Balance transfer credit cards represent one of the most mathematically advantageous tools for eliminating high-interest debt when used correctly. These specialized cards allow cardholders to move existing credit card balances from high-interest accounts to a new card offering a promotional 0% APR period, typically lasting 12 to 21 months.

The math behind this strategy is straightforward: transferring a $5,000 balance from a card charging 22% APR to a card with 0% APR for 18 months saves approximately $1,650 in interest charges, even after accounting for a typical 3% transfer fee.

For additional context, see our full comprehensive guides on the Credit guide.

However, balance transfers only work as a debt elimination strategy when paired with disciplined repayment behavior and a clear mathematical payoff plan. Without understanding the mechanics, fees, and strategic timing involved, cardholders risk extending their debt cycle rather than escaping it.

This guide explains exactly how balance transfer credit cards function, breaks down the cost-benefit analysis with real numbers, and identifies the specific financial situations where transfers make mathematical sense and when they don’t.

Key Takeaways

Balance transfer cards offer 0% promotional APR periods (typically 12-21 months) that pause interest accumulation, allowing faster debt payoff when used strategically

Transfer fees range from 3-5% of the transferred amount, which must be calculated against potential interest savings to determine net benefit

Successful transfers require disciplined repayment plans that eliminate the full balance before the promotional period ends, and the regular APR applies

Credit utilization and hard inquiries temporarily impact credit scores, but responsible use ultimately improves creditworthiness through debt reduction

Balance transfers work best for high-interest debt with clear payoff timelines, not as a solution for ongoing spending problems or chronic debt accumulation

What Is A Balance Transfer Credit Card?

A balance transfer credit card is a financial product specifically designed to help consumers consolidate and pay down existing credit card debt by offering a promotional 0% or low-interest APR period on transferred balances.

The fundamental mechanism works through a simple debt reassignment process. The new card issuer pays off your existing creditors directly, moving your debt obligation from one or more high-interest cards to the new card with favorable promotional terms.

Qualifying balances for transfer typically include:

- Credit card balances from other issuers

- Store credit card debt

- Some personal lines of credit

- Certain installment loans (issuer-dependent)

Most issuers do not allow balance transfers between cards they issue. You cannot transfer a Chase balance to another Chase card, for example.

Here’s a concrete example: Sarah carries a $6,000 balance on a credit card charging 24.99% APR. She applies for and receives a balance transfer card offering 0% APR for 18 months with a 3% transfer fee. The issuer charges a one-time $180 fee (3% of $6,000) and pays off her original card. Sarah now owes $6,180 on the new card at 0% interest for 18 months.

If Sarah divides $6,180 by 18 months, she needs to pay $343.33 monthly to eliminate the debt before the promotional period ends. By doing so, she pays only the $180 transfer fee instead of the approximately $2,100 in interest she would have paid on the original card over the same period—a net savings of $1,920.

This mathematical advantage only materializes when the cardholder commits to aggressive repayment during the promotional window. Understanding how to structure your budget around this payoff timeline determines whether a balance transfer becomes a wealth-building tool or simply postpones the debt problem.

How Balance Transfers Work Step By Step

Understanding the operational sequence of a balance transfer prevents costly mistakes and ensures maximum benefit from the promotional period.

Step 1: Research and Apply for a Balance Transfer Card

Compare offers based on promotional APR length, transfer fee percentage, post-promotional APR, and credit limit likelihood. Most quality offers require good to excellent credit (FICO 670+). Submit your application with accurate income and debt information.

Step 2: Receive Approval and Review Terms

Upon approval, carefully review the credit limit assigned, the exact promotional period end date, the transfer fee percentage, and the ongoing APR that applies after the promotional period. Calculate whether your approved limit accommodates your intended transfer amount plus the fee.

Step 3: Initiate the Balance Transfer

Most issuers provide three transfer methods: online through your account portal, by phone with customer service, or via convenience checks mailed with your card. You’ll need the account numbers and exact balances of the cards you’re transferring from. Specify the exact amount to transfer to each creditor.

Step 4: Wait for Processing (7-21 Days)

Balance transfers are not instantaneous. Processing typically requires 7-14 business days, though some transfers take up to 21 days. Critical: Continue making minimum payments on your old cards until you confirm the transfer completed. Missing a payment during this window damages your credit score and may trigger penalty APRs.

Step 5: Verify Transfer Completion

Check both your new card balance and old card statements to confirm the transfer posted correctly. Your new card balance should show the transferred amount plus the transfer fee. Your old card should show a payment from the new issuer and a zero or reduced balance.

Step 6: Establish Your Repayment Schedule

Calculate your required monthly payment by dividing your total new balance by the number of months in your promotional period. Add a buffer for safety—aim to pay off the balance 1-2 months before the promotional period ends. Set up automatic payments to ensure consistency.

Step 7: Close or Secure Old Accounts

Decide whether to close paid-off accounts or keep them open with zero balances. Keeping accounts open typically benefits your credit utilization ratio, but only if you won’t be tempted to accumulate new charges. If you lack spending discipline, closing accounts prevents the re-accumulation of debt.

The mathematical success of this process depends entirely on Step 6. Without a structured repayment plan that eliminates the balance before promotional terms expire, the transfer merely postpones interest charges rather than eliminating them.

What Is 0% APR Balance Transfer?

A 0% APR balance transfer promotion represents a temporary interest-free period offered by credit card issuers to attract new customers and capture market share from competitors.

During this promotional window—typically ranging from 6 to 21 months—the card issuer charges zero interest on the transferred balance. This pause in interest accumulation creates a mathematical opportunity to direct 100% of your payments toward principal reduction rather than splitting payments between principal and interest.

The promotional mechanics work as follows:

The 0% rate applies only to the transferred balance, not to new purchases (unless the card also offers a separate 0% purchase APR promotion). The promotional period begins on the date your account opens, not when the transfer completes. This timing difference can cost you 2-3 weeks of your promotional period if you’re not aware.

What happens when the promotional period ends:

The moment the promotional period expires, any remaining balance immediately begins accruing interest at the card’s regular APR—typically ranging from 18.99% to 29.99% depending on your creditworthiness. This regular APR applies to the remaining balance going forward, not retroactively.

Some issuers offer “deferred interest” promotions instead of true 0% APR. These predatory structures charge retroactive interest on the entire original balance if you don’t pay it off completely before the promotional period ends. Always verify you’re receiving a true 0% APR offer, not a deferred interest trap.

Here’s the mathematical impact:

Consider a $10,000 balance transferred to a card with 18 months of 0% APR and a 3% transfer fee ($300). Your total balance becomes $10,300.

- Scenario A (Paid off in 18 months): Monthly payment of $572.22 eliminates the debt with only the $300 fee cost.

- Scenario B (Paid off in 24 months): After 18 months of $429 payments, $7,722 remains unpaid. The remaining $2,578 accrues interest at 24.99% APR for 6 additional months, costing approximately $200 in interest plus the original $300 fee—total cost $500.

- Scenario C (Minimum payments only): After 18 months of minimum payments, approximately $8,500 remains. This balance now compounds at 24.99% APR, potentially taking years to eliminate and costing thousands in interest.

The 0% promotional period creates value only when paired with aggressive principal reduction. The math requires dividing your total transferred balance (including fees) by your promotional period length to establish your minimum monthly payment threshold.

Learn more from our complete guide on Credit card APR explained.

Balance Transfer Fees Explained

Balance transfer fees represent the cost of accessing the 0% promotional period, a one-time charge calculated as a percentage of the amount transferred.

Most issuers charge between 3% and 5% of the transferred amount, with 3% being the most common rate among competitive offers. This fee is added to your transferred balance immediately and begins counting against your credit limit.

Fee calculation example:

| Transfer Amount | Fee Percentage | Fee Cost | Total New Balance |

|---|---|---|---|

| $3,000 | 3% | $90 | $3,090 |

| $5,000 | 3% | $150 | $5,150 |

| $8,000 | 5% | $400 | $8,400 |

| $10,000 | 3% | $300 | $10,300 |

| $15,000 | 5% | $750 | $15,750 |

When fees apply:

The transfer fee posts to your account when the transfer processes, not when you’re approved. If you transfer balances from multiple cards, each transfer incurs a separate fee. The fee counts toward your credit limit, reducing available credit for the transfer itself.

Fee versus interest comparison—the critical calculation:

A balance transfer only makes mathematical sense when the fee cost is substantially lower than the interest you would pay on your existing debt during the same timeframe.

Example calculation:

Current balance: $6,000 at 22.99% APR

Transfer offer: 0% for 18 months with 3% fee

Transfer fee: $180

Interest cost if you keep the current card and pay $400/month for 18 months: approximately $1,150

Net savings: $1,150 – $180 = $970

The transfer makes mathematical sense because the fee represents only 15.7% of the interest cost you would otherwise pay.

When fees don’t make sense:

If you’re transferring a small balance with a short payoff timeline, the fee may exceed the interest savings. For example, transferring $1,000 you plan to pay off in 4 months:

- Transfer fee at 3%: $30

- Interest cost at 20% APR for 4 months: approximately $35

- Net savings: only $5

In this scenario, the administrative effort and potential credit score impact aren’t worth a $5 savings. The mathematical threshold typically requires at least $2,000 in debt with a 12+ month payoff timeline to justify the transfer fee.

Some premium cards offer 0% balance transfer promotions with no transfer fee, though these are increasingly rare and typically require excellent credit scores (750+). When available, these offers provide maximum mathematical advantage.

Understanding the relationship between APY vs APR helps clarify how interest compounds on your existing debt, making the fee-versus-interest calculation more precise.

Pros And Cons Of Balance Transfer Cards

Balance transfer credit cards deliver measurable financial benefits in specific situations while creating risks in others. The mathematical advantages depend entirely on disciplined execution.

Advantages

Significant interest savings: Eliminating 18-29% APR charges for 12-21 months redirects hundreds to thousands of dollars from interest payments to principal reduction. A $10,000 balance at 24% APR costs approximately $4,500 in interest over two years with minimum payments. A successful balance transfer eliminates most or all of this cost.

Accelerated debt payoff: Without interest compounding against you, 100% of each payment reduces your principal balance. This mathematical efficiency shortens your debt elimination timeline by months or years compared to paying down high-interest debt.

Simplified debt management: Consolidating multiple credit card balances into a single account with one payment date reduces administrative complexity and missed payment risk. One payment is easier to automate and track than juggling multiple creditors.

Potential credit score improvement: Successfully paying down consolidated debt lowers your overall credit utilization ratio—the second-most important factor in credit scoring models. Lower utilization typically increases your credit score, assuming you make all payments on time.

Psychological momentum: Watching your balance decrease rapidly without interest working against you creates positive behavioral reinforcement. This psychological benefit shouldn’t be dismissed—debt elimination requires sustained motivation over many months.

Disadvantages

Transfer fees reduce net savings: The 3-5% upfront cost must be factored into your total payoff amount. On large balances, this fee can reach $500-$750, which increases your required monthly payment to achieve full payoff during the promotional period.

Promotional period pressure: The fixed timeframe creates a deadline that may not align with your financial reality. Unexpected expenses, income disruptions, or emergencies can derail your payoff plan, leaving you with a large balance when the high regular APR kicks in.

Credit score impact from hard inquiry and utilization: Applying for a new card triggers a hard credit inquiry (typically -5 to -10 points temporarily). Transferring a large balance may initially increase your overall credit utilization if your new credit limit is lower than your previous combined limits.

Temptation to accumulate new debt: Paying off old cards creates available credit that may tempt undisciplined spenders to accumulate new charges. This behavior pattern—transferring debt while simultaneously creating new debt—leads to a worse financial position than before the transfer.

Regular APR risk: If you don’t eliminate the balance before the promotional period ends, the remaining balance faces interest rates often higher than your original card’s (24-29% APR is common). The issuer profits significantly from cardholders who fail to pay off balances during the promotional window.

Purchase APR typically differs: Most balance transfer cards charge regular APR on new purchases immediately, even during the balance transfer promotional period. Using the card for new purchases while carrying a transferred balance creates payment allocation complexity and often results in higher interest costs.

The mathematical net benefit calculation requires an honest assessment of your repayment discipline and financial stability. Balance transfers work exceptionally well for financially stable individuals with temporary high-interest debt and a concrete payoff plan. They work poorly for individuals with ongoing spending problems or unstable income.

When A Balance Transfer Makes Sense

Balance transfer credit cards deliver maximum mathematical advantage in specific financial situations characterized by temporary high-interest debt and stable repayment capacity.

High-Interest Debt With Clear Origin

Balance transfers work best when you carry high-interest credit card debt from a specific event or period—medical expenses, emergency home repairs, temporary income loss, or a one-time large purchase. This type of debt has a defined principal amount that won’t increase because the spending behavior that created it has ended.

If your debt resulted from ongoing overspending or chronic budget shortfalls, a balance transfer addresses the symptom rather than the disease. Without fixing the underlying spending behavior, you’ll likely accumulate new debt while paying off the transferred balance.

Short to Medium Payoff Window (6-18 Months)

The mathematical sweet spot for balance transfers involves debt you can realistically eliminate within 6-18 months of focused payments. This timeframe aligns with most promotional periods and ensures you capture the full interest-savings benefit.

Calculate your required monthly payment by dividing your total balance (including the transfer fee) by your promotional period length. If this payment fits comfortably within your budget with a safety margin, the transfer makes mathematical sense.

Example: $7,500 balance with 3% fee = $7,725 total. With an 18-month promotional period, you need $429.17/month to eliminate the debt. If your budget can support $450-500/month, you have an appropriate margin for success.

Stable Income and Employment

Balance transfers require sustained monthly payments over many months. This strategy works best when your income is stable and predictable—salaried employment, established business income, or reliable contract work.

If your income fluctuates significantly or your employment situation is uncertain, the fixed payment obligation creates risk. Missing payments during the promotional period may trigger penalty APRs that eliminate the transfer’s mathematical advantage.

Good to Excellent Credit Score (670+)

The best balance transfer offers—longest promotional periods, lowest fees, highest credit limits—go to applicants with good to excellent credit scores. If your score is below 670, you may receive approval but with less favorable terms: shorter promotional periods (6-12 months), higher fees (5%), or lower credit limits that don’t accommodate your full balance.

Check your credit score before applying. If you’re below 670, consider whether improving your score for 3-6 months might qualify you for better terms that deliver greater mathematical advantage.

Disciplined Financial Behavior

Successful balance transfer execution requires discipline in three areas: making every payment on time, avoiding new purchases on old cards, and resisting the temptation to use newly available credit.

If you struggle with impulse spending or have a history of accumulating credit card debt, a balance transfer may simply postpone the problem. Honest self-assessment of your financial discipline determines whether this strategy will succeed.

The mathematical advantage of balance transfers compounds when you redirect interest savings toward building an emergency fund. Once you eliminate the transferred debt, continue making the same monthly payment into a high-yield savings account to create a financial buffer that prevents future high-interest debt accumulation.

When Balance Transfers Are A Bad Idea

Certain financial situations and behavioral patterns make balance transfer credit cards mathematically disadvantageous or strategically counterproductive.

Ongoing Spending Problems

If your credit card debt results from chronic overspending rather than a one-time event, a balance transfer doesn’t solve your fundamental problem. Transferring debt while continuing to spend beyond your means creates a worse situation: you’ll carry both the transferred balance and new debt on your old cards.

The math becomes destructive: you’re making payments on the transferred balance while simultaneously accumulating new high-interest debt elsewhere. This pattern leads to a higher total debt load than before the transfer.

Before considering a balance transfer, track your spending for 2-3 months using a structured approach like the 50/30/20 rule. If your spending consistently exceeds your income, address the spending behavior first through budget restructuring, not through debt consolidation.

Short Promotional Periods Relative to Balance Size

Some balance transfer offers provide only 6-12 months of 0% APR. If your balance is large relative to this timeframe, you may not eliminate the debt before the promotional period ends.

Example: $12,000 balance with 3% fee = $12,360 total. With a 12-month promotional period, you need $1,030/month to pay off the debt. If your budget can only support $500-600/month, you’ll carry a $6,000+ balance into the high regular APR period, negating much of the transfer’s benefit.

The mathematical rule: your required monthly payment (total balance ÷ promotional months) should consume no more than 15-20% of your monthly take-home income to maintain financial flexibility for other obligations and emergencies.

Low Credit Limits That Don’t Accommodate Your Balance

If you’re approved for a balance transfer card but receive a credit limit significantly lower than your existing debt, you face a difficult choice: transfer only a portion of your debt or decline the offer.

Partial transfers create administrative complexity—you’re now managing both the new card with the transferred portion and the old card(s) with remaining balances. The mathematical benefit diminishes because you’re still paying interest on the untransferred portion.

Additionally, transferring the maximum amount to a new card creates very high credit utilization on that account (potentially 90-100%), which temporarily damages your credit score and reduces your financial flexibility.

Near-Term Major Credit Applications

Applying for a balance transfer card triggers a hard credit inquiry and potentially increases your credit utilization ratio—both factors that temporarily reduce your credit score by 10-30 points.

If you’re planning to apply for a mortgage, auto loan, or other significant credit within the next 6-12 months, the temporary credit score reduction may cost you more in higher interest rates on those loans than you’d save through the balance transfer.

The mathematical priority: securing the lowest possible rate on a $300,000 mortgage (where a 0.25% rate difference costs approximately $15,000 over 30 years) far exceeds the $1,000-2,000 you might save through a credit card balance transfer.

Inability to Avoid New Purchases on the Transfer Card

Most balance transfer cards charge regular APR (18-29%) on new purchases immediately, even during the 0% balance transfer promotional period. If you use the card for new purchases while carrying a transferred balance, your payments are typically allocated to the 0% balance first, allowing the high-interest purchase balance to grow.

This payment allocation structure is mathematically designed to maximize issuer profit. Unless you can commit to zero new purchases on the transfer card, you risk creating a more expensive debt situation than your original high-interest cards.

Very Small Balances With Short Payoff Timelines

Transferring small balances (under $1,500) that you could pay off within 3-6 months without a transfer often doesn’t justify the administrative effort, credit inquiry, or transfer fee.

Example: $1,200 balance at 21% APR paid off in 4 months costs approximately $55 in interest. A 3% transfer fee costs $36, saving only $19 while adding complexity and a hard inquiry to your credit report.

For small balances, the mathematically superior approach is often aggressive direct payoff using a structured plan rather than balance transfer complexity.

Understanding when balance transfers create a mathematical disadvantage is as important as recognizing when they deliver a benefit. The decision requires honest assessment of your financial behavior, realistic evaluation of your repayment capacity, and clear understanding of your broader financial goals.

How Balance Transfers Affect Your Credit Score

Balance transfer credit cards create both temporary negative impacts and potential long-term positive effects on your credit score, depending on how you manage the account.

Hard Inquiry Impact (-5 to -10 Points, Temporary)

When you apply for a balance transfer card, the issuer performs a hard credit inquiry to evaluate your creditworthiness. This inquiry typically reduces your credit score by 5-10 points.

The impact is temporary—hard inquiries affect your score for 12 months and fall off your credit report entirely after 24 months. If you’re not applying for other major credit within the next 6-12 months, this temporary reduction is mathematically insignificant.

However, if you apply for multiple balance transfer cards within a short period (rate shopping), each application triggers a separate hard inquiry. Unlike mortgage or auto loan inquiries (which are grouped when made within 14-45 days), credit card inquiries are counted individually. Limit your applications to 1-2 cards to minimize this impact.

Credit Utilization Impact

Credit utilization ratio—the percentage of available credit you’re using, accounts for approximately 30% of your FICO score calculation. Balance transfers affect this ratio in complex ways.

Initial impact (often negative): When you transfer a balance to a new card, you may initially increase your overall utilization if the new credit limit is lower than your previous combined available credit.

Example:

- Before transfer: $10,000 total debt across three cards with $30,000 combined limits = 33% utilization

- After transfer: $10,300 debt on one new card with $12,000 limit = 86% utilization on that card, even though overall utilization may improve

High utilization on individual cards can reduce your score even if your overall utilization is reasonable. Credit scoring models evaluate both per-card utilization and aggregate utilization.

Improving impact (as you pay down debt): As you make payments and reduce your balance during the promotional period, your utilization ratio decreases, which typically increases your credit score. This positive effect compounds over time as your balance approaches zero.

The mathematical relationship is non-linear—reducing utilization from 80% to 50% creates a larger score increase than reducing from 30% to 20%. Maximum credit score benefit occurs when you maintain utilization below 30% across all cards and below 10% for optimal scoring.

For detailed strategies on managing this critical metric, review this guide on credit utilization.

Payment History Impact (30-35% of Score)

Payment history represents the single largest factor in credit score calculation. Balance transfers affect this factor through two mechanisms:

Positive impact: Making all payments on time during and after the promotional period builds positive payment history. Consistent on-time payments over 12-18 months can increase your score by 20-50 points, especially if you previously had occasional late payments.

Negative impact risk: Missing even a single payment during the promotional period can trigger penalty APRs (often 29.99%) and report a delinquency to credit bureaus. A single 30-day late payment can reduce your score by 60-110 points, depending on your previous credit profile.

Set up automatic minimum payments to eliminate this risk. You can always make additional manual payments, but automation ensures you never miss the minimum payment deadline.

New Account Impact

Opening a new credit card reduces the average age of your credit accounts, which comprises about 15% of your credit score. This impact is typically minor (5-15 points) and diminishes over time as the account ages.

If you have a thin credit file (fewer than 5 accounts), opening a new account has a more pronounced effect. If you have an established credit history with 10+ accounts, the impact is negligible.

Account Closure Considerations

After paying off your old cards, you face a decision: keep them open with zero balances or close them.

Keeping accounts open:

- Maintains higher total available credit (lower utilization ratio)

- Preserves average account age

- Provides credit flexibility for emergencies

Closing accounts:

- Eliminates temptation to accumulate new debt

- Simplifies credit management

- Reduces identity theft risk from unused accounts

From a pure credit score optimization perspective, keeping accounts open is mathematically superior. However, if you lack spending discipline, the behavioral benefit of closing accounts may outweigh the credit score cost.

Long-Term Credit Score Benefit

When executed properly, balance transfers improve your credit score through a predictable sequence:

Months 1-3: Score decreases 10-20 points from hard inquiry and potentially higher utilization

Months 4-8: Score returns to baseline as inquiry impact fades and utilization decreases

Months 9-18: Score increases 20-50+ points as utilization drops below 30%, payment history strengthens, and debt-to-income ratio improves

Months 18+: Score stabilizes at new, higher level, assuming continued responsible credit management

The mathematical path to credit score improvement through balance transfers requires eliminating the transferred balance, maintaining perfect payment history, and avoiding new debt accumulation on old accounts.

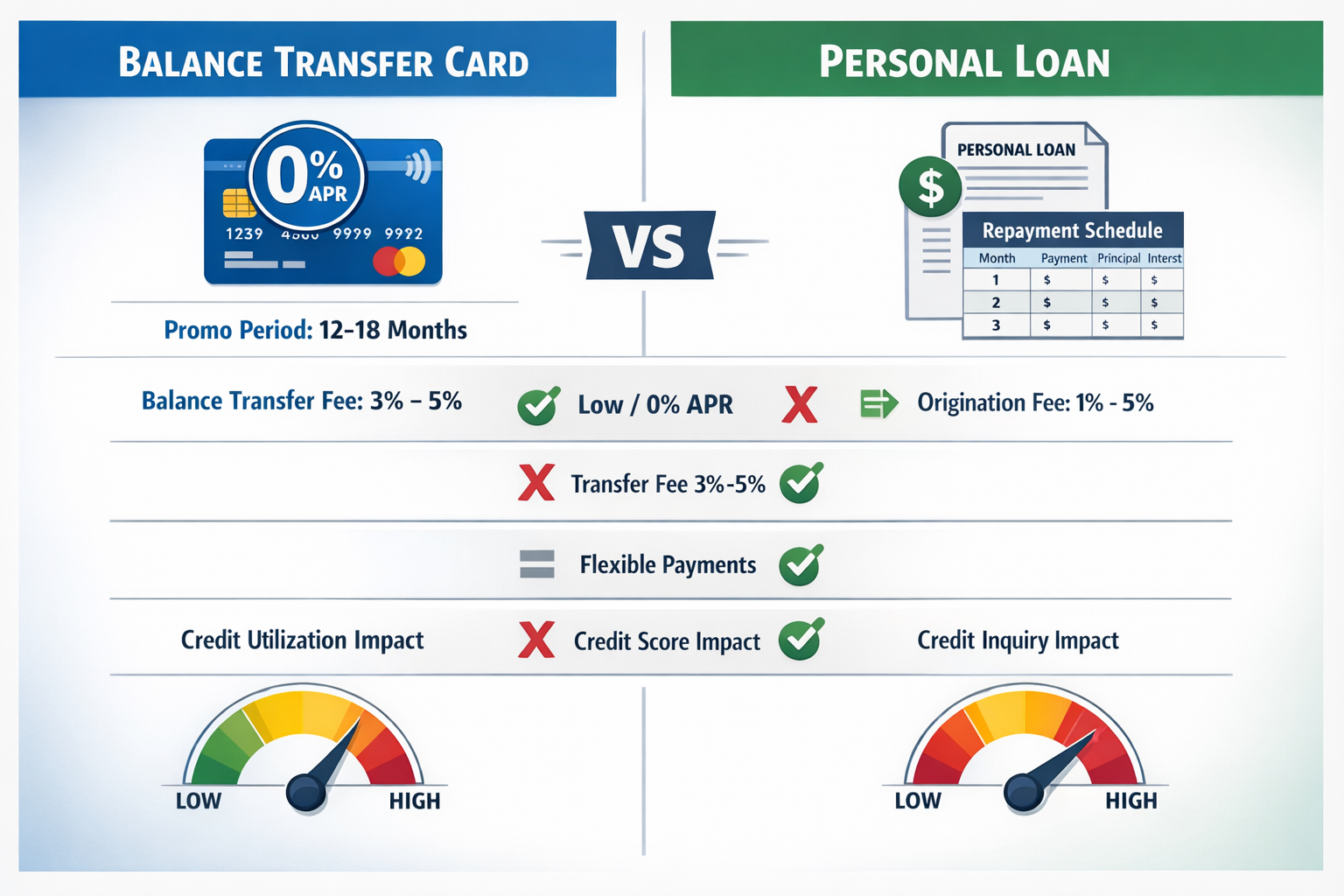

Balance Transfer vs Personal Loan

Both balance transfer credit cards and personal loans consolidate high-interest debt, but they operate through different mathematical structures that create distinct advantages depending on your situation.

| Factor | Balance Transfer Card | Personal Loan |

|---|---|---|

| Interest Rate | 0% promotional (12-21 months), then 18-29% | Fixed 6-36% for entire term |

| Upfront Costs | 3-5% transfer fee | 1-8% origination fee |

| Repayment Structure | Flexible minimum payments | Fixed monthly payment |

| Term Length | Promotional period only | 2-7 years typical |

| Payment Predictability | Variable (you control payment amount) | Fixed (same payment monthly) |

| Credit Impact | Hard inquiry + utilization changes | Hard inquiry + new installment account |

| Debt Type | Revolving credit | Installment loan |

| Discipline Required | High (must pay off before promo ends) | Lower (fixed payment enforced) |

| Best For | Short-term payoff (6-18 months) | Longer-term payoff (2-5 years) |

Interest Rate Comparison

Balance transfer cards offer superior short-term interest rates through 0% promotional periods. During this window, you pay zero interest on the transferred balance, allowing 100% of payments to reduce principal.

Personal loans charge fixed interest rates throughout the loan term, typically ranging from 6% to 36%, depending on your credit score and income. While higher than 0%, these rates are usually lower than credit card regular APRs and remain constant regardless of market changes.

Mathematical advantage: Balance transfers win for short-term payoff (under 18 months). Personal loans win for longer-term payoff (24+ months) because the fixed rate remains lower than the balance transfer card’s post-promotional APR.

Fee Structure Differences

Balance transfer cards charge a one-time fee (3-5% of the transferred amount) added to your balance. This fee is straightforward and predictable.

Personal loans charge origination fees (1-8% of the loan amount), deducted from the loan proceeds. A $10,000 loan with a 5% origination fee provides $9,500 in actual funds, but you repay the full $10,000 plus interest.

Example comparison:

- Balance transfer: $10,000 debt + 3% fee = $10,300 total to repay at 0% for 18 months

- Personal loan: $10,000 loan – 5% fee = $9,500 received, repay $10,000 at 12% APR over 36 months = $11,616 total cost

The balance transfer saves $1,316 in this scenario, but only if you pay off the full balance within the 18-month promotional period.

Repayment Flexibility vs Structure

Balance transfer cards require only minimum monthly payments (typically 2-3% of the balance), giving you flexibility to pay more when possible and less during tight months. This flexibility benefits people with variable income but requires discipline to maintain an aggressive payoff pace.

Personal loans mandate fixed monthly payments for the entire loan term. This structure enforces consistent debt reduction and eliminates the temptation to make only minimum payments. The fixed payment also simplifies budgeting; you know exactly what you’ll pay each month for the next 2-5 years.

Behavioral consideration: If you struggle with financial discipline, the enforced structure of personal loan payments may deliver better outcomes despite a higher total interest cost. If you have strong discipline, balance transfer flexibility allows you to accelerate payoff when extra funds are available.

Credit Score Impact Differences

Balance transfers affect your credit utilization ratio (revolving credit) significantly because the transferred balance counts against your credit card limits. High utilization can temporarily reduce your score.

Personal loans create a new installment account, which diversifies your credit mix (a minor positive factor) without affecting credit card utilization. The loan balance doesn’t impact utilization calculations because it’s not revolving credit.

Credit mix benefit: If you have only credit cards, adding a personal loan improves your credit mix by introducing installment credit. This diversity can increase your score by 10-20 points over time.

For a comprehensive comparison of debt consolidation options, explore various personal loan options that might suit different financial situations.

When to Choose Each Option

Choose a balance transfer card when:

- You can pay off the debt within 12-18 months

- You have strong financial discipline

- Your credit score qualifies for 0% promotional offers

- You want to minimize the total interest cost

- Your debt is currently on high-APR credit cards (20%+)

Choose a personal loan when:

- You need 24+ months to pay off the debt

- You prefer fixed, predictable monthly payments

- You want to avoid the credit card utilization impact

- You lack discipline for aggressive voluntary payments

- You’re consolidating multiple debt types (credit cards + other loans)

The mathematical optimal choice depends on your realistic payoff timeline. Calculate your required monthly payment for both options and honestly assess which structure you’ll successfully execute. The best financial product is the one you’ll actually use correctly, not the one with theoretically superior terms.

How To Pay Off Balance Transfer Debt Fast

Successful balance transfer execution requires a structured mathematical approach that ensures complete debt elimination before the promotional period ends.

Calculate Your Minimum Required Payment

Begin with precise math: divide your total transferred balance (including the transfer fee) by the number of months in your promotional period.

Formula: Required Monthly Payment = (Transferred Balance + Transfer Fee) ÷ Promotional Period Months

Example: $8,000 balance + $240 fee (3%) = $8,240 total ÷ 18 months = $457.78 minimum monthly payment

This calculation represents the absolute minimum payment to eliminate debt before the promotional period ends. Build in a safety margin by adding 10-15% to this amount, creating a buffer against unexpected expenses or calculation errors.

Safety margin payment: $457.78 × 1.15 = $526.45 monthly

This buffer ensures you eliminate the debt 1-2 months before the promotional period expires, protecting against processing delays or unexpected circumstances.

Automate Your Payments

Set up automatic payments for at least the minimum required amount from your checking account to your balance transfer card. Schedule the payment for 3-5 days after your primary income deposits to ensure sufficient funds.

Automation eliminates two critical risks: forgotten payments that trigger late fees and penalty APRs, and the temptation to “skip a month” when discretionary spending opportunities arise.

You can always make additional manual payments above the automated amount, but automation guarantees you never fall below your required minimum payment threshold.

Create a Promotional Period Payoff Plan

Build a simple tracking spreadsheet or use a note-taking app to monitor your progress:

Month | Payment | Remaining Balance | Months Left

Update this tracker after each payment posts. Watching your remaining balance decrease creates psychological momentum and helps you identify if you’re falling behind schedule early enough to make corrections.

Milestone strategy: Set quarterly milestones at 25%, 50%, and 75% debt reduction. If you reach month 4.5 of an 18-month promotional period, you should have eliminated approximately 25% of the debt. Missing these milestones signals the need to increase payment amounts or reduce expenses.

Direct Windfalls to Debt Elimination

Commit to directing 100% of financial windfalls toward your balance transfer debt: tax refunds, work bonuses, gift money, side income, or expense reimbursements.

A single $1,500 tax refund applied to your balance can reduce your remaining required monthly payments by $100+ or shorten your payoff timeline by 3-4 months.

Mathematical impact: Every dollar paid above your minimum required payment reduces future interest risk and accelerates your path to zero balance. Unlike payments on high-interest debt (where a portion goes to interest), every dollar paid on a 0% promotional balance reduces principal 100%.

Implement a Zero-Purchase Policy

Establish a firm rule: make zero new purchases on your balance transfer card during the promotional period. This policy prevents payment allocation complexity and ensures all your payments reduce the transferred balance.

Most issuers allocate your payments to the lowest-APR balance first. If you make new purchases (which typically accrue interest at regular APR immediately), your payments go to the 0% transferred balance while the high-interest purchase balance grows.

Use a different card for necessary purchases, or better yet, use a debit card or cash to maintain spending awareness and avoid accumulating new debt.

Reduce Expenses Strategically

Review your monthly expenses and identify reduction opportunities that can increase your debt payment capacity:

- Pause subscription services temporarily ($50-150/month)

- Reduce dining out frequency ($100-300/month)

- Negotiate lower rates on insurance, phone, or internet ($30-100/month)

- Eliminate discretionary purchases until debt is eliminated

Even modest expense reductions of $100-200 monthly can shorten your payoff timeline by 2-4 months and create a safety margin that protects against the promotional period expiring with a remaining balance.

Increase Income Temporarily

Consider temporary income increases through side work, freelancing, or overtime specifically designated for debt elimination. A few months of additional income can dramatically accelerate your payoff timeline.

Example: Adding $500/month in side income for 12 months provides $6,000 in additional debt payment capacity, potentially eliminating a medium-sized balance or cutting your payoff timeline in half.

The temporary nature of this effort makes it psychologically sustainable—you’re not committing to permanent lifestyle changes, just a focused 12-18 month debt elimination sprint.

Monitor Your Promotional Period End Date

Set calendar reminders at 90 days, 60 days, and 30 days before your promotional period ends. These alerts trigger progress checks and allow you to make final adjustments to ensure complete payoff.

If you reach the 60-day warning with a significant balance remaining, calculate whether you can realistically eliminate it in the remaining time. If not, consider whether a second balance transfer to a new card or a personal loan conversion makes mathematical sense to avoid the high post-promotional APR.

The mathematical discipline of structured debt elimination creates financial skills that extend beyond this single debt payoff. The budgeting, tracking, and payment habits you develop during this process become foundational tools for long-term wealth building and debt avoidance.

Common Balance Transfer Mistakes

Even mathematically sound balance transfer strategies fail when cardholders make predictable execution errors. Understanding these mistakes prevents costly outcomes.

Missing the Promotional Period Deadline

The most expensive mistake is carrying a remaining balance when the 0% promotional period expires. The moment the promotion ends, any remaining balance immediately begins accruing interest at the card’s regular APR (typically 20-29%).

Mathematical impact: A $3,000 remaining balance at 24.99% APR costs approximately $750 in interest over the next year, eliminating the savings you achieved during the promotional period.

Prevention: Calculate your required monthly payment on day one and add a 10-15% safety margin. Set calendar alerts at 90, 60, and 30 days before the promotional period ends to verify you’re on track for complete payoff.

Ignoring the Transfer Fee in Your Payoff Calculation

Many cardholders calculate their required monthly payment by dividing only the transferred balance by the promotional period, forgetting to include the 3-5% transfer fee in the total amount owed.

Example error: $10,000 balance ÷ 18 months = $555.56 monthly payment (incorrect)

Correct calculation: ($10,000 + $300 fee) ÷ 18 months = $572.22 monthly payment

This $16.66 monthly difference results in a $300 remaining balance when the promotional period ends, exactly the amount of the forgotten transfer fee, now accruing 24%+ interest.

Prevention: Always add the transfer fee to your balance before calculating your required monthly payment.

Continuing to Use Old Credit Cards

Paying off old cards through a balance transfer creates available credit on those accounts. Using this newly available credit to make new purchases defeats the entire purpose of the transfer; you’ve simply moved debt around while maintaining or increasing your total debt load.

Behavioral trap: The psychological relief of seeing zero balances on old cards often triggers spending behavior: “I have available credit again, so I can afford this purchase.”

Prevention: Remove old cards from your wallet and online shopping accounts. If you lack spending discipline, consider closing old accounts after confirming the transfer completed, accepting the minor credit score impact to prevent debt reaccumulation.

Making New Purchases on the Balance Transfer Card

Most balance transfer cards charge regular APR (18-29%) on new purchases immediately, even during the 0% balance transfer promotional period. Payment allocation rules typically direct your payments to the lowest-APR balance first (the transferred balance), allowing high-interest purchase balances to grow.

Mathematical trap: You make a $500 purchase on your balance transfer card. Your $600 monthly payment goes entirely to the 0% transferred balance, while the $500 purchase accrues 24% APR. After one month, you owe $510 on the purchase ($500 + $10 interest), and this balance continues growing until you pay off the entire transferred balance.

Prevention: Establish a zero-purchase policy on your balance transfer card. Use a different card for necessary purchases or switch to debit/cash to maintain spending awareness.

Making Only Minimum Payments

Balance transfer cards typically require minimum payments of only 2-3% of your balance, far below what’s needed to eliminate the debt during the promotional period.

Example: $10,000 balance with 2% minimum payment = $200 first month. After 18 months of minimum payments, you’ll still owe approximately $6,500, which immediately begins accruing 24%+ interest.

Prevention: Ignore the minimum payment amount on your statement. Calculate and pay your required monthly payment based on your promotional period length (total balance ÷ promotional months).

Transferring Balances Between Cards From the Same Issuer

Most credit card issuers prohibit balance transfers between their own cards. Attempting to transfer a Chase balance to a different Chase card will be declined, wasting your time and potentially triggering a hard credit inquiry without any benefit.

Prevention: Before applying, verify the issuer is different from your current high-interest cards. You cannot transfer a balance from one card to another card issued by the same bank.

Applying for Multiple Balance Transfer Cards Simultaneously

Each balance transfer card application triggers a hard credit inquiry. Applying for 3-4 cards within a short period can reduce your credit score by 20-40 points and signal financial distress to issuers, potentially resulting in denials or reduced credit limits.

Prevention: Research carefully and apply for only 1-2 cards that best match your needs. If denied, wait 3-6 months before applying for another card to allow your credit score to recover.

Failing to Continue Payments on Old Cards During Transfer Processing

Balance transfers take 7-21 days to process. If your payment due date on your old card occurs during this processing window and you don’t make the payment (assuming the transfer will cover it), you’ll incur a late payment fee and potentially a penalty APR.

Mathematical impact: A single 30-day late payment can reduce your credit score by 60-110 points and trigger a penalty APR of 29.99% on any remaining balance.

Prevention: Continue making at least minimum payments on your old cards until you receive confirmation that the balance transfer completed and posted to those accounts.

Not Reading the Fine Print on Promotional Terms

Some offers advertise “0% APR” but actually provide deferred interest promotions. Under deferred interest terms, if you don’t pay off the entire balance before the promotional period ends, you owe retroactive interest on the entire original balance from day one.

Mathematical disaster: A $10,000 balance with 18 months deferred interest at 24% APR. You pay off $9,000 but carry a $1,000 balance when the period ends. You now owe a $1,000 remaining balance plus approximately $3,600 in retroactive interest on the original $10,000—for a total of $4,600.

Prevention: Carefully read the terms and conditions. Verify you’re receiving a true 0% APR promotional offer, not a deferred interest promotion. True 0% APR only charges interest on remaining balances going forward, never retroactively.

Avoiding these common mistakes requires upfront mathematical planning, disciplined execution, and careful attention to promotional terms and payment deadlines. The difference between successful and failed balance transfer execution often comes down to these preventable errors rather than the quality of the offer itself.

💳 Balance Transfer Savings Calculator

Calculate your potential savings and required monthly payment

📊 Your Balance Transfer Analysis

Conclusion

Balance transfer credit cards represent a mathematically powerful tool for eliminating high-interest debt when used with precision and discipline. The core advantage is straightforward: pausing interest accumulation for 12-21 months allows you to direct 100% of your payments toward principal reduction, potentially saving thousands of dollars compared to paying down debt at 20-29% APR.

However, this strategy only delivers results when paired with a structured payoff plan that eliminates the full balance before the promotional period expires. The mathematical requirements are non-negotiable: calculate your required monthly payment (total balance including fees ÷ promotional months), add a 10-15% safety margin, automate payments, and maintain zero new purchases on the transfer card.

Balance transfers work best for financially stable individuals with temporary high-interest debt, good credit scores (670+), and realistic payoff timelines of 6-18 months. They work poorly for individuals with ongoing spending problems, unstable income, or debt loads that require 24+ months to eliminate.

The decision to pursue a balance transfer requires an honest assessment of your financial discipline and a realistic evaluation of your repayment capacity. The best promotional offer means nothing if you lack the behavioral discipline to execute the payoff plan successfully.

Related Guides

Deepen your understanding of credit management and debt strategies with these resources:

- Credit Cards – Comprehensive guide to how credit cards work, rewards optimization, and responsible usage

- Credit Utilization Guide – Master the second-most important credit score factor with mathematical precision

- APY vs APR – Understand the critical difference between these interest rate calculations

- 50/30/20 Rule Budgeting – Build a sustainable budget framework that prevents future debt accumulation

- Credit Score – Learn how credit scoring works and strategies to optimize your score

Disclaimer

This article provides educational information about balance transfer credit cards and debt management strategies. It does not constitute financial advice, credit counseling, or recommendations for specific financial products.

Credit card terms, promotional offers, fees, and APRs vary by issuer and change frequently. Always review current terms and conditions directly from card issuers before applying. Your individual results will depend on your credit score, income, debt load, spending behavior, and financial discipline.

Balance transfers involve financial risk, including potential credit score impact, promotional period expiration with remaining balances, and accumulation of new debt. Carefully assess your financial situation and repayment capacity before pursuing a balance transfer strategy.

For personalized financial guidance, consult a qualified financial advisor or credit counselor who can evaluate your specific circumstances.

Author Bio

Max Fonji is the founder of The Rich Guy Math, a data-driven financial education platform that explains the math behind money with precision and clarity. With a background in financial analysis and a commitment to evidence-based investing principles, Max translates complex financial concepts into actionable strategies for wealth building.

Max’s approach combines analytical rigor with educational accessibility, helping readers understand not just what to do with their money, but why specific strategies work through mathematical proof and logical reasoning. His work focuses on compound growth, risk management, valuation principles, and the cause-and-effect relationships that drive long-term financial success.

Through The Rich Guy Math, Max provides beginner to intermediate investors with the financial literacy foundation needed to make informed decisions about credit, debt, investing, and wealth accumulation based on data rather than hype.

References

[1] Federal Reserve. “Consumer Credit – G.19.” Federal Reserve Statistical Release. https://www.federalreserve.gov/releases/g19/current/

[2] Consumer Financial Protection Bureau. “What is a balance transfer?” CFPB Consumer Resources. https://www.consumerfinance.gov/

[3] FICO. “What’s in my FICO Scores?” myFICO Credit Education. https://www.myfico.com/credit-education/whats-in-your-credit-score

[4] Federal Trade Commission. “Credit and Your Consumer Rights.” FTC Consumer Information. https://consumer.ftc.gov/articles/credit-and-your-consumer-rights

[5] Office of the Comptroller of the Currency. “Credit Cards: Know the Costs.” OCC Consumer Resources. https://www.occ.gov/topics/consumers-and-communities/consumer-protection/index-consumer-protection.html

FAQs

Can I transfer balances from multiple credit cards to one balance transfer card?

Yes, most issuers allow you to transfer balances from multiple cards during the application process or shortly after approval. You’ll need to provide the account numbers and transfer amounts for each card.

The total of all balance transfers plus fees must stay within your approved credit limit on the new card. Each transfer usually carries a separate 3%–5% balance transfer fee based on the amount transferred.

Consolidating multiple balances into one card simplifies payments and allows you to apply the 0% promotional APR to all transferred debt at the same time.

Does a balance transfer hurt my credit score?

Balance transfers can cause a short-term dip in your credit score but often lead to long-term improvement if managed correctly.

The initial application triggers a hard inquiry (typically a 5–10 point drop). Transferring a large balance may temporarily raise your credit utilization if your new credit limit is lower than your previous combined limits.

As you pay down the balance and maintain on-time payments, utilization improves and payment history strengthens. Many people see a net gain of 20–50+ points over 12–18 months.

Can I transfer a balance from a card issued by the same bank?

No. Most issuers do not allow balance transfers between cards issued by the same bank. For example, you can’t transfer a Chase balance to another Chase card or a Capital One balance to another Capital One card.

This rule exists because the issuer gains no advantage by moving debt between its own products. Your balance transfer card must come from a different bank than the card carrying the debt.

What happens if I don’t pay off the balance before the promotional period ends?

Any remaining balance begins accruing interest at the card’s regular APR, typically between 18% and 29%, once the promotional period ends.

This interest applies going forward, not retroactively, unless the promotion uses deferred interest. For example, carrying a $2,000 balance at a 24% APR can result in roughly $480 in interest over the next year.

Failing to pay off the balance before the promotion ends can significantly reduce or eliminate your interest savings.

Can I make new purchases on a balance transfer card?

While allowed, making new purchases on a balance transfer card is usually a bad idea. New purchases typically accrue interest immediately at the card’s regular APR.

Credit card payment rules usually apply your payments to the lowest-interest balance first (the 0% transferred balance), allowing higher-interest purchase balances to grow.

Best practice: avoid all new purchases on your balance transfer card until the transferred balance is fully paid off.

How long does a balance transfer take to process?

Balance transfers usually take 7–14 business days to complete, though some can take up to 21 days depending on the issuers involved.

Continue making at least the minimum payments on your old cards during this time to avoid late fees and credit score damage.

Once complete, confirm that the payment posted to your old accounts and that your new card reflects the transferred balance plus fees. Your promotional period starts when your account opens, not when the transfer finishes.

Related posts:

Credit Utilization Ratio Explained: What It Is, How It Works, And How To Improve It

Credit Utilization Ratio Explained: What It Is, How It Works, And How To Improve It

How Long Do Late Payments Stay on Credit Report? The Complete 7-Year Timeline Explained

How Long Do Late Payments Stay on Credit Report? The Complete 7-Year Timeline Explained

Statement Balance: What It Is and How It Works Complete Guide

Statement Balance: What It Is and How It Works Complete Guide

Statement Balance vs Current Balance: Which One Should You to Pay

Statement Balance vs Current Balance: Which One Should You to Pay

How Credit Cards Work: Beginner’s Step-By-Step Guide

How Credit Cards Work: Beginner’s Step-By-Step Guide

How Long Does It Take to Build Credit? Real Timeline Explained

How Long Does It Take to Build Credit? Real Timeline Explained