A billing cycle is the fixed period of time, usually 28 to 31 days, that a lender or service provider uses to track charges, payments, and balances on an account. At the end of each billing cycle, you receive a statement showing what you owe, the payment due date, and how your balance affects interest, fees, or credit reporting.

For example, if your credit card billing cycle runs from March 5 to April 4, any purchases made during that window appear on your April statement, and you typically have 21–25 days after the cycle ends to pay before interest is charged.

This article is part of our complete Credit Cards Guide, where we break down APRs, interest, rewards, fees, and how to use credit cards the smart way.

The math behind billing cycles reveals a critical truth: your payment due date and the date that affects your credit score are completely different. Most consumers focus on the wrong date, resulting in unnecessarily high reported balances and lower scores. This article breaks down the mechanics of billing cycles, explains exactly when and how they affect your credit, and provides data-driven strategies to optimize your credit utilization timing.

Key Takeaways

- Billing cycles typically run 28-31 days and reset monthly, creating the period during which all transactions are recorded and compiled into your statement

- Statement closing date—not payment due date—determines what balance gets reported to credit bureaus and impacts your credit score

- Credit utilization is locked in at statement closing, meaning you must pay down balances 2-3 days before this date to improve your reported utilization ratio

- Each credit card has its own billing cycle, requiring separate tracking and strategic payment timing for optimal credit score management

- Strategic mid-cycle payments can boost scores by 50+ points by ensuring low utilization percentages are reported to Experian, Equifax, and TransUnion

What Is a Billing Cycle?

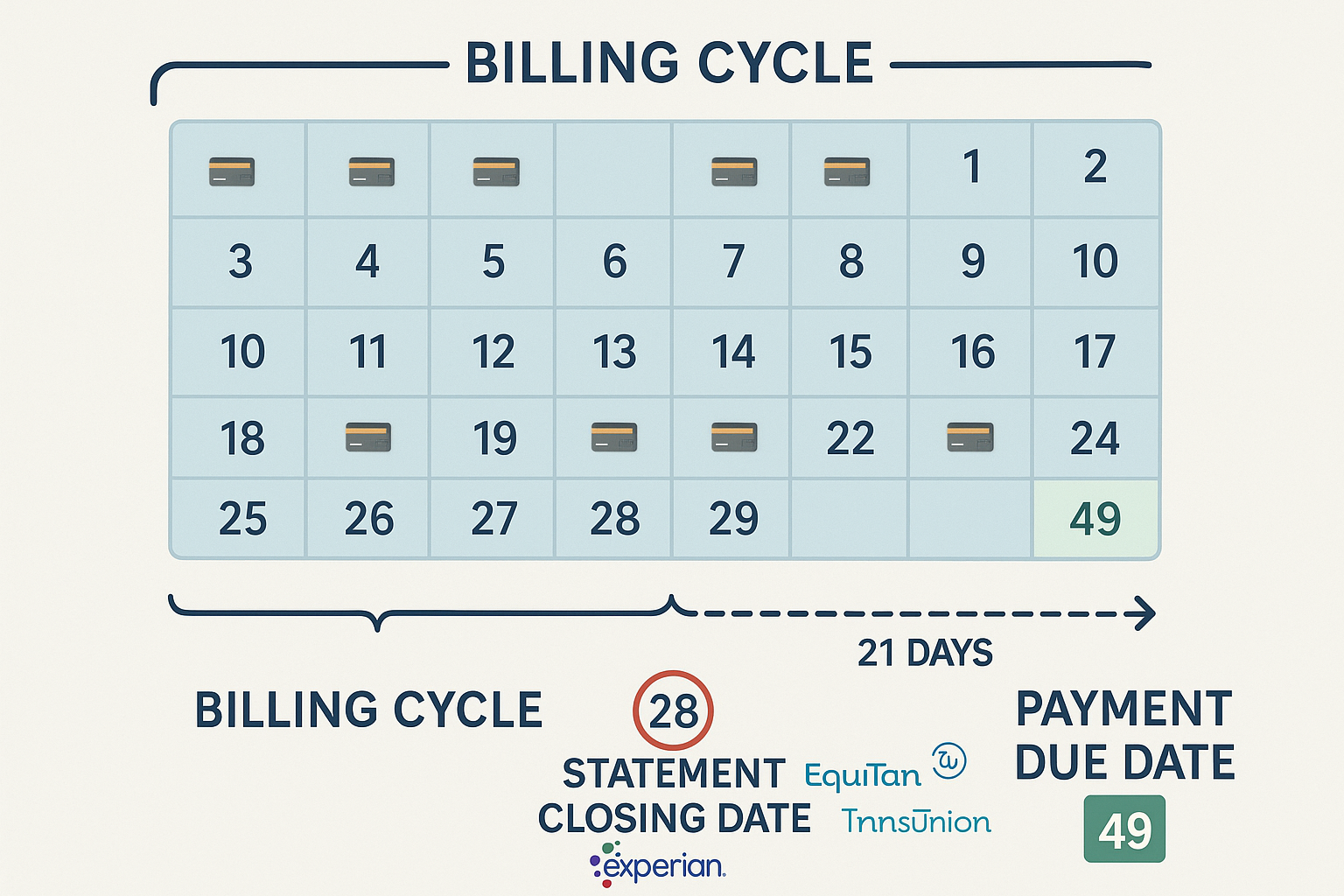

A billing cycle is a standardized period of time, typically 28 to 31 days for credit cards, during which all account activity is tracked and recorded. At the end of this period, the account “closes” for statement purposes, and a new cycle begins immediately.

Think of it as an accounting period with a hard reset. On Day 1 of your billing cycle, your slate starts fresh. Every purchase, payment, cash advance, and fee during the next 28-31 days gets recorded. On the final day (the statement closing date), everything stops, gets totaled, and becomes your official statement balance.

Here’s what happens during a billing cycle:

- Day 1: Billing cycle opens with a starting balance (previous balance minus any payments made)

- Days 1-28: All transactions are recorded in real-time but not yet finalized

- Day 28 (example): Statement closing date, all activity stops, balance is calculated and reported to credit bureaus

- Day 29: New billing cycle begins immediately; previous cycle’s balance becomes your statement balance

The cycle length varies slightly by issuer and account type. Credit cards typically use 28-31 day cycles to align roughly with monthly calendar periods. Some service providers use shorter cycles (25 days) or longer ones (45 days), depending on industry standards and cash flow requirements.

Why the cycle resets matters: Your credit card balance doesn’t just accumulate indefinitely. It gets “photographed” at the statement closing date, and that snapshot is what appears on your credit report. This is why understanding the exact day your cycle closes is more valuable than knowing your credit limit or even your payment due date when it comes to optimizing your credit score.

Why Billing Cycles Matter

Financial institutions use billing cycles to standardize accounting, automate reporting, and create predictable cash flow patterns. For credit card issuers specifically, the billing cycle serves three critical functions:

Transaction aggregation: All purchases, payments, fees, and interest charges during the cycle are compiled into a single statement.

Credit bureau reporting: At the end of each billing cycle, card issuers report your balance to the three major credit bureaus—Experian, Equifax, and TransUnion.

Payment scheduling: The cycle establishes your statement closing date and subsequent payment due date, creating a consistent timeline for account management.

The subscription economy has grown 435% over the past decade, making recurring billing cycles increasingly common across industries. Understanding how these cycles function is now essential financial literacy, particularly for anyone building or repairing credit.

The difference between understanding and ignoring billing cycles can mean the difference between a 720 credit score and an 800 credit score, a gap that translates to thousands of dollars in interest savings on mortgages, auto loans, and other credit products.

Billing Cycle vs Statement Closing Date

This distinction is where most credit confusion begins. The terms are related but represent fundamentally different concepts:

Billing cycle = The entire 28-31 day period during which transactions occur

Statement closing date = The final day of that billing cycle when your balance is finalized and reported

The billing cycle is the container; the statement closing date is the endpoint. You can make purchases throughout the entire billing cycle, but only the balance remaining on the statement closing date matters for credit reporting purposes.

Why the Closing Date Is More Important for Credit Reporting

Credit card companies report your balance to the three major credit bureaus once per month, and they do so on or immediately after your statement closing date, not when you make payments, not on your due date, and not in real-time.

This creates a critical timing opportunity:

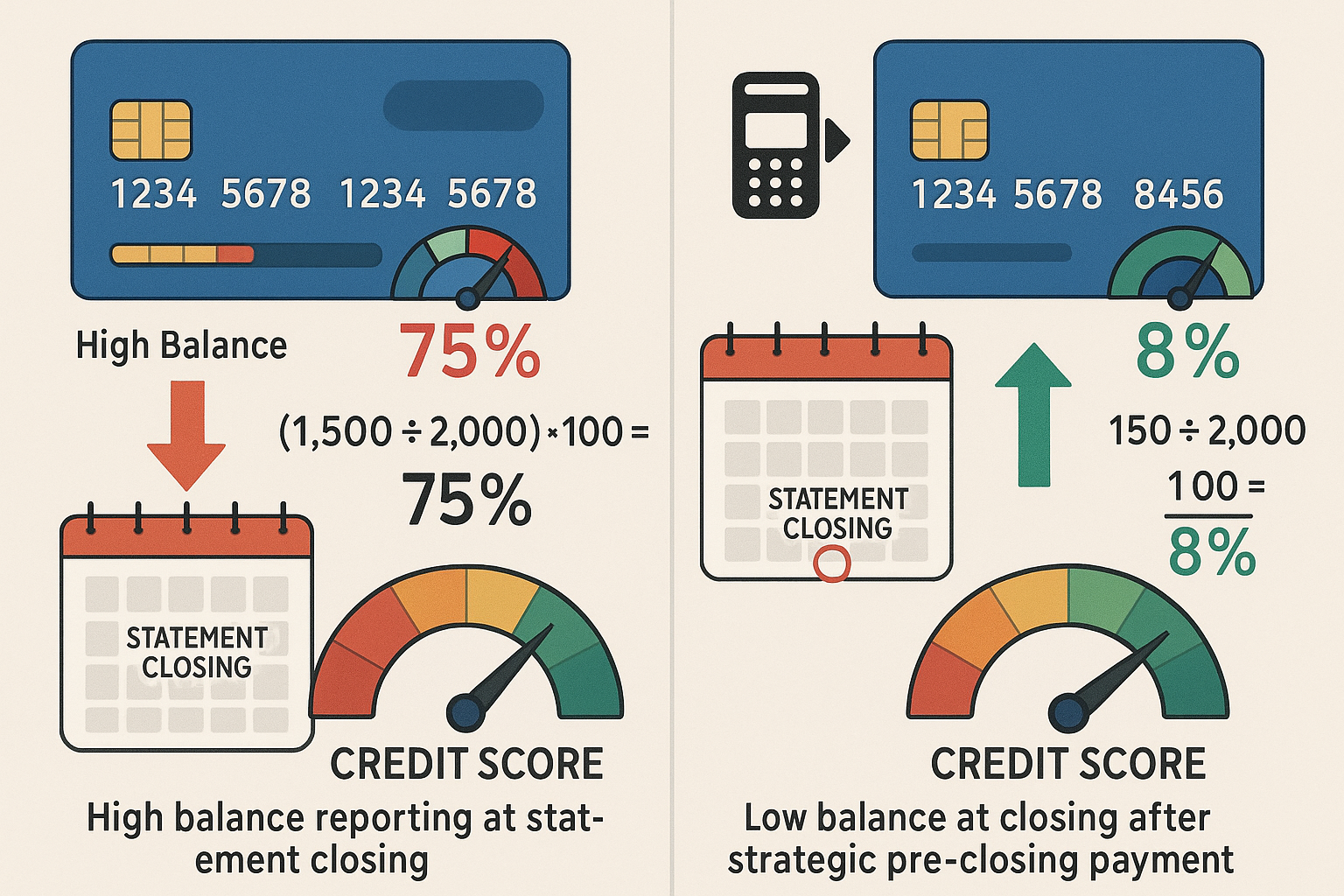

If your statement closing date is the 15th of each month, the balance on your card on the 15th is what gets reported to Experian, Equifax, and TransUnion. If you have a $5,000 balance on the 14th but pay it down to $500 on the 14th, your reported balance will be $500 (10% utilization on a $5,000 limit) rather than $5,000 (100% utilization).

The math is straightforward:

- Credit utilization ratio = (Reported Balance ÷ Credit Limit) × 100

- Reported balance = Balance on statement closing date

- Therefore, controlling your balance on the closing date controls your utilization ratio

Since credit utilization accounts for approximately 30% of your FICO score, this timing strategy can have an immediate, measurable impact on your creditworthiness.

Billing Cycle vs Payment Due Date

The payment due date is typically 21-25 days after the statement closing date. This is your grace period, the window during which you can pay your statement balance without incurring interest charges.

Here’s the timeline:

- Statement closing date (e.g., March 15): Billing cycle ends, balance is finalized, and reported to bureaus

- Grace period (e.g., March 16 – April 9): 21-25 days to review statement and make payment

- Payment due date (e.g., April 9): Deadline to pay at least the minimum payment to avoid late fees

Why Due Date Has Nothing to Do With Credit Reporting

This is the most common and costly misconception in consumer credit management: believing that paying your bill by the due date protects your credit score.

The truth: By the time your payment due date arrives, your balance has already been reported to the credit bureaus 3+ weeks earlier. Paying on the due date prevents late fees and interest charges, but it does nothing to improve the utilization ratio that was locked in at statement closing.

Example of the confusion:

Sarah has a $10,000 credit limit and typically carries a $7,000 balance (70% utilization). She always pays on time by the due date. Her credit score hovers around 680.

She doesn’t realize that even though she pays in full each month, her $7,000 balance gets reported at statement closing before her payment arrives. The credit bureaus see 70% utilization every single month, which suppresses her score.

If Sarah understood billing cycles, she would pay down to $1,000 (10% utilization) before her statement closing date, then pay the remaining balance by the due date. This simple timing shift could increase her score to 750 or higher within 30 days.

This is not a loophole or trick; it’s understanding the math behind how credit mix and utilization are calculated and reported.

How Billing Cycles Affect Your Credit Score

Credit card companies report account information to credit bureaus once per billing cycle, and they report the balance that appears on your statement; the balance on your statement’s closing date.

This creates three critical effects:

1. Your Utilization Is Locked In at Closing

Your credit utilization ratio, one of the most heavily weighted factors in credit scoring models, is determined by the balance reported at statement closing, not your average balance, not your highest balance, and not your balance on the due date.

The formula:

- Individual card utilization = (Statement balance ÷ Credit limit) × 100

- Overall utilization = (Total reported balances ÷ Total credit limits) × 100

For maximum credit score benefit, both individual and overall utilization should remain below 10%. Between 10-30% is acceptable but suboptimal. Above 30% begins to significantly damage scores.

2. Timing Creates Score Volatility

Because utilization has no memory in FICO scoring models, your score can swing dramatically month-to-month based solely on reported balances. A $5,000 balance reported one month can drop your score 40 points; paying it down to $500 before the next closing date can recover those 40 points within 30 days.

This volatility is actually an advantage for informed consumers. Unlike payment history (which takes 7 years to fully recover from a single late payment), utilization can be optimized immediately.

3. Multiple Cards Require Coordinated Strategy

Each credit card has its own billing cycle, often on different dates. Card A might close on the 5th, Card B on the 15th, and Card C on the 28th. This means you need to track and manage three separate closing dates to optimize your overall credit profile.

Example of how balances impact scores:

Scenario 1 – Unoptimized:

- Card A: $2,000 balance / $5,000 limit = 40% utilization (closes on the 5th)

- Card B: $3,000 balance / $10,000 limit = 30% utilization (closes on the 15th)

- Card C: $1,500 balance / $5,000 limit = 30% utilization (closes on the 28th)

- Overall utilization: $6,500 / $20,000 = 32.5%

- Approximate score: 680-700

Scenario 2 – Optimized (same spending, different timing):

- Card A: $200 balance / $5,000 limit = 4% utilization (paid down before the 5th)

- Card B: $500 balance / $10,000 limit = 5% utilization (paid down before the 15th)

- Card C: $300 balance / $5,000 limit = 6% utilization (paid down before the 28th)

- Overall utilization: $1,000 / $20,000 = 5%

- Approximate score: 750-780

Same person, same spending, same credit limits, just different payment timing relative to billing cycles. The score difference of 50-80 points translates to dramatically better loan terms and lower interest rates across all credit products.

Understanding this mechanism is fundamental to financial literacy and wealth building because credit scores affect the cost of capital for major purchases.

How to Use Your Billing Cycle to Increase Your Score

The strategic application of billing cycle knowledge creates immediate, measurable credit score improvements. Here’s the data-driven approach:

Pay Down Cards 2-3 Days Before Your Statement Closing Date

Payment processing takes 1-3 business days, depending on your bank and card issuer. To ensure your payment posts before the statement closing date, submit payments 2-3 days early.

Action steps:

- Identify your statement closing date (see next section)

- Set a recurring calendar reminder for 3 days before closing

- Make a payment to reduce your balance to the target utilization

- Verify the payment posted before the closing date

- Pay the remaining balance by the due date to avoid interest

Keep Utilization Under 10% for Maximum Scoring

Research and credit scoring models consistently show that utilization below 10% produces the highest scores, with diminishing returns as utilization increases.

The utilization tiers:

- 0-9%: Optimal scoring range (760-850 potential)

- 10-29%: Good but suboptimal (700-759 potential)

- 30-49%: Begins significant score damage (650-699 potential)

- 50-74%: Major score suppression (600-649 potential)

- 75-100%: Severe score damage (below 600)

Note that 0% utilization (reporting zero balances on all cards) can actually be slightly worse than 1-9% utilization because it suggests you’re not actively using credit. Optimal strategy: report small balances (1-9%) on one or two cards while keeping others at zero.

Set Reminders Based on Your Own Cycle

Generic advice to “pay your credit card bill” isn’t actionable. Specific, calendar-based reminders tied to your individual statement closing dates create consistent execution.

Implementation:

- Use a phone calendar with recurring monthly reminders

- Set a reminder for 3 days before each card’s closing date

- Include the target payment amount in the reminder (e.g., “Pay Card A to $500”)

- Review and adjust monthly based on spending patterns

Advanced Tactic: Mid-Cycle Payments

For consumers with high monthly spending who want to maximize rewards without damaging utilization, mid-cycle payments allow you to spend more while reporting less.

How it works:

If you spend $8,000 per month on a card with a $10,000 limit, waiting until the statement closing date would report 80% utilization. Instead:

- Day 1-14: Spend $4,000 (40% utilization)

- Day 15: Make $4,000 payment (back to 0%)

- Day 16-28: Spend another $4,000 (40% utilization)

- Day 25: Make $3,500 payment (down to $500, or 5% utilization)

- Day 28: Statement closes with $500 balance (5% utilization reported)

Result: You spent $8,000 and earned full rewards, but only 5% utilization was reported to credit bureaus.

This strategy requires careful tracking and discipline, but can be particularly valuable for business owners or high-income earners who funnel significant expenses through rewards cards. The principle aligns with broader risk management concepts: optimize the metric being measured (reported utilization) while maintaining the behavior that creates value (reward earning).

How to Find Your Billing Cycle

Every credit card and service account has billing cycle information readily available through multiple channels:

Mobile App

Most card issuers display billing cycle dates prominently in their mobile apps:

- Open your credit card app

- Navigate to account details or statements

- Look for “Statement Closing Date” or “Billing Cycle”

- Note: Some apps show “Next Closing Date” rather than cycle length

The app method is the fastest and most convenient for regular monitoring.

Statement

Your monthly statement (paper or electronic) always includes:

- Statement closing date: The date the statement was generated

- Payment due date: Deadline for payment

- Billing cycle dates: Often shown as “Billing period: 02/15/2025 – 03/14/2025”

Statements provide the most comprehensive view of your billing cycle, including the exact start and end dates.

Customer Service

Calling the number on the back of your card connects you to customer service representatives who can:

- Confirm your exact statement closing date

- Explain your billing cycle length

- Request a change to your closing date (some issuers allow this)

- Clarify any confusion about cycle timing

Pro tip: Some issuers allow you to request a specific statement closing date. If you manage multiple cards, aligning all closing dates to the same day of the month simplifies tracking and payment scheduling.

Why Each Card Has Different Cycles

Credit card issuers stagger billing cycles across their customer base to distribute workload evenly throughout the month. If all customers had the same closing date, the issuer would face massive processing spikes once monthly rather than steady, manageable volume.

Your closing date is typically set when you open the account, often based on the day you were approved or activated the card. This means:

- Cards opened on different dates will have different cycles

- Cards from different issuers will almost certainly have different cycles

- Even multiple cards from the same issuer may have different cycles

This variation requires tracking each card individually. Consider creating a simple spreadsheet:

| Card | Issuer | Credit Limit | Closing Date | Payment Due Date | Target Balance at Closing |

|---|---|---|---|---|---|

| Card A | Chase | $10,000 | 5th | 28th | $500 (5%) |

| Card B | Amex | $15,000 | 15th | 7th (next month) | $750 (5%) |

| Card C | Citi | $8,000 | 22nd | 15th (next month) | $400 (5%) |

This level of organization transforms billing cycle management from confusing to systematic.

Common Billing Cycle Mistakes

Understanding the mechanics is only valuable if you avoid the common errors that sabotage credit scores:

Only Paying on the Due Date

The mistake: Waiting until the payment due date to pay your balance, assuming this protects your credit.

Why it fails: Your balance was already reported to credit bureaus 21-25 days earlier at statement closing. Paying on the due date prevents late fees but does nothing for your utilization ratio.

The fix: Make a payment 2-3 days before your statement closing date to reduce reported utilization, then pay any remaining balance by the due date.

Maxing Out Before Closing

The mistake: Using cards heavily throughout the month without considering the closing date balance.

Why it fails: Even if you pay in full every month, a high balance at statement closing reports high utilization and damages your score.

The fix: Either make mid-cycle payments to reduce the closing balance, or shift heavy spending to immediately after statement closing so you have the full cycle to pay it down.

Letting Small Balances Report

The mistake: Assuming that small balances (like $50-100) don’t matter for credit scoring.

Why it fails: While small balances are better than large ones, reporting zero balances on all cards can be suboptimal. The ideal scenario is small balances (1-9% utilization) on one or two cards.

The fix: Strategically allow small balances to report on select cards while keeping others at zero. This demonstrates active credit use without high utilization.

Assuming All Cards Report at the Same Time

The mistake: Treating all credit cards as if they have synchronized billing cycles.

Why it fails: Each card reports independently on its own closing date. Your overall credit profile is the sum of all individual card reports, which occur on different days throughout the month.

The fix: Track each card’s closing date separately and manage each account individually. Your credit report updates continuously throughout the month as different cards report.

Additional mistake: Ignoring the grace period

Some consumers confuse the billing cycle with the grace period. The grace period is the time between statement closing and payment due date; it’s not part of the billing cycle itself. Purchases made during the grace period belong to the next billing cycle, not the one that just closed.

These mistakes stem from the same root cause: focusing on payment due dates rather than statement closing dates. The due date matters for avoiding fees; the closing date matters for credit scores. Both are important, but they serve completely different functions in credit management.

Example Timeline

To make billing cycle mechanics concrete, here’s a detailed walkthrough of a single cycle:

Day 1 (March 1): Billing cycle opens

- Starting balance: $0 (previous balance was paid in full)

- Credit limit: $5,000

- Current utilization: 0%

Day 5 (March 5): Make a purchase

- Purchase: $800 (groceries, gas, dining)

- Current balance: $800

- Current utilization: 16%

Day 14 (March 14): Make additional purchases

- Purchases: $1,200 (travel, shopping)

- Current balance: $2,000

- Current utilization: 40%

Day 20 (March 20): Receive paycheck, continue spending

- Additional purchases: $500

- Current balance: $2,500

- Current utilization: 50%

Day 25 (March 25): Strategic payment (3 days before closing)

- Payment: $2,100

- New balance: $400

- Current utilization: 8%

- This is the critical action: Paying down before closing to optimize reported utilization

Day 28 (March 28): Statement closing date

- Balance reported to credit bureaus: $400

- Utilization reported: 8%

- Statement generated showing $400 balance

- New billing cycle begins immediately (Day 1 of next cycle)

Day 29 (March 29): Grace period begins

- Statement balance: $400

- Payment due date: 21 days away (April 18)

- Any new purchases belong to the new cycle (April 1-28)

April 5 (Day 8 of grace period): Optional additional purchases

- New purchases: $600 (these belong to the new cycle, not the closed one)

- Statement balance still: $400 (unchanged)

- New cycle balance: $600

April 18 (Day 21 of grace period): Payment due date

- Payment: $400 (pays off statement balance)

- Result: No interest charged, no late fees

- New cycle balance: $600 (from purchases made after the previous closing)

Key insights from this timeline:

- The payment on Day 25 (before closing) determined the reported utilization (8%)

- The payment on Day 49 (due date) prevented interest and fees, but didn’t affect credit reporting

- Purchases made after Day 28 belong to the next cycle and won’t be reported until the next closing date

- The consumer spent $2,500 total, but only reported $400 (8% utilization) by timing payments strategically

This timeline demonstrates why understanding billing cycles is a form of financial literacy that directly impacts creditworthiness and borrowing costs. The same spending behavior produces dramatically different credit outcomes based solely on payment timing.

📅 Billing Cycle Payment Optimizer

Calculate your optimal payment timing to maximize your credit score

Conclusion

The billing cycle is not just an administrative detail—it’s the mechanism that determines when and how your credit behavior is reported to the three major credit bureaus. Understanding the difference between your billing cycle, statement closing date, and payment due date gives you strategic control over your credit utilization ratio and, therefore, your credit score.

The essential truths about billing cycles:

- Your billing cycle is typically 28-31 days and resets monthly

- Your statement closing date (the last day of the cycle) is when your balance gets reported to credit bureaus

- Your payment due date (21-25 days after closing) determines late fees and interest, not credit reporting

- Strategic payments 2-3 days before closing, optimize your reported utilization

- Each card has its own cycle requiring individual tracking and management

The math is straightforward: credit utilization accounts for approximately 30% of your FICO score, and utilization is determined by the balance reported at statement closing. Therefore, controlling your balance on closing dates directly controls roughly one-third of your credit score.

Actionable next steps:

- Identify all statement closing dates: Check your app, statement, or call customer service for each credit card

- Create a tracking system: Use a spreadsheet or calendar to monitor each card’s closing date

- Set recurring reminders: Schedule alerts for 3 days before each closing date

- Calculate target balances: Determine what balance represents 5-10% utilization for each card

- Execute strategic payments: Pay down to target utilization before closing, then pay the remaining balance by the due date

- Monitor results: Check your credit report 30-60 days after implementation to verify utilization improvements

This strategy requires no additional spending, no credit limit increases, and no new accounts, just better timing of payments you’re already making. For consumers with good payment history but suboptimal utilization, this single change can increase scores by 50-80 points within 60 days.

The broader principle applies beyond credit cards: understanding the timing and mechanisms of financial reporting systems allows you to optimize outcomes. Whether it’s billing cycles affecting credit scores, compound interest timing affecting investment returns, or accounts payable timing affecting business cash flow, the math behind money rewards those who understand the systems.

Master your billing cycles, and you master a significant component of your financial profile.

Author Bio

Max Fonji is a data-driven financial educator and the voice behind The Rich Guy Math. With a background in financial analysis and a commitment to evidence-based investing principles, Max breaks down complex financial concepts into clear, actionable insights. His approach combines analytical precision with educational clarity, helping readers understand the math behind wealth building, credit management, and long-term financial success.

Educational Disclaimer

This article is provided for educational and informational purposes only and should not be construed as financial, legal, or credit advice. While the information presented is based on current credit scoring models and industry practices as of 2025, individual circumstances vary, and credit scoring algorithms are proprietary and subject to change.

Credit scores are influenced by multiple factors beyond utilization, including payment history, credit age, credit mix, and recent inquiries. Results from implementing billing cycle strategies will vary based on individual credit profiles.

Readers should verify their specific billing cycle dates with their card issuers and consider consulting with qualified financial professionals before making significant credit or financial decisions. The Rich Guy Math and its authors are not responsible for any financial outcomes resulting from the application of information contained in this article.

Always read your credit card agreement, understand your specific terms, and maintain responsible credit practices, including paying all bills on time and keeping balances manageable relative to income.

References

[1] Consumer Financial Protection Bureau. (2025). “Credit Card Billing Cycles and Credit Reporting.” CFPB.gov.

[2] Federal Reserve. (2025). “Consumer Credit Report: Billing Practices and Credit Utilization.” Federal Reserve Board.

[3] Experian. (2025). “Understanding Your Credit Card Statement and Billing Cycle.” Experian.com.

[4] TransUnion. (2025). “How Credit Card Issuers Report to Credit Bureaus.” TransUnion.com.

[5] FICO. (2025). “Credit Utilization and FICO Score Calculation.” MyFICO.com.

[6] Equifax. (2025). “Credit Card Reporting Dates and Your Credit Score.” Equifax.com.

[7] Office of the Comptroller of the Currency. (2025). “Credit Card Billing Standards and Consumer Protection.” OCC.gov.

Frequently Asked Questions

What is a billing cycle on a credit card?

A billing cycle on a credit card is the recurring 28–31 day period between billing statements during which all transactions are recorded. At the end of the cycle (the statement closing date), your balance is finalized, reported to credit bureaus, and a new cycle begins immediately. This cycle determines when your credit utilization is calculated and reported, making it critical for credit score management.

When does my credit card company report to credit bureaus?

Credit card companies report your balance to Experian, Equifax, and TransUnion once per month, typically on or within 1–2 days after your statement closing date. This is not your payment due date—it is the last day of your billing cycle. The balance on this date appears on your credit report and directly affects your credit utilization ratio.

How can I use my billing cycle to improve my credit score?

To boost your credit score using billing cycle timing, make a payment 2–3 days before your statement closing date to reduce your balance to below 10% of your credit limit. This ensures a low utilization ratio gets reported to credit bureaus, which can raise your score by 50+ points within 30–60 days. Then pay any remaining balance by the payment due date to avoid interest charges.

What’s the difference between statement closing date and payment due date?

The statement closing date is the final day of your billing cycle when your balance is finalized and reported to credit bureaus—this directly affects your credit score. The payment due date is usually 21–25 days later and is the deadline to pay your bill to avoid late fees and interest—this date does not directly affect credit reporting. Both are important but serve very different purposes.

How do I find my billing cycle dates?

You can find your billing cycle dates by checking your credit card mobile app, reviewing your monthly statement (which lists the start and end dates), or contacting customer service. The statement closing date is the most important because it determines what gets reported to credit bureaus.

Can I change my billing cycle or statement closing date?

Some credit card issuers allow you to change your statement closing date, though policies vary by company. Contact your issuer’s customer service to see if this option is available. Changing your closing date can help align your cards to the same date or match your paycheck schedule for better cash-flow management.

What happens if I make a purchase after my statement closing date?

Purchases made after your statement closing date fall into the next billing cycle. They will not appear on your current statement or be reported to credit bureaus until the next closing date. This allows you to make purchases after closing without affecting your current utilization ratio.

Why is my credit score low if I always pay on time?

If your credit score is low despite paying on time, the likely reason is high credit utilization being reported at your statement closing date. Even if you pay in full every month, high balances at closing get reported and can lower your score. The fix is to make payments before the closing date—not just by the due date—to reduce the reported utilization.