Imagine buying a brand-new laptop for $1,200 today. Five years from now, would you still be able to sell it for the same price? Of course not! That laptop loses value over time as technology advances, components wear out, and newer models hit the market. This gradual loss of value is called depreciation, and understanding it is crucial whether you’re managing personal finances, running a business, or making smart investment decisions.

Depreciation isn’t just an accounting concept buried in financial textbooks—it’s a real-world phenomenon that affects everything from the car in your driveway to the equipment in a factory. For business owners, it’s a valuable tax deduction. For investors analyzing company financials, it’s a critical metric that reveals how efficiently a company manages its assets. And for anyone trying to build wealth, understanding depreciation helps you make smarter decisions about which assets to buy and when. IRS – Depreciation of Assets

In this comprehensive guide, we’ll break down everything you need to know about depreciation in plain English. You’ll learn what it is, why it matters, how to calculate it using different methods, and how to apply this knowledge in real-world scenarios.

TL;DR

- Depreciation is the systematic allocation of an asset’s cost over its useful life, reflecting the gradual loss of value due to wear, obsolescence, or age

- Businesses use depreciation as a non-cash expense to reduce taxable income while spreading the cost of long-term assets across multiple accounting periods

- The four main depreciation methods are Straight-Line (equal annual expense), Declining Balance (accelerated), Units of Production (usage-based), and Sum-of-the-Years’ Digits (accelerated)

- Depreciation impacts both the income statement (as an expense) and the balance sheet (reducing asset value), making it essential for financial analysis and investment decisions

- Understanding depreciation helps investors evaluate a company’s true profitability and assess how efficiently management allocates capital to productive assets

What Is Depreciation? The Complete Definition

In simple terms, depreciation means the reduction in value of an asset over time due to wear and tear, age, or obsolescence.

From an accounting perspective, depreciation is a method of allocating the cost of a tangible asset over its useful life. Instead of recording the entire purchase price as an expense in the year you buy the asset, depreciation spreads that cost across multiple years—matching the expense with the revenue the asset helps generate. Investopedia – Depreciation

Why Does Depreciation Matter?

Depreciation serves several critical purposes:

- Matching Principle: In accounting, the matching principle states that expenses should be recorded in the same period as the revenues they help generate. A delivery truck used for 10 years helps generate revenue throughout that decade, so its cost should be spread across those 10 years.

- Tax Benefits: Depreciation is a deductible expense that reduces taxable income. Even though no cash actually leaves the business when depreciation is recorded, it still lowers the tax bill—creating real savings.

- Accurate Financial Reporting: Depreciation ensures that a company’s balance sheet reflects the true current value of its assets, not just what was originally paid for them.

- Investment Analysis: For investors evaluating stocks, understanding depreciation helps assess whether a company is investing appropriately in maintaining and replacing its productive assets. Companies in different industries have vastly different depreciation profiles, affecting their stock market performance.

What Assets Can Be Depreciated?

Not every asset can be depreciated. To qualify for depreciation, an asset must meet these criteria:

You must own it (not lease it, unless it’s a capital lease)

You must use it in a business or income-producing activity

It must have a determinable useful life

It must be expected to last more than one year

Common depreciable assets include:

- Buildings (but not land)

- Vehicles and transportation equipment

- Machinery and manufacturing equipment

- Office furniture and fixtures

- Computer equipment and software

- Tools and equipment

Non-depreciable assets:

- Land (it doesn’t wear out)

- Inventory (expensed when sold)

- Personal-use property

- Assets held for investment (like stocks and bonds)

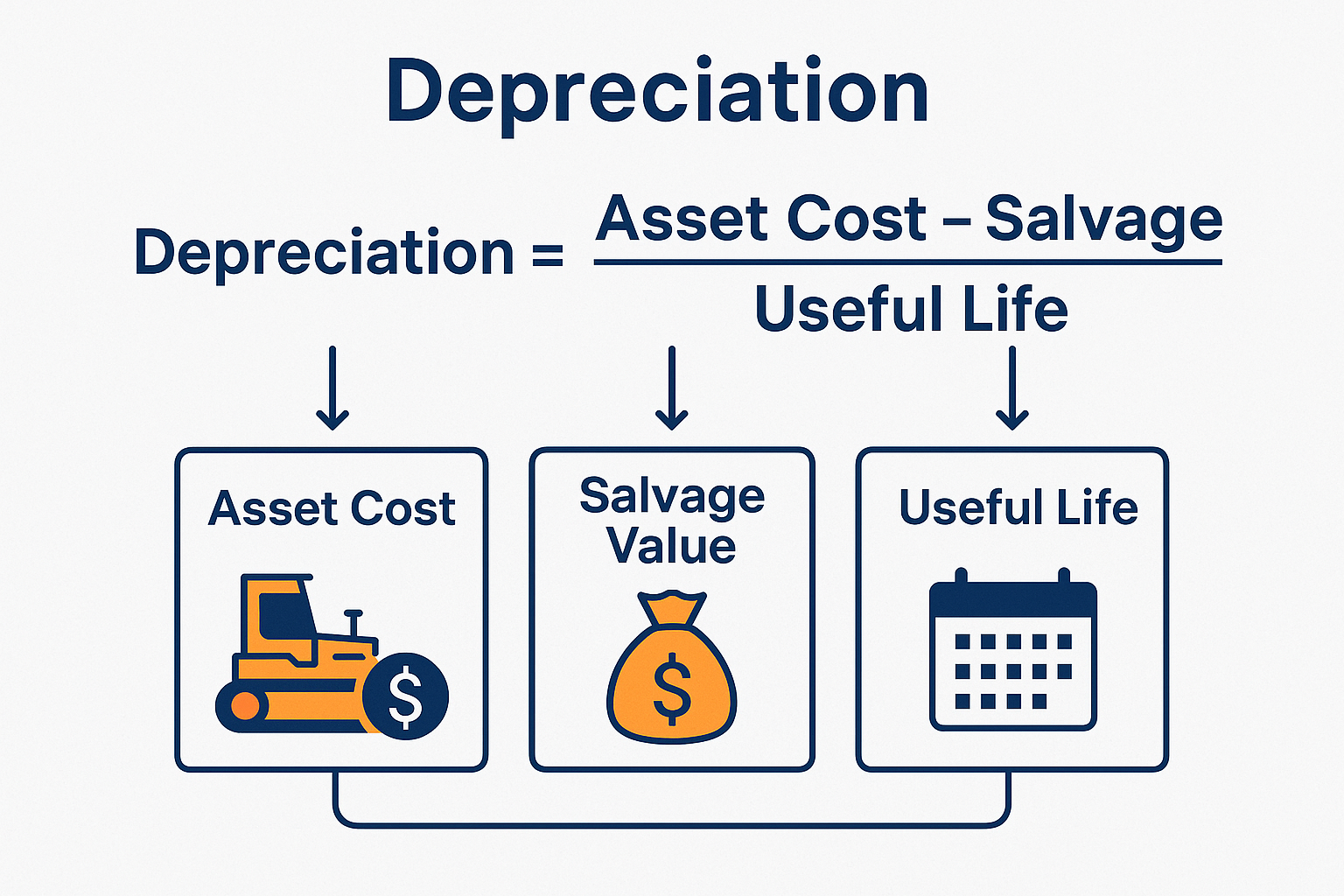

The Fundamental Depreciation Formula

While different depreciation methods use different formulas, they all start with the same basic components:

Depreciation Expense = (Asset Cost – Salvage Value) / Useful Life

Let’s break down each component:

- Asset Cost (also called “basis”): The total amount paid to acquire and prepare the asset for use, including purchase price, delivery fees, installation costs, and any other expenses necessary to make the asset operational.

- Salvage Value (also called “residual value” or “scrap value”): The estimated amount you expect to receive when you dispose of the asset at the end of its useful life. This could be zero for some assets.

- Useful Life: The estimated period over which the asset will be productively used in the business. This is typically measured in years, but can also be measured in units produced, hours used, or miles driven.

“The depreciable amount of an asset is its cost minus its estimated salvage value—this is the total amount that will be expensed over the asset’s useful life.”

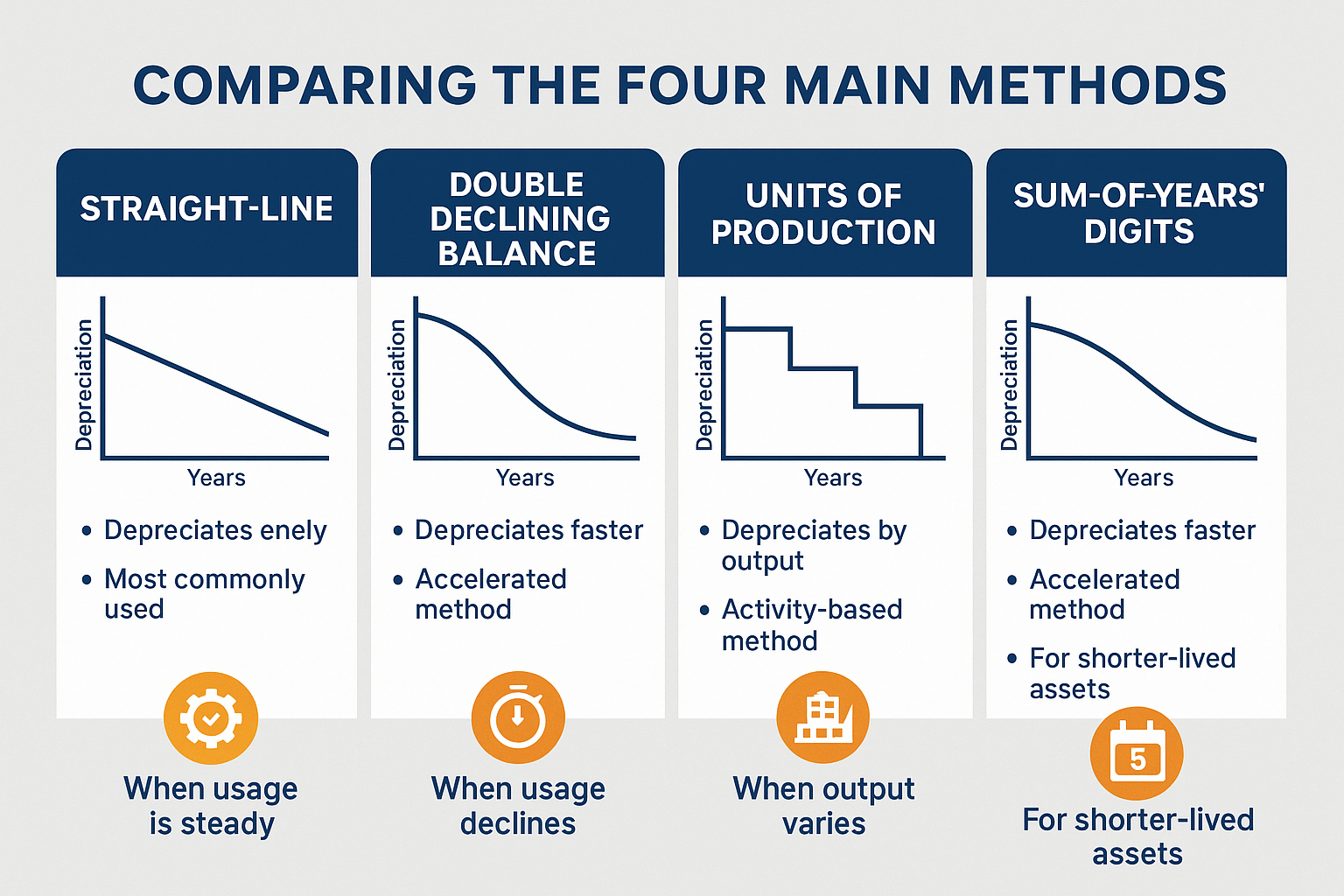

The Four Main Depreciation Methods Explained

Different depreciation methods suit different types of assets and business needs. Let’s explore each one with detailed examples.

1. Straight-Line Depreciation Method

The straight-line method is the simplest and most commonly used depreciation method. It allocates an equal amount of depreciation expense to each year of the asset’s useful life.

Formula:

Annual Depreciation Expense = (Asset Cost - Salvage Value) / Useful Life in YearsExample:

A company purchases manufacturing equipment for $50,000. The equipment is expected to last 10 years and have a salvage value of $5,000.

- Depreciable Amount = $50,000 – $5,000 = $45,000

- Annual Depreciation = $45,000 / 10 years = $4,500 per year

Depreciation Schedule:

| Year | Beginning Book Value | Depreciation Expense | Accumulated Depreciation | Ending Book Value |

|---|---|---|---|---|

| 1 | $50,000 | $4,500 | $4,500 | $45,500 |

| 2 | $45,500 | $4,500 | $9,000 | $41,000 |

| 3 | $41,000 | $4,500 | $13,500 | $36,500 |

| 4 | $36,500 | $4,500 | $18,000 | $31,500 |

| 5 | $31,500 | $4,500 | $22,500 | $27,500 |

| 6 | $27,500 | $4,500 | $27,000 | $23,000 |

| 7 | $23,000 | $4,500 | $31,500 | $18,500 |

| 8 | $18,500 | $4,500 | $36,000 | $14,000 |

| 9 | $14,000 | $4,500 | $40,500 | $9,500 |

| 10 | $9,500 | $4,500 | $45,000 | $5,000 |

When to use straight-line depreciation:

- Assets that provide consistent benefits over time

- Office furniture, buildings, and equipment with predictable wear

- When simplicity and consistency are priorities

- For financial reporting, when you want to smooth out expenses

2. Declining Balance Depreciation Method

The declining balance method is an accelerated depreciation method that records larger depreciation expenses in the early years of an asset’s life and smaller expenses in later years.

This method recognizes that many assets lose value more quickly when they’re new and provide greater benefits in their early years.

The most common version is the Double Declining Balance (DDB) method.

Formula:

Depreciation Rate = (1 / Useful Life) × 2

Annual Depreciation = Book Value at Beginning of Year × Depreciation RateImportant: With declining balance, you ignore salvage value in the calculation but never depreciate below it.

Example:

Using the same equipment from before: Cost = $50,000, Useful Life = 10 years, Salvage Value = $5,000.

- Depreciation Rate = (1/10) × 2 = 0.20 or 20%

Depreciation Schedule (first 5 years):

| Year | Beginning Book Value | Depreciation Expense (20%) | Accumulated Depreciation | Ending Book Value |

|---|---|---|---|---|

| 1 | $50,000 | $10,000 | $10,000 | $40,000 |

| 2 | $40,000 | $8,000 | $18,000 | $32,000 |

| 3 | $32,000 | $6,400 | $24,400 | $25,600 |

| 4 | $25,600 | $5,120 | $29,520 | $20,480 |

| 5 | $20,480 | $4,096 | $33,616 | $16,384 |

When to use declining balance depreciation:

- Technology and computer equipment that becomes obsolete quickly

- Vehicles that lose significant value in early years

- Assets that require more maintenance as they age (offsetting lower depreciation with higher repair costs)

- For tax purposes, to accelerate deductions and improve cash flow

3. Units of Production Depreciation Method

The units of production method bases depreciation on actual usage rather than time. This method is ideal for assets whose wear and tear depends more on how much they’re used than how old they are.

Formula:

Depreciation per Unit = (Asset Cost - Salvage Value) / Total Estimated Units

Annual Depreciation = Depreciation per Unit × Units Produced in YearExample:

A delivery company purchases a truck for $80,000 with an expected salvage value of $8,000. The truck is estimated to last 200,000 miles.

- Depreciable Amount = $80,000 – $8,000 = $72,000

- Depreciation per Mile = $72,000 / 200,000 miles = $0.36 per mile

If the truck drives 40,000 miles in Year 1:

- Year 1 Depreciation = 40,000 × $0.36 = $14,400

If it drives 35,000 miles in Year 2:

- Year 2 Depreciation = 35,000 × $0.36 = $12,600

When to use units of production depreciation:

- Manufacturing equipment (depreciates based on units produced)

- Vehicles (based on miles driven)

- Mining equipment (based on tons extracted)

- Any asset where usage varies significantly from year to year

4. Sum-of-the-Years’ Digits (SYD) Method

The sum-of-the-years’ digits method is another accelerated depreciation technique that produces results between straight-line and declining balance methods.

Formula:

SYD = (n × (n + 1)) / 2

Where n = useful life in years

Depreciation Expense = (Remaining Life / SYD) × (Cost - Salvage Value)Example:

Using our equipment example: Cost = $50,000, Useful Life = 10 years, Salvage Value = $5,000.

- SYD = (10 × 11) / 2 = 55

- Depreciable Amount = $50,000 – $5,000 = $45,000

Depreciation Schedule (first 5 years):

| Year | Remaining Life | Fraction | Depreciation Expense | Accumulated Depreciation | Book Value |

|---|---|---|---|---|---|

| 1 | 10 | 10/55 | $8,182 | $8,182 | $41,818 |

| 2 | 9 | 9/55 | $7,364 | $15,545 | $34,455 |

| 3 | 8 | 8/55 | $6,545 | $22,091 | $27,909 |

| 4 | 7 | 7/55 | $5,727 | $27,818 | $22,182 |

| 5 | 6 | 6/55 | $4,909 | $32,727 | $17,273 |

When to use SYD depreciation:

- Assets that lose value quickly but not as dramatically as a declining balance

- When you want accelerated depreciation but with more predictable patterns

- For tax planning purposes

How Depreciation Impacts Financial Statements

Understanding how depreciation flows through financial statements is crucial for anyone analyzing company financials or making investment decisions.

Impact on the Income Statement

Depreciation appears as an operating expense on the income statement, reducing net income. However, it’s a non-cash expense—meaning no money actually leaves the company when depreciation is recorded.

Example Income Statement Extract:

Revenue: $500,000

Cost of Goods Sold: -$200,000

________

Gross Profit: $300,000

Operating Expenses:

Salaries: -$100,000

Rent: -$30,000

Depreciation: -$20,000

Other Expenses: -$50,000

________

Operating Income: $100,000Impact on the Balance Sheet

On the balance sheet, depreciation affects the Property, Plant & Equipment (PP&E) section:

- Gross PP&E remains at original cost

- Accumulated Depreciation increases each year (a contra-asset account)

- Net PP&E (Book Value) = Gross PP&E – Accumulated Depreciation

Example Balance Sheet Extract:

Property, Plant & Equipment:

Equipment (at cost): $200,000

Less: Accumulated Depreciation: -$80,000

________

Net PP&E: $120,000Impact on Cash Flow Statement

On the cash flow statement, depreciation is added back to net income in the operating activities section because it’s a non-cash expense that reduced net income but didn’t reduce cash.

Example Cash Flow Statement Extract:

Cash Flow from Operating Activities:

Net Income: $100,000

Add: Depreciation: +$20,000

Changes in Working Capital: -$10,000

________

Net Cash from Operations: $110,000“Depreciation is a non-cash expense that reduces taxable income without reducing cash—creating a tax shield that improves actual cash flow.”

Depreciation in Real-World Business Scenarios

Let’s examine how depreciation works in practice across different industries and situations.

Case Study 1: Manufacturing Company

TechParts Manufacturing purchases a CNC machine for $250,000 with an expected useful life of 8 years and salvage value of $10,000.

Using straight-line depreciation:

- Annual Depreciation = ($250,000 – $10,000) / 8 = $30,000/year

Business Impact:

- Tax Savings: If the company’s tax rate is 25%, the annual depreciation deduction saves $30,000 × 0.25 = $7,500 in taxes each year

- Financial Reporting: The depreciation expense reduces reported profits but doesn’t affect cash

- Replacement Planning: After 8 years, the company knows it needs to budget for a replacement machine

Case Study 2: Delivery Service

QuickShip Logistics operates a fleet of 50 delivery vans. Each van costs $35,000 and is expected to drive 150,000 miles before retirement, with a salvage value of $5,000.

Using units of production depreciation:

- Depreciation per Mile = ($35,000 – $5,000) / 150,000 = $0.20 per mile

- If the fleet drives 2,000,000 miles in Year 1: Depreciation = 2,000,000 × $0.20 = $400,000

- If the fleet drives 1,800,000 miles in Year 2: Depreciation = 1,800,000 × $0.20 = $360,000

Business Impact:

- Depreciation expense matches actual vehicle usage

- Better reflects the true cost of operations

- Helps with the accurate pricing of delivery services

Case Study 3: Real Estate Investment

Greenfield Properties purchases a commercial building for $2,000,000 (land value: $400,000, building value: $1,600,000). The building has a useful life of 39 years (IRS standard for commercial real estate).

Using straight-line depreciation:

- Annual Depreciation = $1,600,000 / 39 years = $41,026/year

- Remember: Land is NOT depreciated

Business Impact:

- Annual tax deduction of $41,026 reduces taxable rental income

- Over 10 years, accumulated depreciation = $410,260

- This creates a significant tax benefit for passive income investors

Comparing Depreciation Methods: Which One Should You Choose?

Different depreciation methods produce different financial outcomes. Here’s a side-by-side comparison using the same asset:

Asset: Equipment costing $100,000 with a 5-year useful life and $10,000 salvage value

| Year | Straight-Line | Double Declining | Sum-of-Years’ Digits | Units of Production* |

|---|---|---|---|---|

| 1 | $18,000 | $40,000 | $30,000 | $22,500 |

| 2 | $18,000 | $24,000 | $24,000 | $18,000 |

| 3 | $18,000 | $14,400 | $18,000 | $20,250 |

| 4 | $18,000 | $8,640 | $12,000 | $16,200 |

| 5 | $18,000 | $2,960 | $6,000 | $13,050 |

| Total | $90,000 | $90,000 | $90,000 | $90,000 |

*Assumes variable production: 25%, 20%, 22.5%, 18%, 14.5%

Key Observations:

- Total depreciation is the same across all methods (cost minus salvage value)

- Accelerated methods (declining balance, SYD) front-load depreciation expenses

- Straight-line provides consistency and predictability

- Units of production vary based on actual usage

Decision Framework: Choosing the Right Method

| Choose This Method | When… |

|---|---|

| Straight-Line | • You want simplicity and consistency • The asset provides equal benefits over time • Financial reporting is the priority • You’re depreciating buildings or office furniture |

| Declining Balance | • The asset loses value quickly when new • You want maximum early-year tax deductions • You’re depreciating technology or vehicles • Cash flow optimization is important |

| Units of Production | • Asset wear depends on usage, not time • Usage varies significantly year to year • You’re depreciating manufacturing equipment or vehicles • You want to match depreciation to revenue generation |

| Sum-of-Years’ Digits | • You want accelerated depreciation • You prefer more predictable patterns than declining balance • You’re planning for tax optimization |

Common Depreciation Mistakes to Avoid

Even experienced business owners and accountants make these common errors:

1. Depreciating Land

Mistake: Including land value in the depreciable basis of real estate.

Why it’s wrong: Land doesn’t wear out or become obsolete, so it’s never depreciated.

Correct approach: Separate land value from building value. Only depreciate the building.

2. Using the Wrong Useful Life

Mistake: Guessing at useful life instead of following IRS guidelines or industry standards.

Why it matters: The IRS has specific guidelines (Modified Accelerated Cost Recovery System – MACRS) that dictate useful lives for different asset classes.

Correct approach: Consult IRS Publication 946 or work with a tax professional to determine the correct recovery period.

3. Forgetting About Salvage Value

Mistake: Depreciating an asset down to zero when it has significant residual value.

Why it’s wrong: This overstates depreciation expense and understates asset value.

Correct approach: Estimate a reasonable salvage value based on market research and never depreciate below it.

4. Not Recording Partial-Year Depreciation

Mistake: Taking a full year of depreciation in the year an asset is purchased, regardless of purchase date.

Why it’s wrong: This violates the matching principle and can create tax issues.

Correct approach: Use conventions like half-year (assume all assets purchased at mid-year) or mid-month for real estate.

5. Continuing to Depreciate Fully Depreciated Assets

Mistake: Recording depreciation expense after accumulated depreciation equals the depreciable amount.

Why it’s wrong: Once an asset is fully depreciated, no more expense should be recorded (even if the asset is still in use).

Correct approach: Stop recording depreciation once book value equals salvage value, but keep the asset on the books at that value until disposal.

6. Mixing Methods Without Justification

Mistake: Switching depreciation methods from year to year without proper justification.

Why it’s wrong: Consistency is a fundamental accounting principle. Changes require disclosure and can raise red flags.

Correct approach: Choose a method and stick with it. If you must change, document the business reason and disclose it in financial statements.

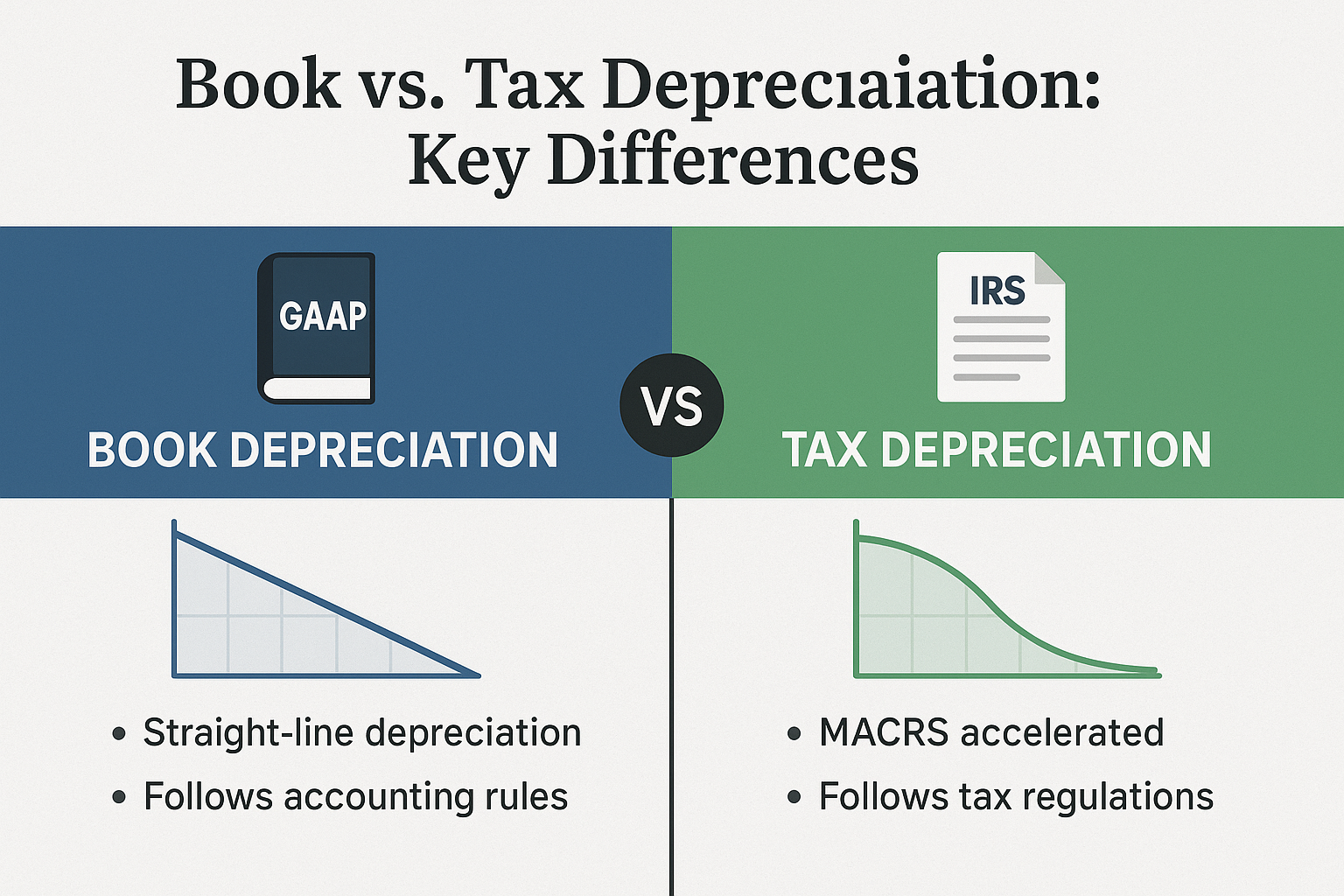

Depreciation for Tax Purposes vs Financial Reporting

One of the most important concepts to understand is that tax depreciation and book depreciation can differ.

Book Depreciation (Financial Reporting)

- Used for financial statements provided to investors, lenders, and stakeholders

- Follows Generally Accepted Accounting Principles (GAAP) or International Financial Reporting Standards (IFRS)

- Companies choose the method that best matches expenses with revenues

- Typically uses straight-line depreciation for consistency

Tax Depreciation

- Used for tax returns filed with the IRS

- Follows Internal Revenue Code rules, primarily MACRS (Modified Accelerated Cost Recovery System)

- Designed to encourage business investment through accelerated deductions

- Often results in lower taxable income in early years compared to book income

Key Tax Depreciation Concepts

MACRS (Modified Accelerated Cost Recovery System):

- The primary tax depreciation system in the United States

- Uses predetermined recovery periods and methods

- Common recovery periods: 3, 5, 7, 15, 27.5, and 39 years

- Generally uses 200% declining balance for 3-, 5-, 7-, and 10-year property

Section 179 Deduction:

- Allows businesses to immediately expense (rather than depreciate) certain asset purchases

- 2025 limit: Up to $1,220,000 in qualifying purchases

- Phases out for businesses purchasing more than $3,050,000 in assets

- Excellent for small businesses wanting immediate tax relief

Bonus Depreciation:

- Allows businesses to deduct a large percentage of eligible asset costs in the first year

- Percentage varies by year (check current tax law)

- Applies to new and used qualified property

- Particularly valuable for larger capital investments

“Many businesses maintain two sets of depreciation records—one for financial reporting (book depreciation) and one for tax purposes (tax depreciation)—to optimize both financial presentation and tax savings.”

How Investors Should Interpret Depreciation

For those analyzing companies as potential investments, understanding depreciation provides crucial insights. Whether you’re evaluating high dividend stocks or growth companies, depreciation tells an important story.

What Depreciation Reveals About a Company

1. Capital Intensity

Companies with high depreciation relative to revenue are capital-intensive—they require significant investment in fixed assets to generate sales.

- High capital intensity: Manufacturing, airlines, telecommunications, utilities

- Low capital intensity: Software, consulting, financial services

Example: An airline might have depreciation expense equal to 10-15% of revenue, while a software company might have less than 2%.

2. Asset Age and Replacement Needs

The ratio of accumulated depreciation to gross PP&E indicates how old a company’s assets are:

Asset Age Ratio = Accumulated Depreciation / Gross PP&E- Higher ratio (70%+): Assets are old; significant capital expenditures are likely needed soon

- Lower ratio (30% or less): Assets are relatively new; less immediate replacement pressure

3. Maintenance Capital Expenditures

Compare depreciation expense to capital expenditures (CapEx):

- CapEx > Depreciation: Company is growing or upgrading its asset base

- CapEx ≈ Depreciation: The Company is maintaining its current capacity

- CapEx < Depreciation: Company may be underinvesting; assets may be deteriorating

This is particularly important when evaluating dividend investing strategies, as companies that underinvest in maintenance may be artificially inflating free cash flow.

Depreciation and Valuation Metrics

EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization):

Many investors use EBITDA to compare companies because it removes the effects of different depreciation methods and capital structures.

EBITDA = Net Income + Interest + Taxes + Depreciation + AmortizationHowever, be cautious: EBITDA ignores the real cost of maintaining and replacing assets. As Warren Buffett famously said, “Does management think the tooth fairy pays for capital expenditures?”

Free Cash Flow:

A better metric for many investors is free cash flow, which accounts for capital expenditures:

Free Cash Flow = Operating Cash Flow - Capital ExpendituresThis metric recognizes that depreciation, while non-cash, represents the eventual need to replace assets.

Red Flags Related to Depreciation

Watch for these warning signs when analyzing companies:

Extending useful lives: If a company suddenly increases the estimated useful life of assets, it reduces annual depreciation expense and artificially boosts profits.

Increasing salvage values: Similar to above—higher salvage values reduce depreciation expense.

CapEx consistently below depreciation: Suggests underinvestment that could hurt future competitiveness.

Frequent impairment charges: Large write-downs suggest the company has been overstating asset values.

Aggressive depreciation policies: Using unrealistically long useful lives compared to industry peers. FASB – Accounting Standards Codification

Depreciation Across Different Industries

Different industries have vastly different depreciation profiles. Understanding these differences helps with stock market analysis.

Manufacturing & Heavy Industry

Characteristics:

- High capital intensity

- Significant PP&E on the balance sheet

- Depreciation is often 5-15% of revenue

- Long-lived assets (10-30 years)

Key Metrics:

- Asset turnover (Revenue / PP&E)

- Maintenance CapEx ratio

- Depreciation as % of revenue

Example Companies: Caterpillar, General Electric (industrial divisions), steel manufacturers

Technology & Software

Characteristics:

- Low capital intensity for software companies

- Higher for hardware manufacturers

- Rapid obsolescence of equipment

- Often use accelerated depreciation

Key Metrics:

- R&D spending vs. depreciation

- Asset-light business models

- Intangible assets (often amortized, not depreciated)

Example Companies: Microsoft (low depreciation), Intel (moderate-high depreciation)

Real Estate

Characteristics:

- Very high PP&E relative to other assets

- Long useful lives (27.5 years residential, 39 years commercial)

- Depreciation is a major tax benefit

- Land is not depreciated

Key Metrics:

- Cap rate (Net Operating Income / Property Value)

- Funds From Operations (FFO) = Net Income + Depreciation + Amortization

- Depreciation as a tax shield

Example Companies: Real Estate Investment Trusts (REITs)

Airlines & Transportation

Characteristics:

- Extremely capital-intensive

- High depreciation expense

- Assets have moderate useful lives (15-30 years for aircraft)

- Significant maintenance requirements

Key Metrics:

- Depreciation per available seat mile

- Fleet age

- CapEx for fleet renewal

Example Companies: Delta, United Airlines, FedEx

Retail & E-commerce

Characteristics:

- Moderate capital intensity

- Store fixtures, warehouses, technology

- Increasing investment in automation

- E-commerce has a different profile than brick-and-mortar

Key Metrics:

- Sales per square foot

- Depreciation as % of revenue

- Technology investment trends

Example Companies: Walmart (higher depreciation), Amazon (moderate-high for warehouses)

Advanced Depreciation Topics

Impairment of Assets

Sometimes an asset’s value drops suddenly due to damage, obsolescence, or market changes. This is called impairment.

When to test for impairment:

- Significant decrease in market value

- Adverse change in how the asset is used

- Negative economic or legal factors

- Accumulation of costs exceeding original expectations

How impairment works:

- Compare the asset’s book value to its recoverable amount (the higher of fair value or value in use)

- If the book value exceeds the recoverable amount, record an impairment loss

- Reduce the asset’s carrying value and record the loss on the income statement

Example:

A company has equipment with a book value of $100,000. Due to technological advancement, the equipment’s fair value drops to $60,000.

- Impairment Loss = $100,000 – $60,000 = $40,000

- This loss appears on the income statement

- The asset’s new book value becomes $60,000

- Future depreciation is based on this new value

Depreciation Recapture

When you sell a depreciated asset for more than its book value, the IRS may require you to pay depreciation recapture tax.

How it works:

- You depreciated an asset, reducing your taxable income

- You sell the asset for more than its depreciated book value

- The IRS “recaptures” some of that depreciation as ordinary income

Example:

- Original cost: $50,000

- Accumulated depreciation: $30,000

- Book value: $20,000

- Sale price: $35,000

The gain of $15,000 ($35,000 – $20,000) is split:

- $15,000 is depreciation recapture (taxed at ordinary income rates, up to 25%)

- If sold for more than the original cost, the excess would be a capital gain

Component Depreciation

Instead of depreciating an entire asset as one unit, component depreciation breaks it into parts with different useful lives.

Example: Commercial Building

- Structure: 40-year life

- HVAC system: 15-year life

- Roof: 20-year life

- Elevators: 15-year life

This method provides more accurate depreciation and is required under IFRS (International Financial Reporting Standards).

Real-World Example: Complete Depreciation Analysis

Let’s walk through a comprehensive example that ties together everything we’ve learned.

Scenario: TechManufacturing Inc. purchases a robotic assembly line on January 1, 2025, for $500,000. Additional costs include:

- Shipping: $10,000

- Installation: $15,000

- Employee training: $25,000

The equipment is expected to:

- Produce 1,000,000 units over its lifetime

- Last 10 years

- Has a salvage value of $50,000

Step 1: Calculate Asset Cost

Asset Cost = Purchase Price + Shipping + Installation

Asset Cost = $500,000 + $10,000 + $15,000 = $525,000Note: Training costs are expensed immediately, not capitalized.

Step 2: Calculate Depreciation Using Different Methods

Straight-Line Method:

Annual Depreciation = ($525,000 - $50,000) / 10 years

Annual Depreciation = $47,500 per yearDouble Declining Balance:

Depreciation Rate = (1/10) × 2 = 20%

Year 1: $525,000 × 20% = $105,000

Year 2: ($525,000 - $105,000) × 20% = $84,000

Year 3: ($420,000 - $84,000) × 20% = $67,200Units of Production:

Depreciation per Unit = ($525,000 - $50,000) / 1,000,000 units

Depreciation per Unit = $0.475 per unit

If Year 1 production = 120,000 units:

Year 1 Depreciation = 120,000 × $0.475 = $57,000Step 3: Analyze the Impact

Income Statement Impact (Year 1):

| Method | Depreciation Expense | Effect on Net Income (25% tax rate) |

|---|---|---|

| Straight-Line | $47,500 | -$35,625 after tax |

| Double Declining | $105,000 | -$78,750 after tax |

| Units of Production | $57,000 | -$42,750 after tax |

Tax Savings (Year 1):

| Method | Depreciation Expense | Tax Savings (25% rate) |

|---|---|---|

| Straight-Line | $47,500 | $11,875 |

| Double Declining | $105,000 | $26,250 |

| Units of Production | $57,000 | $14,250 |

Cash Flow Impact:

While net income is lower with accelerated depreciation, actual cash is higher due to reduced tax payments. The double declining method saves an additional $14,375 in cash in Year 1 compared to the straight-line.

Step 4: Make the Decision

For financial reporting, TechManufacturing chooses straight-line depreciation because:

- It provides consistent, predictable expenses

- It better matches the equipment’s steady contribution to revenue

- It presents more stable earnings to investors

For tax purposes, TechManufacturing uses MACRS (likely 7-year property with 200% declining balance) to:

- Maximize early-year deductions

- Improve cash flow

- Reduce current tax liability

This dual approach is perfectly legal and common among businesses.

Practical Tips for Business Owners

If you’re a business owner dealing with depreciation, here are actionable strategies:

1. Maintain Detailed Asset Records

Create a fixed asset register that tracks:

- Asset description and location

- Purchase date and cost

- Depreciation method and useful life

- Accumulated depreciation

- Current book value

This documentation is essential for tax audits and financial reporting.

2. Review Depreciation Assumptions Annually

At least once a year, assess whether your depreciation assumptions still make sense:

- Are useful lives still accurate?

- Have salvage values changed?

- Should any assets be tested for impairment?

- Are you using the optimal methods?

3. Maximize Tax Benefits

Work with a tax professional to:

- Take advantage of Section 179 expensing for qualifying purchases

- Utilize bonus depreciation when available

- Time asset purchases strategically (end of tax year vs. beginning)

- Segregate building components for faster depreciation (cost segregation study)

4. Plan for Asset Replacement

Use depreciation as a planning tool:

- Set aside funds for eventual replacement

- Monitor when assets will be fully depreciated

- Plan capital budgets based on expected replacement needs

- Consider leasing vs. buying decisions

5. Understand the Cash Flow Impact

Remember that depreciation:

- Reduces taxable income (saves cash on taxes)

- Doesn’t require cash outlay when recorded

- Should be considered when evaluating project profitability

- Affects borrowing capacity (lower net income may impact loan covenants)

| Year | Beginning Value | Depreciation | Accumulated | Ending Value |

|---|

Conclusion: Mastering Depreciation for Financial Success

Depreciation is far more than an obscure accounting concept—it’s a powerful tool that impacts business profitability, tax strategy, investment analysis, and financial decision-making. Whether you’re a business owner, investor, or someone simply trying to understand financial statements, mastering depreciation gives you a significant advantage.

Key points to remember:

Depreciation systematically allocates asset costs over their useful lives, matching expenses with the revenues they help generate

Different methods serve different purposes—straight-line for consistency, accelerated methods for tax benefits, units of production for usage-based assets

Depreciation is a non-cash expense that reduces taxable income and creates valuable tax savings without reducing cash

For investors, depreciation reveals crucial insights about capital intensity, asset age, maintenance needs, and management’s capital allocation decisions

Tax depreciation and book depreciation can differ, allowing businesses to optimize both financial reporting and tax outcomes

Your Next Steps

If you’re a business owner:

- Review your current depreciation policies with your accountant

- Ensure you’re maximizing available tax benefits (Section 179, bonus depreciation)

- Implement a fixed asset tracking system if you don’t have one

- Plan for future asset replacements based on depreciation schedules

If you’re an investor:

- Start analyzing depreciation in companies you’re evaluating

- Compare depreciation policies across industry peers

- Calculate key metrics like CapEx vs. depreciation ratios

- Look for red flags like extended useful lives or unusual policy changes

- Explore investment strategies that consider asset quality and replacement needs

If you’re learning about finance:

- Practice calculating depreciation using different methods

- Study real company financial statements to see how depreciation is disclosed

- Understand how depreciation flows through all three financial statements

- Learn about industry-specific depreciation patterns

Depreciation might seem dry on the surface, but it’s a window into how businesses create value, manage assets, and generate returns. By understanding depreciation deeply, you’ll make better business decisions, identify better investments, and build a stronger foundation for financial success.

The companies that master depreciation strategy—choosing the right methods, timing asset purchases wisely, and maintaining optimal asset bases—often outperform their peers over the long term. Similarly, investors who understand depreciation can spot opportunities and avoid pitfalls that others miss.

As you continue your financial education journey, remember that concepts like depreciation are building blocks. Each piece of knowledge you gain connects to others, creating a comprehensive understanding of how businesses operate and how wealth is created. Keep learning, keep questioning, and keep building your financial literacy.

For more insights on building wealth through smart financial decisions, explore our guides on passive income strategies and understanding market dynamics.

There is no universally “good” depreciation rate—it depends entirely on the industry and business model. Capital-intensive industries like manufacturing and transportation naturally have higher depreciation rates (8-15% of revenue), while asset-light businesses like software companies may have rates below 3%. Compare a company’s depreciation rate to industry peers rather than absolute benchmarks.

For U.S. tax purposes, most businesses use the Modified Accelerated Cost Recovery System (MACRS), which assigns specific recovery periods to different asset classes. For example, computers are 5-year property, office furniture is 7-year property, and commercial buildings are 39-year property. MACRS typically uses accelerated depreciation methods. Additionally, Section 179 allows immediate expensing of up to $1,220,000 (2025 limit) for qualifying assets.

Yes, but changes must be justified and properly disclosed. For financial reporting, changing depreciation methods requires demonstrating that the new method better reflects the asset’s consumption pattern. The change must be disclosed in the notes to financial statements. For tax purposes, changing methods typically requires IRS approval using Form 3115 (Application for Change in Accounting Method).

When you sell an asset, you stop recording depreciation. Calculate any gain or loss by comparing the sale price to the book value (cost minus accumulated depreciation). If you sell for more than book value, you have a gain; if less, you have a loss. For tax purposes, gains may be subject to depreciation recapture, taxing the gain up to the original cost at ordinary income rates.

Depreciation is a non-cash expense, meaning it reduces net income without reducing cash. On the cash flow statement, depreciation is added back to net income in the operating activities section. However, depreciation does affect cash indirectly by reducing taxable income and therefore reducing cash paid for taxes—creating a valuable tax shield.

Land is not depreciated because it doesn’t wear out, become obsolete, or get used up over time. Unlike buildings, equipment, or vehicles, land has an indefinite useful life. In fact, land often appreciates over time. When purchasing real estate, you must allocate the purchase price between land (not depreciable) and buildings/improvements (depreciable).

Depreciation applies to tangible assets (physical assets you can touch), such as buildings, equipment, and vehicles. Amortization applies to intangible assets (non-physical assets), such as patents, copyrights, trademarks, and goodwill. Both serve the same purpose—allocating the cost of a long-term asset over its useful life—but they apply to different asset categories.

Financial Disclaimer

This article is for educational purposes only and does not constitute financial, tax, accounting, or legal advice. Depreciation rules, tax laws, and accounting standards change regularly and vary by jurisdiction. Always consult with qualified professionals—including certified public accountants, tax advisors, and financial planners—before making business or investment decisions based on depreciation strategies. The examples provided are simplified for illustration purposes and may not reflect all complexities of real-world scenarios.

About the Author

Written by Max Fonji — With over a decade of experience in financial education and investment analysis, Max is your go-to source for clear, data-backed investing education. Max specializes in breaking down complex financial concepts into actionable insights that help readers make smarter money decisions. Through TheRichGuyMath.com, Max has helped thousands of people improve their financial literacy and build wealth through informed investing strategies.

Related posts:

What Is SmartPass? Raptor Digital Hall Pass Explained for K-12 Schools

What Is SmartPass? Raptor Digital Hall Pass Explained for K-12 Schools

What Is the 3x Rent Rule & How to Calculate It (With Examples)

What Is the 3x Rent Rule & How to Calculate It (With Examples)

Types of Income: A Complete Guide to Earning and Growing Wealth

Types of Income: A Complete Guide to Earning and Growing Wealth

Tax Filing: A Clear, Step-by-Step Guide for Stress-Free Taxes

Tax Filing: A Clear, Step-by-Step Guide for Stress-Free Taxes

Return on Assets (ROA): Definition, Formula & How to Improve It

Return on Assets (ROA): Definition, Formula & How to Improve It

How to Save Money Fast: A Smart Savings Plan That Actually Works

How to Save Money Fast: A Smart Savings Plan That Actually Works