive income covers 100%+ of expenses

- Additional active income provides diminishing returns

- Your time becomes more valuable for other pursuits

- Health or family priorities shift

Example: Patricia built her portfolio to generate $85,000 annually in passive income (dividends, real estate, business investments). Her expenses are $70,000. She reduced her consulting from full-time to 10 hours/week, trading some active income for time with her family. OECD research shows that countries with higher household wealth often have greater proportions of passive income sources such as dividends, pensions, or rental yields.

The Semi-Retirement Strategy

Many wealthy individuals don’t quit active income entirely; they optimize for enjoyment rather than maximum dollars:

- Work on passion projects

- Consult part-time on their expertise

- Mentor or teach

- Build businesses for fulfillment, not just profit

This approach combines the structure and purpose of active income with the freedom that passive income provides.

Active Income Around the World: A Global Perspective

Active income varies dramatically by geography:

Global Active Income Comparison (2025)

Highest average active income (annual):

- 🇨🇭 Switzerland: $91,000

- 🇱🇺 Luxembourg: $79,000

- 🇺🇸 United States: $63,000

- 🇳🇴 Norway: $59,000

- 🇩🇰 Denmark: $57,000

Fastest growing active income markets:

- 🇮🇳 India: Tech sector boom

- 🇻🇳 Vietnam: Manufacturing expansion

- 🇵🇱 Poland: EU integration benefits

- 🇵🇭 Philippines: BPO industry growth

Remote work opportunities have created unprecedented ability to earn first-world active income while living in lower-cost countries, a strategy called geographic arbitrage.

The Future of Active Income: Trends to Watch

As we move deeper into 2025 and beyond, several trends are reshaping active income

1. AI and Automation Impact

Jobs at risk: Routine, repetitive tasks

Jobs growing: AI oversight, creative work, human interaction roles

Strategy: Develop skills that complement AI rather than compete with it

2. Skills-Based Hiring

Traditional degrees matter less; demonstrable skills matter more. Platforms like LinkedIn are emphasizing skills over credentials.

Action: Build a portfolio showcasing your abilities, not just listing qualifications.

3. The Four-Day Work Week Movement

More companies are experimenting with compressed work weeks, offering the same salary for fewer hours.

Implication: Your hourly equivalent active income increases without changing annual compensation.

4. Hybrid and Remote Work

Remote work is stabilizing at around 30% of the workforce. This creates:

- Access to higher-paying markets regardless of location

- Reduced commute costs (more net active income)

- Opportunity for geographic arbitrage

5. Multiple Income Stream Normalization

Having just one source of active income is becoming less common. The average millennial now has 2.5 income sources.

New normal: Primary job + side hustle + small passive income streams

Not at all! Active income is essential, especially early in your wealth-building journey. It’s the fuel for building passive income. The goal is balance, not elimination.

A good rule of thumb is the 50/30/20 rule: 50% for needs, 30% for wants, 20% for savings and investments. If you’re aggressively building wealth, aim for 30-40% savings rate.

Only if you save aggressively and invest wisely. Most people need passive income streams (Social Security, pensions, investment income) to retire comfortably.

Changing jobs typically yields 10-20% increases, faster than annual raises. Alternatively, developing high-demand skills (coding, data analysis, digital marketing) can dramatically boost earning potential.

Both, sequentially. Use active income to build passive income. Think of active income as the seed and passive income as the tree that grows from it.

Maximizing Active Income: Your 90-Day Action Plan

Ready to take action? Here’s what to do in the next 90 days:

Days 1-30: Assessment Phase

- Calculate your current total active income (use the calculator above)

- Determine your effective hourly rate

- Research market rates for your position/skills

- Identify your top 3 most valuable skills

- Set a specific income increase goal

Days 31-60: Development Phase

- Enroll in one skill-building course

- Update your resume and LinkedIn profile

- Reach out to 5 people in your industry for informational interviews

- Research side hustle opportunities aligned with your skills

- Create a personal brand online (blog, portfolio, or social media presence)

Days 61-90: Action Phase

- Apply for higher-paying positions or ask for a raise

- Launch your side hustle (even a small one)

- Complete your first skill certification or course

- Set up automatic transfers: 20% of active income to investments

- Review and adjust your budget to maximize the savings rate

Beyond 90 Days: Momentum Phase

- Quarterly income reviews and adjustments

- Continuous skill development

- Scale successful side hustles

- Reinvest passive income as it grows

- Track progress toward financial independence

The Active-to-Passive Income Bridge

The ultimate strategy isn’t choosing between active and passive income; it’s using active income to build passive income.

The Wealth Building Sequence

Phase 1: Active Income Foundation (Years 1-5)

- Focus: Maximize earning potential

- Goal: Increase active income by 50-100%

- Action: Skill development, career advancement, side hustles

Phase 2: Investment Acceleration (Years 5-15)

- Focus: Convert active to passive income

- Goal: Build passive income to 25% of expenses

- Action: Aggressive investing, real estate, business building

Phase 3: Passive Income Growth (Years 15-25)

- Focus: Scale passive income

- Goal: Passive income covers 75% of expenses

- Action: Reinvestment, portfolio optimization, tax efficiency

Phase 4: Financial Independence (Year 25+)

- Focus: Maintain and enjoy

- Goal: Passive income exceeds expenses

- Action: Active income becomes optional, pursue passion projects

This journey is exactly what many successful investors follow, understanding the importance of making smart financial moves at each phase.

Real Numbers: What Active Income Can Build

Let’s look at concrete examples of how active income translates to wealth:

Scenario 1: The Consistent Saver

Active income: $60,000/year

Savings rate: 20% ($12,000/year)

Investment return: 8% annually

Time horizon: 30 years

Result: $1.47 million portfolio

Scenario 2: The Income Grower

Starting active income: $50,000/year

Income growth: 5% annually

Savings rate: 25%

Investment return: 8% annually

Time horizon: 30 years

Result: $2.18 million portfolio

Scenario 3: The Side Hustler

Primary active income: $70,000/year (saving 15% = $10,500)

Side hustle income: $15,000/year (saving 80% = $12,000)

Total annual investment: $22,500

Investment return: 8% annually

Time horizon: 25 years

Result: $1.79 million portfolio

The lesson: Your active income, when strategically saved and invested, becomes the foundation of substantial wealth.

Active Income and Financial Independence

The FIRE (Financial Independence, Retire Early) movement has popularized the concept of using active income strategically to achieve freedom.

The FIRE Formula

Financial Independence Number = Annual Expenses × 25

If your annual expenses are $50,000, you need $1.25 million invested to be financially independent (using the 4% safe withdrawal rate).

How Active Income Accelerates FIRE

Three levers to pull:

- Increase active income → More to invest

- Decrease expenses → Lower FI number needed

- Optimize investments → Faster growth

Example: Increasing active income from $60,000 to $80,000 while maintaining the same $45,000 lifestyle means you can invest $35,000 instead of $15,000 annually, cutting your time to FI in half.

The Emotional Side of Active Income

Money isn’t just mathematics; it’s deeply emotional. Your active income affects:

Identity and Self-Worth

Many people tie their self-worth to their income. This is dangerous because:

- Income fluctuates due to factors beyond your control

- Your value as a person is independent of your paycheck

- This mindset creates anxiety and poor decision-making

Healthier perspective: Your active income reflects the current market value of your skills, not your worth as a human being.

Security and Stress

Active income provides security but also creates stress:

- Fear of job loss

- Pressure to maintain performance

- Anxiety about career trajectory

Solution: Build an emergency fund (6-12 months’ expenses) and diversify income sources to reduce stress.

Freedom and Control

The paradox: active income provides freedom (to buy things, make choices) while also restricting freedom (must work to maintain it).

Resolution: View active income as a tool for building true freedom through passive income and financial independence.

Protecting Your Active Income

Your ability to earn active income is your most valuable asset. Protect it:

1. Disability Insurance

Why: If you can’t work, active income stops

Coverage: 60-70% of your income

Cost: 1-3% of annual income

2. Emergency Fund

Purpose: Bridge income gaps

Amount: 6-12 months of expenses

Location: High-yield savings account

3. Skills Maintenance

Risk: Skills become obsolete

Solution: Continuous learning and adaptation

Investment: 5-10% of time on skill development

4. Professional Network

Value: Job opportunities and career advancement

Action: Regular networking, relationship building

Return: Often 10x your time investment

5. Health Maintenance

Reality: Poor health = reduced earning capacity

Strategy: Regular exercise, good nutrition, stress management

ROI: Incalculable, your health enables everything else

Conclusion: Your Active Income Mastery Blueprint

Active income isn’t just about making money; it’s about strategically using your time and skills to build the life you want.

Here’s what we’ve covered:

✅ Active income is the foundation of wealth building for most people

✅ It comes in many forms: salary, wages, commissions, freelance work, and business income

✅ You can significantly increase it through skill development, negotiation, and strategic career moves

✅ The goal isn’t to eliminate active income but to eventually make it optional through passive income

✅ Your active income today funds your financial freedom tomorrow

Your Next Steps (Start Today)

- Calculate your total active income using the calculator above

- Determine your effective hourly rate to understand your true earning power

- Identify one skill you can develop in the next 90 days to increase your income

- Set up automatic investing of at least 20% of your active income

- Create a 12-month plan to increase your active income by at least 10%

Remember: Every dollar of active income is a seed. Plant it wisely through investing, and it will grow into a forest of passive income that provides shade (financial security) for the rest of your life.

The journey from active income dependency to financial freedom isn’t quick or easy, but it’s absolutely achievable. Millions have walked this path before you, using their active income as the springboard to build wealth, security, and ultimately, choice.

Your active income is powerful. Your potential is unlimited. Your financial future starts with the decisions you make today.

Now get out there and maximize your active income; your future self will thank you.

Disclaimer

The information provided in this article is for educational and informational purposes only and should not be construed as financial, investment, tax, or legal advice. Active income strategies, investment returns, and financial outcomes vary based on individual circumstances, market conditions, and numerous other factors. Past performance does not guarantee future results. Before making any financial decisions, please consult with qualified financial, tax, and legal professionals who can assess your specific situation. TheRichGuyMath.com and its authors are not responsible for any financial decisions made based on this content.

About the Author

Max Fonji is a financial educator and wealth-building strategist with over 15 years of experience helping individuals maximize their earning potential and build sustainable wealth. Having personally transitioned from active income dependency to financial independence, Max understands both the challenges and opportunities that come with optimizing your income strategy. Through TheRichGuyMath.com, Max provides practical, actionable guidance for people at every stage of their financial journey. When not writing about personal finance, Max enjoys analyzing market trends, mentoring young professionals, and exploring new investment strategies.

Related posts:

What Is SmartPass? Raptor Digital Hall Pass Explained for K-12 Schools

What Is SmartPass? Raptor Digital Hall Pass Explained for K-12 Schools

What Is the 3x Rent Rule & How to Calculate It (With Examples)

What Is the 3x Rent Rule & How to Calculate It (With Examples)

Portfolio Income: Definition, Examples, Tax Rules, and Strategies

Portfolio Income: Definition, Examples, Tax Rules, and Strategies

Bookkeeping vs Accounting: What’s the Difference & Which Do You Need?

Bookkeeping vs Accounting: What’s the Difference & Which Do You Need?

Return on Assets (ROA): Definition, Formula & How to Improve It

Return on Assets (ROA): Definition, Formula & How to Improve It

How to Save Money Fast: A Smart Savings Plan That Actually Works

How to Save Money Fast: A Smart Savings Plan That Actually Works