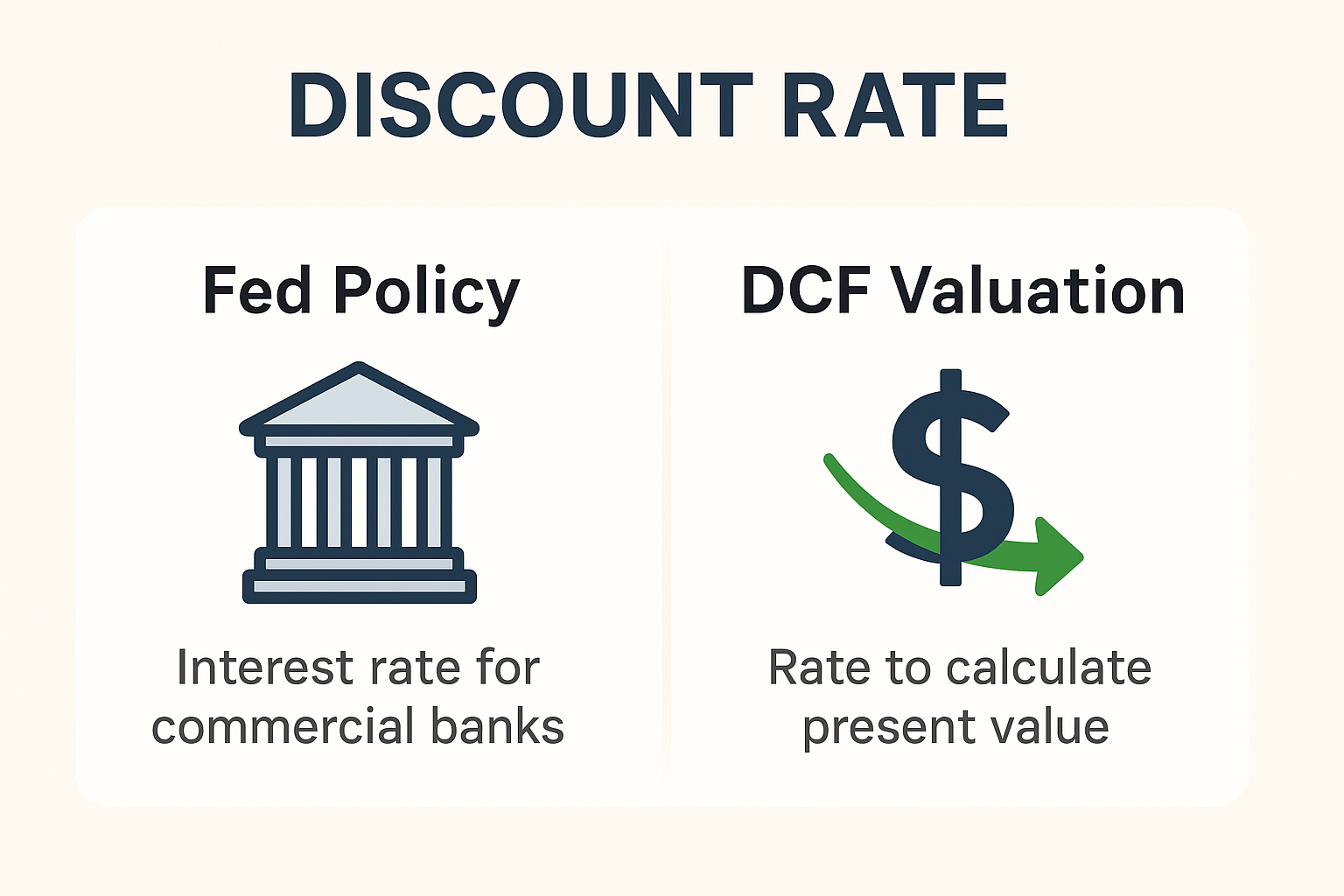

Discount Rate: is the rate used to figure out how much future money is worth today.

The term discount rate is one of the most widely used yet often misunderstood concepts in finance. Depending on context, it can mean:

- Federal Reserve Discount Rate – the interest rate charged to commercial banks for short-term loans.

- Valuation Discount Rate – the rate used in discounted cash flow (DCF) analysis to determine the present value of future money.

While these two meanings serve different purposes, both share a common principle: the time value of money. A dollar today is worth more than a dollar tomorrow.

This guide breaks down what the discount rate is, how it’s calculated, why it matters, and how investors and businesses use it.

What Is the Discount Rate?

Federal Reserve Discount Rate

- The Fed’s discount rate is the interest rate at which commercial banks can borrow directly from the Federal Reserve.

- It’s part of U.S. monetary policy and influences broader interest rates across the economy.

- When the Fed raises the discount rate, borrowing becomes more expensive → slowing down economic activity.

- When the Fed lowers it, borrowing becomes cheaper → stimulating growth.

Discount Rate in Valuation (DCF)

- In investing, the discount rate is used to calculate the present value of future cash flows.

- It reflects:

- Risk-free rate (usually U.S. Treasury yields)

- Risk premium for uncertainty

- Opportunity cost of capital

Discount Rate Formula

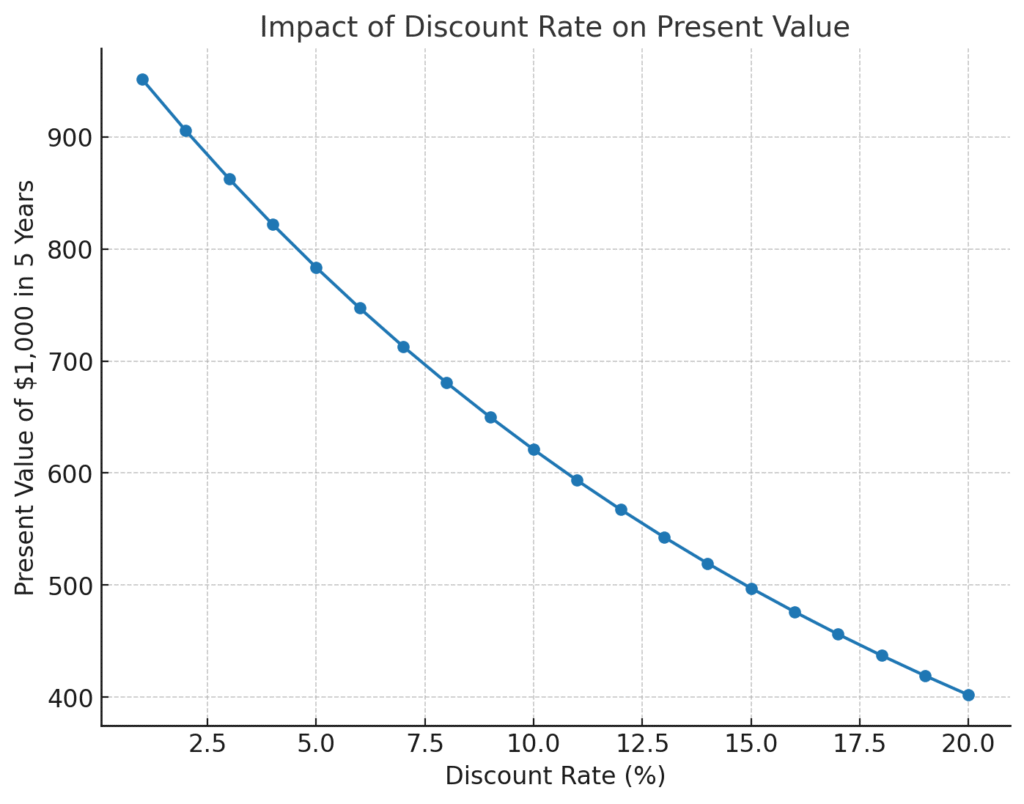

The present value (PV) of a future cash flow (FV) is calculated as: PV = FV/(1+r)n

Where:

- PV = Present Value

- FV = Future Value

- r = Discount Rate

- n = Number of periods

Example Calculation

If you expect $1,000 in 5 years and the discount rate is 10%: PV = 1000/(1+0.10)5=620.92

That means $1,000 received five years from now is only worth about $621 today at a 10% discount rate.

Discount Rate vs. Interest Rate vs. Required Rate of Return

| Term | Meaning | Use Case |

|---|---|---|

| Discount Rate | Rate used to calculate present value | Valuation, DCF |

| Interest Rate | Cost of borrowing or return on lending | Loans, mortgages, bonds |

| Required Return | Minimum return expected by an investor | Equity analysis, project finance |

How the Federal Reserve Uses the Discount Rate

- Primary Credit Rate: Short-term loans to healthy banks.

- Secondary Credit Rate: Loans to banks with temporary financial difficulty (slightly higher).

- Seasonal Credit Rate: For small banks with seasonal liquidity needs (e.g., farming communities).

By adjusting these rates, the Fed impacts liquidity, inflation, and lending across the economy.

Advantages & Disadvantages of Discount Rate

Advantages

- Captures the time value of money

- Useful for comparing projects or investments

- Incorporates risk premiums into valuation

- Central banks use it to manage the economy

Disadvantages

- Highly sensitive to assumptions — small changes can drastically alter valuations

- No universal “correct” rate — depends on investor judgment

- Can oversimplify risks if chosen poorly

Investor & Business Use Cases

- Businesses: Use discount rates to evaluate projects and capital investments.

- Investors: Use DCF models to determine if a stock is undervalued or overvalued.

- Banks: Monitor the Fed discount rate for funding and liquidity planning.

- Individuals: Use in retirement planning, annuities, or bond valuation.

It’s the rate used to figure out how much future money is worth today.

Use the formula: PV = FV/(1+r)n

Interest rate = cost of borrowing/lending. Discount rate = used in valuation or set by the Fed.

Higher discount rates → lower present values → lower company valuations.

Other Link:

Source Links:

The Bottom Line

The discount rate is a cornerstone of finance. In the policy world, it’s a lever the Federal Reserve pulls to influence the economy. In investing, it’s the rate used to translate uncertain future cash flows into today’s dollars.

For investors, businesses, and everyday savers, understanding the discount rate helps them make more informed financial decisions.

Related posts:

What Is SmartPass? Raptor Digital Hall Pass Explained for K-12 Schools

What Is SmartPass? Raptor Digital Hall Pass Explained for K-12 Schools

What Is the 3x Rent Rule & How to Calculate It (With Examples)

What Is the 3x Rent Rule & How to Calculate It (With Examples)

Types of Income: A Complete Guide to Earning and Growing Wealth

Types of Income: A Complete Guide to Earning and Growing Wealth

Tax Filing: A Clear, Step-by-Step Guide for Stress-Free Taxes

Tax Filing: A Clear, Step-by-Step Guide for Stress-Free Taxes

Return on Assets (ROA): Definition, Formula & How to Improve It

Return on Assets (ROA): Definition, Formula & How to Improve It

How to Save Money Fast: A Smart Savings Plan That Actually Works

How to Save Money Fast: A Smart Savings Plan That Actually Works