Imagine having a financial safety net worth tens of thousands of dollars sitting right in your living room. For millions of homeowners, that safety net is real; it’s called home equity. And with a Home Equity Line of Credit (HELOC), you can tap into that wealth whenever you need it. But before you sign on the dotted line, understanding exactly how a HELOC works can mean the difference between smart financial leverage and a costly mistake.

Borrowing against home equity should only be done after understanding the full credit system basics.

A HELOC is a revolving line of credit secured by the equity in your home, allowing you to borrow money as needed up to a predetermined limit, much like a credit card, but typically with lower interest rates. Homeowners use HELOCs for everything from home renovations and debt consolidation to emergency expenses and investment opportunities. In 2025, with home values remaining elevated in many markets and interest rates fluctuating, HELOCs have become an increasingly popular tool for accessing cash without selling your home.

Key Takeaways

- A HELOC is a revolving credit line secured by your home equity, allowing you to borrow and repay funds repeatedly during the draw period.

- Most lenders allow you to borrow up to 80-85% of your home’s value minus what you still owe on your mortgage.

- HELOCs typically have two phases: a 5-10 year draw period (when you can borrow) and a 10-20 year repayment period (when you must pay back)

- Interest rates are usually variable, meaning your monthly payments can change based on market conditions.

- Your home serves as collateral, so failing to repay could result in foreclosure.

What Is a HELOC? The Complete Definition

In simple terms, a HELOC means you’re borrowing against the value of your home, using your equity as collateral.

A Home Equity Line of Credit is a secured loan that uses your home as collateral. Unlike a traditional loan, where you receive a lump sum upfront, a HELOC works like a credit card—you have access to a credit limit and can draw from it as needed during what’s called the “draw period.” You only pay interest on the amount you actually borrow, not on the entire credit line.

Here’s the basic formula lenders use:

Maximum HELOC Amount = (Home Value × Loan-to-Value Ratio) – Existing Mortgage Balance

For example, if your home is worth $400,000, the lender allows an 85% loan-to-value ratio, and you owe $200,000 on your mortgage:

($400,000 × 0.85) – $200,000 = $140,000 potential HELOC

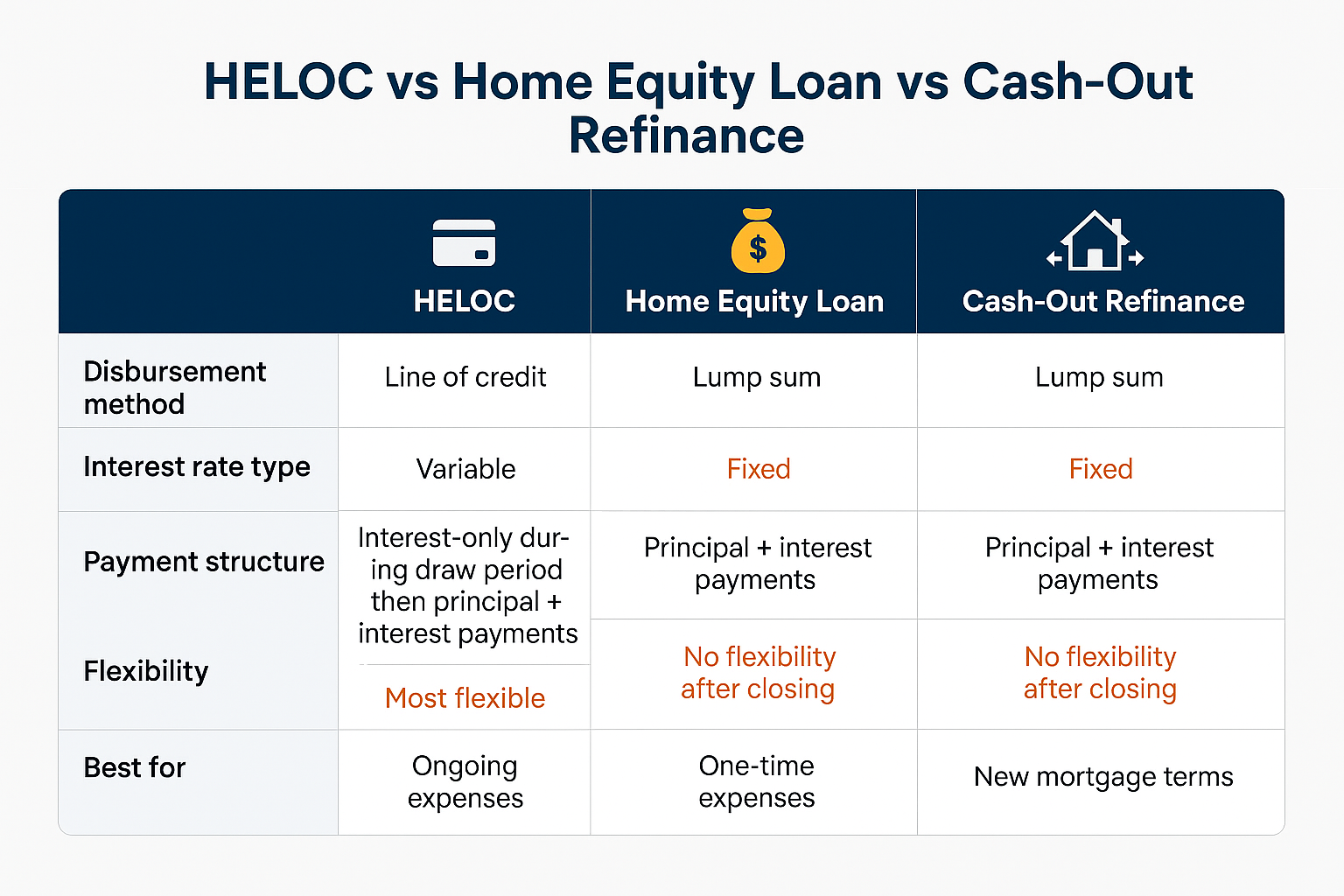

How HELOCs Differ from Other Home Loans

| Feature | HELOC | Home Equity Loan | Cash-Out Refinance |

|---|---|---|---|

| Disbursement | Draw as needed | Lump sum | Lump sum |

| Interest Rate | Usually variable | Usually fixed | Usually fixed |

| Repayment | Lowering the mortgage rate + getting cash | Fixed monthly payments | Fixed monthly payments |

| Flexibility | High – borrow, repay, reborrow | Low – one-time funding | Low – one-time funding |

| Best For | Ongoing expenses, uncertain costs | One-time large expense | Lowering mortgage rate + getting cash |

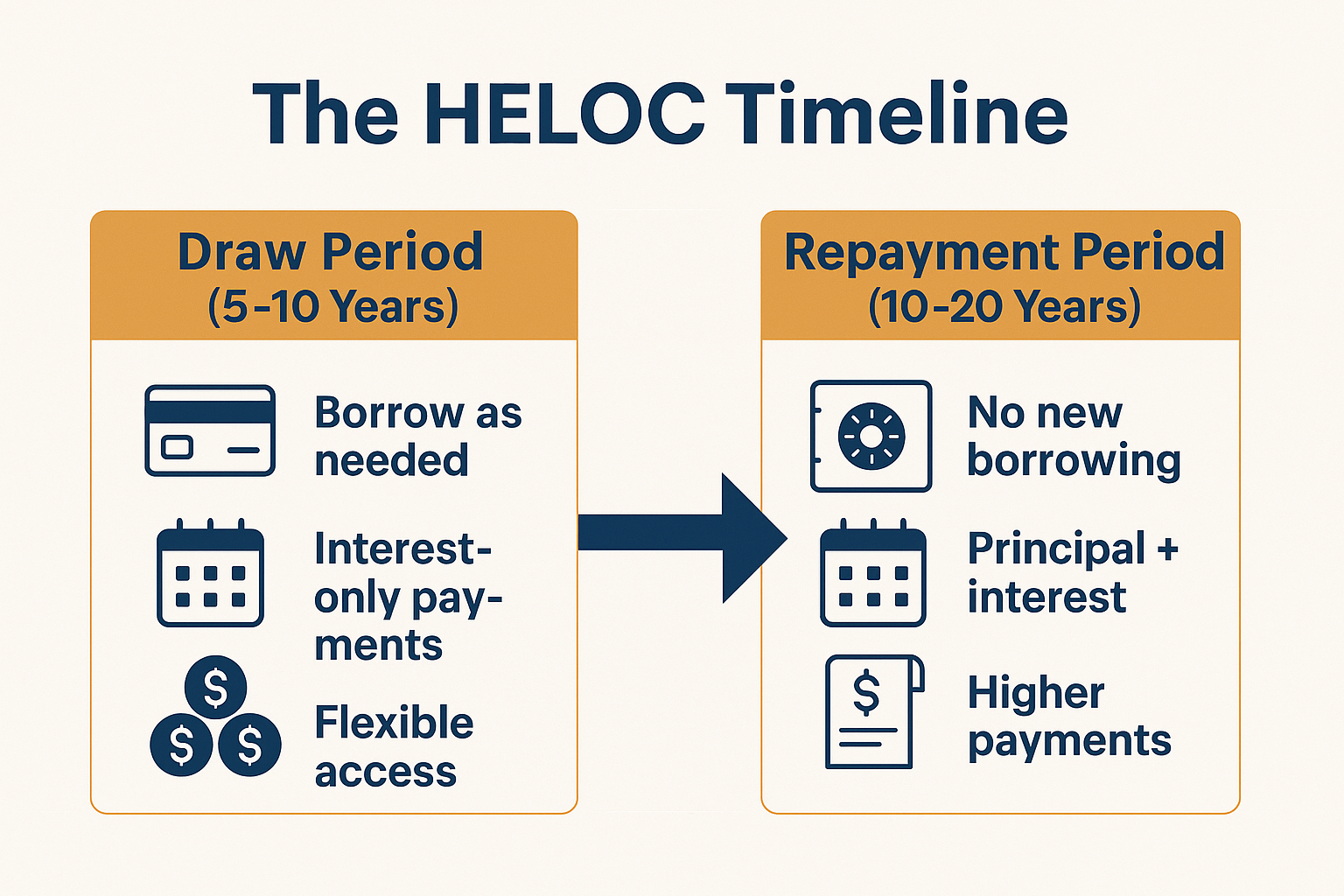

The Two Phases of a HELOC Lifecycle

Understanding the HELOC timeline is crucial because your obligations change dramatically between phases.

Phase 1: The Draw Period (5-10 Years)

During the draw period, you can:

- Withdraw funds up to your credit limit

- Make minimum payments (often interest-only)

- Repay and reborrow repeatedly

- Access funds via checks, credit cards, or online transfers

Example: Sarah has a $100,000 HELOC. She withdraws $30,000 for a kitchen renovation. Her monthly payment might be only $150 (interest-only at 6% APR). After paying back $10,000, she can borrow that $10,000 again if needed.

Phase 2: The Repayment Period (10-20 Years)

Once the draw period ends:

- You can no longer withdraw funds

- You must repay both principal and interest

- Monthly payments typically increase significantly

- The line of credit closes

The payment shock can be substantial. If Sarah still owes $30,000 when repayment begins, her monthly payment could jump from $150 to $350+ as she pays down the principal over 15 years.

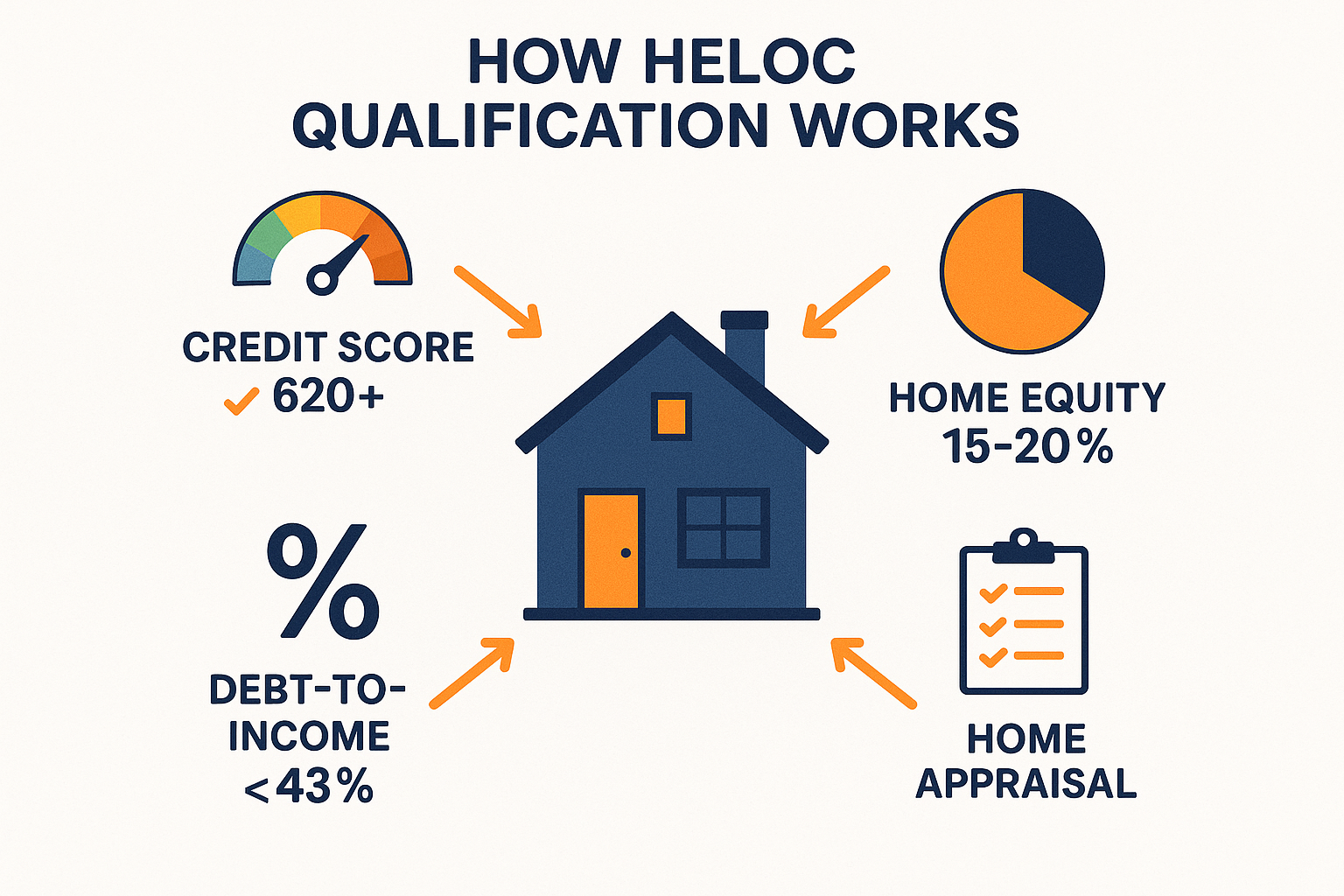

How to Qualify for a HELOC in 2025

Lenders evaluate several factors before approving your HELOC application:

Credit Score Requirements

- Minimum: 620 (though some lenders require 640+)

- Competitive rates: 700+

- Best rates: 740+

Your credit score directly impacts your interest rate. A borrower with a 780 score might get 6.5% APR, while someone with a 650 score could face 9.5% or higher.

Debt-to-Income Ratio (DTI)

Investors use DTI to measure your ability to handle monthly debt payments.

Lenders typically require:

- Maximum DTI: 43-50%

- Preferred DTI: Below 36%

DTI Formula: (Total Monthly Debt Payments ÷ Gross Monthly Income) × 100

If you earn $8,000/month and have $2,400 in debt payments (including the potential HELOC), your DTI is 30%—well within the acceptable range.

Home Equity Requirements

Most lenders require you to maintain at least 15-20% equity in your home after the HELOC is established. This protects both you and the lender from being underwater if property values decline.

Additional Documentation

Be prepared to provide:

- Recent pay stubs and W-2s

- Tax returns (1-2 years)

- Home appraisal or valuation

- Existing mortgage statements

- Proof of homeowners’ insurance

HELOC Interest Rates: What to Expect

Unlike fixed-rate loans, most HELOCs have variable interest rates tied to the Prime Rate, which fluctuates based on Federal Reserve decisions.

How Variable Rates Work

HELOC Rate = Prime Rate + Lender Margin

As of early 2025, the Prime Rate hovers around 8.5%. If your lender adds a 1% margin, your HELOC rate would be 9.5%. When the Federal Reserve raises or lowers rates, your HELOC rate—and monthly payment—adjusts accordingly.

Rate Caps and Protections

Federal regulations require HELOCs to include:

- Lifetime cap: Maximum rate over the loan’s life

- Periodic cap: Limit on rate increases per adjustment period

A typical HELOC might have an 18% lifetime cap and a 2% annual adjustment cap, protecting you from extreme rate spikes.

Fixed-Rate Options

Some lenders allow you to “lock in” portions of your balance at a fixed rate, providing payment predictability for larger draws. This hybrid approach offers flexibility with some stability.

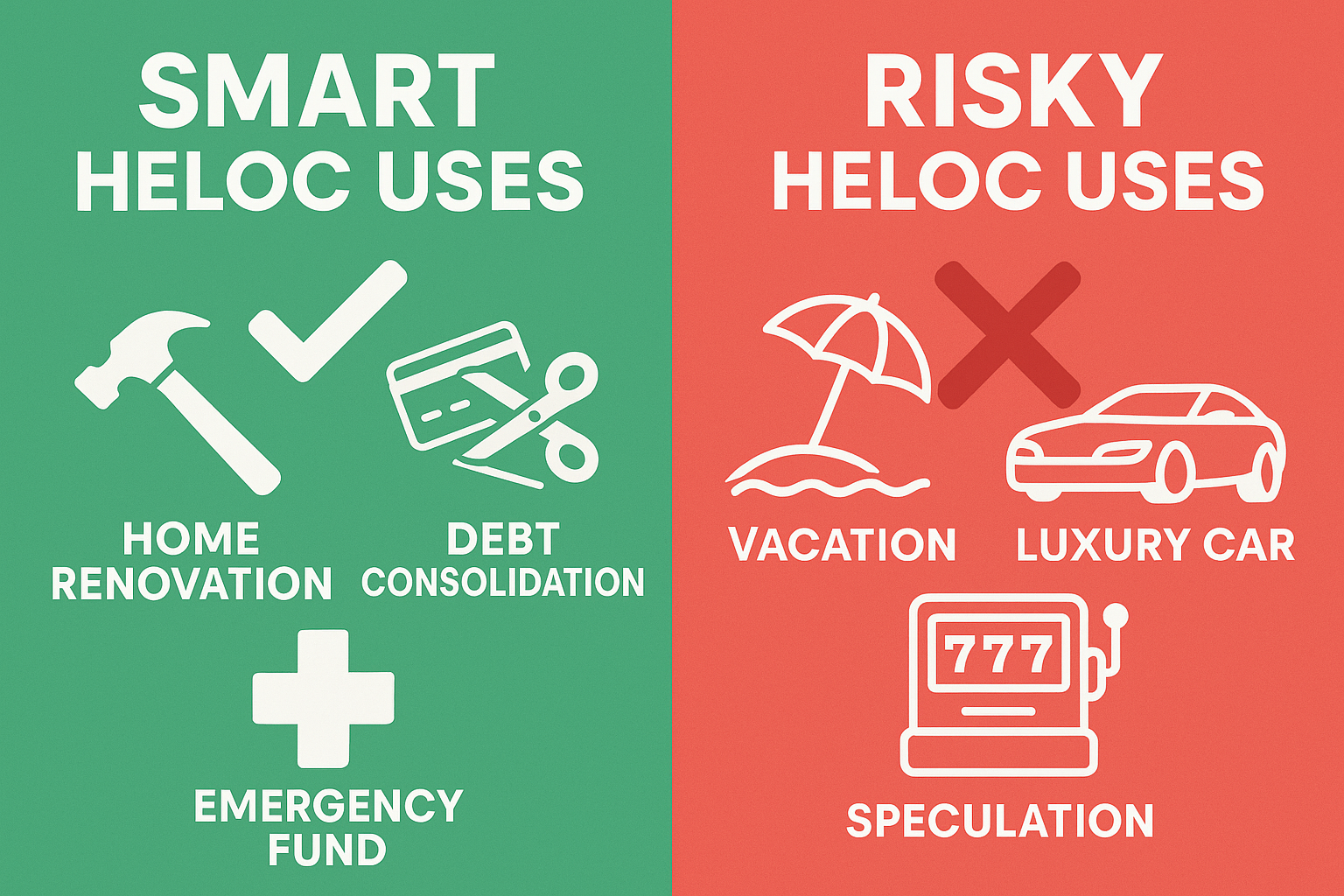

Common Uses for HELOCs (Smart and Not-So-Smart)

Smart HELOC Uses

1. Home Improvements That Add Value

Renovating your kitchen, adding a bathroom, or finishing a basement can increase your home’s value by more than the renovation cost. Since HELOC interest may be tax-deductible when used for home improvements (consult a tax professional), this is one of the most strategic uses.

2. Debt Consolidation

If you’re carrying high-interest credit card debt at 20-25% APR, consolidating with a HELOC at 7-9% can save thousands in interest. However, this only works if you address the spending habits that created the debt.

3. Education Expenses

While student loans exist, a HELOC might offer lower rates for graduate programs or continuing education, especially if federal loan options are exhausted.

4. Investment Opportunities

Some sophisticated investors use HELOCs to invest in dividend-paying stocks or real estate. This strategy, called “leverage,” amplifies both gains and losses. Understanding what moves the stock market is crucial before using borrowed money for investments.

Risky HELOC Uses

1. Vacations and Luxury Purchases

Borrowing against your home to fund a European vacation or buy a boat means you’re still paying for that experience years later, with interest.

2. Daily Living Expenses

If you need a HELOC to cover groceries and utilities, you have a budget problem, not a borrowing opportunity.

3. Speculative Investments

Using a HELOC to day-trade or invest in cryptocurrency is extremely risky. Many people lose money in the stock market through speculation, and doing so with borrowed money secured by their home magnifies the danger.

4. Funding a Business Without a Solid Plan

While entrepreneurship is admirable, risking your home on an untested business idea can lead to financial disaster.

The Pros and Cons of HELOCs

Advantages of HELOCs

Flexibility and Convenience

- Borrow only what you need, when you need it

- Repay and reborrow during the draw period

- Multiple access methods (checks, cards, transfers)

Lower Interest Rates Than Unsecured Debt

- Typically, 4-6 percentage points lower than credit cards

- Secured by collateral, reducing lender risk

Potential Tax Benefits

- Interest may be tax-deductible if used for home improvements

- Consult IRS Publication 936 or a tax advisor for specifics

Interest-Only Payment Option

- During the draw period, you can make minimum payments

- Preserves cash flow for other priorities

No Prepayment Penalties

- Pay off your balance early without fees (most lenders)

- Reduces total interest paid

Disadvantages and Risks

Your Home Is at Risk

- Failing to repay could result in foreclosure

- Unlike credit card debt, this is secured by your primary residence

Variable Interest Rates

- Monthly payments can increase unexpectedly

- Makes budgeting more challenging

- Could become unaffordable if rates spike

Payment Shock at Repayment Phase

- Transition from interest-only to principal + interest

- The monthly payment can double or triple

Fees and Closing Costs

- Application fees: $0-$500

- Appraisal: $300-$600

- Annual fees: $0-$100

- Early closure fees: $250-$500 (if you close within 2-3 years)

Temptation to Overborrow

- Easy access can lead to unnecessary spending

- Treats home equity like a piggy bank

Market Risk

- If home values decline, you could owe more than your home is worth

- Lenders can freeze or reduce your credit line in declining markets

HELOC vs Home Equity Loan: Which Is Right for You?

The choice between a HELOC and a home equity loan depends on your specific situation.

| Feature / Situation | Choose a HELOC If… | Choose a Home Equity Loan If… |

|---|---|---|

| Type of Expense | You have ongoing or uncertain expenses (e.g., multi-phase renovation) | You need a specific lump sum for a one-time expense |

| Payment Structure | You want flexible payments and can borrow as needed | You prefer predictable, fixed monthly payments |

| Interest Rate | You’re comfortable with variable interest rates | You want a fixed interest rate for stability |

| Access to Funds | You need access to funds over several years | You receive the entire loan amount upfront |

| Best For | Long-term projects or flexible financing needs | Debt consolidation or one-time major purchases |

| Lender’s View | May favor borrowers with lower debt-to-income ratios | Works well for borrowers who want stability |

See our full guide on HELOC vs Home Equity Loan

A higher debt-to-income ratio usually indicates greater financial risk to lenders.

Step-by-Step: How to Get a HELOC

Step 1: Determine Your Available Equity

Calculate: (Home Value × 0.85) – Mortgage Balance = Available Equity

Get a realistic home value estimate from:

- Recent comparable sales in your neighborhood

- Online estimators (Zillow, Redfin—use as starting points)

- Professional appraisal (most accurate)

Step 2: Check Your Credit and DTI

- Pull your credit reports from AnnualCreditReport.com

- Calculate your debt-to-income ratio

- Address any credit issues before applying

Step 3: Shop Multiple Lenders

Compare offers from:

- Your current mortgage lender

- Local banks and credit unions

- Online lenders

- National banks

Compare:

- Interest rates and margins

- Fees and closing costs

- Draw and repayment period lengths

- Minimum draw requirements

- Rate lock options

Step 4: Submit Your Application

Provide documentation:

- Proof of income

- Tax returns

- Credit authorization

- Property information

- Existing mortgage details

Step 5: Complete the Appraisal

The lender will order a home appraisal to verify your property’s value. This typically costs $300-$600 and takes 1-2 weeks.

Step 6: Review and Sign

Carefully review:

- Credit limit

- Interest rate and how it adjusts

- Draw and repayment periods

- Fees and penalties

- Prepayment terms

You have a 3-day right of rescission after signing—you can cancel without penalty during this period.

Step 7: Access Your Funds

Once finalized, you’ll receive:

- Checks linked to your HELOC

- A credit card or debit card

- Online transfer capabilities

Managing Your HELOC Responsibly

Create a Borrowing Strategy

Before drawing funds, ask yourself:

- Is this expense necessary?

- Will this increase my home’s value or my earning potential?

- Can I afford the payments if interest rates rise 2-3%?

- Do I have a repayment plan?

Track Your Balance and Payments

- Monitor your outstanding balance monthly

- Understand how much available credit remains

- Track interest rate changes

- Set up automatic payments to avoid late fees

Pay More Than the Minimum

Even during the draw period, paying principal is reduced:

- Total interest paid over the loan’s life

- Payment shock when repayment begins

- Risk of owing more than your home is worth

Example: On a $50,000 balance at 7% APR, paying an extra $200/month during a 10-year draw period saves approximately $18,000 in interest and reduces the balance by $24,000.

Prepare for the Repayment Period

5 years before your draw period ends:

- Calculate your projected payment using online calculators

- Increase monthly payments to reduce principal

- Consider refinancing if rates are favorable

- Build an emergency fund to handle payment increases

Understand Rate Adjustment Triggers

Know when and how your rate adjusts:

- What index is used? (Prime Rate is the most common)

- How often does it adjust? (Monthly, quarterly, annually)

- What are the caps? (Periodic and lifetime)

HELOC Risks and How to Protect Yourself

Risk 1: Foreclosure

The reality: Your home secures the HELOC. Missing payments can lead to foreclosure, just like with your primary mortgage.

Protection strategies:

- Only borrow what you can comfortably repay

- Maintain 3-6 months of payments in emergency savings

- Consider unemployment or disability insurance

- Communicate with your lender immediately if you face hardship

Risk 2: Declining Home Values

The reality: If your home’s value drops significantly, lenders can freeze or reduce your credit line.

Protection strategies:

- Don’t borrow your maximum available equity

- Maintain at least 20% equity cushion

- Focus HELOC spending on value-adding improvements

- Monitor local real estate market conditions

Risk 3: Rising Interest Rates

The reality: Variable rates can increase your monthly payment substantially.

Protection strategies:

- Stress-test your budget at 2-3% higher rates

- Lock in portions of your balance when possible

- Pay down principal aggressively during low-rate periods

- Consider converting to a fixed-rate loan if rates spike

Risk 4: Overborrowing

The reality: Easy access to funds can lead to unnecessary spending and debt accumulation.

Protection strategies:

- Create a specific purpose for HELOC funds

- Don’t use it for consumables or depreciating assets

- Treat it like a financial tool, not extra income

- Review spending quarterly

Real-World HELOC Example

Meet the Johnsons:

- Home value: $500,000

- Existing mortgage: $300,000

- Credit score: 740

- Combined income: $150,000

- DTI before HELOC: 28%

Their HELOC approval:

Maximum HELOC = ($500,000 × 0.85) – $300,000 = $125,000

The Johnsons are approved for a $125,000 HELOC with:

- 7.5% variable APR (Prime + 1%)

- 10-year draw period

- 15-year repayment period

- $500 closing costs

- No annual fee

Their plan: Borrow $60,000 for a kitchen and bathroom renovation expected to add $80,000 to their home’s value.

During the draw period (interest-only payments):

- Monthly payment on $60,000: $375

- Total paid over 10 years (interest only): $45,000

During the repayment period:

- Monthly payment (principal + interest): $555

- Total paid over 15 years: $99,900

- Total interest paid (entire loan): $39,900

If they had instead paid $600/month from the start, they would:

- Pay off the balance in 11 years

- Save approximately $17,000 in interest

- Avoid payment shock

HELOC Tax Implications

Potential Tax Deductibility

Under the Tax Cuts and Jobs Act, HELOC interest is tax-deductible only if the funds are used to “buy, build, or substantially improve” the home securing the loan.

Deductible uses:

- Kitchen or bathroom renovation

- Adding a room or a second story

- New roof, HVAC, or major systems

- Accessibility improvements

Non-deductible uses:

- Debt consolidation

- Vacation expenses

- Car purchases

- College tuition

- Investment purchases

Deduction limits: Interest on up to $750,000 of combined mortgage and HELOC debt ($375,000 if married filing separately).

Tax Reporting

If you claim the deduction:

- You’ll receive Form 1098 from your lender

- Report interest on Schedule A (itemized deductions)

- Keep detailed records of how funds were used

- Consult a tax professional for complex situations

Source: IRS Publication 936 – Home Mortgage Interest Deduction

Alternatives to HELOCs

Before committing to a HELOC, consider these alternatives:

Cash-Out Refinance

Best for: Homeowners who can secure a lower rate than their current mortgage while extracting equity.

Pros: Single fixed payment, potentially lower rate

Cons: Refinancing costs, resets the mortgage term, less flexible

Personal Loan

Best for: Smaller amounts ($5,000-$50,000) with predictable repayment.

Pros: No collateral risk, fixed rate and term, faster approval

Cons: Higher interest rates (8-15%+), less borrowing capacity

401(k) Loan

Best for: Short-term needs with certain repayment ability.

Pros: No credit check, low interest (often prime + 1%)

Cons: Reduces retirement savings, must repay if you leave your job, and loses investment growth

Credit Cards

Best for: Very short-term needs you can repay within months.

Pros: No collateral, potential rewards, 0% intro APR offers

Cons: High interest rates (18-25%), low limits, debt cycle risk

Building Savings

Best for: Non-urgent expenses where you have time to save.

Pros: No debt, no interest, builds financial discipline

Cons: Delayed gratification, requires time

For those looking to build wealth without taking on debt, exploring smart ways to make passive income or understanding high dividend stocks might be better long-term strategies than borrowing against your home.

Common HELOC Mistakes to Avoid

1: Only Making Minimum Payments

Why it’s problematic: You’re not reducing principal, maximizing interest costs, and setting yourself up for payment shock.

Solution: Pay principal from day one, even if it’s just an extra $100-200/month.

2: Using HELOC Funds for Depreciating Assets

Why it’s problematic: You’re paying interest on something losing value (cars, boats, electronics).

Solution: Only use HELOCs for appreciating or value-maintaining purposes.

3: Ignoring the Repayment Period

Why it’s problematic: Many borrowers are shocked when their payment doubles or triples.

Solution: Calculate your repayment-period payment before borrowing and ensure it fits your budget.

4: Not Reading the Fine Print

Why it’s problematic: Hidden fees, rate adjustment terms, and prepayment penalties can cost thousands.

Solution: Review all documentation carefully and ask questions about anything unclear.

5: Borrowing Maximum Available Equity

Why it’s problematic: Leaves no equity cushion if home values decline or you need to sell.

Solution: Borrow only what you need and maintain at least 20% equity.

6: Treating It Like Free Money

Why it’s problematic: Creates a dangerous spending mentality and debt accumulation.

Solution: Create a specific budget and purpose for every dollar borrowed.

HELOC During Economic Uncertainty

The economic environment significantly impacts HELOC attractiveness and risk.

In Rising Rate Environments

When the Federal Reserve raises rates:

- HELOC rates increase, raising monthly payments

- Existing HELOC holders see payment increases

- New applicants face higher starting rates

- Fixed-rate alternatives become more attractive

Strategy: Consider locking in fixed-rate portions or converting to a home equity loan if you anticipate further rate increases.

In Declining Rate Environments

When rates fall:

- HELOC payments decrease

- New applicants get better rates

- Variable-rate products become more attractive

- Good time to tap equity if needed

Strategy: Take advantage of lower rates but remain prepared for eventual increases.

During Housing Market Volatility

When home values are uncertain:

- Lenders may tighten approval standards

- Existing credit lines can be frozen or reduced

- Appraisals become more conservative

- Equity calculations change

Strategy: Maintain conservative borrowing levels and don’t rely on maximum credit availability.

Understanding the cycle of market emotions can help you make rational HELOC decisions during economic uncertainty rather than emotional ones.

How Lenders Evaluate HELOC Applications

Understanding the lender’s perspective helps you prepare a stronger application.

Combined Loan-to-Value (CLTV) Ratio

Lenders use CLTV to measure total debt against home value.

CLTV Formula: [(First Mortgage + HELOC) ÷ Home Value] × 100

Most lenders cap CLTV at 80-85%, though some go to 90% for exceptional borrowers.

Example:

- Home value: $400,000

- First mortgage: $250,000

- Desired HELOC: $70,000

- CLTV: [($250,000 + $70,000) ÷ $400,000] × 100 = 80%

Debt Service Coverage

Lenders want confidence that you can handle payments even if rates rise.

They typically:

- Calculate payments at current rate + 2-3%

- Verify DTI remains under 43-50% at higher rates

- Review payment history on existing debts

- Assess employment stability

Property Type and Condition

Easier approval for:

- Single-family primary residences

- Well-maintained properties

- Desirable neighborhoods

- Properties with clear titles

More difficult for:

- Investment properties

- Condos or co-ops

- Properties needing significant repairs

- Homes in declining markets

HELOC Red Flags and Warning Signs

Lender Red Flags

Be cautious of lenders who:

- Promise approval without documentation

- Pressure you to borrow more than requested

- Are vague about fees and rate adjustments

- Don’t clearly explain the draw and repayment periods

- Offer rates significantly below the market average

Personal Red Flags

Reconsider a HELOC if you:

- Don’t have a specific purpose for the funds

- They are already struggling with current debt payments

- Have unstable income or employment

- Don’t understand how variable rates work

- Are you using it to maintain a lifestyle you can’t afford

Market Red Flags

Be extra cautious when:

- Local home values are declining

- Your area has high foreclosure rates

- Interest rates are at historic lows (likely to rise)

- Economic recession indicators are present

- Your industry faces significant disruption

💰 HELOC Payment Calculator

Calculate your monthly payments during draw and repayment periods

Making Smart HELOC Decisions: Key Principles

Principle 1: Borrow with Purpose

Every dollar borrowed should serve a specific, value-creating purpose:

- Value-adding home improvements that increase property worth

- Debt consolidation that genuinely reduces interest costs and improves cash flow

- Emergency expenses that are truly urgent and necessary

- Education or skills that increase earning potential

Avoid borrowing for:

- Lifestyle inflation

- Consumables and depreciating assets

- Speculative investments

- Maintaining appearances

Principle 2: Understand the True Cost

The advertised rate isn’t the full story. Calculate:

- Total interest over the loan’s life

- All fees (application, appraisal, annual, closing)

- Payment increases during the repayment period

- Opportunity cost of using equity vs. other options

Principle 3: Maintain Financial Flexibility

- Keep 20%+ equity cushion

- Don’t max out your credit line

- Maintain 3-6 months of emergency savings

- Have a backup plan if income decreases

Principle 4: Plan for Rate Increases

Variable rates will change. Prepare by:

- Stress-testing your budget at 2-3% higher rates

- Making principal payments during the draw period

- Building savings to handle payment increases

- Monitoring economic indicators

Principle 5: Read Everything

Before signing:

- Review all terms and conditions

- Understand rate adjustment mechanisms

- Know all fees and penalties

- Clarify the draw and repayment period lengths

- Ask questions about anything unclear

Making smart moves with your home equity requires the same discipline and research as any major financial decision.

The Bottom Line: Is a HELOC Right for You?

A HELOC can be a powerful financial tool when used strategically, offering flexible access to low-interest funds for value-creating purposes. The key is understanding exactly how it works, what it costs, and what risks you’re accepting.

A HELOC makes sense when you:

- Have substantial home equity (20%+ after the HELOC)

- Need funds for home improvements that add value

- Can comfortably afford payments even if rates rise 2-3%

- Have a stable income and good credit

- Understand the risks and responsibilities

- Have a specific purpose and repayment plan

Avoid a HELOC if you:

- They are already struggling with debt

- Don’t have a specific, value-creating purpose

- Have unstable income or employment

- Would be uncomfortable with variable payments

- Don’t fully understand the terms and risks

- Are you considering it for speculative investments

Remember, your home is likely your largest asset and most important financial foundation. Using it as collateral requires careful consideration, thorough planning, and disciplined execution.

For those exploring ways to build wealth, understanding why the stock market goes up over time and learning about the stock market more broadly might offer alternative paths to financial growth that don’t involve borrowing against your home.

Conclusion: Your Next Steps

If you’ve decided a HELOC aligns with your financial goals, here’s your action plan:

Step 1: Assess Your Situation

- Calculate your available equity

- Check your credit score

- Review your debt-to-income ratio

- Determine your specific borrowing purpose

Step 2: Prepare Your Application

- Gather financial documentation

- Research your home’s current value

- Address any credit issues

- Calculate how much you actually need

Step 3: Shop and Compare

- Get quotes from at least 3-5 lenders

- Compare rates, fees, and terms

- Read reviews and check lender reputations

- Ask detailed questions about all terms

Step 4: Make an Informed Decision

- Review all loan documents carefully

- Calculate total costs over the loan’s life

- Ensure payments fit comfortably in your budget

- Consider alternatives one final time

Step 5: Manage Responsibly

- Use funds only for the intended purpose

- Pay more than the minimum when possible

- Monitor your balance and rate regularly

- Prepare for the repayment period transition

A HELOC isn’t inherently good or bad—it’s a tool whose value depends entirely on how you use it. With proper understanding, careful planning, and disciplined execution, it can help you achieve important financial goals while preserving your home equity and financial security.

Before making any final decisions, consider consulting with a financial advisor who can evaluate your specific situation and help you determine whether a HELOC or alternative financing option best serves your needs.

For more insights on building wealth and making informed financial decisions, explore our comprehensive guides on personal finance and investing strategies.

FAQ: HELOCs

As of 2025, competitive HELOC rates range from 7.5% to 10%, depending on your credit score, debt-to-income ratio, and lender. Borrowers with excellent credit (740+) and strong financials can secure rates on the lower end of this range. Shop multiple lenders and compare not just the rate but also fees, terms, and features.

Use this formula: (Home Value × Lender’s LTV Ratio) – Existing Mortgage Balance = Maximum HELOC. For example, with a $400,000 home, 85% LTV, and $250,000 mortgage: ($400,000 × 0.85) – $250,000 = $90,000 maximum HELOC. Most lenders cap LTV at 80-85%, though some go higher for exceptional borrowers.

Yes. A HELOC is secured by your home, so failing to make payments can result in foreclosure, just like with your primary mortgage. This is why it’s crucial to borrow only what you can comfortably repay and maintain an emergency fund. Never use a HELOC for frivolous expenses or investments you don’t fully understand.

If your home value declines significantly, lenders may freeze your credit line or reduce your available credit to maintain acceptable loan-to-value ratios. In extreme cases where you owe more than your home is worth (being “underwater”), you could face difficulty refinancing or selling. This is why maintaining an equity cushion is important.

HELOC interest is tax-deductible only if you use the funds to “buy, build, or substantially improve” the home securing the loan, according to the IRS. Using a HELOC for debt consolidation, education, or investments does not qualify for the deduction. Consult a tax professional for your specific situation and refer to IRS Publication 936.

The HELOC approval process typically takes 2-6 weeks, depending on the lender and the complexity of your application. The timeline includes application submission (1-3 days), home appraisal (1-2 weeks), underwriting (1-2 weeks), and final approval and closing (3-5 days). Some online lenders offer faster processing, while traditional banks may take longer.

Most HELOCs allow early payoff without prepayment penalties, but some lenders charge an “early closure fee” if you close the HELOC within 2-3 years of opening. Always review your loan documents for specific terms. Paying down your balance early (without closing the account) typically has no penalty and saves substantial interest.

Most lenders require a minimum credit score of 620-640 for HELOC approval, though competitive rates typically require 700+. Borrowers with scores above 740 qualify for the best rates and terms. If your score is below 620, focus on improving it before applying—even a 20-30 point increase can significantly impact your rate.

Disclaimer

This article is for educational purposes only and does not constitute financial, tax, or legal advice. HELOC terms, rates, and regulations vary by lender, location, and individual circumstances. Interest rates, fees, and lending standards are subject to change. Tax treatment of HELOC interest depends on how funds are used and your individual tax situation, consult a qualified tax professional for personalized guidance.

Before applying for a HELOC, carefully review all loan documents, compare multiple lenders, and consider consulting with a financial advisor to ensure the product aligns with your financial goals and risk tolerance. Your home serves as collateral for a HELOC, and failure to repay could result in foreclosure.

The examples and calculations provided are for illustrative purposes and may not reflect actual costs or terms available to you. Always verify current rates, terms, and requirements directly with lenders.

Reference

- U.S. Securities and Exchange Commission (SEC.gov) – Investor education resources

- IRS Publication 936 – Home Mortgage Interest Deduction

- Consumer Financial Protection Bureau (CFPB) – HELOC regulations and consumer protections

- Federal Reserve – Interest rate data and economic indicators

Author Bio

Written by Max Fonji — With over a decade of experience in personal finance education and investment strategy, Max is your trusted guide for clear, data-backed financial insights. As the founder of TheRichGuyMath.com, Max is committed to helping everyday investors and homeowners make informed decisions that build lasting wealth. When not analyzing financial products or market trends, Max enjoys teaching others how to take control of their financial futures through education and smart planning.