When comparing a savings account offering 5% interest compounded monthly against another offering 5% compounded annually, most people assume they’re identical. They’re not. The first account actually delivers 5.116% in real returns, and understanding this difference is the foundation of making smarter financial decisions.

The effective interest rate reveals the true cost of borrowing or the actual return on savings by accounting for compounding frequency. While banks advertise nominal rates, the math behind money shows that how often interest compounds dramatically changes what you actually earn or pay. This concept separates financially literate investors from those who leave money on the table.

Key Takeaways

- The effective interest rate (EIR) represents the actual annual return or cost after accounting for compounding, providing a more accurate picture than nominal rates

- Compounding frequency directly impacts returns—the more frequently interest compounds, the higher the effective rate, even with identical nominal rates

- The formula EAR = (1 + i/n)^n – 1 calculates the effective annual rate, where i is the nominal rate and n is the number of compounding periods per year

- Different financial products use different compounding schedules, making effective rate comparisons essential for evaluating savings accounts, loans, bonds, and credit cards

- Effective interest rate differs from real interest rate; EIR accounts for compounding, while real rates subtract inflation from nominal rates

What Is the Effective Interest Rate?

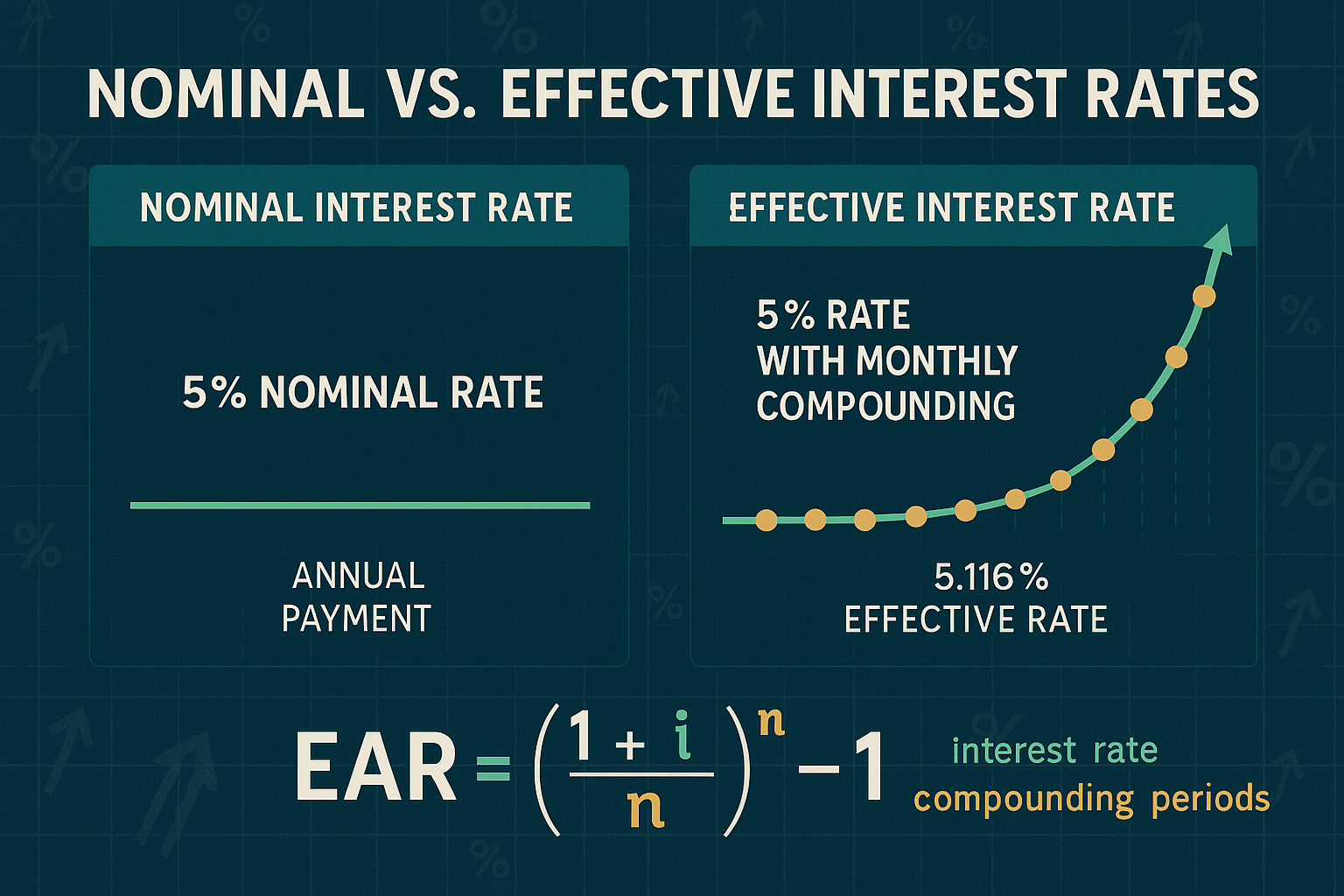

The effective interest rate (EIR) measures the actual interest earned or paid over a year when accounting for the effects of compounding. Unlike the nominal interest rate, which simply states the advertised percentage, the effective rate reveals what actually happens to your money.

Here’s why this matters: When a bank advertises a 6% annual interest rate compounded monthly, you don’t earn exactly 6% by year’s end. You earn slightly more because each month’s interest starts earning interest itself. This is compound growth in action, and it’s the mathematical foundation of wealth building.

The effective interest rate goes by several names depending on context and geography:

- Effective Annual Rate (EAR)

- Annual Equivalent Rate (AER)

- Effective Annual Interest Rate (EAIR)

- Effective APR

In the United States, consumers typically encounter Annual Percentage Yield (APY) for savings products and Annual Percentage Rate (APR) for borrowing products. Both represent forms of effective interest rates, though APR may include additional fees beyond pure interest.[1]

The Core Principle: Compounding Changes Everything

Simple interest calculates returns based solely on the principal amount. If you invest $1,000 at 5% simple interest, you earn exactly $50 per year, every year.

Compound interest calculates returns on both the principal and previously earned interest. That same $1,000 at 5% compounded monthly doesn’t just earn $50; it earns $51.16 in the first year because each month’s interest immediately begins generating additional returns.

This seemingly small difference compounds exponentially over time. After 30 years, simple interest delivers $2,500 total. Compound interest at the same nominal rate delivers $4,467, nearly double the wealth accumulation. See our full guide on Compound vs Simple interest

“Compound interest is the eighth wonder of the world. He who understands it, earns it; he who doesn’t, pays it.” — Attributed to Albert Einstein

Understanding effective interest rates means understanding the math behind this compounding effect and using it to your advantage.

How to Calculate Effective Interest Rate

The effective annual rate formula provides precise mathematical clarity:

EAR = (1 + i/n)^n – 1

Where:

- EAR = Effective Annual Rate

- i = Nominal interest rate (expressed as a decimal)

- n = Number of compounding periods per year

Let’s break down this formula with a concrete example.

Step-by-Step Calculation Example

Scenario: A savings account advertises a 5% annual interest rate, compounded monthly. What’s the effective annual rate?

Step 1: Convert the nominal rate to decimal form

- i = 5% = 0.05

Step 2: Identify the compounding frequency

- Monthly compounding = 12 periods per year

- n = 12

Step 3: Apply the formula

- EAR = (1 + 0.05/12)^12 – 1

- EAR = (1 + 0.004167)^12 – 1

- EAR = (1.004167)^12 – 1

- EAR = 1.05116 – 1

- EAR = 0.05116

Step 4: Convert to a percentage

- EAR = 5.116%

Result: While the bank advertises 5%, you actually earn 5.116% annually, an additional 0.116% that compounds into significant wealth over decades.

Compounding Frequency Comparison Table

The table below demonstrates how compounding frequency affects the effective rate for a 5% nominal rate:

| Compounding Frequency | Periods per Year (n) | Effective Annual Rate | Additional Return vs. Annual |

|---|---|---|---|

| Annually | 1 | 5.000% | 0.000% |

| Semi-annually | 2 | 5.063% | 0.063% |

| Quarterly | 4 | 5.095% | 0.095% |

| Monthly | 12 | 5.116% | 0.116% |

| Weekly | 52 | 5.125% | 0.125% |

| Daily | 365 | 5.127% | 0.127% |

| Continuous | ∞ | 5.127% | 0.127% |

Key insight: The difference between annual and monthly compounding (0.116%) might seem trivial on a $1,000 balance, just $1.16 per year. But on a $100,000 balance, that’s $116 annually. Over 30 years with regular contributions, this difference creates thousands in additional wealth.

This principle applies equally to debt. When you carry a credit card balance with daily compounding, you’re paying a higher effective rate than the advertised APR suggests. Understanding this math is fundamental to risk management and financial literacy.

Why the Effective Interest Rate Matters More Than the Nominal Rate

Nominal rates tell you what banks advertise. Effective rates tell you what actually happens to your money. This distinction separates informed financial decisions from costly mistakes.

Real-World Impact on Savings

Consider two savings accounts:

Account A: 4.5% APY, compounded daily

Account B: 4.6% APY, compounded annually

Most people choose Account B because 4.6% exceeds 4.5%. But let’s calculate the effective rates:

Account A:

- EAR = (1 + 0.045/365)^365 – 1 = 4.603%

Account B:

- EAR = (1 + 0.046/1)^1 – 1 = 4.600%

Account A actually delivers higher returns despite the lower advertised rate because daily compounding creates more frequent growth opportunities. On a $50,000 balance, Account A generates approximately $15 more per year, and that compounds over time.

This demonstrates why comparing APY vs APR requires understanding the underlying compounding mechanics.

Real-World Impact on Borrowing

The effective interest rate becomes even more critical when evaluating debt. Credit cards typically compound interest daily, which significantly increases the actual cost of carrying a balance.

Example: A credit card advertises an 18% APR with daily compounding.

- Nominal rate: 18%

- Daily rate: 18% / 365 = 0.0493% per day

- EAR = (1 + 0.18/365)^365 – 1 = 19.72%

The reality: You’re actually paying 19.72% annually—1.72 percentage points higher than advertised. On a $5,000 balance, that’s an additional $86 in interest charges per year.

This math explains why credit utilization management and paying balances in full matter so much. The effective rate on carried balances erodes wealth faster than most people realize.

Bond Valuation and the Effective Interest Method

In bond accounting and investing, the effective interest method provides superior accuracy compared to straight-line amortization. This method calculates interest expense or income based on the bond’s carrying value and the effective interest rate at issuance.[3]

Why this matters: When bonds are purchased at a premium or discount, the effective interest rate differs from the stated coupon rate. The effective rate represents the bond’s yield to maturity, the actual return an investor earns if holding to maturity.

Example:

- Bond face value: $10,000

- Coupon rate: 5% ($500 annual payment)

- Purchase price: $9,500 (discount)

- Years to maturity: 5

The effective interest rate exceeds 5% because the investor receives $500 annually plus gains $500 total ($10,000 – $9,500) at maturity. The effective rate calculates to approximately 5.8%, reflecting the true return.

Professional investors use effective interest rates to compare bonds with different coupon rates, maturities, and purchase prices on an apples-to-apples basis. This is fundamental to valuation principles and evidence-based investing.

Effective Interest Rate vs Other Interest Rate Concepts

Financial terminology includes multiple “interest rates,” each measuring different aspects of returns or costs. Understanding these distinctions prevents confusion and improves decision-making.

Effective Interest Rate vs Nominal Interest Rate

Nominal interest rate represents the stated, advertised rate without accounting for compounding frequency. It’s the percentage banks display prominently in marketing materials.

Effective interest rate accounts for compounding frequency, revealing the actual annual return or cost.

The relationship: Effective rate always equals or exceeds nominal rate. They’re identical only when compounding occurs once annually. As compounding frequency increases, the effective rate rises above the nominal rate. See our full guide on Nominal vs Effective Interest Rate

| Nominal Rate | Compounding | Effective Rate | Difference |

|---|---|---|---|

| 6% | Annual | 6.000% | 0.000% |

| 6% | Quarterly | 6.136% | 0.136% |

| 6% | Monthly | 6.168% | 0.168% |

| 6% | Daily | 6.183% | 0.183% |

Effective Interest Rate vs Real Interest Rate

Real interest rate subtracts inflation from the nominal rate, measuring purchasing power growth rather than nominal dollar growth.

Formula: Real Rate ≈ Nominal Rate – Inflation Rate

Example:

- Nominal rate: 5%

- Inflation: 3%

- Real rate: ≈ 2%

Effective interest rate accounts for compounding but ignores inflation. It measures actual dollar returns in nominal terms.

The distinction matters: A savings account offering 5% APY (5.116% effective rate with monthly compounding) might seem attractive. But if inflation runs at 4%, your real return is only about 1.116%—barely outpacing purchasing power erosion.

Successful wealth building requires beating inflation with effective returns, not just accumulating nominal dollars.

Effective Interest Rate vs APR vs APY

APR (Annual Percentage Rate) represents the annualized cost of borrowing, including interest and certain fees. U.S. regulations require lenders to disclose the APR for transparency. APR typically uses the effective interest rate formula but may include origination fees, closing costs, and other charges beyond pure interest.[4]

APY (Annual Percentage Yield) represents the effective annual rate of return on savings and investment products. APY always accounts for compounding frequency, making it identical to EAR for deposit accounts.

Effective Interest Rate is the broader mathematical concept underlying both APR and APY calculations.

Practical application: When comparing savings accounts, look at APY: it already incorporates compounding. When comparing loans, examine both APR (total cost including fees) and the effective interest rate (pure interest cost) to understand the complete picture. See our full guide on APR vs APY

For major purchases like vehicles, understanding these concepts helps you apply strategies like the 20/4/10 rule more effectively.

Practical Applications of Effective Interest Rate

Understanding effective interest rate theory means nothing without practical application. Here’s how this concept influences real financial decisions.

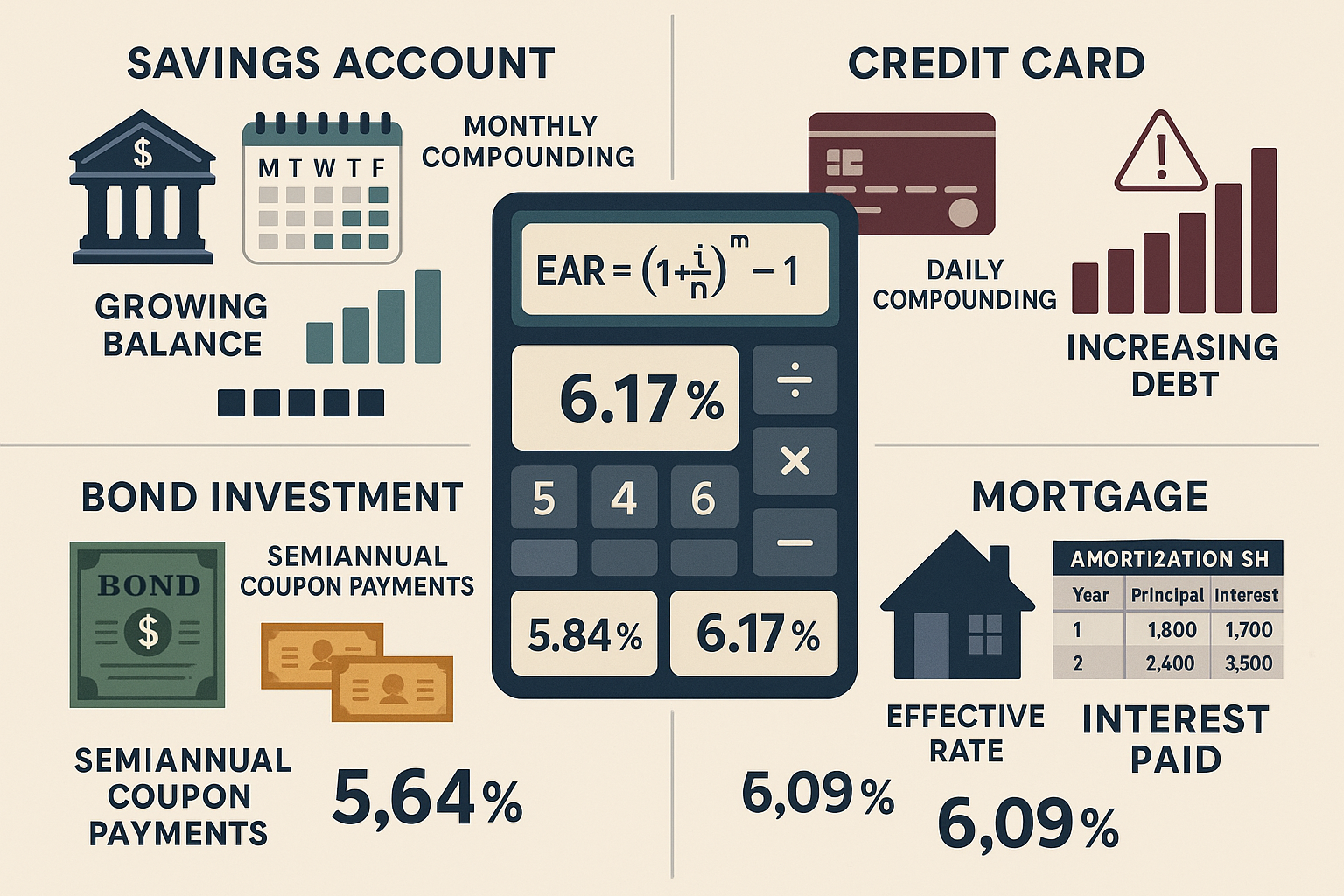

Comparing Savings Accounts and CDs

Banks compete for deposits by advertising attractive rates, but comparing requires calculating effective rates with identical compounding assumptions.

Scenario: You’re choosing between three savings options for a $25,000 emergency fund:

Option 1: Online bank offering 4.5% APY, compounded daily

Option 2: Credit union offering 4.55% APY, compounded monthly

Option 3: Traditional bank offering 4.6% APY, compounded quarterly

The APY already reflects effective rates, so direct comparison works:

- Option 1: 4.500% effective

- Option 2: 4.550% effective

- Option 3: 4.600% effective

Annual interest earned:

- Option 1: $1,125

- Option 2: $1,137.50

- Option 3: $1,150

Option 3 delivers $25 more annually than Option 1, a meaningful difference over time, especially as your balance grows.

This analysis applies equally to compound interest accounts and certificates of deposit. Always compare effective rates, not just advertised nominal rates.

Evaluating Loan Costs

Mortgage lenders, auto financiers, and personal loan providers all advertise rates differently. Calculating effective rates enables true cost comparison.

Example: Two mortgage offers for a $300,000 home loan:

Lender A:

- Nominal rate: 6.5%

- Compounding: Monthly

- Effective rate: 6.697%

Lender B:

- Nominal rate: 6.45%

- Compounding: Daily

- Effective rate: 6.664%

Despite Lender A’s higher nominal rate, Lender B’s daily compounding creates a higher effective rate. Over a 30-year mortgage, this difference costs thousands in additional interest.

Monthly payment comparison:

- Lender A: $1,896

- Lender B: $1,890

The $6 monthly difference seems trivial. But over 360 payments, Lender A costs $2,160 less in total interest due to the lower effective rate.

This mathematical precision matters for every borrowing decision, from mortgages to credit cards to personal loans. When combined with smart budgeting strategies, understanding effective rates accelerates debt payoff.

Investment Return Analysis

Professional investors use effective interest rates to evaluate bond yields, preferred stock dividends, and fixed-income investments.

Bond comparison example:

Bond X:

- Coupon rate: 4%

- Price: $950 (discount)

- Maturity: 10 years

- Effective yield: 4.58%

Bond Y:

- Coupon rate: 4.5%

- Price: $1,050 (premium)

- Maturity: 10 years

- Effective yield: 3.95%

Despite Bond Y’s higher coupon rate, Bond X delivers superior effective returns because the discount price increases yield to maturity. This is why expected return calculations must account for purchase price, not just stated yields.

Sophisticated investors apply these principles across asset classes, from dividend stocks to real estate investment trusts, always seeking the highest risk-adjusted effective returns.

Credit Card Debt Management

Credit cards represent the most common debt due to high rates and daily compounding. Understanding effective rates reveals the true cost of carrying balances.

Typical credit card:

- Advertised APR: 21.99%

- Compounding: Daily

- Effective rate: 24.60%

On a $10,000 balance, this means:

- Expected annual interest (based on APR): $2,199

- Actual annual interest (based on EAR): $2,460

- Hidden cost: $261 additional

This explains why minimum payments trap borrowers in debt cycles. The effective rate compounds daily, causing balances to grow faster than most people realize.

The math behind money clearly demonstrates that eliminating high-interest debt should precede most investing activities. A guaranteed 24.60% “return” from paying off credit card debt exceeds the expected value of most investment opportunities.

Common Misconceptions About Effective Interest Rate

Financial literacy requires not just understanding concepts but also recognizing common application errors.

Misconception 1: “Nominal and Effective Rates Are Basically the Same”

Reality: They diverge significantly as compounding frequency increases or rates rise.

At 2% with annual compounding, the difference is negligible (0%). At 20% with daily compounding, the effective rate reaches 22.13%—a 2.13 percentage point difference that dramatically impacts long-term costs.

Misconception 2: “Effective Rate Only Matters for Large Balances”

Reality: The percentage difference remains constant regardless of balance size, but the dollar impact scales proportionally.

A 0.5% effective rate advantage on $1,000 generates $5 annually. On $100,000, it generates $500 annually. Over 30 years with compound growth, even small rate differences create massive wealth gaps.

This principle underlies dollar cost averaging strategies; small, consistent advantages compound into significant outcomes.

Misconception 3: “Higher Compounding Frequency Always Means Better Returns”

Reality: Compounding frequency only matters relative to the nominal rate. A 3% rate compounded daily delivers lower returns than a 5% rate compounded annually.

Comparison:

- 3% daily compounding: 3.045% effective

- 5% annual compounding: 5.000% effective

Always compare effective rates, not compounding schedules in isolation.

Misconception 4: “Effective Rate and Real Rate Are Interchangeable”

Reality: These measure entirely different concepts.

- The effective rate accounts for compounding frequency

- Real rate adjusts for inflation

A savings account might offer a 5% effective rate (excellent compounding), but if inflation runs at 6%, the real rate is -1%; you’re losing purchasing power despite positive nominal returns.

Comprehensive financial planning requires considering both effective returns and inflation-adjusted real returns.

Advanced Considerations: Continuous Compounding

As compounding frequency increases toward infinity, effective rates approach a mathematical limit called continuous compounding.

The Continuous Compounding Formula

EAR = e^r – 1

Where:

- e = Euler’s number (approximately 2.71828)

- r = Nominal interest rate (as decimal)

Example: 5% nominal rate with continuous compounding

- EAR = e^0.05 – 1

- EAR = 2.71828^0.05 – 1

- EAR = 1.05127 – 1

- EAR = 0.05127 = 5.127%

Practical insight: Daily compounding (365 periods) yields 5.127%, identical to continuous compounding to three decimal places. This demonstrates that beyond daily compounding, additional frequency provides negligible benefit.

Some financial institutions market “continuous compounding” as a premium feature, but the mathematical reality shows minimal advantage over daily compounding. This is why data-driven insights matter; they prevent falling for marketing hype.

Building Wealth Through Effective Rate Optimization

Understanding effective interest rates transforms from theoretical knowledge to practical wealth building through systematic application.

Strategy 1: Maximize Effective Rates on Savings

Action steps:

- Compare APY (effective rates) across multiple institutions

- Prioritize online banks offering higher rates with daily compounding

- Consider high-yield savings accounts for emergency funds

- Evaluate CD ladders for longer-term savings goals

Expected impact: A 1% higher effective rate on $50,000 in savings generates $500 additional annual income—$15,000 over 30 years before compounding effects.

Strategy 2: Minimize Effective Rates on Debt

Action steps:

- Calculate effective rates on all outstanding debts

- Prioritize paying off the highest effective rate debts first

- Refinance when lower effective rates become available

- Avoid daily-compounding debt (credit cards) whenever possible

Expected impact: Reducing effective debt costs from 24% to 6% on $20,000 saves $3,600 annually, money that can be redirected toward investing fundamentals.

Strategy 3: Understand Investment Yields

Action steps:

- Calculate effective yields on bonds and fixed-income investments

- Compare dividend yields, accounting for payment frequency

- Evaluate total return, including price appreciation and compounding distributions

- Consider tax implications on effective after-tax returns

Expected impact: Selecting investments based on effective yields rather than stated rates improves portfolio returns by 0.5-1% annually, a difference that compounds into hundreds of thousands over a career.

Strategy 4: Leverage Compounding Frequency

Action steps:

- Reinvest dividends and interest immediately to maximize compounding periods

- Make debt payments more frequently than required (weekly vs. monthly) to reduce the effective interest paid

- Choose investments with automatic dividend reinvestment

- Understand how continuous compounding approaches the theoretical maximum returns

Expected impact: Increasing effective compounding frequency on a $100,000 portfolio from annual to monthly can generate an additional $15,000-$20,000 over 30 years at typical market returns.

Effective Interest Rate Calculator

💰 Effective Interest Rate Calculator

Calculate the true annual rate accounting for compounding frequency

Conclusion: Master the Math Behind Money

The effective interest rate separates financial literacy from financial confusion. While nominal rates fill marketing materials, effective rates reveal what actually happens to your wealth.

The core principle: Compounding frequency transforms stated rates into real outcomes. A seemingly small difference, 5% versus 5.116%, compounds into thousands of dollars over decades. This is the math behind money that wealthy individuals understand and apply systematically.

Actionable next steps:

- Audit your current accounts: Calculate effective rates on all savings accounts, loans, and investments. Identify opportunities to increase returns or decrease costs.

- Prioritize high-effective-rate debt elimination: Credit cards with daily compounding create the highest effective rates—often exceeding 24% annually. Eliminating this debt delivers guaranteed returns exceeding most investment opportunities.

- Optimize savings compounding: Choose accounts with the highest APY (effective rate) and most frequent compounding. Online banks typically offer superior rates compared to traditional institutions.

- Evaluate investments using effective yields: Compare bonds, preferred stocks, and fixed-income investments based on effective yields to maturity, not just stated coupon rates.

- Reinvest returns immediately: Maximize compounding frequency by automatically reinvesting dividends, interest, and distributions. This transforms stated returns into higher effective returns over time.

- Apply effective rate thinking to major decisions: Whether evaluating a mortgage, choosing between index funds, or planning retirement contributions, effective rate calculations provide clarity.

The difference between nominal and effective rates might seem like academic minutiae. But this mathematical precision creates the foundation for evidence-based investing and systematic wealth building. Understanding how compounding frequency transforms advertised rates into actual outcomes gives you a permanent advantage in every financial decision.

The math doesn’t lie. The compounding effect works with mathematical certainty, either building your wealth or eroding it through debt. Your choice is which side of the equation you occupy.

Sources

[1] Consumer Financial Protection Bureau. (2024). “Annual Percentage Rate (APR) and Annual Percentage Yield (APY).” CFPB.gov.

[2] Federal Reserve Bank of St. Louis. (2024). “The Power of Compound Interest.” Economic Research Division.

[3] Financial Accounting Standards Board. (2024). “FASB ASC 835-30: Interest – Imputation of Interest.” FASB Accounting Standards Codification.

[4] Truth in Lending Act. (2024). “Regulation Z – Annual Percentage Rate Calculations.” 12 CFR § 1026.14.

Author Bio

Max Fonji is a data-driven financial educator and the voice behind The Rich Guy Math. With expertise in financial analysis and valuation principles, Max breaks down complex financial concepts into clear, actionable insights. His evidence-based approach helps readers understand the math behind money, enabling smarter decisions about investing, debt management, and wealth building.

Educational Disclaimer

This article provides educational information about effective interest rates and should not be construed as financial advice. Individual financial situations vary significantly based on income, risk tolerance, time horizon, and personal goals. Before making investment or borrowing decisions, consult with qualified financial professionals who understand your specific circumstances. Past performance and mathematical projections do not guarantee future results. All financial decisions carry risk, and readers are responsible for conducting their own due diligence.

Frequently Asked Questions

What is the effective interest rate in simple terms?

The effective interest rate is the actual percentage you earn on savings or pay on debt after accounting for how often interest compounds. While banks advertise nominal rates, the effective rate shows what really happens to your money. For example, 5% compounded monthly actually delivers 5.116% annually because each month’s interest immediately starts earning additional returns.

How do you calculate the effective interest rate?

Use the formula: EAR = (1 + i/n)^n – 1, where i is the nominal rate (as a decimal) and n is the number of compounding periods per year. For a 6% rate compounded monthly: EAR = (1 + 0.06/12)^12 – 1 = 6.168%. This reveals the true annual return or cost after compounding effects.

Why is effective interest rate higher than nominal rate?

Compounding causes previously earned interest to generate additional interest, creating exponential rather than linear growth. The more frequently interest compounds, the more opportunities for this growth multiplication. Daily compounding produces higher effective rates than monthly, which exceeds quarterly, which beats annual compounding—all at the same nominal rate.

What’s the difference between APR and effective interest rate?

APR (Annual Percentage Rate) includes both interest and certain fees like origination costs, while effective interest rate focuses purely on interest compounding. For loans, APR provides a more complete cost picture. For savings accounts, APY (Annual Percentage Yield) represents the effective interest rate. Both APR and APY use effective rate calculations but apply them differently.

Does effective interest rate account for inflation?

No. Effective interest rate measures nominal returns after compounding but doesn’t adjust for inflation. Real interest rate subtracts inflation from nominal returns to show purchasing power growth. A 5% effective rate with 3% inflation delivers approximately 2% real return. Successful investing requires beating inflation with effective returns, not just earning positive nominal rates.

How does compounding frequency affect effective interest rate?

Higher compounding frequency increases effective rate even when nominal rates stay constant. A 5% rate compounded annually stays at 5% effective. Monthly compounding raises it to 5.116%. Daily compounding reaches 5.127%. The difference seems small but compounds significantly over decades, creating thousands in additional wealth or debt costs.

When should I use effective interest rate instead of nominal rate?

Always use effective rate when comparing financial products with different compounding schedules or evaluating true costs and returns. Nominal rates mislead when compounding frequencies differ. Use effective rates for comparing savings accounts, evaluating loan costs, analyzing bond yields, and making any decision where compounding impacts outcomes.

Can effective interest rate be lower than nominal rate?

No. Effective rate always equals or exceeds nominal rate. They’re identical only with annual compounding (once per year). Any more frequent compounding raises effective rate above nominal rate. This mathematical relationship holds universally—if someone claims an effective rate below the nominal rate, the calculation contains an error.