Figma Stock has become one of the most searched investment queries among tech-savvy investors in 2025. The collaborative design platform transformed how teams create digital products, attracting massive attention from both users and potential shareholders. But here’s the financial truth most investors miss: you cannot buy Figma stock on public exchanges yet.

The math behind Figma’s investment appeal is straightforward. The company was valued at $20 billion during Adobe’s attempted acquisition in 2022, demonstrating exceptional revenue growth and market dominance in collaborative design software. When regulators blocked that deal in late 2023, Figma returned to private ownership, leaving investors wondering how and when they might access this high-growth opportunity.

This guide explains the current status of Figma stock, the regulatory events that shaped its trajectory, and the realistic pathways available to investors who want exposure to this category-defining company. You’ll learn the mechanics of pre-IPO investing, understand why most retail investors cannot access Figma shares, and discover publicly-traded alternatives that offer similar market exposure.

Key Takeaways

- Figma is not publicly traded and cannot be purchased through standard brokerage accounts as of 2025

- The Adobe acquisition failed due to antitrust concerns from EU and UK regulators, returning Figma to private status with a $1 billion breakup fee.

- Pre-IPO access is limited to accredited investors through venture capital funds or secondary markets with significant liquidity risks.

- No official IPO date exists, though market conditions and company fundamentals suggest potential public listing within 2-3 years.

- Public alternatives include Adobe (ADBE), Autodesk (ADSK), and Microsoft (MSFT) for investors seeking design software and SaaS exposure today.

Is Figma Stock Publicly Traded?

No. Figma stock is not available on public exchanges like the NYSE or NASDAQ. The company remains privately held, meaning its shares are owned by founders, employees, and institutional venture capital investors—not available to retail investors through standard brokerage accounts.

Why Figma remains private: Most technology companies stay private during high-growth phases to avoid quarterly earnings pressure and maintain operational flexibility. Figma has raised sufficient venture capital funding to support expansion without needing public market capital. The company secured $332.9 million across multiple funding rounds before the Adobe acquisition attempt, achieving a private valuation exceeding $10 billion by 2021.

Who owns Figma today: Primary shareholders include Index Ventures, Greylock Partners, Kleiner Perkins, Sequoia Capital, and company founders Dylan Field (CEO) and Evan Wallace (CTO). These institutional investors hold preferred shares with special rights not available to common shareholders. Employee stock options represent another significant ownership block, though these shares typically carry transfer restrictions until a liquidity event occurs.

The distinction between public and private companies matters because it determines access. Public companies must register with the SEC, file regular financial disclosures, and allow anyone to purchase shares through licensed brokers. Private companies face no such requirements, controlling exactly who can invest and under what terms.[2]

Takeaway: Until Figma completes an initial public offering (IPO) or direct listing, retail investors cannot purchase shares through conventional channels. This restriction protects early investors but limits access for individual shareholders who want exposure to Figma’s growth trajectory.

For context on how public markets work, understanding absolute return strategies helps investors evaluate whether pre-IPO opportunities align with their portfolio objectives.

What Happened to the Adobe–Figma Deal?

Adobe’s $20 Billion Acquisition Explained.

In September 2022, Adobe announced plans to acquire Figma for approximately $20 billion, half cash, half stock. This represented one of the largest software acquisitions in history, valuing Figma at roughly 50 times its annual recurring revenue based on estimated 2022 performance.

The strategic rationale: Adobe sought to eliminate its primary competitor in collaborative design while expanding its Creative Cloud ecosystem. Figma’s browser-based, real-time collaboration tools represented the future of design software, directly threatening Adobe XD and other legacy products. The acquisition would have consolidated Adobe’s market dominance across creative professional tools.

Deal structure breakdown:

- Total value: $20 billion ($10 billion cash + $10 billion Adobe stock)

- Premium: Approximately 2x Figma’s last private valuation

- Expected close: 2023, pending regulatory approval

- Breakup fee: $1 billion if terminated due to regulatory rejection

The valuation multiple shocked financial analysts. At 50x revenue, Adobe was paying a significant premium even by high-growth SaaS standards. This pricing reflected Figma’s exceptional growth rate (estimated 100%+ year-over-year), near-zero churn, and network effects that made the product more valuable as more teams adopted it.

For investors evaluating similar opportunities, understanding capital allocation strategies helps assess whether management teams are deploying resources effectively or overpaying for growth.

Why the Deal Was Blocked

Regulators in the European Union and the United Kingdom formally blocked the acquisition in late 2023, citing antitrust concerns. The U.S. Department of Justice also signaled opposition, creating insurmountable regulatory barriers.[4]

Primary regulatory concerns:

- Market concentration: Adobe and Figma represented the two dominant players in professional design software, particularly for UI/UX and product design workflows

- Elimination of competition: Regulators determined Figma was Adobe’s most significant competitive threat, and the acquisition would remove that pressure

- Innovation reduction: Authorities worried that consolidation would reduce incentives for product development and competitive pricing

- Customer harm: Enterprise customers testified that competition between Adobe and Figma drove better features and lower prices

The European Commission’s investigation revealed that Adobe held 60%+ market share in certain design software categories, with Figma representing the fastest-growing alternative. Removing Figma from the competitive landscape would likely result in price increases and slower innovation—exactly what antitrust law aims to prevent.

What it means for investors: The deal’s collapse returned Figma to independent operation with an additional $1 billion in cash from the breakup fee. This capital strengthens Figma’s balance sheet, extends its runway, and reduces pressure for near-term monetization. Paradoxically, regulatory rejection may have improved Figma’s long-term value by preserving its independence and competitive positioning.

The failed acquisition demonstrates how regulatory risk affects capital structure decisions and valuation assumptions in technology M&A transactions.

Does Figma Have an IPO Planned?

Official IPO Status (As of 2025)

Figma has not announced an initial public offering date or filed preliminary registration documents (S-1) with the Securities and Exchange Commission. The company maintains a private status with no confirmed timeline for public listing.

Current official position: CEO Dylan Field has stated in interviews that Figma is “in no rush” to go public, emphasizing the company’s strong financial position and preference for long-term strategic thinking over quarterly earnings cycles. The $1 billion breakup fee from Adobe provides a substantial capital runway, reducing immediate pressure for IPO liquidity.

Financial requirements for IPO readiness:

- Revenue threshold: Typically $100M+ annual recurring revenue (Figma likely exceeds this based on 2022-2023 estimates)

- Growth rate: Sustained 40%+ year-over-year growth (Figma reportedly maintains this trajectory)

- Profitability path: Clear route to positive operating margins within 2-3 years (status unknown publicly)

- Corporate governance: Board structure, audit committees, and financial controls meeting public company standards

Most technology companies delay IPOs until market conditions favor high-growth SaaS valuations. The 2022-2023 tech market downturn suppressed IPO activity, with many companies postponing public listings until investor appetite for growth stocks recovered.

Signs Figma Could Go Public

Despite no official announcement, several indicators suggest Figma may pursue an IPO within the next 2-3 years:

1. Revenue scale and growth trajectory

Figma’s estimated annual recurring revenue (ARR) reportedly exceeded $400 million in 2022, with growth rates above 100% year-over-year.[5] This scale and velocity match or exceed comparable companies at IPO (Snowflake, Datadog, HashiCorp).

2. Market position and competitive moat

Figma dominates collaborative design with an estimated 50%+ market share among product design teams. Network effects create switching costs—as more designers use Figma, more companies adopt it as their standard tool. This defensibility attracts public market investors seeking sustainable competitive advantages.

3. Comparable tech IPO activity

The IPO market shows signs of recovery in 2025, with several high-growth SaaS companies successfully listing. Improved market conditions typically trigger a wave of delayed IPOs from well-positioned private companies.

4. Investor liquidity pressure

Venture capital investors typically seek exits within 7-10 years. Figma’s Series D funding occurred in 2020, meaning institutional investors may push for liquidity events (IPO or acquisition) by 2025-2027.

5. Corporate governance developments

Reports indicate Figma has strengthened its financial reporting infrastructure and hired executives with public company experience—common pre-IPO preparation steps.

Realistic timeline estimate: Based on these factors and typical IPO preparation timelines, a Figma public listing between late 2025 and 2027 represents a reasonable possibility—but remains speculative without official confirmation.

IPO Readiness Factors:

| Factor | Figma Status (Estimated) | Typical IPO Threshold |

|---|---|---|

| Annual Revenue | $400M+ (2022 est.) | $100M+ |

| Growth Rate | 100%+ YoY | 40%+ YoY |

| Market Position | Category leader | Top 3 in category |

| Customer Count | 4M+ users, thousands of enterprise accounts | Diversified base |

| Breakeven Timeline | Unknown | 2-3 years post-IPO |

Understanding annualized return calculations helps investors evaluate whether waiting for a Figma IPO aligns with their portfolio timeline and return objectives.

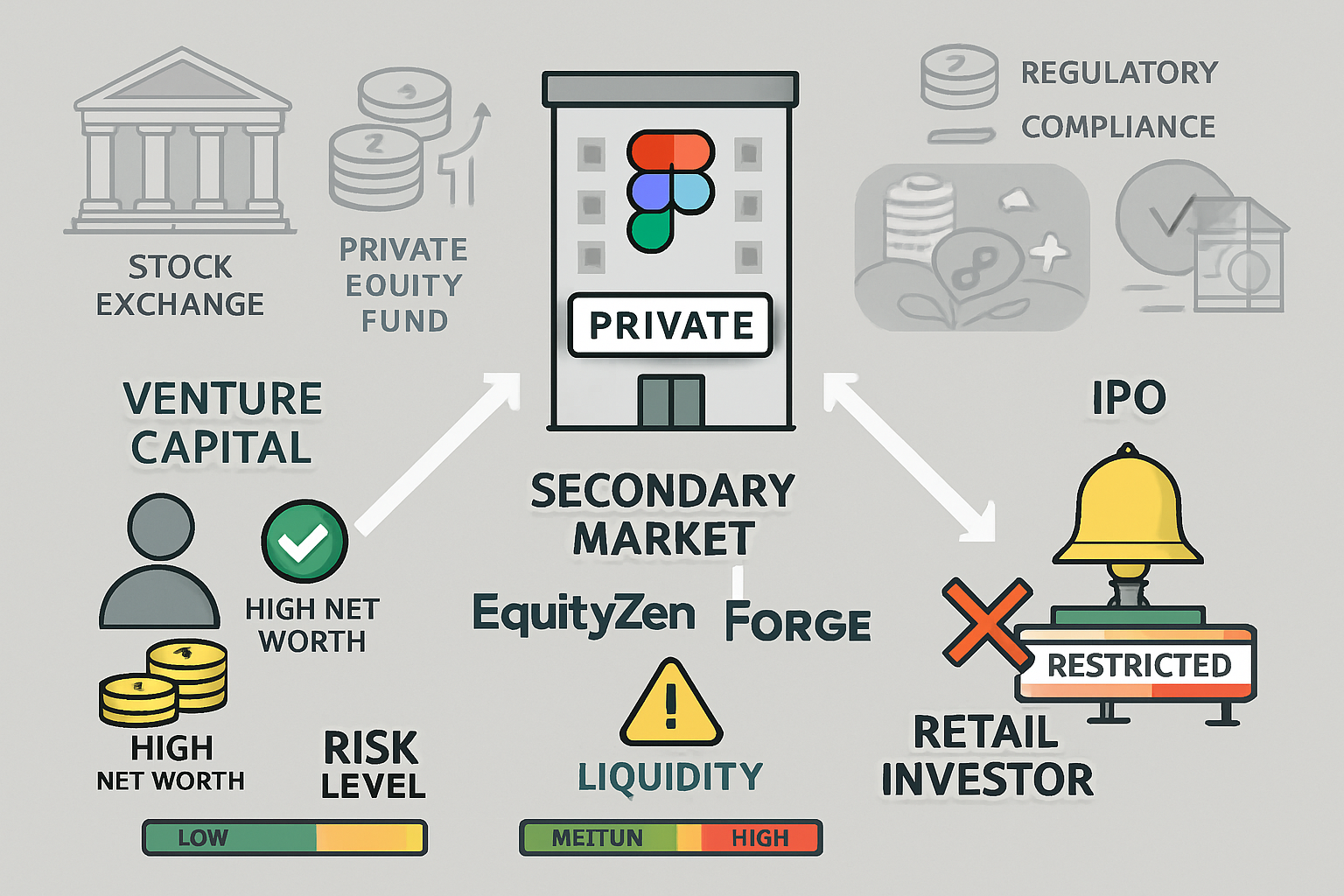

How to Invest in Figma Before an IPO

Private Equity & Venture Capital (Who Qualifies)

Direct investment in Figma requires accredited investor status and access to venture capital funds or direct investment opportunities. This pathway excludes most retail investors due to regulatory restrictions and high minimum investment thresholds.

Accredited investor requirements (SEC definition):

- Individual income exceeding $200,000 annually ($300,000 jointly) for the past two years with a reasonable expectation of continuation, OR

- Net worth exceeding $1 million excluding primary residence, OR

- Professional credentials (Series 7, 65, or 82 licenses) demonstrating investment sophistication[6]

These requirements exist to protect unsophisticated investors from illiquid, high-risk private securities that lack public disclosure and regulatory oversight.

Venture capital fund access:

Most VC funds require $250,000-$1,000,000 minimum commitments with 10-year lock-up periods. These funds invest across multiple private companies, providing diversification but diluting specific Figma exposure. Additionally, top-tier VC funds (like those holding Figma shares) typically restrict access to institutional investors and ultra-high-net-worth individuals.

Direct investment opportunities:

Occasionally, late-stage private companies offer direct investment rounds to strategic investors or wealthy individuals. These opportunities rarely reach retail investors and typically require $500,000+ minimum investments with significant due diligence requirements.

Why this matters: The regulatory framework intentionally limits pre-IPO access to protect investors from risks, including total capital loss, indefinite illiquidity, and information asymmetry. If you don’t meet accredited investor thresholds, legal pathways to Figma ownership before IPO are essentially nonexistent.

For investors building wealth through more accessible channels, understanding active income versus investment returns helps optimize overall financial strategy.

Secondary Markets Explained (Risks Included)

Secondary markets like EquityZen, Forge Global, and SharesPost facilitate private company share transactions between existing shareholders and qualified buyers. These platforms offer limited access to pre-IPO companies but carry substantial risks.

How secondary markets work:

- Existing shareholders (typically employees with vested stock options) seek liquidity before IPO

- Platforms verify buyer accreditation and seller share ownership

- Buyers and sellers negotiate price based on recent funding rounds or comparable valuations

- Company approval is often required (Figma maintains transfer restrictions on most shares)

- The transaction closes with legal documentation transferring ownership

Pricing dynamics: Secondary market prices typically trade at 10-30% discounts to last primary funding round valuations, reflecting illiquidity premiums and uncertainty about exit timing. However, during periods of high demand or near anticipated IPOs, prices can trade at premiums.

Critical risks investors must understand:

Liquidity risk: No guaranteed exit until IPO or acquisition. Shares may remain illiquid for years, with no ability to sell except through limited secondary transactions.

Valuation risk: Private company valuations lack market validation. Last funding round prices may not reflect the true market value, especially if market conditions have deteriorated.

Information asymmetry: Private companies disclose minimal financial information. Investors make decisions with incomplete data about revenue, profitability, customer retention, and competitive positioning.

Regulatory and transfer restrictions: Company bylaws often restrict share transfers or grant the right of first refusal. Your purchase may be blocked or delayed by company action.

Concentration risk: Investing significant capital in a single private company violates basic diversification investing strategies and exposes portfolios to company-specific failure risk.

Minimum investment thresholds: Secondary market transactions typically require $25,000-$100,000 minimum purchases, creating portfolio concentration for all but the wealthiest investors.

Realistic assessment: For investors with $100,000+ available for illiquid, high-risk investments, secondary markets provide theoretical access to Figma shares. However, the combination of accreditation requirements, transfer restrictions, information gaps, and liquidity risk makes this pathway unsuitable for most individual investors.

Better alternative: Wait for IPO when shares become freely tradable with full financial disclosure, or invest in publicly-traded competitors offering similar market exposure without illiquidity penalties.

Understanding risk management principles helps investors evaluate whether pre-IPO opportunities justify their risk-adjusted return potential compared to liquid alternatives.

Figma Stock Alternatives You Can Buy Today

Public Companies Similar to Figma

Investors seeking exposure to collaborative design software and enterprise SaaS markets can access several publicly traded companies offering similar business models and market positioning.

| Company | Ticker | Market Cap (2025) | Why It’s Relevant | Key Metrics |

|---|---|---|---|---|

| Adobe | ADBE | ~$240B | Direct competitor; owns Adobe XD, Creative Cloud suite; attempted Figma acquisition | P/S ratio: ~10x, Revenue growth: 10-12% |

| Autodesk | ADSK | ~$55B | Design software for architecture, engineering, product design; subscription SaaS model | P/S ratio: ~12x, Revenue growth: 12-15% |

| Microsoft | MSFT | ~$3.1T | Enterprise SaaS exposure; owns design tools within Office 365; cloud infrastructure | P/S ratio: ~13x, Revenue growth: 15-17% |

| Canva | N/A | Private (~$26B) | Closest competitor in collaborative design; simplified interface; not yet public | Expected IPO: 2025-2026 |

| Atlassian | TEAM | ~$45B | Collaboration software (Jira, Confluence); similar team-based SaaS model | P/S ratio: ~9x, Revenue growth: 20-25% |

Adobe (ADBE): The most direct Figma competitor, Adobe offers comprehensive design tools through Creative Cloud subscriptions. While Adobe XD competes directly with Figma, the company’s broader portfolio includes Photoshop, Illustrator, and Premiere Pro—industry-standard tools with high switching costs. Adobe trades at reasonable valuations for a mature SaaS company with 10%+ annual growth and strong free cash flow generation.

Investors interested in Adobe specifically can explore detailed analysis at Adobe Stock for comprehensive valuation metrics and investment considerations.

Autodesk (ADSK): Focused on architecture, engineering, and construction (AEC) design software, Autodesk serves adjacent markets to Figma with similar subscription economics. The company successfully transitioned from perpetual licenses to recurring revenue, demonstrating pricing power and customer retention. Autodesk offers exposure to design software trends with less direct Figma competition overlap.

Microsoft (MSFT): While not a pure-play design software company, Microsoft provides broad enterprise SaaS exposure through Office 365, Azure cloud services, and collaboration tools like Teams. The company’s scale and diversification reduce company-specific risk while maintaining exposure to digital transformation trends driving Figma’s growth.

Atlassian (TEAM): Collaboration-focused SaaS company serving software development teams with project management and documentation tools. Atlassian’s business model closely mirrors Figma’s approach: freemium acquisition, team-based pricing, and network effects driving expansion. The company offers similar growth characteristics with public market liquidity.

Portfolio construction approach: Rather than concentrating capital in pre-IPO Figma shares (if accessible), diversified exposure across these public companies provides:

- Immediate liquidity and transparent pricing

- Full financial disclosure and regulatory oversight

- Dividend potential (Microsoft) and growth characteristics (Atlassian)

- Reduced company-specific risk through diversification

For investors building comprehensive portfolios, exploring the best ETFs to buy provides additional diversification across technology and SaaS sectors without individual stock concentration.

Takeaway: Public market alternatives offer superior risk-adjusted returns for most investors compared to illiquid pre-IPO positions. These companies provide immediate access to similar market trends, competitive positioning, and growth drivers that make Figma attractive—without liquidity penalties or information gaps.

Is Figma a Good Investment If It Goes Public?

Business Model Explained Simply

Figma operates a freemium SaaS (Software as a Service) business model with usage-based pricing that scales with team size and feature requirements. Understanding this revenue structure helps investors evaluate potential IPO valuation and long-term sustainability.

Core product offering:

Figma provides browser-based design tools enabling real-time collaboration for product design, prototyping, and design system management. Unlike traditional desktop software (Adobe Creative Suite), Figma requires no installation and allows multiple users to edit simultaneously—similar to Google Docs for design work.

Revenue model breakdown:

- Free tier: Individual designers access basic features at no cost, driving viral adoption and network effects

- Professional tier ($12-15/editor/month): Unlimited projects, version history, and team libraries

- Organization tier ($45/editor/month): Advanced security, centralized administration, design systems, and analytics

- Enterprise tier (custom pricing): Dedicated support, enhanced security controls, and service level agreements

Key business metrics:

- Land-and-expand model: Free users convert to paid as teams grow; organizations upgrade tiers as usage increases

- Net dollar retention: Estimated 130%+, meaning existing customers increase spending by 30%+ annually through seat expansion and tier upgrades[7]

- Gross margins: Estimated 85-90%, typical for SaaS companies with minimal marginal delivery costs

- Customer acquisition cost (CAC): Low due to viral freemium adoption and word-of-mouth growth

Competitive advantages (economic moat):

Network effects: As more designers use Figma, more companies adopt it as their standard tool. Design files shared between companies require Figma to view and edit, creating switching costs and reinforcing market position.

Switching costs: Migrating design systems, component libraries, and team workflows to competing platforms requires significant time and training investment. Once embedded in product development processes, Figma becomes mission-critical infrastructure.

Product velocity: Figma ships new features rapidly, maintaining a competitive distance from Adobe and smaller competitors. The browser-based architecture enables instant updates without user intervention.

Brand and community: Strong designer community, educational resources, and ecosystem of plugins create cultural momentum beyond pure product features.

Revenue projection (speculative):

Based on the estimated 2022 ARR of $400M+ and historical 100%+ growth rates, Figma could potentially reach $800M-$1B in annual revenue by 2025-2026 if growth moderates to 40-50% annually. This scale would support a public company valuation between $8B-$15B, depending on market multiples for high-growth SaaS companies.

For context on how SaaS companies generate returns, exploring the dividend investing guide principles helps investors understand different return profiles across growth versus income-focused stocks.

Key Risks Investors Should Know

Despite strong fundamentals, Figma faces material risks that could impair investment returns if the company goes public. Sophisticated investors evaluate both upside potential and downside scenarios before committing capital.

1. Valuation risk and market timing

The $20 billion Adobe acquisition price established a high valuation benchmark. If Figma IPOs at similar or higher valuations, investors face limited upside unless the company sustains exceptional growth. High revenue multiples (15-20x) leave little margin for execution missteps or market multiple compression.

Math behind valuation risk: At $20B valuation and $500M revenue (2024 estimate), Figma trades at 40x revenue. For investors to achieve 100% returns (2x), the company must either:

- Double revenue to $1B while maintaining 40x multiple = $40B market cap, OR

- Expand revenue multiple to 80x (unlikely for a maturing company), OR

- A combination of revenue growth and multiple expansion

Historical data shows SaaS multiples compress as companies mature and growth rates decline. Investors buying at peak valuations often experience muted returns even when underlying businesses perform well.

2. Competitive pressure from Adobe and Microsoft

Adobe remains formidable with massive R&D budgets, established customer relationships, and an integrated Creative Cloud ecosystem. Microsoft could leverage Teams integration and enterprise sales relationships to compete more aggressively. Both companies can sustain losses in design tools to protect broader strategic positions.

Competitive dynamics: Adobe generates $19B+ annual revenue with $5B+ R&D spending. Figma’s estimated $100M+ R&D budget (assuming 20-25% of revenue) provides innovation capacity, but Adobe can outspend 50:1 if design tools become a strategic priority.

3. Market saturation and growth deceleration

Figma has already captured significant market share among product designers and tech companies. Future growth requires expanding into adjacent markets (marketing design, presentation tools, whiteboarding) where competitive advantages may not transfer. Growth rates will inevitably moderate from 100%+ to more sustainable 30-40% levels, potentially disappointing growth-focused investors.

4. Monetization challenges

Freemium models create large user bases with relatively small paying conversion rates (typically 2-5%). If Figma struggles to convert free users or expand average revenue per account, revenue growth may disappoint despite user growth. Enterprise sales cycles extend 6-12 months, creating revenue recognition delays and quarterly volatility.

5. Product execution and technical debt

Browser-based architecture provides distribution advantages but creates performance constraints for complex design files. Competitors with native applications may offer superior performance for specific use cases. Maintaining product leadership requires continuous innovation while managing technical debt from rapid growth.

6. Regulatory and privacy concerns

Enterprise customers increasingly scrutinize data security, privacy compliance (GDPR, CCPA), and vendor concentration risk. Any security breach or compliance failure could trigger customer churn and reputational damage. Government and regulated industry customers may require on-premise or private cloud deployments, complicating Figma’s SaaS economics.

7. Key person dependency

CEO Dylan Field and CTO Evan Wallace represent significant institutional knowledge and product vision. The departure of either founder could disrupt product strategy and company culture, particularly important for companies where product excellence drives competitive positioning.

Risk-adjusted perspective: These risks don’t necessarily make Figma a poor investment, but they require realistic return expectations. Investors should model scenarios where growth decelerates, competitive pressure intensifies, or market multiples compress—not just optimistic cases where everything executes perfectly.

Understanding capital gains tax implications helps investors structure positions and holding periods to optimize after-tax returns from growth stocks like a potential Figma IPO.

How to Prepare for a Potential Figma IPO

While no official IPO date exists, investors can take specific actions to position themselves for participation if and when Figma goes public.

1. Establish and fund a brokerage account

Open accounts with reputable brokers offering IPO access programs. Fidelity, Charles Schwab, E*TRADE, and TD Ameritrade provide IPO access to qualified customers, though allocation depends on account size and trading activity. Requirements typically include:

- Minimum account balances ($100,000-$250,000)

- Active trading history (25+ trades annually)

- Account tenure (6-12 months before IPO)

2. Monitor SEC filings

Companies must file Form S-1 registration statements with the SEC 3-6 months before IPO. These documents contain detailed financial information, risk factors, and business descriptions. Set up alerts for “Figma” on SEC.gov/EDGAR to receive immediate notification when the preliminary prospectus becomes available.

3. Understand IPO allocation mechanics

Most retail investors receive minimal or zero allocation in hot IPOs. Shares are allocated preferentially to:

- Institutional investors (mutual funds, hedge funds)

- High-net-worth individual clients of underwriting banks

- Employees and insiders (with lock-up restrictions)

Retail investors typically access shares only after public trading begins, often at prices above the IPO price if demand is strong.

4. Evaluate first-day trading dynamics

IPO stocks frequently experience 20-50% first-day price swings driven by supply-demand imbalances rather than fundamental value. Patient investors often find better entry points 3-6 months post-IPO after initial volatility subsides and lock-up periods expire (releasing insider shares).

Statistical reality: Research shows that buying IPOs at first-day close prices produces lower returns than waiting 6-12 months for post-IPO volatility to normalize.[8] The math favors patience over FOMO-driven purchases.

5. Develop a valuation framework

Before the IPO announcement, establish your own valuation model based on:

- Comparable public company multiples (Adobe, Autodesk, Atlassian)

- Revenue growth rates and margin assumptions

- Market share and competitive positioning

- Total addressable market (TAM) analysis

This framework prevents emotional decision-making when IPO pricing is announced. If Figma IPOs at valuations exceeding your model by 50%+, disciplined investors wait for better entry points rather than chasing momentum.

For investors building systematic approaches to stock evaluation, understanding the best stocks to invest in 2025 provides frameworks for comparing opportunities across sectors.

📊 Figma IPO Investment Calculator

Calculate potential returns based on different IPO valuation scenarios

Conclusion

Figma Stock represents one of the most compelling private technology companies in 2025, but access remains limited to accredited investors through illiquid secondary markets. The failed Adobe acquisition, blocked by antitrust regulators, returned Figma to independent operation with a strengthened financial position and continued market dominance in collaborative design.

For retail investors, the math is clear: waiting for an IPO provides superior risk-adjusted opportunities compared to pre-IPO investments. Public markets offer transparent pricing, full financial disclosure, immediate liquidity, and regulatory protections unavailable in private transactions. The premium paid for early access rarely justifies the illiquidity risk and information asymmetry.

Actionable next steps:

- Monitor SEC filings for Form S-1 registration indicating IPO preparation

- Establish brokerage accounts with IPO access programs if you meet qualification thresholds

- Invest in public alternatives (Adobe, Autodesk, Atlassian) for immediate design software exposure

- Develop a valuation framework before the IPO announcement to make rational investment decisions

- Maintain portfolio diversification by limiting any single stock position to 5% or less of total assets

The opportunity to invest in category-defining companies like Figma will arrive when the company chooses to go public. Until then, patient investors build wealth through accessible, liquid alternatives while avoiding the illiquidity penalties and concentration risks of pre-IPO investing.

Understanding the math behind money means recognizing that exceptional returns require exceptional patience—not exceptional access. The companies available today through public markets offer sufficient growth potential for long-term wealth building without the risks inherent in private market speculation.

For investors committed to evidence-based investing and systematic wealth building, the principles remain constant: diversify broadly, invest in quality businesses at reasonable valuations, maintain a long-term perspective, and avoid concentration risk. These fundamentals generate superior risk-adjusted returns regardless of whether you access companies before or after they go public.

References

[1] Crunchbase. “Figma Funding Rounds and Investors.” Accessed 2025. https://www.crunchbase.com/organization/figma

[2] U.S. Securities and Exchange Commission. “Going Public.” Investor.gov. https://www.investor.gov/introduction-investing/investing-basics/glossary/going-public

[3] Adobe. “Adobe to Acquire Figma.” Press Release, September 2022. https://www.adobe.com/news-room/

[4] European Commission. “Mergers: Commission prohibits acquisition of Figma by Adobe.” December 2023. https://ec.europa.eu/commission/presscorner/

[5] The Information. “Figma Revenue and Growth Metrics.” 2023. https://www.theinformation.com/

[6] U.S. Securities and Exchange Commission. “Accredited Investor Definition.” https://www.sec.gov/education/capitalraising/building-blocks/accredited-investor

[7] Bessemer Venture Partners. “State of the Cloud 2024.” https://www.bvp.com/atlas/state-of-the-cloud-2024

[8] Ritter, Jay R. “Initial Public Offerings: Updated Statistics.” University of Florida, 2024. https://site.warrington.ufl.edu/ritter/ipo-data/

Educational Disclaimer

This article provides educational information about Figma stock, IPO mechanics, and investment considerations. It does not constitute financial advice, investment recommendations, or solicitation to buy or sell securities.

Key disclaimers:

- No guarantee of accuracy: While information is researched from credible sources, Figma’s private status limits publicly available data. Revenue estimates, valuation projections, and IPO timing represent informed speculation, not confirmed facts.

- Investment risk: All investments carry the risk of loss, including total capital loss. Pre-IPO investments carry additional risks, including illiquidity, limited disclosure, and concentration risk. IPO stocks frequently experience high volatility.

- No professional relationship: This content does not create advisor-client relationships. Readers should consult qualified financial advisors, tax professionals, and legal counsel before making investment decisions.

- Forward-looking statements: Projections about IPO timing, valuations, and returns represent hypothetical scenarios based on assumptions that may not materialize. Actual results may differ materially.

- Regulatory compliance: Ensure any investment activity complies with securities regulations in your jurisdiction. Accredited investor requirements and transfer restrictions apply to private securities.

Investment decisions should be based on:

- Personal financial situation and risk tolerance

- Comprehensive due diligence and professional advice

- Diversified portfolio construction principles

- Long-term financial goals and time horizons

The Rich Guy Math provides financial education to improve financial literacy and decision-making skills. We do not manage money, sell securities, or provide personalized investment advice.

Past performance does not guarantee future results. All securities involve risk.

About the Author

Max Fonji is the founder of The Rich Guy Math, a financial education platform dedicated to teaching the mathematical principles behind wealth building, investing, and risk management. With a background in financial analysis and data-driven decision-making, Max translates complex financial concepts into clear, actionable insights for investors at all levels.

Max’s approach combines rigorous quantitative analysis with accessible explanations, helping readers understand not just what to do with money, but why specific strategies work and how to evaluate them independently. His work emphasizes evidence-based investing, compound growth principles, and the critical importance of financial literacy in building long-term wealth.

Through The Rich Guy Math, Max has helped thousands of readers understand investment fundamentals, valuation principles, and risk management strategies that form the foundation of successful wealth building.

Connect with Max:

- Website: The Rich Guy Math

- Topics covered: Investment analysis, financial ratios, compound interest, portfolio construction, risk management, and evidence-based wealth strategies

Frequently Asked Questions About Figma Stock

Why can’t retail investors buy Figma stock yet?

Figma remains a private company, meaning its shares are not registered with the SEC for public trading. Only accredited investors with access to venture capital funds or approved secondary markets can purchase shares, subject to company approval and transfer restrictions.

SEC regulations require companies to register securities before selling them to the public, ensuring standardized disclosures and investor protections. Until Figma completes an IPO and files the required registration documents, retail investors cannot legally buy Figma stock through standard brokerage accounts.

What valuation would Figma likely IPO at?

Figma’s IPO valuation will depend on revenue growth, profitability outlook, and market conditions at the time of listing. The failed Adobe acquisition set a $20 billion reference point in 2022, but IPO valuation could reasonably range from $15 billion to $30+ billion.

- Revenue scale: $800M–$1B ARR at 15–25× SaaS multiples implies $12B–$25B

- Growth rate: 50%+ growth supports premium multiples; slower growth compresses valuation

- Market conditions: Strong IPO markets increase valuations

- Profitability path: Clear margins timeline adds valuation premium

A realistic base case suggests an $18–$25 billion IPO valuation if Figma lists in 2025–2026 under favorable conditions.

Did the Adobe breakup fee affect Figma financially?

Yes—positively. Adobe paid Figma a $1 billion termination fee after regulators blocked the acquisition. This significantly strengthened Figma’s balance sheet.

- Extended operational runway without fundraising pressure

- Capital for product development or acquisitions

- Reduced urgency to pursue an IPO

- Stronger negotiating position with future acquirers

The fee likely covers 2–3 years of operating expenses, giving management flexibility to time an IPO strategically.

Is Figma profitable?

Figma does not publicly disclose profitability, but industry estimates suggest the company operates at a loss while prioritizing growth—common among high-growth SaaS firms.

- Estimated revenue: $400M–$500M (2024)

- Gross margin: 85–90%

- Operating margin: –20% to –40%

- Profitability timeline: Likely within 2–3 years post-IPO

Most venture-backed software companies delay profitability to maximize market share before public listing.

Can Figma employees sell shares before an IPO?

Employees have limited ability to sell shares through approved secondary transactions, subject to company restrictions.

- Four-year vesting schedules with one-year cliffs

- Board approval required for share transfers

- Right of first refusal for the company or investors

- Post-IPO lock-up periods of 90–180 days

Some employees gain partial liquidity through company-organized tender offers, but most equity remains locked until IPO or acquisition.

What’s the safest way to invest in companies like Figma?

For most investors, the safest approach is waiting for an IPO and buying shares in public markets with full disclosure and liquidity.

- Invest in public competitors like Adobe or Autodesk

- Use diversified technology or SaaS ETFs

- Wait 6–12 months post-IPO to reduce volatility risk

- Limit exposure to 2–5% of portfolio per stock

- Use dollar-cost averaging instead of lump-sum buying

Diversification and risk management matter more than capturing maximum upside in pre-IPO speculation.