A “beginner” in the credit card world typically means someone with limited or no credit history, or someone new to managing revolving credit. This might include recent graduates, young adults establishing independence, or anyone building credit for the first time. The best credit cards for beginners prioritize simple approval requirements, straightforward terms, and features that support responsible credit building rather than complex reward structures.

Picking the right first card matters more than many realize. Your initial credit card establishes your payment history, influences your credit utilization ratio, and sets the foundation for your entire credit profile. A poor choice can lead to unnecessary fees, confusing terms, or missed opportunities to build credit effectively.

This comprehensive guide will help you understand what makes a card suitable for beginners, how to evaluate your options, and which specific cards offer the best combination of accessibility, value, and credit-building potential in 2026. Whether you’re considering a secured card to establish credit or an unsecured card with beginner-friendly features, you’ll find clear, actionable guidance to make an informed decision.

For foundational information before diving into specific cards, explore our credit basics guide to understand how credit cards work.

Key Takeaways

- Beginner cards prioritize accessibility over premium rewards, focusing on simple approval requirements, low or no annual fees, and credit-building tools rather than complex point systems

- Secured cards remain the most reliable path for those with no credit history, requiring a refundable security deposit that becomes your credit limit while reporting to all three credit bureaus

- Your first card’s impact on your credit score depends primarily on payment history (35%) and credit utilization (30%), making on-time payments and keeping balances below 30% of your limit critical

- The best starter cards in 2026 offer $0 annual fees with straightforward cash back structures (1.5%-2% flat rate) rather than rotating categories that require activation and tracking

- Common beginner mistakes include carrying balances month-to-month, opening multiple cards simultaneously, and ignoring the difference between statement balance and minimum payment—avoiding these pitfalls matters more than choosing the “perfect” card

How to Choose Your First Credit Card

Selecting your first credit card requires evaluating several key factors that align with your current financial situation and credit-building goals.

Credit Score Range Needed

Different cards target different credit profiles. Understanding where you stand helps narrow your options:

- No credit history or scores below 580: Secured cards or student cards designed for first-time users

- Fair credit (580-669): Entry-level unsecured cards with basic rewards

- Good credit (670-739): Broader selection, including cards with better rewards and lower APRs

Check your credit score before applying. Many banks and credit monitoring services offer free score checks that won’t impact your credit.

Annual Fees

For beginners, annual fees rarely justify their cost. The best credit cards for beginners typically charge $0 annual fees, allowing you to build credit without ongoing costs. Premium cards with annual fees ($95-$550+) generally require good-to-excellent credit and offer benefits that matter more to experienced users.

APR Expectations

Annual Percentage Rate (APR) represents the interest you’ll pay on carried balances. Beginner cards typically feature:

- Regular APRs: 16.99%-24.99% variable

- Introductory 0% APR periods: 12-18 months on purchases and/or balance transfers (available on some beginner-friendly cards)

While APR matters, planning to pay your full statement balance monthly makes the rate less critical. If you anticipate carrying balances initially, prioritize cards with lower APRs or introductory 0% periods.

Rewards Suitability

Beginners benefit most from simple reward structures:

- Flat-rate cash back (1.5%-2% on all purchases): No category tracking required

- Basic tiered rewards (3% dining, 2% groceries, 1% everything else): Simple, automatic categories

- Rotating 5% categories: Require quarterly activation and tracking

- Complex point systems: Better suited for experienced users who maximize redemption value

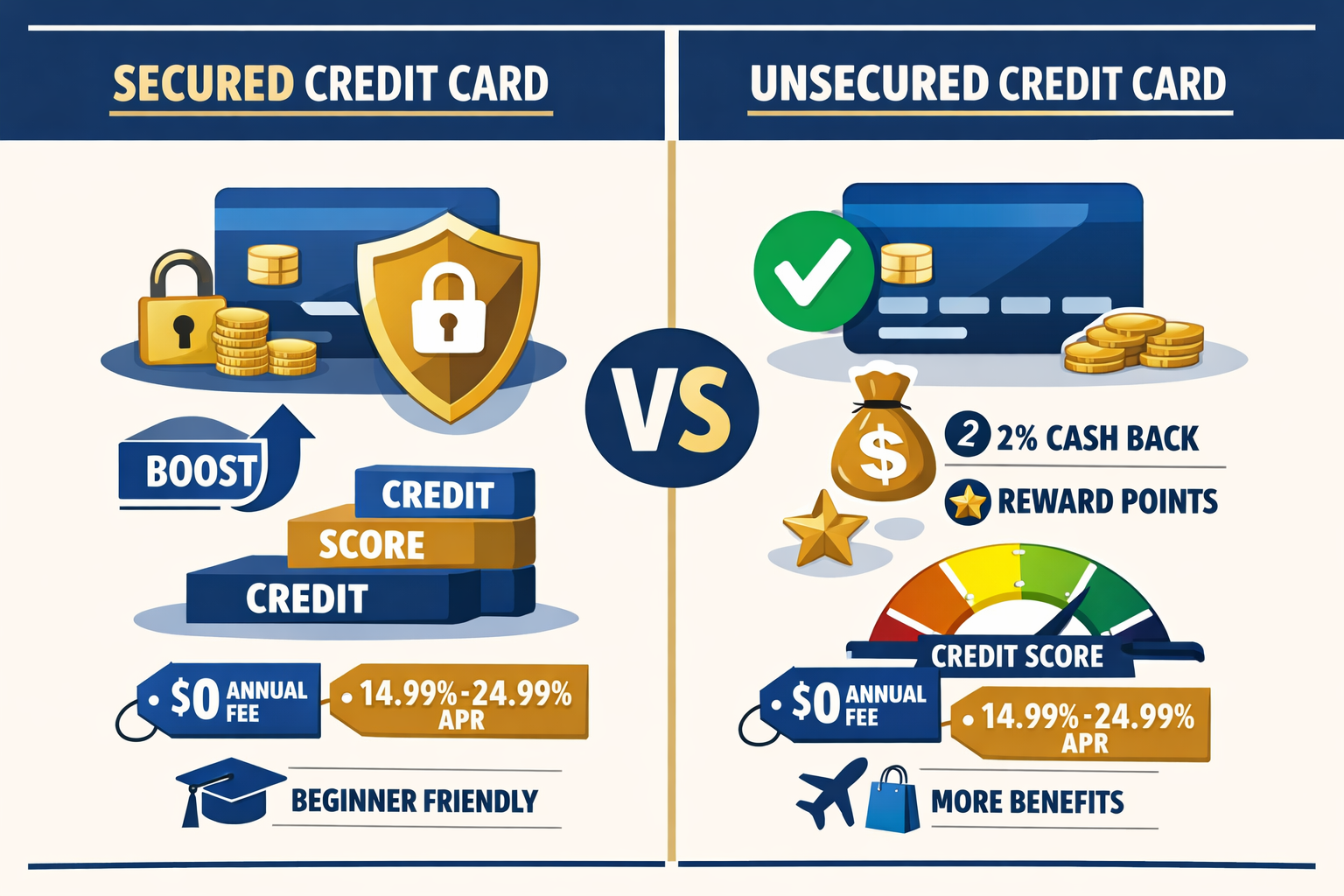

Secured vs Unsecured Cards

This fundamental choice depends on your credit history:

| Card Type | Best For | How It Works | Credit Building |

|---|---|---|---|

| Secured | No credit history or rebuilding credit | Standard credit reporting typically offers rewards and benefits | Reports to all three bureaus; many issuers review for upgrade to unsecured after 6-12 months |

| Unsecured | Fair credit or better, students with limited history | No deposit required; approval based on creditworthiness | Standard credit reporting; typically offers rewards and benefits |

Secured cards aren’t inferior; they’re strategic tools for establishing credit when unsecured approval isn’t likely. Many beginners successfully use secured cards for 6-12 months before transitioning to unsecured options with better benefits.

What Makes a Good Beginner Credit Card

Not all entry-level cards serve beginners equally well. The strongest options share specific characteristics that support credit building while minimizing complexity and costs.

Simple Approval Requirements

The best credit cards for beginners feature accessible approval standards that don’t require extensive credit history or high scores. These cards recognize that everyone starts somewhere and design their underwriting accordingly.

Look for cards explicitly marketed to students, first-time users, or those building credit. These typically accept applicants with:

- Limited or no credit history

- Fair credit scores (580-669)

- Modest income levels (including student income, part-time work, or household income for those under 21)

Avoid applying for premium travel cards, high-tier cash back cards, or business cards as your first card. These require good-to-excellent credit (670+) and often result in hard inquiries that temporarily lower your score without approval.

Student cards deserve special mention. Issuers like Capital One and Discover offer student-specific cards with relaxed approval requirements, recognizing that students typically have limited credit history but represent lower risk due to educational enrollment.

No or Low Annual Fee

Annual fees create ongoing costs that rarely benefit beginners. A $0 annual fee card allows you to:

- Build credit indefinitely without cost pressure to use the card

- Maintain the account long-term, extending your average credit age

- Avoid the calculation of whether rewards offset the fee

Some beginner cards charge modest annual fees ($25-$39), often for secured cards. These remain acceptable if the card offers clear credit-building features like:

- Automatic reviews for credit line increases

- Graduation paths to unsecured cards

- Free credit score monitoring

- Fraud protection and account alerts

The Capital One Platinum card exemplifies this approach—$0 annual fee with access to higher credit limits after making on-time payments for over five months, making it the most popular no-annual-fee card among Bankrate users as of February 2026.[5]

No Complex Rewards Structures

Beginners benefit from straightforward rewards that don’t require strategy, activation, or category management.

Ideal beginner reward structures:

- Flat-rate cash back: The Capital One Quicksilver Cash Rewards Credit Card offers 1.5% cash back on all purchases with no category tracking or activation required.[1]

- Simple tiered categories: Automatic elevated rates on common spending (dining, gas, groceries) without quarterly changes

- Matched rewards programs: The Discover it® Secured Credit Card matches all cash back earned in the first year—a unique incentive for responsible use that doubles your rewards automatically.[2]

Avoid as a beginner:

- Rotating 5% categories requiring quarterly activation (like Chase Freedom Flex℠, though it’s recommended for beginners “willing to learn quickly”)[2]

- Point systems requiring the transfer of knowledge for maximum value

- Complex redemption tiers with varying point values

The Citi Double Cash® Card demonstrates perfect simplicity: 2% cash back on all purchases (1% when you buy, 1% when you pay), with unlimited earning and no categories to track.[1][6]

Tools & Support for Credit Building

The strongest beginner cards include educational resources and monitoring tools that help you understand and improve your credit.

Essential features:

- Free credit score access: Monthly FICO or VantageScore updates help you track progress

- Credit monitoring alerts: Notifications about score changes, new accounts, or unusual activity

- Educational resources: Guides explaining credit utilization, payment timing, and score factors

- Mobile app functionality: Easy payment scheduling, spending tracking, and account management

Many issuers now provide these tools standard. Discover, Capital One, and Chase offer particularly robust mobile apps with credit education sections, spending categorization, and customizable alerts.

Upgrade pathways matter too. Secured cards should offer clear paths to unsecured status. The Discover it® Secured Card, for example, automatically reviews accounts for upgrade potential after eight months of responsible use, returning your security deposit when you graduate to unsecured status.

Customer service accessibility helps beginners navigate questions about payments, fees, or credit building. Look for 24/7 phone support, live chat options, and comprehensive FAQ sections.

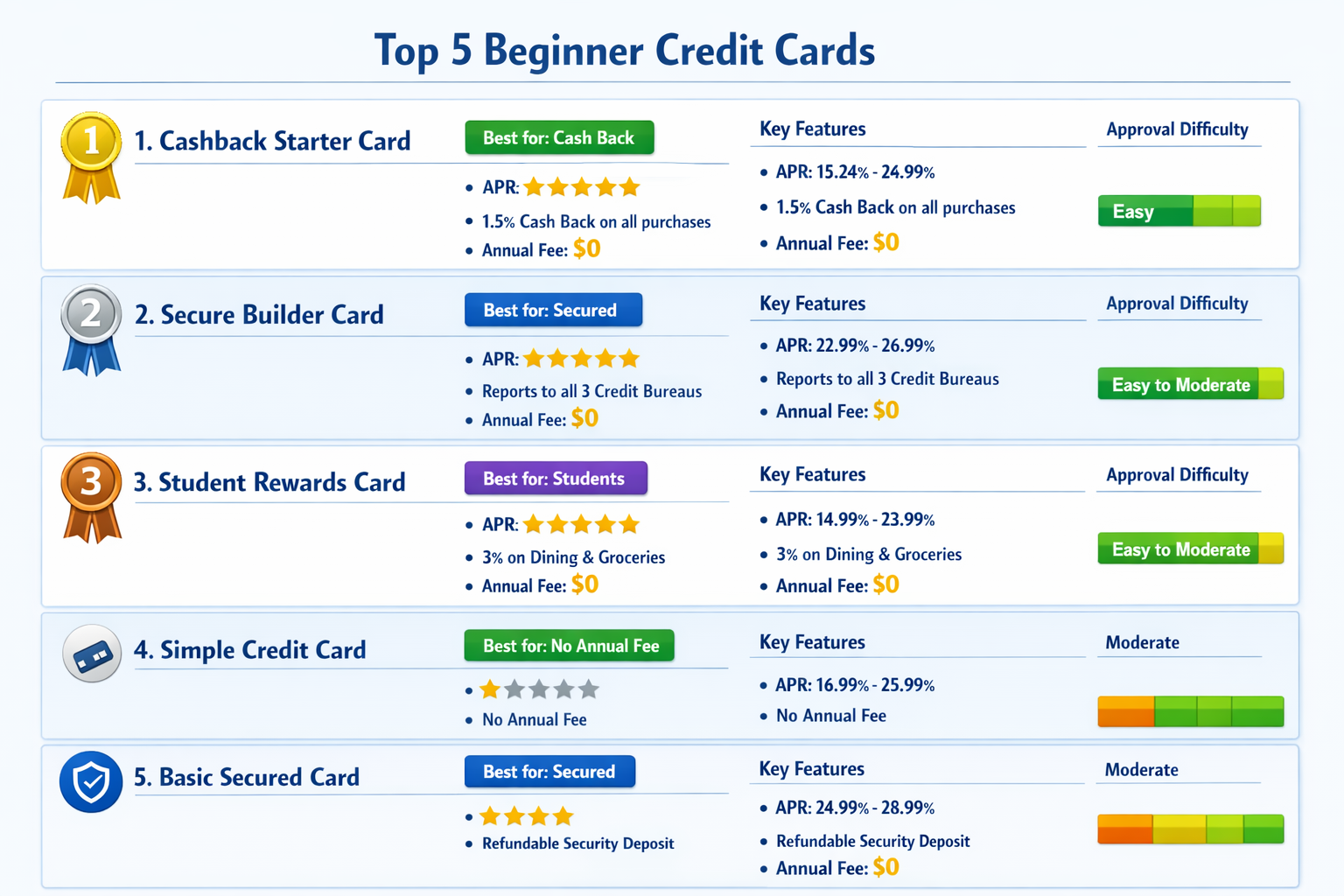

Top Best Credit Cards for Beginners in 2026 (Ranked)

Based on approval accessibility, fee structures, rewards simplicity, and credit-building features, these cards represent the strongest options for beginners in 2026.

| Rank | Card Name | Best For | APR Range | Rewards | Annual Fee | Key Feature |

|---|---|---|---|---|---|---|

| 🥇 | Chase Freedom Unlimited® | All-around flexibility | 15.99%-24.99% variable | 1.5%-5% cash back | $0 | $200 bonus after $500 spend; 0% intro APR for 15 months[4][6] |

| 🥈 | Capital One Quicksilver Cash Rewards | Simple cash back | 16.99%-26.99% variable | 1.5% cash back on all purchases | $0 | No category tracking; $200 bonus after $500 spend[1] |

| 🥉 | Discover it® Secured | Building/rebuilding credit | 28.24% variable | 2% at gas stations & restaurants (up to $1,000/quarter), 1% elsewhere | $0 | Cashback Match™ doubles first-year rewards; automatic upgrade reviews[2] |

| 4 | Citi Double Cash® Card | Maximum simple cash back | 18.24%-28.24% variable | 2% total (1% purchase + 1% payment) | $0 | $200 bonus after $1,500 spend in 6 months; unlimited earning[1][6] |

| 5 | Capital One Platinum | No-fee credit building | 30.49% variable | None | $0 | Access to higher limits after 5 months of on-time payments; most popular no-fee card[5] |

| 6 | Capital One VentureOne Rewards | Travel beginners | 19.99%-29.99% variable | 1.25 miles per dollar | $0 | 20,000 bonus miles after $500 spend; simple flat earning[1] |

| 7 | Capital One Journey Student Rewards | College students | 26.99%-30.99% variable | 1% cash back (1.25% with on-time payments) | $0 | Designed for first-time financial independence[2] |

Detailed Card Breakdowns

Chase Freedom Unlimited® leads as the most versatile beginner option. The 0% intro APR for 15 months on purchases provides breathing room for larger initial expenses, while the straightforward 1.5% cash back on all purchases (with 5% on travel through Chase, 3% on dining and drugstores) offers solid returns without complexity.[4][6] The $200 bonus after spending just $500 in three months makes it immediately rewarding for new users.

Capital One Quicksilver Cash Rewards Credit Card excels through pure simplicity. The flat 1.5% cash back structure requires zero category management, making it ideal for beginners who want rewards without strategy.[1] The identical $200 bonus threshold ($500 spend in three months) provides quick value, and Capital One’s credit monitoring tools help beginners track their progress.

Discover it® Secured Card stands alone among secured cards by offering the Cashback Match™ program—Discover automatically matches all cash back earned in your first year, effectively doubling your rewards.[2] This creates a strong incentive for responsible use while building credit. The card reports to all three credit bureaus and reviews accounts for an unsecured upgrade after eight months of on-time payments.

Citi Double Cash® Card provides the highest straightforward cash back rate at 2% total—1% when you purchase, 1% when you pay your bill.[1][6] This structure subtly encourages full payment (you only earn the second 1% when you pay), aligning rewards with healthy credit habits. The higher bonus threshold ($1,500 spend over six months versus three) suits beginners with moderate spending levels.

Capital One Platinum offers pure credit building without rewards complexity. As the most popular no-annual-fee card among Bankrate users in February 2026, it demonstrates that many beginners prioritize accessible approval and credit line growth over rewards.[5] After five months of on-time payments, Capital One automatically considers you for higher limits—valuable for improving credit utilization ratios.

For more detailed comparisons of these card types, see our guide on secured vs unsecured credit cards.

Secured vs Unsecured Cards for Beginners

Understanding the secured versus unsecured distinction helps beginners choose the right starting point based on their current credit profile.

Secured Credit Cards: The Foundation Builder

Secured cards require a refundable security deposit—typically $200-$2,500—that becomes your credit limit. This deposit protects the issuer against default risk, allowing them to approve applicants with no credit history or damaged credit.

How secured cards work:

- You submit a security deposit (often $200 minimum)

- The issuer sets your credit limit equal to your deposit

- You use the card normally, making purchases and payments

- The issuer reports your activity to credit bureaus monthly

- After 6-12 months of responsible use, many issuers review for an upgrade to unsecured status

- Upon upgrade or account closure in good standing, you receive your deposit back

Why secured cards excel for beginners with limited credit:

- Guaranteed approval pathway: Deposit eliminates most credit requirements

- Identical credit building: Reports to bureaus the same as unsecured cards

- Lower risk for first-time users: Your deposit limits potential debt

- Upgrade potential: Many convert to unsecured cards, returning your deposit while maintaining your account age

The Discover it® Secured Card exemplifies best-in-class secured cards with its Cashback Match™ program and $0 annual fee.[2] Unlike many secured cards that offer no rewards, Discover provides 2% cash back at gas stations and restaurants (up to $1,000 quarterly spend) and 1% on all other purchases—then doubles everything you’ve earned at the end of your first year.

Unsecured Credit Cards: The Standard Path

Unsecured cards require no deposit. Approval depends entirely on creditworthiness—your credit score, income, existing debts, and credit history.

When unsecured cards make sense for beginners:

- You have fair credit (580+) from being an authorized user on someone else’s account

- You’re a student with limited history, but an enrollment status

- You have thin credit (few accounts), but a positive payment history

- You want rewards and benefits from day one

Student cards bridge the gap, offering unsecured approval with relaxed requirements. The Capital One Journey Student Rewards card specifically targets college students with limited credit history, offering 1% cash back (boosted to 1.25% when you pay on time) and credit-building tools designed for first-time financial independence.[2]

Transitioning from Secured to Unsecured

Most secured card users should plan for 6-12 months of responsible use before requesting an upgrade or applying for unsecured cards:

- Make every payment on time: Payment history accounts for 35% of your credit score

- Keep utilization below 30%: Use less than 30% of your credit limit monthly

- Wait for automatic review: Many issuers (Discover, Capital One) automatically review for upgrades

- Request manual review: After 6+ months, contact your issuer to request an unsecured conversion

- Apply for unsecured cards: Once your score reaches 650+, consider adding an unsecured card while keeping your secured card open (for credit age)

The key insight: secured cards aren’t inferior products—they’re strategic tools. Many people with excellent credit started with secured cards. The goal isn’t avoiding secured cards; it’s using them effectively to access better unsecured options within 6-12 months.

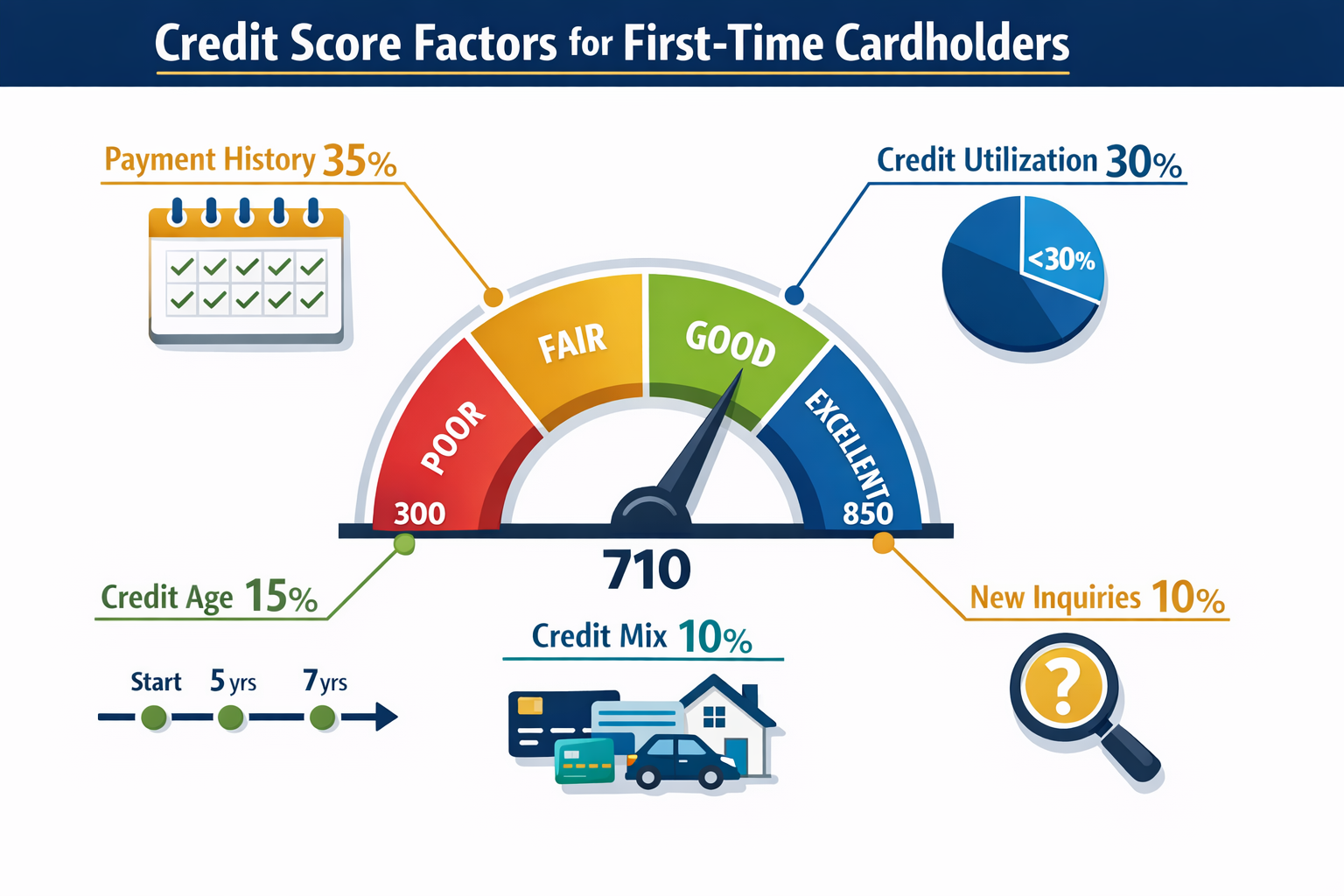

How Your First Card Affects Your Credit Score

Your first credit card creates your credit history and significantly influences your score through five key factors. Understanding these helps beginners maximize credit-building potential.

Payment History (35% of Your Score)

Payment history represents the single most important factor in credit scoring. Every monthly payment—whether full, minimum, or anything between—gets reported to credit bureaus as on-time or late.

What matters:

- Payments received by due date: Reported as on-time, building positive history

- Payments 30+ days late: Reported as delinquent, severely damaging scores

- Payments 1-29 days late: Not reported to bureaus but may incur late fees

Beginner strategy: Set up automatic minimum payments to ensure you never miss a due date, then manually pay the remaining balance. This creates a safety net while you establish payment habits.

One late payment can drop a beginner’s score 60-100 points and remain on your report for seven years. The impact diminishes over time, but avoiding late payments entirely sets the strongest foundation.

Credit Utilization Ratio (30% of Your Score)

Credit utilization measures how much of your available credit you’re using. It’s calculated both per-card and across all cards combined.

Formula: (Total Credit Card Balances ÷ Total Credit Limits) × 100

Optimal ranges:

- Under 10%: Excellent for score maximization

- 10-30%: Good, maintains healthy scores

- 30-50%: Fair, begins negatively impacting scores

- Over 50%: Poor, significantly damages scores

Example: If your first card has a $500 limit and you carry a $150 balance, your utilization is 30%—right at the threshold. Paying down to $50 (10% utilization) would improve your score.

Beginner challenges: Low initial credit limits make utilization management difficult. A $300 limit means spending over $90 pushes you above 30%. Strategies include:

- Making multiple payments per month before the statement date

- Requesting a credit limit increase after 6 months of on-time payments

- Keep spending low relative to your limit

- Adding a second card to increase total available credit (after 6-12 months)

For detailed strategies on managing this crucial factor, read our complete guide on the credit utilization ratio.

Length of Credit History (15% of Your Score)

Credit age measures how long you’ve had credit accounts. Scores consider:

- Age of your oldest account

- Age of your newest account

- Average age across all accounts

Why your first card matters permanently: Your first card becomes your oldest account, anchoring your credit age. Closing it later shortens your history and can drop your score.

Beginner strategy: Choose the first card you can keep forever. Since age matters, prioritize $0 annual fee cards that you’ll never need to close for cost reasons. Even after you add premium cards later, keeping your first card open (with occasional small purchases to prevent closure) maintains your maximum credit age.

Credit Mix (10% of Your Score)

Credit mix examines the variety of credit types you manage—credit cards, installment loans (auto, student, personal), mortgages, etc.

For beginners, this factor matters least initially. Having only one credit card is perfectly fine. As your credit journey progresses, naturally adding different credit types (student loans, car loans, and eventually mortgages) will improve this factor without forcing it.

New Credit Inquiries (10% of Your Score)

Each credit card application generates a “hard inquiry” that appears on your credit report and slightly lowers your score (typically 5-10 points) for 12 months.

Beginner guidelines:

- Limit applications to 1-2 cards in your first year

- Space applications at least 6 months apart

- Avoid applying for multiple cards simultaneously (appears risky to lenders)

- Use pre-qualification tools (soft pulls that don’t affect your score) before applying

The impact of inquiries fades quickly—they stop affecting your score after 12 months and disappear from your report after 24 months. However, multiple inquiries in a short period signal risk to lenders and can result in denials.

The Compound Effect

These factors work together. Your first card’s impact extends beyond individual factors:

- On-time payments build history while keeping utilization low maximizes scoring

- Maintaining your first card long-term extends credit age while adding payment history months

- Responsible use leads to credit limit increases, making utilization management easier

Most beginners see their scores rise from the 600s to the 700s within 12-18 months of responsible first-card use—opening access to premium cards, better interest rates on loans, and improved financial opportunities.

Common Mistakes New Cardholders Make

Beginners often stumble into predictable traps that damage credit, create unnecessary costs, or slow credit-building progress. Avoiding these mistakes matters more than choosing the “perfect” card.

Carrying a Balance Month-to-Month

The mistake: Many beginners believe that carrying a small balance “builds credit faster” or that you must pay interest to improve your score.

The reality: This myth costs beginners hundreds in unnecessary interest annually. Credit bureaus don’t distinguish between full payment and partial payment—both count as “on-time” if you meet the minimum by the due date.

The fix: Pay your full statement balance every month before the due date. This builds an identical credit history while avoiding all interest charges. The only time to carry a balance is during a genuine 0% APR promotional period for a planned large purchase.

Example cost: Carrying a $500 balance on a card with 22% APR costs approximately $110 in annual interest, money that provides zero credit-building benefit.

Only Paying Minimum Payments

The mistake: Making only minimum payments (typically 1-3% of your balance) feels manageable, but creates a debt spiral.

The math: A $1,000 balance at 20% APR with $25 minimum payments takes 5+ years to pay off and costs over $1,000 in interest.

The fix: Treat your credit card like a debit card—only charge what you can pay in full when the statement arrives. If you’ve already accumulated a balance, pay as much above the minimum as possible each month, prioritizing this debt above non-essential spending.

Minimum payments cover mostly interest, barely touching principal. This keeps you in debt indefinitely while damaging your credit through high utilization.

Not Understanding Fees

The mistake: Beginners often miss fee disclosures and get surprised by charges for:

- Late payments ($25-$40 per occurrence)

- Returned payments ($25-$35)

- Foreign transactions (1-3% of purchase amount)

- Cash advances (3-5% fee plus immediate interest)

- Over-limit fees (rare since CARD Act, but possible if you opt in)

The fix: Read your card agreement’s fee schedule. Set up payment reminders or autopay to avoid late fees. Never use your credit card for cash advances—the fees and immediate interest (no grace period) make this extremely expensive.

Hidden cost example: A $30 late fee on a $200 balance represents 15% of what you owe—far exceeding any rewards you might earn.

Opening Too Many Cards Too Soon

The mistake: Enthusiastic beginners sometimes apply for multiple cards within months, thinking that cards build credit faster.

The problems:

- Multiple hard inquiries lower your score

- Shortened average account age

- Lenders view rapid account opening as risky behavior

- Harder to manage multiple payment dates and terms

- Temptation to overspend across multiple cards

The fix: Start with one card. Use it responsibly for 6-12 months, establishing payment history and learning credit management. Then, if desired, add a second card strategically (perhaps a secured card graduating to unsecured, or adding a rewards card once you have good credit).

Ideal timeline:

- Months 0-6: First card, focus on on-time payments and low utilization

- Months 6-12: Request a credit limit increase on the first card

- Months 12+: Consider adding a second card if needed for rewards or backup

Using Cards Without Tracking Spending

The mistake: Credit cards’ delayed payment creates psychological distance from spending. Beginners often overspend because purchases don’t feel “real” until the bill arrives.

The consequences:

- Balances exceeding the ability to pay in full

- High utilization ratios damage credit scores

- Stress and potential debt accumulation

The fix: Track spending in real-time using:

- Your card issuer’s mobile app (most categorize spending automatically)

- Budgeting apps that sync with your card (Mint, YNAB, PocketGuard)

- Simple spreadsheet logging each purchase

- Mental running total if you make a few purchases

Beginner-friendly approach: For the first 3-6 months, use your card only for one category of spending you already budget for (groceries, gas, or subscriptions). Pay it off immediately or weekly. This builds the habit of treating credit like cash while earning rewards.

Ignoring Your Credit Card Statement

The mistake: Many beginners pay the bill without reviewing the statement details.

What you miss:

- Fraudulent or incorrect charges

- Fee assessments you could dispute

- Understanding of your spending patterns

- Important notices about rate changes or terms

The fix: Spend 5 minutes reviewing each statement before paying.

- Verify every charge is legitimate

- Check for unexpected fees

- Note your statement balance versus the minimum payment

- Review your available credit and utilization

- Look for issuer notices or messages

Catching fraudulent charges early (within 60 days) ensures full protection under federal law. After 60 days, your liability increases.

Closing Your First Card

The mistake: After getting approved for “better” cards, beginners sometimes close their first card, especially if it has no rewards.

The damage:

- Reduces total available credit (increases utilization ratio)

- Eventually shortens credit history when the closed account ages off your report (10 years)

- Eliminates your oldest account, reducing average credit age

The fix: Keep your first card open indefinitely, especially if it has no annual fee. Make a small purchase every 3-6 months to keep it active (many issuers close cards after 12 months of inactivity). Pay it off immediately.

Exception: If your first card has an annual fee you can’t justify, try requesting a product change to a no-fee card from the same issuer before closing. This often preserves your account age while eliminating the fee.

Credit Card Terms Every Beginner Should Know

Understanding key terminology helps beginners navigate card agreements, avoid fees, and maximize benefits.

Annual Percentage Rate (APR)

The yearly interest rate charged on carried balances. Credit cards typically have variable APRs that fluctuate with the prime rate.

Types of APRs:

- Purchase APR: Rate on regular purchases (15.99%-24.99% typical for beginners)

- Balance transfer APR: Rate on transferred balances from other cards

- Cash advance APR: Rate on cash withdrawals (usually higher, 25%-29.99%)

- Penalty APR: Elevated rate triggered by late payments (up to 29.99%)

Key insight: APR only matters if you carry a balance. Pay in full monthly, and you’ll never pay interest, regardless of APR. However, lower APRs provide a safety margin for unexpected situations.

For a complete guide on APR, see our credit card apr explained.

Grace Period

The time between your statement closing date and payment due date (typically 21-25 days) is during which no interest accrues on new purchases if you paid the previous balance in full.

How it works:

- Pay full statement balance by due date → maintain grace period → no interest on new purchases

- Carry any balance → lose grace period → immediate interest on all purchases until you pay in full for two consecutive months

Example: Your statement closes March 15 with a $500 balance. Your payment is due April 10. If you pay the full $500 by April 10, purchases made March 16-April 15 won’t accrue interest until the next due date. If you pay only $400, purchases start accruing interest immediately.

Billing Cycle

The period (usually 28-31 days) between credit card statements. Your billing cycle determines:

- Which purchases appear on which statement

- When your statement balance is calculated

- Your payment due date (typically 21-25 days after the cycle ends)

Why it matters for utilization: Credit bureaus typically receive your balance information on your statement closing date. Making payments before this date lowers the reported balance and improves your utilization ratio, even if you pay in full every month.

Minimum Payment

The smallest amount you can pay by the due date to keep your account in good standing. Typically calculated as:

- 1-3% of your statement balance, or

- $25-$35 (whichever is greater)

Critical understanding: Minimum payments are designed to maximize issuer profit, not help you pay off debt. They cover mostly interest with minimal principal reduction.

Example: $2,000 balance at 20% APR with $60 minimum payments takes 7+ years to pay off and costs over $2,000 in interest. Paying $100 monthly instead reduces payoff time to under 2 years and interest to about $400.

Annual Fee

A yearly charge for holding the card, regardless of usage. Ranges from $0 (most beginner cards) to $550+ (premium travel cards).

Beginner guidance: Avoid annual fees until you have established credit and can calculate whether rewards/benefits exceed the fee. The best credit cards for beginners typically charge $0 annually.

When fees make sense (later): A $95 annual fee card that provides $300 in annual benefits (travel credits, statement credits, high rewards on your spending) justifies the cost. But this calculation requires established spending patterns and credit card experience.

Rewards

Benefits earned on spending, typically in three forms:

Cash back: Percentage of purchases returned as statement credit or deposit (1%-5% typical)

- Flat rate: Same percentage on all purchases (1.5%-2%)

- Tiered: Different percentages by category (3% dining, 2% groceries, 1% other)

- Rotating: Categories change quarterly and require activation (5% on specific categories)

Points: Earned at fixed rates (1-5 points per dollar) with varying redemption values

- Transferable points: Can transfer to airline/hotel partners (often 1-2 cents per point value)

- Fixed-value points: Redeem through issuer portal (often 0.5-1 cent per point value)

Miles: Similar to points but typically travel-focused (airline miles, hotel points)

Beginner recommendation: Start with simple cash back. The Capital One Quicksilver’s flat 1.5% cash back requires no strategy, category tracking, or redemption optimization.[1] Graduate to more complex reward systems after mastering basic credit management.

Credit Limit

The maximum amount you can charge to your card at any time. Determined by the issuer based on your creditworthiness, income, and other factors.

Beginner ranges:

- Secured cards: $200-$2,500 (equal to your deposit)

- Unsecured beginner cards: $300-$1,500 initially

- Student cards: $500-$2,000 typically

Improving your limit: After 6-12 months of on-time payments, request increases or accept automatic increases. Higher limits improve your utilization ratio (assuming spending stays constant) and provide more flexibility.

Statement Balance vs Current Balance

Statement balance: Total amount owed when your billing cycle closed—this is what you should pay to avoid interest

Current balance: Total amount owed right now, including new purchases since your statement closed

Critical distinction: Pay your statement balance in full by the due date to avoid interest and maintain your grace period. Your current balance will be higher if you’ve made purchases since your statement closed, but those charges aren’t due until the next statement.

Authorization vs Posted Transaction

Authorization: Temporary hold when you make a purchase (reduces available credit immediately)

Posted transaction: Finalized charge that appears on your statement (usually 1-3 days after authorization)

Why it matters: Your available credit reflects authorizations immediately, but your statement balance only includes posted transactions. Gas stations and hotels often authorize more than the final charge, temporarily reducing your available credit.

🎯 Find Your Perfect Beginner Credit Card

Answer 4 quick questions to get personalized recommendations

✨ Your Personalized Recommendations

Conclusion

Choosing the best credit cards for beginners requires balancing accessibility, simplicity, and credit-building potential rather than chasing premium rewards or complex benefits. The right first card depends on your current credit situation: secured cards like the Discover it® Secured Card provide guaranteed approval and unique rewards for those with no history, while unsecured options like the Chase Freedom Unlimited® and Capital One Quicksilver offer straightforward cash back for those with fair credit or student status.[1][2][4][6]

The most important factors for beginners include:

- $0 annual fees that allow indefinite credit building without cost pressure

- Simple reward structures (flat 1.5%-2% cash back) that don’t require category management or activation

- Accessible approval requirements matched to your credit profile

- Credit-building tools like free score monitoring and educational resources

Your first card’s long-term impact extends beyond immediate rewards. Making on-time payments establishes the payment history that comprises 35% of your credit score, while managing utilization below 30% of your limit optimizes the 30% of your score tied to credit usage. Keeping your first card open indefinitely anchors your credit age, and responsible use creates the foundation for accessing better cards, lower loan rates, and improved financial opportunities.

Common beginner mistakes—carrying balances unnecessarily, making only minimum payments, opening multiple cards too quickly, and closing your first card—damage credit and create costs far exceeding any rewards earned. Avoiding these pitfalls matters more than choosing the “perfect” card from the rankings above.

Start with one card matched to your credit profile. Use it for purchases you’d make anyway, pay the full statement balance monthly, and keep utilization below 30%. After 6-12 months of responsible use, you’ll have established credit sufficient to qualify for better cards, request limit increases, or graduate from secured to unsecured status.

For more foundational information about how credit cards work and how to use them effectively, visit our comprehensive credit card basics guide.

The journey from credit beginner to experienced user takes patience and consistency, but your first card choice sets the trajectory. Choose wisely, use responsibly, and your credit profile will open doors for decades to come.

Disclaimer

This article provides educational information about credit cards for beginners and should not be considered financial advice. Credit card terms, rates, rewards, and approval requirements change frequently and vary by applicant. The cards mentioned represent examples based on publicly available information as of early 2026, but specific offers may differ when you apply. Annual Percentage Rates (APRs), fees, and rewards structures are subject to change without notice.

Your approval odds and specific terms depend on your individual credit profile, income, existing debts, and the issuer’s current underwriting standards. Pre-qualification tools provide estimates but don’t guarantee approval. Always review the complete terms and conditions, including the Schumer Box disclosure, before applying for any credit card.

Credit card usage involves financial risk. Carrying balances results in interest charges that can accumulate quickly at typical APRs of 15.99%-29.99%. Only charge amounts you can afford to pay in full by the due date. Late payments damage your credit score and may result in penalty APRs and fees.

The information in this article is current as of February 2026, but it may become outdated as issuers modify their products. Verify all details directly with card issuers before making financial decisions. This article contains references to specific credit card products for educational purposes and comparison—these references do not constitute endorsements or recommendations to apply for any particular card.

Consult with a qualified financial advisor or credit counselor for personalized guidance based on your specific financial situation, goals, and credit profile.

Author Bio

Max Fonji is the founder of The Rich Guy Math, a data-driven financial education platform that explains the mathematical principles behind wealth building and credit optimization. With expertise in financial analysis and credit scoring algorithms, Max translates complex financial concepts into actionable strategies for building long-term wealth.

His evidence-based approach to personal finance helps readers understand the quantitative relationships between credit decisions, investment returns, and financial outcomes. Max’s work focuses on empowering individuals with the mathematical knowledge needed to make optimal financial decisions throughout their wealth-building journey.

References

[1] Best First Credit Cards – https://thepointsguy.com/credit-cards/best-first-credit-cards/

[2] 2c55ee089202d65700d6b36373864e24 – http://oreateai.com/blog/the-best-credit-cards-for-beginners-your-guide-to-smart-choices/2c55ee089202d65700d6b36373864e24

[3] Best Credit Card For Beginners – https://entellusapparel.com/blog/best-credit-card-for-beginners/

[4] Best – https://www.nerdwallet.com/credit-cards/best

[5] Best No Annual Fee Cards – https://www.bankrate.com/credit-cards/rewards/best-no-annual-fee-cards/

[6] Credit Cards – https://www.creditkarma.com/credit-cards

[7] Best Travel Credit Cards for Beginners – https://www.ourfamilypassport.com/best-travel-credit-cards-beginners/

Frequently Asked Questions (FAQ)

Do beginner credit cards usually have rewards?

Yes. Many beginner credit cards offer simple cash back rewards, typically ranging from 1% to 1.5%. Some starter cards focus only on credit building, while a few secured cards also provide limited rewards. Flat-rate cash back cards are usually best for beginners because they’re easy to use and track.

Should I get a secured card first?

You should get a secured credit card if you have no credit history or a credit score below 580. If you have fair credit (580 or higher), student status, or authorized user history, you may qualify for unsecured beginner cards.

Secured cards are not inferior—they are stepping stones to better unsecured cards within 6 to 12 months of responsible use.

Does applying for a credit card hurt my credit?

Yes, slightly. A hard inquiry usually lowers your credit score by about 5 to 10 points temporarily. This impact fades within a few months and is usually outweighed by on-time payments and responsible usage.

Avoid applying for multiple credit cards at the same time to reduce approval risk.

What’s a good credit score to start applying?

You don’t need a credit score to qualify for secured or student credit cards.

- 580–669: Qualifies for basic unsecured beginner cards

- 670+: Access to better rewards and lower interest rates

If you have no credit score at all, start with a secured or student credit card.

Can I get a credit card with no credit history?

Yes. You can qualify for a credit card with no credit history by using:

- Secured credit cards

- Student credit cards

- Authorized user accounts

Many issuers also consider income and existing banking relationships during approval.

How long should I wait before applying for a second card?

Wait 6 to 12 months after opening your first credit card. This allows time to build payment history, improve your score, and increase approval odds for better cards.

Applying too quickly can reduce approval chances and temporarily lower your credit score.

What credit limit should I expect on my first card?

Most beginners start with a credit limit between $200 and $1,500. Secured credit cards usually match your deposit amount.

Credit limits commonly increase after 6 to 12 months of on-time payments and low utilization. Low starting limits are normal and not a negative signal.

Related posts:

Credit Utilization Ratio Explained: What It Is, How It Works, And How To Improve It

Credit Utilization Ratio Explained: What It Is, How It Works, And How To Improve It

How Long Do Late Payments Stay on Credit Report? The Complete 7-Year Timeline Explained

How Long Do Late Payments Stay on Credit Report? The Complete 7-Year Timeline Explained

Statement Balance: What It Is and How It Works Complete Guide

Statement Balance: What It Is and How It Works Complete Guide

Statement Balance vs Current Balance: Which One Should You to Pay

Statement Balance vs Current Balance: Which One Should You to Pay

How Credit Cards Work: Beginner’s Step-By-Step Guide

How Credit Cards Work: Beginner’s Step-By-Step Guide

How Long Does It Take to Build Credit? Real Timeline Explained

How Long Does It Take to Build Credit? Real Timeline Explained