Every business owner faces a fundamental choice that shapes how they track money, report taxes, and understand profitability. That choice is between cash and accrual accounting, two methods that record the same transactions but tell dramatically different financial stories.

Cash vs Accrual Accounting represents more than just bookkeeping preferences. This decision determines when revenue appears on financial statements, how expenses reduce taxable income, and whether a business can accurately assess its true financial health. The math behind money becomes clearer when you understand that timing, not just amounts, drives financial reality.

Small business owners often start with cash accounting because it mirrors their bank account. Large corporations use accrual accounting because regulations demand it. The difference between these methods can mean paying taxes on money not yet collected or missing critical insights about accounts receivable and future obligations.

Key Takeaways

- Cash accounting records transactions when money physically changes hands, making it simple but potentially misleading about the true financial position

- Accrual accounting records revenue when earned and expenses when incurred, regardless of payment timing, providing a more accurate long-term financial picture

- GAAP requires accrual accounting for most larger businesses, while smaller operations may choose the cash basis for simplicity and immediate tax benefits

- The timing difference affects tax liability, financial reporting accuracy, and strategic decision-making in ways that compound over time

- Your business size, complexity, growth plans, and regulatory requirements should drive your choice between these fundamental accounting methods

Understanding Cash Basis Accounting

Cash basis accounting operates on a straightforward principle: record money when it enters or leaves the bank account. This method tracks financial reality as most people naturally think about it: income exists when cash arrives, and expenses exist when payments go out.

How Cash Accounting Works

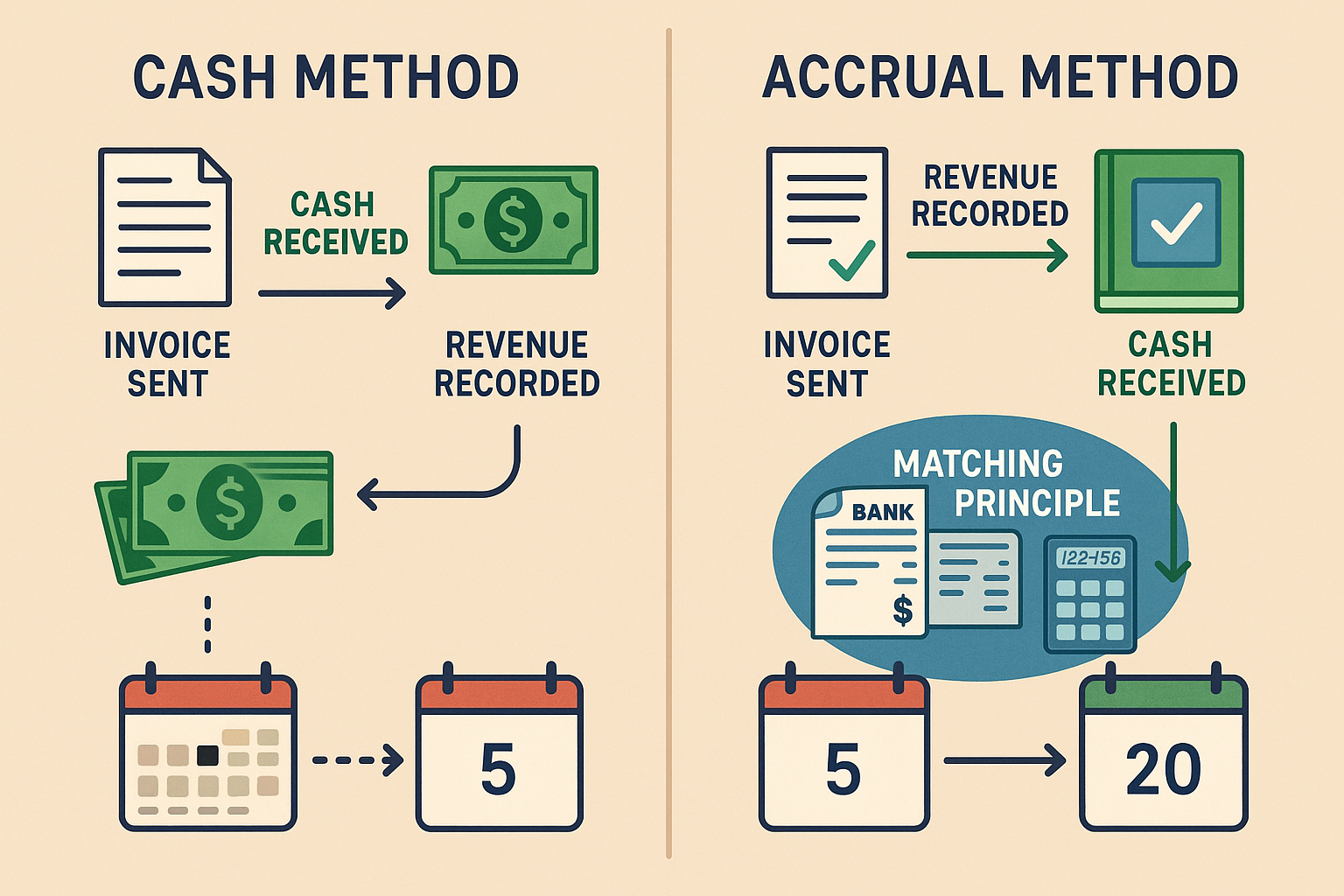

Under the cash method, a business records revenue only when payment is received. If an invoice is sent in December but payment arrives in January, that revenue belongs to January’s financial records. The same logic applies to expenses; a bill received in one month but paid in another gets recorded when the check clears.

This creates a direct connection between accounting records and bank statements. The simplicity makes cash accounting attractive for sole proprietors, freelancers, and small service businesses without significant inventory.

Example: A freelance consultant completes a $5,000 project on December 15, 2025, and sends an invoice. The client pays on January 10, 2026. Under cash accounting, this $5,000 appears as 2026 income, not 2025 income.

Advantages of Cash Basis Accounting

The cash method delivers several practical benefits:

Simplicity and lower costs. Cash accounting requires minimal bookkeeping expertise. Business owners can often manage their own books without expensive accounting software or professional services. This reduces overhead and makes financial literacy more accessible.

Clear cash flow visibility. Financial statements directly reflect available cash. When the books show $10,000 in revenue, that money sits in the bank account. This transparency helps with immediate budgeting decisions and emergency fund planning.

Tax timing advantages. Businesses never pay taxes on uncollected revenue. If customers owe $20,000 at year-end but haven’t paid, that amount doesn’t increase tax liability. This can significantly improve cash flow for businesses with slow-paying clients.

Easier tax planning. Business owners can strategically time payments to shift expenses between tax years. Paying January bills in December increases current-year deductions and reduces taxable income.

Limitations of Cash Basis Accounting

Despite its simplicity, cash accounting creates significant blind spots:

Incomplete financial picture. Cash basis statements ignore accounts receivable and accounts payable. A business might show a strong cash position while owing substantial unpaid bills, or appear cash-poor while customers owe significant amounts.

Poor matching of revenue and expenses. The matching principle, recording expenses alongside the revenue they generate, breaks down under cash accounting. A business might record revenue from a project in one year but pay related expenses in another, distorting accounting profit calculations.

Limited usefulness for decision-making. Investors, lenders, and strategic partners need to understand total obligations and expected income. Cash accounting hides these critical data points, making it difficult to assess true business value or secure financing.

Regulatory restrictions. The IRS prohibits cash basis accounting for C corporations, partnerships with corporate partners, and businesses with average annual gross receipts exceeding $27 million over the prior three years. GAAP also requires accrual accounting for audited financial statements.

Understanding Accrual Basis Accounting

Accrual accounting recognizes economic events when they occur, not when cash changes hands. This method records revenue when earned and expenses when incurred, creating a comprehensive view of financial obligations and future income.

How Accrual Accounting Works

Under accrual accounting, transactions are recorded based on the underlying economic activity. When a business delivers goods or completes services, revenue is recognized immediately, even if the customer pays 30, 60, or 90 days later.

The same principle applies to expenses. When a business receives inventory, uses utilities, or incurs any cost, that expense is recorded when the obligation arises, not when the bill is paid.

This creates two critical balance sheet categories that don’t exist in cash accounting:

Accounts Receivable: Money customers owe for delivered goods or completed services. This represents earned revenue not yet collected as cash.

Accounts Payable: Money the business owes to suppliers, vendors, or service providers for received goods or services not yet paid.

Example: A manufacturing company ships $50,000 in products on December 20, 2025, with payment terms of net-30 days. Under accrual accounting, this $50,000 appears as December 2025 revenue, with a corresponding $50,000 increase in accounts receivable. When payment arrives in January 2026, cash increases, and accounts receivable decrease; revenue doesn’t change.

The Matching Principle

Accrual accounting implements the matching principle, a cornerstone of accurate financial reporting. This principle requires businesses to record expenses in the same period as the revenue those expenses helped generate.

Consider a retail business that purchases inventory in November, sells it in December, but pays the supplier in January. Under accrual accounting:

- November: Inventory increases (asset)

- December: Revenue is recorded when sold; cost of goods sold (expense) is recorded simultaneously

- January: Cash decreases when payment is made; accounts payable decrease

This matching creates an accurate picture of profit margins. The cash flow statement separately tracks actual cash movements, while the income statement shows true profitability.

Advantages of Accrual Basis Accounting

Accrual accounting provides substantial benefits for growing businesses:

Accurate financial health assessment. Balance sheet basics become meaningful when they include receivables and payables. Decision-makers can assess total assets versus liabilities, not just current cash position.

Better long-term planning. Accrual accounting reveals patterns in customer payment behavior, seasonal revenue fluctuations, and expense timing. This data-driven insight supports strategic planning and capital allocation.

GAAP compliance. Accrual accounting meets Generally Accepted Accounting Principles, making financial statements auditable and credible to investors, lenders, and potential buyers.

Improved business valuation. When selling a business or seeking investment, accrual-based financial statements provide the comprehensive data buyers need. They show the full economic value, including money owed and obligations due.

Enhanced decision-making speed. Managers can assess project profitability immediately after completion, rather than waiting for all payments to clear. This accelerates strategic adjustments and resource allocation.

Limitations of Accrual Basis Accounting

Accrual accounting introduces complexity and potential challenges:

Greater complexity and cost. Maintaining accrual records requires more sophisticated bookkeeping skills, accounting software, and often professional accounting services. This increases operational costs, particularly for small businesses.

Potential cash flow disconnection. Financial statements might show strong profitability while the bank account runs low. A business can be “profitable but broke” if customers delay payments while expenses come due.

Tax timing considerations. Businesses may owe taxes on revenue not yet collected as cash. If a company records $100,000 in December revenue but doesn’t receive payment until February, December’s tax liability increases despite an unchanged cash position.

Requires judgment and estimates. Accrual accounting demands estimates for bad debt reserves, depreciation schedules, and revenue recognition timing. These judgments introduce subjectivity and potential for manipulation.

Cash vs Accrual Accounting: Side-by-Side Comparison

Understanding the practical differences between these methods requires examining how each handles identical transactions.

Transaction Timing Differences

| Scenario | Cash Accounting | Accrual Accounting |

|---|---|---|

| Invoice sent for $10,000 on Dec 15 | No entry until payment received | Revenue recorded Dec 15; Accounts Receivable increases |

| Payment received Jan 10 | Revenue recorded Jan 10 | Cash increases; Accounts Receivable decreases (no revenue impact) |

| Supplier bill received Nov 30 for $3,000 | No entry until payment made | Expense recorded Nov 30; Accounts Payable increases |

| Payment made Dec 20 | Expense recorded Dec 20 | Cash decreases; Accounts Payable decreases (no expense impact) |

| Annual insurance paid Jan 1 ($12,000) | Full $12,000 expense in January | $1,000 monthly expense via prepaid asset amortization |

These timing differences create dramatically different financial statements for the same underlying business activity.

Impact on Financial Statements

Income Statement Differences:

Cash basis income statements show only collected revenue and paid expenses. They provide a snapshot of historical cash movements but miss future obligations and expected income.

Accrual basis income statements show earned revenue and incurred expenses, regardless of payment status. They reveal true profitability by matching revenue with the costs required to generate it.

Balance Sheet Differences:

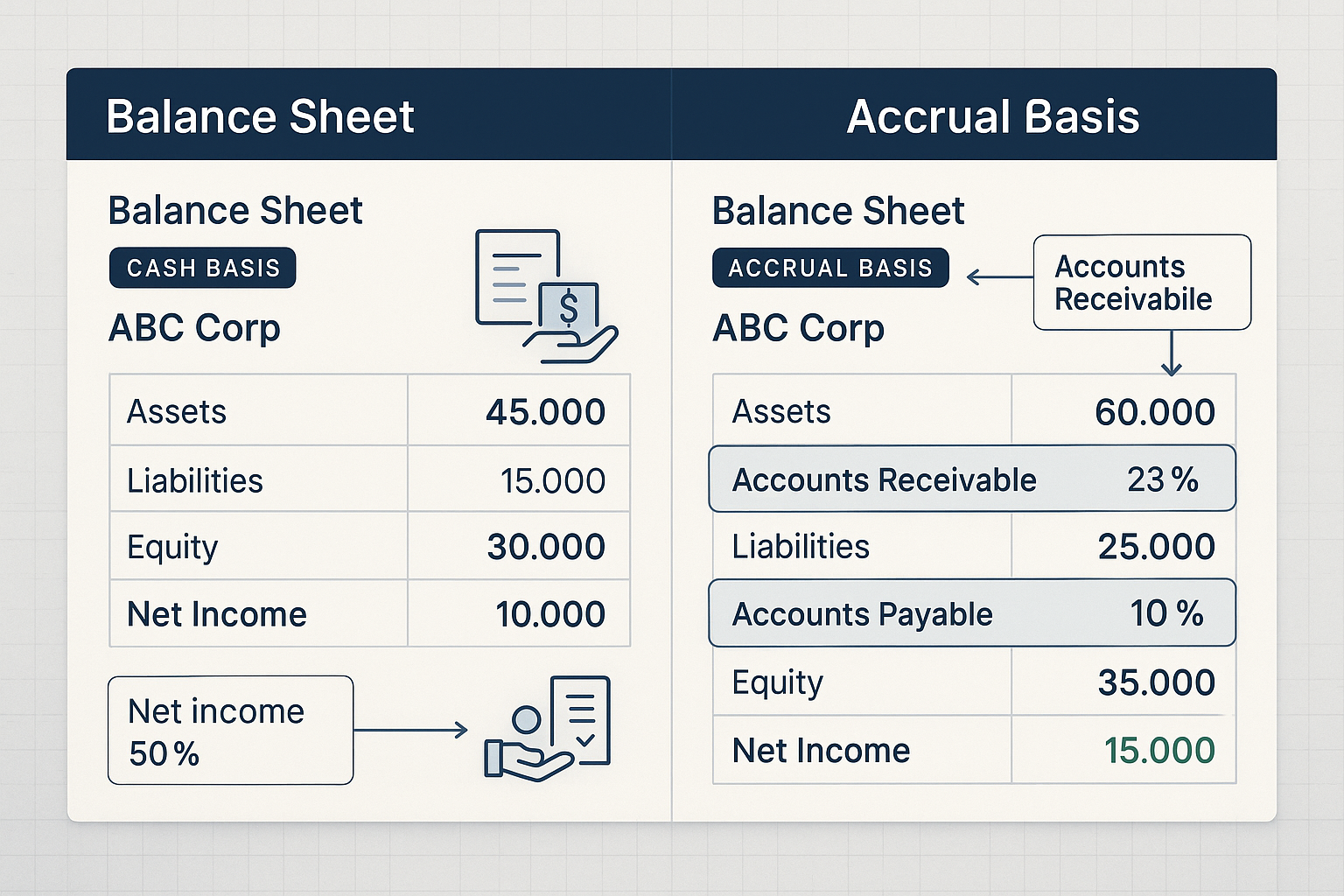

Cash basis balance sheets are simplified; they don’t include accounts receivable, accounts payable, or many accrued liabilities. This makes them less useful for assessing total assets and obligations.

Accrual basis balance sheets provide comprehensive financial position data, including all resources owned and all obligations owed. This enables calculation of meaningful financial ratios like the current ratio, debt-to-equity ratio, and debt ratio.

Tax Implications

The choice between cash and accrual accounting significantly affects tax liability:

Cash basis tax advantages:

- Revenue is taxed only when received, improving cash flow

- Expenses are deductible when paid, allowing strategic year-end payments

- Never pay taxes on uncollected revenue

- Simpler tax preparation with lower accounting costs

Accrual basis tax considerations:

- Revenue is taxed when earned, even if not yet collected

- May defer taxes if accrued expenses exceed accrued income

- Advance payments may be deferrable under certain circumstances[1]

- More complex tax preparation requires professional assistance

Example: A consulting firm completes $80,000 in projects during December 2025 but doesn’t receive payment until January 2026. Under cash accounting, this income appears on the 2026 tax return. Under accrual accounting, it appears on the 2025 tax return, creating a tax liability before cash is received.

The tax timing difference can substantially impact cash flow, particularly for businesses with long payment cycles or seasonal revenue patterns.

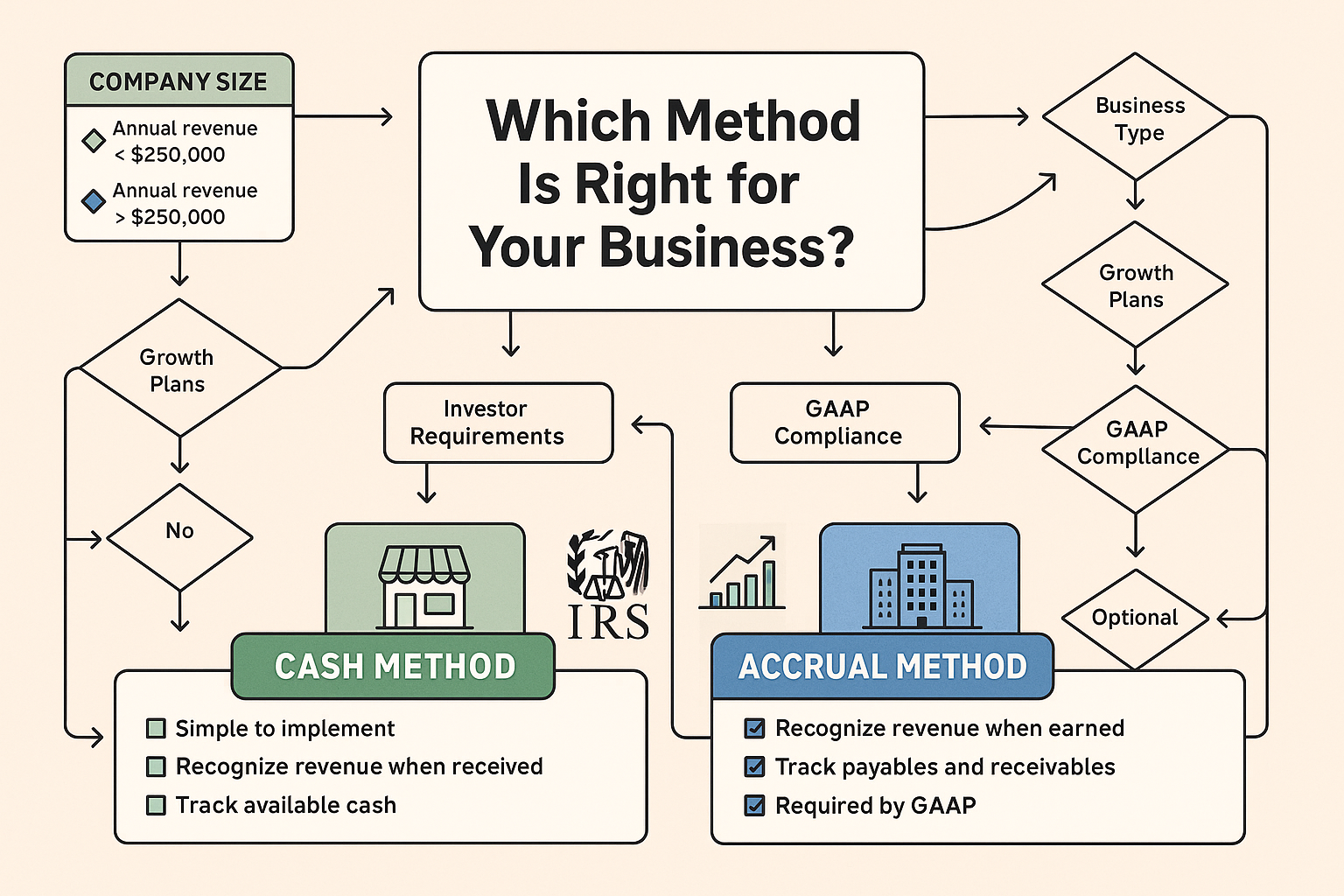

Choosing Between Cash and Accrual Accounting

The decision between these methods depends on multiple factors specific to each business situation.

Business Size and Revenue Thresholds

Small businesses and sole proprietors generally benefit from cash accounting’s simplicity. The method works well when:

- Annual revenue stays below $27 million (IRS threshold)

- The business operates as a sole proprietorship, partnership, or S corporation

- Inventory is not a significant income-producing factor

- Most transactions involve immediate or near-immediate payment

Larger businesses and corporations typically must use accrual accounting because:

- IRS regulations require it above certain revenue thresholds

- GAAP compliance is mandatory for audited statements

- Investors and lenders demand comprehensive financial data

- Business complexity makes the cash basis inadequate

Industry and Business Type Considerations

Service businesses like consultants, lawyers, and freelancers often start with cash accounting because:

- No inventory tracking required

- Simple transaction structures

- Direct correlation between work completed and payment received

- Lower accounting costs preserve profit margins

Product-based businesses selling physical goods typically need accrual accounting because:

- Inventory management requires tracking costs and sales separately

- Purchase and payment timing rarely align

- Cost of goods sold calculations, demand matching principles

- Wholesale and retail operations involve extended payment terms

Subscription and SaaS businesses benefit from accrual accounting’s ability to handle deferred revenue and recognize income over service delivery periods.

Growth and Financing Plans

Businesses planning to seek investment, secure loans, or eventually sell should implement accrual accounting early. The comprehensive financial data support:

Investor due diligence: Venture capitalists and private equity firms require GAAP-compliant financial statements showing total assets, liabilities, and true profitability.

Bank financing: Lenders evaluate balance sheet strength, including accounts receivable as collateral and accounts payable as obligations.

Business valuation: Accurate valuation multiples depend on accrual-based earnings before interest, taxes, depreciation, and amortization (EBITDA).

Acquisition preparation: Buyers expect historical accrual-based statements to assess true business value and identify hidden liabilities.

Regulatory and Compliance Requirements

GAAP compliance: Publicly traded companies and businesses seeking audited financial statements must use accrual accounting. GAAP explicitly requires accrual basis for external financial reporting.

IRS regulations: The Internal Revenue Service mandates accrual accounting for:

- C corporations (with limited exceptions)

- Businesses with average annual gross receipts exceeding $27 million

- Businesses maintain inventory as an income-producing factor

- Certain partnerships and tax shelters

Industry-specific requirements: Some industries face additional regulations. Healthcare providers, government contractors, and franchisees often must use accrual accounting regardless of size.

Making the Transition

Businesses can switch from cash to accrual accounting, though the process requires careful planning:

IRS approval: Changing accounting methods requires filing Form 3115 (Application for Change in Accounting Method) and receiving IRS approval.

Adjustment period: The transition year requires adjustments to prevent double-counting or omitting transactions that span the change date.

System implementation: Moving to accrual accounting typically requires upgrading accounting software and potentially hiring professional accountants.

Historical restatement: Some situations require restating prior periods’ financial statements under the new method for comparative purposes.

The transition complexity reinforces the importance of choosing the right method initially, based on long-term business plans rather than short-term convenience.

Practical Examples: Cash vs Accrual Accounting in Action

Real-world scenarios illustrate how these methods create different financial pictures from identical business activities.

Example 1: Freelance Graphic Designer (Cash Basis)

Sarah’s Design Studio operates as a sole proprietorship providing graphic design services. Sarah uses cash basis accounting.

December 2025 Activity:

- Completed three client projects totaling $15,000

- Sent invoices on December 20, 2025

- Purchased new design software for $2,400 (paid immediately)

- Received $8,000 payment from the November projects

Cash Basis December 2025 Financial Results:

- Revenue: $8,000 (only November payments received)

- Expenses: $2,400 (software paid)

- Net Income: $5,600

January 2026 Activity:

- Received $15,000 from December projects

- No new expenses

Cash Basis January 2026 Financial Results:

- Revenue: $15,000 (December work, January payment)

- Expenses: $0

- Net Income: $15,000

Analysis: Sarah’s cash basis statements show wildly fluctuating monthly income despite consistent work output. December appears weak ($5,600 profit) while January appears exceptional ($15,000 profit). This makes budgeting and financial planning challenging.

Example 2: Same Business Under Accrual Accounting

If Sarah used accrual accounting instead:

Accrual Basis December 2025 Financial Results:

- Revenue: $15,000 (work completed in December)

- Expenses: $200 (software amortized over 12 months: $2,400 ÷ 12)

- Net Income: $14,800

- Accounts Receivable: $15,000 (invoices sent, payment pending)

Accrual Basis January 2026 Financial Results:

- Revenue: $0 (no new work completed)

- Expenses: $200 (monthly software amortization)

- Net Income: -$200

- Cash Received: $15,000 (reduces accounts receivable, doesn’t affect income)

Analysis: Accrual accounting shows December as a strong month ($14,800 profit), reflecting actual work completed. January shows minimal activity (slight loss), accurately representing that no new projects were delivered. The financial statements match economic reality rather than payment timing.

Example 3: Retail Business Inventory Challenge

Tech Gadgets LLC sells consumer electronics. Understanding the difference between cash and accrual becomes critical with inventory.

November 2025:

- Purchased $50,000 in inventory from the supplier (payment due December 30)

- Sold $30,000 in products (cost basis: $20,000)

- Received $25,000 cash from customers; $5,000 remains on account

Cash Basis November Results:

- Revenue: $25,000 (only cash received)

- Expenses: $0 (inventory not yet paid)

- Net Income: $25,000

This shows $25,000 profit, but ignores the $50,000 payment due in December and the $30,000 in actual inventory costs.

Accrual Basis November Results:

- Revenue: $30,000 (all sales completed)

- Cost of Goods Sold: $20,000 (matching expense for sold inventory)

- Gross Profit: $10,000

- Accounts Receivable: $5,000

- Accounts Payable: $50,000

- Inventory (remaining): $30,000

Accrual accounting reveals the true economic picture: $10,000 gross profit, $30,000 in unsold inventory, and $50,000 owed to suppliers. This comprehensive view enables accurate assessment of working capital needs and profitability.

Advanced Considerations and Hybrid Approaches

Some businesses navigate the complexity between pure cash and pure accrual methods.

Modified Cash Basis Accounting

Modified cash basis combines elements of both methods. Businesses record most transactions on a cash basis, but track certain accrual items like:

- Fixed assets and depreciation

- Long-term liabilities and loans

- Inventory (when material to operations)

This hybrid approach provides some accrual benefits while maintaining cash accounting. However, the modified cash basis doesn’t satisfy GAAP requirements and may not be acceptable for audited statements.

Cash Flow Management Under Accrual Accounting

Businesses using accrual accounting must actively manage the disconnect between reported income and available cash. Key strategies include:

Cash flow forecasting: Project when accounts receivable will convert to cash and when accounts payable will require payment. This prevents liquidity crises despite profitable operations.

Monitoring the cash conversion cycle: Track the time between paying suppliers and collecting from customers. Shorter cycles improve cash position.

Maintaining cash reserves: Build emergency funds to cover periods when accrued revenue hasn’t yet been converted to cash.

Analyzing cash flow statements: Review operating, investing, and financing cash flows separately from income statements to understand true liquidity.

Tax Planning Strategies

Sophisticated businesses leverage accounting method choice for tax optimization:

Strategic method selection by entity: Some business structures allow different accounting methods for different entities or divisions, optimizing tax timing.

Revenue recognition timing: Under accrual accounting, businesses can sometimes defer revenue recognition using specific criteria, delaying tax liability.

Expense acceleration: Both methods allow year-end expense acceleration, but accrual accounting provides additional tools through accrued expenses and prepaid assets.

Working with tax professionals: The complexity of tax implications makes professional guidance essential for businesses near revenue thresholds or considering method changes.

Common Mistakes and How to Avoid Them

Understanding pitfalls helps businesses implement their chosen method effectively.

Cash Basis Mistakes

Ignoring future obligations: Cash basis businesses sometimes make decisions based solely on current bank balance, forgetting about unpaid bills or uncollected invoices. This can lead to cash flow crises.

Solution: Maintain informal tracking of accounts receivable and payable even under cash accounting. Know what’s owed and what’s due.

Inconsistent application: Some businesses accidentally mix methods, recording some transactions when earned and others when paid.

Solution: Establish clear procedures and consistently apply cash basis rules to all transactions.

Missing tax planning opportunities: Failing to strategically time year-end payments wastes valuable tax deductions.

Solution: Review accounts payable in December and prepay January expenses when beneficial for tax purposes.

Accrual Basis Mistakes

Neglecting cash flow monitoring: Focusing exclusively on accrual-based profit while ignoring cash position can cause liquidity problems.

Solution: Review cash flow statements monthly alongside income statements. Track days sales outstanding and days payable outstanding.

Improper revenue recognition: Recording revenue before it’s truly earned violates accrual principles and can overstate income.

Solution: Apply revenue recognition criteria consistently. Revenue should be recorded when earned, realizable, and measurable, not simply when invoiced.

Inadequate bad debt reserves: Failing to estimate uncollectible accounts overstates assets and income.

Solution: Analyze historical collection patterns and establish appropriate allowances for doubtful accounts.

Overcomplicated systems: Implementing unnecessarily complex accrual systems wastes resources without adding value.

Solution: Match accounting system sophistication to business complexity. Small businesses don’t need enterprise-level systems.

The Math Behind Money: Financial Ratios and Analysis

The choice between cash and accrual accounting affects the financial ratios used to assess business health.

Ratios Requiring Accrual Accounting

Several critical financial metrics become meaningless under cash accounting:

Current Ratio: Current Assets ÷ Current Liabilities measures short-term liquidity. Cash accounting doesn’t track accounts receivable or accounts payable, making this ratio impossible to calculate accurately.

Quick Ratio: (Current Assets – Inventory) ÷ Current Liabilities assesses immediate liquidity. Again, requires accrual-based balance sheet data.

Days Sales Outstanding (DSO): (Accounts Receivable ÷ Revenue) × 365 measures how quickly customers pay. Cash accounting doesn’t track receivables.

Efficiency Ratios: Metrics like inventory turnover and asset turnover require accrual-based data to match revenues with the assets that generated them.

Profitability Analysis

Accrual accounting enables more sophisticated profitability analysis:

Gross Profit Margin: (Revenue – Cost of Goods Sold) ÷ Revenue shows product profitability. Proper matching of revenue and costs requires accrual accounting.

Operating Margin: Operating Income ÷ Revenue reveals operational efficiency. Accrual accounting’s matching principle ensures expenses align with related revenue.

EBITDA Margin: EBITDA ÷ Revenue measures operational cash generation before financing and accounting decisions. While related to cash flow, it’s calculated from accrual-based income statements.

These metrics support data-driven decision-making and enable comparison with industry benchmarks, critical for competitive positioning and strategic planning.

Building Financial Literacy Through Accounting Method Understanding

Mastering the difference between cash and accrual accounting builds broader financial literacy.

Connecting to Personal Finance

The same timing principles apply to personal financial management:

Personal cash basis thinking: Most individuals naturally think in cash terms—income when paychecks arrive, expenses when bills are paid. This mirrors cash basis accounting.

Personal accrual thinking: Credit cards create a personal version of accounts payable. Charging $1,000 in December but paying in January means the economic impact (expense) occurred in December, even though cash left the account in January.

Understanding this distinction helps with budgeting and avoiding the trap of spending based on current bank balance while ignoring credit card obligations.

Investment Implications

Investors analyzing companies must understand which accounting method drives reported results:

Earnings quality: Accrual-based earnings can be manipulated through aggressive revenue recognition or delayed expense recording. Cash flow statements provide a reality check.

Cash flow analysis: Even profitable companies (on an accrual basis) can fail if they can’t convert receivables to cash quickly enough. Investors should analyze both earnings and cash flow.

Valuation principles: Discounted cash flow models ultimately value businesses based on future cash generation, not accrual-based accounting profits. Understanding the difference prevents overvaluing companies with strong reported earnings but weak cash flow.

This knowledge supports evidence-based investing and better assessment of business quality.

💰 Cash vs Accrual Accounting Calculator

Compare how the same transactions appear under different accounting methods

💵 Cash Basis Results

📊 Accrual Basis Results

Conclusion: Making the Right Accounting Choice for Your Business

The difference between Cash vs Accrual Accounting extends far beyond simple bookkeeping preferences. This fundamental choice shapes tax liability, financial visibility, regulatory compliance, and strategic decision-making capacity.

Cash accounting delivers simplicity, direct cash flow visibility, and favorable tax timing for small businesses with straightforward operations. It works when transactions are simple, payment cycles are short, and regulatory requirements don’t mandate accrual methods.

Accrual accounting provides comprehensive financial insight, accurate profitability measurement, and compliance with GAAP standards. It becomes essential as businesses grow, seek financing, manage inventory, or operate with extended payment terms.

The math behind money reveals that timing matters as much as amounts. A business showing $100,000 profit under cash accounting might show $150,000 under accrual accounting—or vice versa—depending on when customers pay and when bills come due.

Actionable Next Steps

For new business owners:

- Assess your business type, expected revenue, and growth plans

- Consult with a CPA or tax professional about method implications

- Choose the method that aligns with long-term goals, not just immediate convenience

- Implement proper accounting software and procedures from day one

For existing businesses:

- Review whether your current method still serves your needs

- Evaluate if you’re approaching IRS revenue thresholds requiring method changes

- Consider transitioning to accrual accounting before seeking investment or loans

- Maintain both accrual records and cash flow projections regardless of official method

For financial literacy building:

- Study how public companies report earnings versus cash flow

- Practice analyzing both balance sheets and cash flow statements

- Understand how accounts receivable and payable affect working capital

The choice between cash and accrual accounting represents a foundational decision in building financial literacy and business success. Understanding both methods—and their implications—empowers better decisions about money, taxes, and long-term wealth building.

Data-driven insights emerge when accounting methods match business reality. Choose wisely, implement consistently, and let the numbers guide strategic decisions.

References

[1] Internal Revenue Service. (2025). “Publication 538: Accounting Periods and Methods.” IRS.gov.

[2] Financial Accounting Standards Board. (2025). “Generally Accepted Accounting Principles.” FASB.org.

[3] American Institute of CPAs. (2025). “Accrual Accounting vs. Cash Basis Accounting.” AICPA.org.

[4] U.S. Securities and Exchange Commission. (2025). “Financial Reporting Manual.” SEC.gov.

[5] Harvard Business School. (2024). “Understanding Financial Statements: The Matching Principle.” HBS Online.

[6] Journal of Accountancy. (2024). “Cash vs. Accrual: Choosing the Right Method for Your Business.” JournalofAccountancy.com.

[7] Small Business Administration. (2025). “Guide to Small Business Accounting Methods.” SBA.gov.

Author Bio

Max Fonji is a data-driven financial educator and the voice behind The Rich Guy Math. With expertise in financial analysis and valuation principles, Max breaks down complex money concepts into clear, evidence-based insights. His approach combines analytical precision with educational clarity, helping readers understand the math behind wealth building, investing fundamentals, and sound financial decision-making.

Educational Disclaimer

This article provides educational information about accounting methods and should not be construed as professional accounting, tax, or legal advice. Accounting method selection has significant tax and regulatory implications that vary based on individual business circumstances.

Readers should consult with qualified certified public accountants (CPAs), tax professionals, and legal advisors before making accounting method decisions or changes. The information presented reflects general principles and may not apply to specific situations, industries, or jurisdictions.

While every effort has been made to ensure accuracy, accounting regulations and tax laws change frequently. Verify current requirements with appropriate regulatory authorities and professional advisors before implementing any accounting strategies discussed in this article.