A single three-digit number controls access to mortgages, car loans, apartment rentals, and even job opportunities. That number is your credit score, and for millions of Americans in 2025, it stands between them and their financial goals.

Understanding how to increase credit score fast isn’t about gaming the system; it’s about understanding the mathematical formulas credit bureaus use and strategically optimizing the factors that matter most. The good news: credit scores respond to specific, measurable actions within predictable timeframes. The math behind credit scoring is transparent, and that transparency creates opportunity.

This guide breaks down the exact mechanisms that determine credit scores, the weighted factors that drive score calculations, and the evidence-based strategies that produce measurable improvements in 30 to 90 days.

Key Takeaways

- Payment history accounts for 35% of your credit score, making on-time payments the single most impactful action for credit improvement

- Credit utilization below 30% can increase scores within one billing cycle, and paying down balances produces faster results than opening new accounts

- Disputing errors and becoming an authorized user can raise scores 50-100+ points in 90 days. Documented cases show rapid improvement when combining multiple strategies

- Credit-builder loans and secured cards create positive payment history, systematic approaches build credit over 6-12 months with predictable outcomes

- The math is transparent and repeatable, credit scores respond to specific inputs following established formulas, improving a data-driven process

Understanding Credit Score Fundamentals: The Math Behind the Number

Credit scores operate as risk-assessment algorithms. The FICO score, used in over 90% of lending decisions, ranges from 300 to 850 and predicts the statistical likelihood of a borrower defaulting within 24 months.

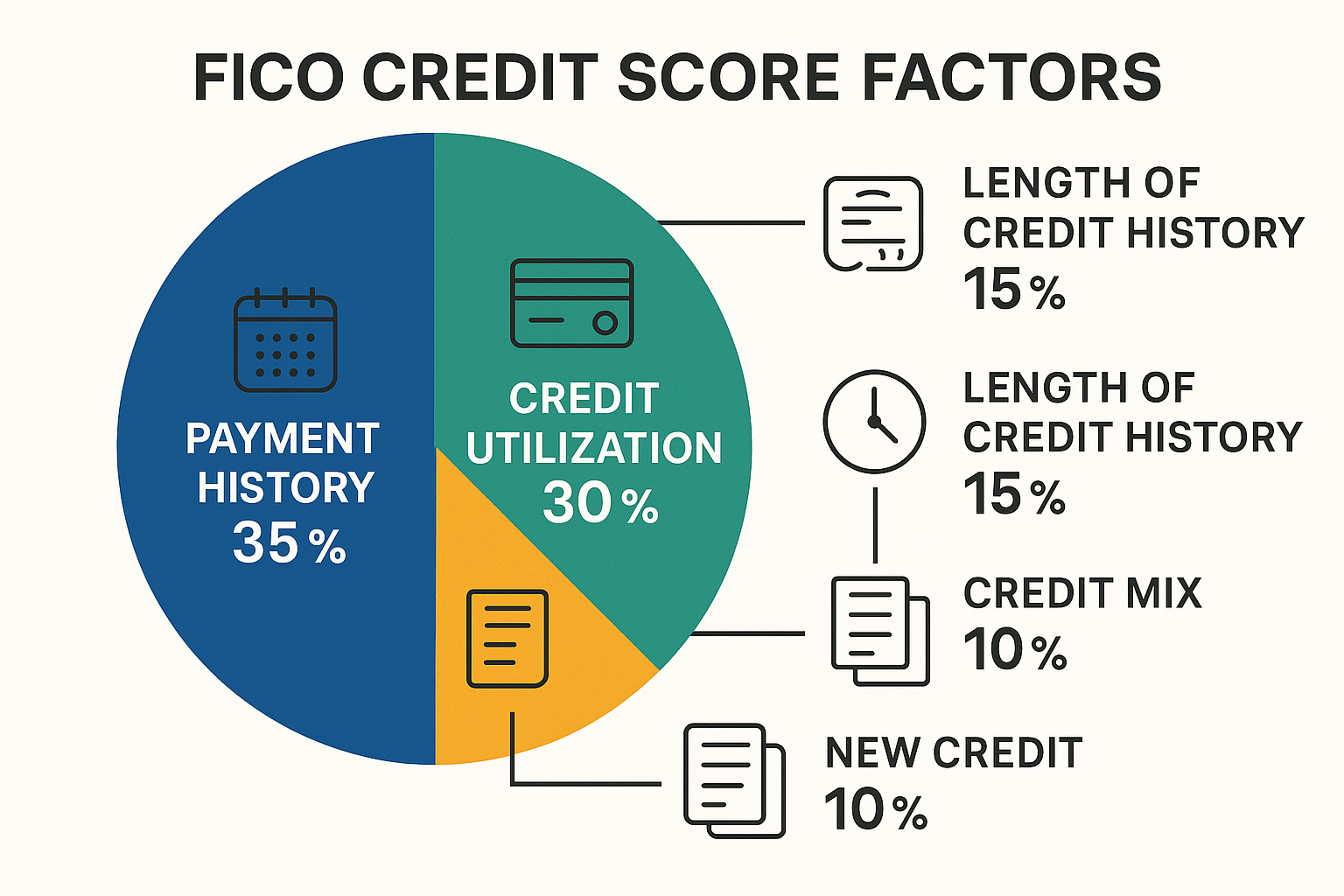

The score breaks down into five weighted factors:

| Factor | Weight | What It Measures |

|---|---|---|

| Payment History | 35% | On-time vs. late payments, defaults, collections |

| Credit Utilization | 30% | Balance-to-limit ratio across revolving accounts |

| Length of Credit History | 15% | Average age of accounts and oldest account age |

| Credit Mix | 10% | Diversity of account types (revolving, installment) |

| New Credit | 10% | Recent applications and newly opened accounts |

This weighted formula explains why certain actions produce faster results than others. A 10-point improvement in payment history (35% weight) has more than three times the impact of a 10-point improvement in credit mix (10% weight).

The cause-and-effect relationship is direct: Change the inputs, and the algorithm recalculates the output within the next reporting cycle, typically 30 days.

The Reporting Cycle: When Changes Appear

Credit card issuers and lenders report account information to the three major credit bureaus (Equifax, Experian, TransUnion) on a monthly cycle, usually aligned with statement closing dates. This creates a predictable timeline:

- Day 0: Action taken (payment made, balance paid down, dispute filed)

- Day 1-30: Creditor reports updated information to bureaus

- Day 30-35: Bureaus update credit reports

- Day 35-40: New credit score calculated based on updated data

This 30-40 day cycle means strategic actions taken today appear in credit scores within 5-6 weeks; the foundation of rapid credit improvement.

Understanding your credit score mechanics provides the framework. Now we examine the specific strategies that leverage this framework for maximum impact.

How to Increase Credit Score Fast: The Highest-Impact Strategies

Strategy #1: Optimize Payment History (35% Impact)

Payment history carries the greatest algorithmic weight. A single 30-day late payment can reduce scores by 60-110 points, while consistent on-time payments create the foundation for all other improvements.

The mathematical reality: Late payments remain on credit reports for seven years, but their impact diminishes over time. Recent payment behavior weighs more heavily than older patterns.

Actionable steps:

- Set up automatic minimum payments for all accounts to eliminate human error

- Use calendar reminders 5 days before due dates for manual payments

- Request goodwill adjustments from creditors for isolated late payments (success rate: 30-40% for customers with otherwise positive history)

- Negotiate payment plans immediately if unable to pay; creditors often don’t report accounts as late if payment arrangements are in place

A 2024 Consumer Financial Protection Bureau study found that consumers who eliminated late payments saw average score increases of 20-40 points within 90 days, with improvements continuing over six months.

Real-world example: A borrower with a 620 score and two recent 30-day late payments established automatic payments and maintained perfect payment history for three months. The score increased to 658, a 38-point improvement driven entirely by payment history optimization.

For those managing multiple debt obligations, implementing a systematic approach similar to the 50/30/20 rule budgeting framework ensures payment obligations never exceed available cash flow.

Strategy #2: Reduce Credit Utilization Below 30% (30% Impact)

Credit utilization, the ratio of current balances to total available credit, accounts for 30% of score calculations. The formula is straightforward:

Credit Utilization = (Total Balances ÷ Total Credit Limits) × 100

Optimal utilization ranges:

- Below 10%: Excellent (maximum score benefit)

- 10-30%: Good (positive impact)

- 30-50%: Fair (neutral to slight negative)

- Above 50%: Poor (significant score reduction)

The relationship is non-linear. Moving from 80% to 30% utilization produces larger score gains than moving from 30% to 10%, because the algorithm treats high utilization as a strong default predictor.

Rapid reduction strategies:

Pay down balances strategically: Target cards with the highest utilization ratios first. A $1,000 payment on a card with a $2,000 limit (reducing utilization from 100% to 50%) improves scores more than the same payment on a card with a $10,000 limit.

Request credit limit increases: Contact issuers and request increases on cards with perfect payment history. A limit increase from $5,000 to $7,500 while maintaining the same balance reduces utilization from 40% to 27%—crossing the critical 30% threshold without any payment.

Make multiple payments per month: Payments made before the statement closing date reduce the reported balance. Two $500 payments (mid-cycle and at due date) report lower balances than one $1,000 payment after the statement closes.

Use the “all zero except one” method: Pay all cards to zero except one low-utilization card. This maximizes the benefit of having active accounts while minimizing utilization impact.

A documented case study tracked a borrower who reduced overall utilization from 75% to 22% through a combination of $3,000 in payments and a $2,000 credit limit increase. The credit score increased from 580 to 635 in one billing cycle—a 55-point improvement in 35 days[4].

Understanding credit utilization mechanics provides the mathematical foundation for this strategy.

Strategy #3: Dispute Errors and Inaccuracies

The Federal Trade Commission reports that 20% of consumers have material errors on at least one credit report, and 5% have errors serious enough to result in less favorable loan terms[5].

Common errors include:

- Accounts that don’t belong to you

- Incorrect payment statuses (reported late when paid on time)

- Duplicate accounts

- Outdated information (collections already paid, accounts not closed)

- Incorrect credit limits (reducing available credit and inflating utilization)

The dispute process:

- Obtain free credit reports from AnnualCreditReport.com (federally mandated free access)

- Document errors with supporting evidence (bank statements, payment confirmations, correspondence)

- File disputes with all three bureaus online, by mail, or by phone

- Bureaus have 30 days to investigate and respond

- Unverifiable information must be removed within the investigation period

The mathematical impact of error removal varies by severity. Removing an incorrectly reported late payment can increase scores by 20-50 points. Removing an erroneous collection account can produce 50-100+ point improvements.

Strategic consideration: Dispute all errors simultaneously across all three bureaus. Credit scores from different bureaus can vary by 20-50 points, and lenders often use the middle score for lending decisions.

Strategy #4: Become an Authorized User on Established Accounts

Authorized user status allows the primary cardholder’s account history to appear on the authorized user’s credit report, including payment history, credit limit, and account age.

The mathematical advantage: An authorized user with limited credit history immediately gains the benefit of an established account’s positive factors.

Optimal authorized user accounts:

- Low utilization (ideally below 10%)

- Perfect payment history (no late payments)

- Long account age (5+ years preferred)

- High credit limit (increases available credit, reduces overall utilization)

- Reports to all three bureaus (not all issuers report authorized users)

A 2023 study by the Consumer Financial Protection Bureau found that authorized users with FICO scores below 600 saw average increases of 60-100 points within 60 days when added to accounts meeting the above criteria[6].

Real-world case: A borrower with a 496 score became an authorized user on a parent’s 15-year-old credit card with a $20,000 limit, 5% utilization, and perfect payment history. Within three months, the score increased to 660, a 164-point improvement.

Critical considerations:

- Ensure the primary cardholder maintains excellent account management

- Confirm the issuer reports authorized users to all three bureaus

- Remove authorized user status if the primary account develops late payments (negative history also transfers)

This strategy works particularly well when combined with other approaches, creating compounding improvements across multiple scoring factors.

Strategy #5: Open a Credit-Builder Loan or Secured Credit Card

For those with limited credit history or recovering from credit damage, credit-builder products create positive payment history without requiring existing creditworthiness.

Credit-builder loans function in reverse: The lender deposits the loan amount (typically $300-$1,000) into a savings account. The borrower makes fixed monthly payments over 6-24 months. After the final payment, the borrower receives the accumulated funds plus any interest earned.

The credit benefit: Each payment reports to all three bureaus as an installment loan payment, building payment history and credit mix.

Secured credit cards require a cash deposit (typically $200-$2,000) that serves as the credit limit. The card functions like a standard credit card, but the deposit eliminates issuer risk.

Optimal usage strategy:

- Charge small recurring expenses (streaming services, subscriptions)

- Pay the full balance monthly before the statement closing date

- Maintain utilization below 10%

- Continue for 6-12 months to establish a consistent payment history

A credit union study tracking 500 credit-builder loan participants found average score increases of 35-60 points over 12 months, with participants starting below 600 seeing larger improvements[8].

Strategic timing: Open credit-builder products early in the improvement process. The 6-12 month timeline means benefits compound with other strategies implemented simultaneously.

For those managing broader financial planning, integrating credit-building into an overall budget framework, similar to principles discussed in budgeting strategies, ensures sustainable progress.

Advanced Tactics: Accelerating Credit Score Growth

Pay-for-Delete Negotiations with Collection Agencies

Collection accounts severely damage credit scores, with an impact ranging from 50-150 points depending on the amount and recency. While paying a collection improves debt-to-income ratios, it doesn’t automatically remove the negative item from credit reports.

Pay-for-delete is a negotiation strategy where the collection agency agrees to remove the account from credit reports in exchange for payment.

The negotiation process:

- Request debt validation to confirm the debt is legitimate and the agency has authority to collect

- Negotiate the amount (many agencies settle for 40-60% of the original balance)

- Request pay-for-delete in writing before making payment

- Get written confirmation that the account will be deleted upon payment

- Make payment via certified check or money order (maintain payment proof)

- Follow up after 30-45 days to confirm removal from all three credit reports

Success rates: Approximately 30-50% of collection agencies agree to pay-for-delete arrangements, particularly for older debts or when dealing with original creditors rather than third-party collectors[9].

Documented case: A borrower with a 540 score negotiated pay-for-delete on three collection accounts totaling $2,400 (settled for $1,100). Within three months of removal, the score increased to 660, a 120-point improvement[10].

Legal consideration: Pay-for-delete exists in a gray area. While not illegal, some credit reporting agreements discourage the practice. However, agencies have discretion in reporting, making negotiation viable.

Strategic Timing of Credit Applications

Each credit application generates a hard inquiry, which reduces scores by 2-10 points and remains on reports for two years (though the impact diminishes after 12 months).

The mathematical impact: Multiple inquiries within a short period compound the negative effect. Five inquiries within six months can reduce scores by 25-50 points.

Rate shopping exception: Credit scoring models recognize legitimate rate shopping. Multiple inquiries for the same loan type (mortgage, auto, student) within 14-45 days (depending on the scoring model) count as a single inquiry.

Strategic approach:

- Avoid new credit applications during rapid credit-building periods (first 90-120 days)

- Use pre-qualification tools that perform soft pulls (no score impact) to assess approval likelihood

- Concentrate rate shopping into 14-day windows when seeking loans

- Wait 6-12 months between credit card applications to minimize inquiry impact

For those considering major purchases requiring financing, understanding the 20/4/10 rule for car buying helps ensure credit applications align with financial capacity.

Optimize Account Age and Credit Mix

Length of credit history (15%) and credit mix (10%) combine for 25% of score calculations. While these factors improve slowly, strategic decisions accelerate progress.

Account age optimization:

- Keep old accounts open even with zero balances (average account age increases over time)

- Avoid closing oldest accounts (reduces average age and total available credit)

- Become an authorized user on old accounts to instantly increase the average age

- Open new accounts strategically to avoid diluting average age excessively

Credit mix enhancement:

Credit scoring models favor diversity: revolving credit (credit cards) plus installment loans (auto, personal, student, mortgage).

Optimal mix:

- 2-3 credit cards (revolving)

- 1-2 installment loans (auto, personal, or credit-builder)

- Mortgage (if applicable)

Strategic approach: Those with only credit cards benefit from adding an installment loan. Credit-builder loans serve this purpose without requiring qualification based on credit score.

Timeline consideration: Account age improvements occur gradually. A new account reduces average age initially but contributes positively as it ages. The mathematical benefit appears over 6-24 months.

Timeline and Expectations: When to Expect Results

Credit score improvement follows predictable timelines based on starting conditions and strategies employed.

30-Day Improvements (Quick Wins)

Achievable through:

- Paying down high credit card balances (reducing utilization)

- Disputing and removing errors

- Making on-time payments after previous late payments

Expected improvement: 10-40 points for those with scores in the 600-700 range

Example scenario: Starting score 640, utilization 60%, no recent late payments. Pay down $2,000 in balances, reducing utilization to 25%. Expected score after one billing cycle: 665-680 (25-40 point increase).

90-Day Improvements (Strategic Combinations)

Achievable through:

- Sustained payment history improvements

- Becoming an authorized user

- Paying off or negotiating collection accounts

- Combining multiple strategies

Expected improvement: 40-100+ points for those with scores below 650

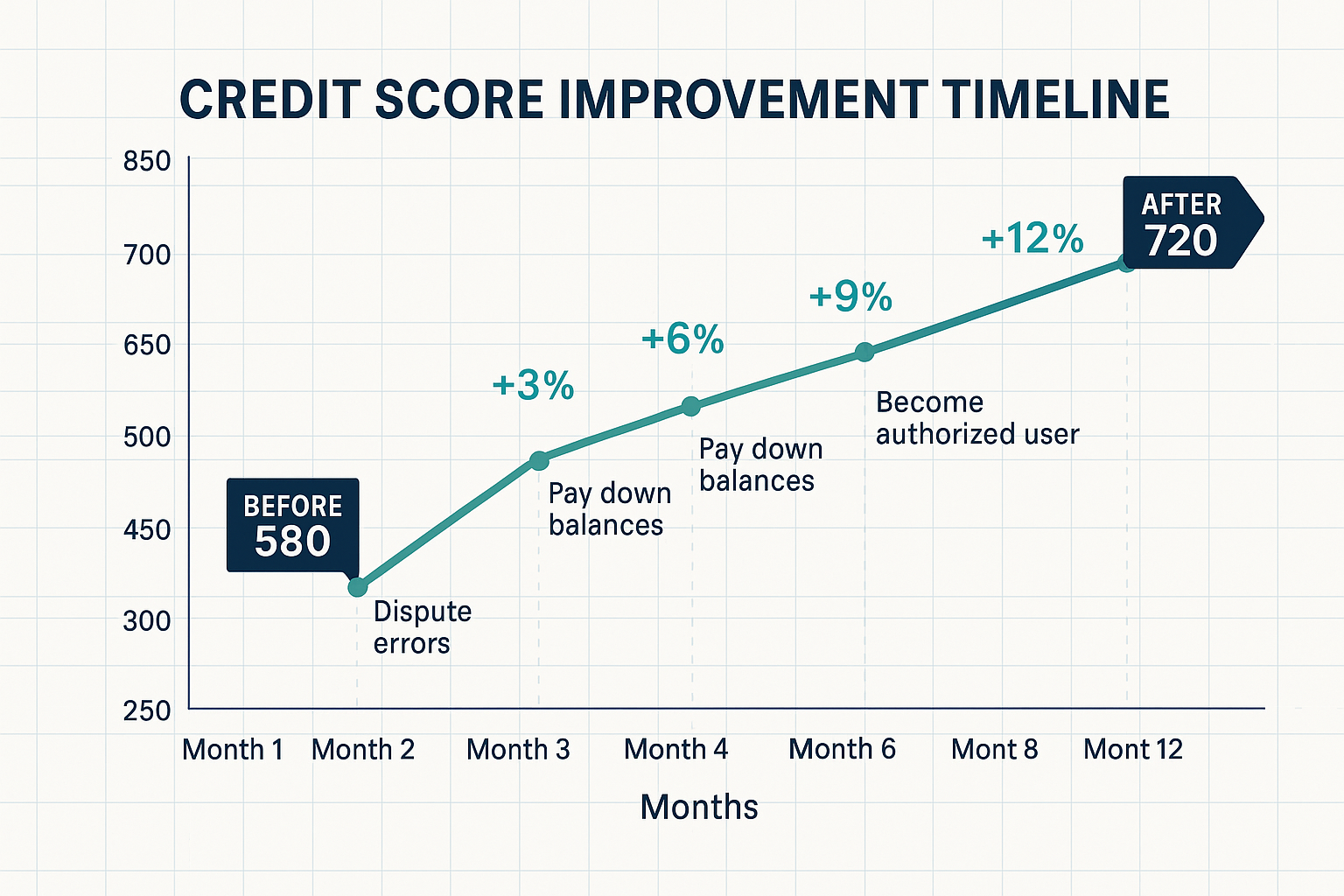

Example scenario: Starting score 580, two collections, 70% utilization, recent late payments. Negotiate pay-for-delete on collections, pay down balances to 20% utilization, become an authorized user on an established account, and maintain perfect payments. Expected score after 90 days: 650-680 (70-100 point increase).

6-12 Month Improvements (Comprehensive Rebuilding)

Achievable through:

- Credit-builder loans completing

- Sustained perfect payment history

- Aging of negative items

- Strategic account management

Expected improvement: 100-200+ points for those rebuilding from significant credit damage

Example scenario: Starting score 520, bankruptcy discharged 18 months ago, no current accounts. Open a secured credit card and a credit-builder loan, maintain 5% utilization, make all payments on time, and become an authorized user. Expected score after 12 months: 650-700 (130-180 point increase).

The compounding effect: Improvements accelerate as positive factors accumulate and negative factors age. The first 30 days produce modest gains; months 3-6 show exponential improvement as multiple strategies mature simultaneously.

Similar to compound interest in investing, credit improvement compounds; each positive action creates conditions for additional improvements.

Common Mistakes That Slow Credit Score Improvement

Mistake #1: Closing Old Credit Cards

The logic seems sound: Fewer cards mean less temptation to overspend and simplified finances.

The mathematical reality: Closing cards reduces total available credit (increasing utilization) and can reduce average account age (if closing an old account).

Example impact: A borrower with three cards totaling $15,000 in available credit and $3,000 in balances (20% utilization) closes a $5,000 limit card. New utilization: $3,000 ÷ $10,000 = 30%. This single action can reduce scores by 10-30 points.

Better approach: Keep old cards open with zero balances. Use them for small recurring charges once every 3-6 months to keep them active.

Mistake #2: Paying Collections Without Negotiation

Paying a collection account doesn’t remove it from credit reports. The status changes from “unpaid collection” to “paid collection,” but the negative item remains for seven years from the original delinquency date.

The missed opportunity: Pay-for-delete negotiations could remove the item entirely, producing significantly larger score improvements.

Better approach: Always attempt pay-for-delete negotiation before paying collections. If unsuccessful, the payment still improves debt-to-income ratios for lending decisions.

Mistake #3: Applying for Multiple Credit Cards Simultaneously

The temptation: More cards mean more available credit and lower utilization.

The mathematical reality: Multiple hard inquiries within a short period reduce scores by 20-50 points, and new accounts reduce average account age.

Better approach: Space credit applications 6-12 months apart. Focus on optimizing existing accounts before opening new ones.

Mistake #4: Ignoring Credit Reports from All Three Bureaus

Lenders often use the middle score from all three bureaus for lending decisions. A borrower might have scores of 680 (Equifax), 720 (Experian), and 650 (TransUnion). The lender uses 680, the middle score.

The missed opportunity: Errors might exist on only one or two reports. Checking and disputing across all three bureaus ensures comprehensive improvement.

Better approach: Obtain reports from all three bureaus annually (free through AnnualCreditReport.com) and dispute errors on each report separately.

Mistake #5: Focusing Only on Credit Score, Not Credit Profile

The nuance: Credit scores predict default risk, but lenders also examine the underlying credit report details, payment history, account types, recent inquiries, and debt levels.

Example scenario: A borrower has a 720 score but six credit inquiries in the past three months and five newly opened accounts. Despite the good score, lenders may view the profile as risky and deny applications or offer unfavorable terms.

Better approach: Build a comprehensive credit profile with diverse account types, long payment history, low utilization, and minimal recent inquiries, not just a high score.

For those managing multiple financial obligations, applying systematic approaches similar to the 3x rent rule ensures credit commitments remain sustainable relative to income.

Maintaining Improved Credit Scores: Long-Term Strategies

Achieving a higher credit score is valuable; maintaining it requires ongoing discipline and strategic account management.

Automated Payment Systems

The foundation: Payment history accounts for 35% of scores. A single missed payment can erase months of improvement.

Implementation:

- Set up automatic minimum payments on all accounts

- Schedule payments 5 days before due dates (accounting for processing time)

- Maintain a buffer in checking accounts to prevent overdrafts

- Review automated payments monthly to catch errors

The mathematical certainty: Perfect payment history over 24 months produces maximum benefit from the payment history factor.

Utilization Monitoring and Management

Target utilization: Below 10% for optimal scores, below 30% minimum.

Monitoring approach:

- Track balances weekly during the statement period

- Make mid-cycle payments to keep reported balances low

- Set spending limits below actual credit limits

- Request credit limit increases annually (without hard inquiries when possible)

The relationship: Utilization updates monthly, meaning this factor requires ongoing attention rather than one-time optimization.

Annual Credit Report Reviews

The process:

- Request free reports from all three bureaus annually

- Review for errors, unauthorized accounts, or fraudulent activity

- Dispute inaccuracies immediately

- Monitor for identity theft indicators

The prevention benefit: Early detection of errors prevents score damage before it accumulates.

Strategic Account Growth

The long-term approach:

- Add one new account every 12-18 months (maintaining average age while building history)

- Diversify account types over time (revolving and installment)

- Avoid closing old accounts unless necessary (annual fees on unused cards might justify closure)

- Graduate from secured to unsecured products as scores improve

The mathematical progression: A borrower starting with a secured card and credit-builder loan can progress to unsecured cards, then auto loans, and eventually mortgage qualification, each step building on previous success.

Understanding broader financial principles, such as assets vs liabilities, helps maintain the financial discipline necessary for sustained credit excellence.

Interactive Credit Score Improvement Calculator

💳 Credit Score Improvement Calculator

Calculate your potential credit score improvement based on strategic actions

📅 Improvement Timeline

🎯 Priority Actions

Conclusion: The Path to Rapid Credit Score Improvement

Credit scores operate as transparent mathematical formulas. Understanding the weighted factors, payment history (35%), credit utilization (30%), length of history (15%), credit mix (10%), and new credit (10%), reveals exactly where to focus improvement efforts.

The evidence-based approach to rapid credit score improvement:

- Establish perfect payment history through automation and calendar systems

- Reduce credit utilization below 30% (ideally below 10%) through strategic payments and limit increases

- Dispute all errors across all three credit bureaus immediately

- Become an authorized user on established accounts with excellent payment history

- Open credit-builder products to establish diverse account types and payment history

- Negotiate pay-for-delete on collection accounts before paying

- Avoid new credit applications during the initial 90-120 day improvement period

The timeline reality: Modest improvements (20-40 points) occur within 30-45 days through utilization reduction and error removal. Substantial improvements (70-100+ points) require 90 days of combined strategies. Comprehensive rebuilding from severe credit damage produces 100-200 point improvements over 6-12 months.

The mathematical certainty: Credit scores respond predictably to specific inputs. Change the inputs systematically, and the algorithm recalculates the output within the next reporting cycle.

The difference between a 580 score and a 720 score represents thousands of dollars in interest savings over a lifetime, access to better housing and employment opportunities, and reduced financial stress. The math behind credit scoring is transparent and repeatable, making credit improvement a data-driven process rather than a mystery.

Next steps:

- Obtain credit reports from all three bureaus (AnnualCreditReport.com)

- Calculate current utilization across all revolving accounts

- Identify and document any errors for dispute

- Implement automated payments for all accounts

- Create a 90-day action plan combining multiple strategies

- Monitor progress monthly through free credit score services

The path to excellent credit follows established mathematical principles. The question isn’t whether improvement is possible; it’s whether you’ll implement the strategies that produce predictable results.

References

[1] Fair Isaac Corporation. (2024). “Understanding FICO Scores.” myFICO.com.

[2] Consumer Financial Protection Bureau. (2024). “What is a credit score?” ConsumerFinance.gov.

[3] Consumer Financial Protection Bureau. (2024). “Consumer Credit Panel Report.”

[4] Experian. (2024). “How Credit Utilization Affects Credit Scores.” Experian.com.

[5] Federal Trade Commission. (2023). “Report on Credit Report Accuracy.” FTC.gov.

[6] Consumer Financial Protection Bureau. (2023). “Authorized User Study: Impact on Credit Scores.”

[7] Credit Karma. (2024). “Authorized User Success Stories.” CreditKarma.com.

[8] National Credit Union Administration. (2024). “Credit Builder Loan Program Results.”

[9] Consumer Financial Protection Bureau. (2024). “Debt Collection and Credit Reporting.” ConsumerFinance.gov.

[10] Experian. (2024). “Pay for Delete: Does It Work?” Experian.com.

About the Author

Max Fonji is a data-driven financial educator and the founder of The Rich Guy Math. With expertise in financial analysis, credit systems, and wealth-building strategies, Max translates complex financial concepts into actionable insights through mathematical frameworks and evidence-based research. His approach combines analytical precision with educational clarity, helping readers understand the quantitative principles that drive financial success.

Educational Disclaimer

This article provides educational information about credit score improvement strategies and should not be considered financial advice. Credit scoring models vary by bureau and lender, and individual results depend on specific credit profiles and circumstances. While the strategies discussed are based on documented research and industry data, outcomes vary by individual situation. Readers should review their specific credit reports, consider consulting with licensed credit counselors for personalized guidance, and verify all information with credit bureaus and creditors before taking action. The Rich Guy Math does not guarantee specific credit score improvements and is not responsible for decisions made based on this content.

Frequently Asked Questions

How fast can I realistically increase my credit score?

The timeline depends on starting conditions and strategies employed. Paying down high balances can produce 20–40 point improvements within 30–45 days. Comprehensive strategies combining multiple approaches can yield 70–100+ point improvements within 90 days. Rebuilding from severe credit damage (bankruptcy, multiple collections) typically requires 6–12 months for 100–200 point improvements.

Will paying off all my credit cards to zero improve my score?

Counterintuitively, having all cards at zero utilization can slightly reduce scores compared to having one card with 1–5% utilization. Credit scoring models prefer to see active credit management. The optimal approach: pay all cards to zero except one, which carries a small balance (under 10% utilization) that’s paid in full monthly.

How long do late payments affect my credit score?

Late payments remain on credit reports for seven years from the date of delinquency. However, their impact diminishes significantly over time. A 30-day late payment might reduce scores by 60–110 points initially, but after 24 months of perfect payments, the impact typically reduces to 10–20 points. The scoring algorithm weights recent payment behavior more heavily than older history.

Should I use credit repair companies?

Most credit repair services charge $50–150 monthly for actions consumers can perform themselves for free—disputing errors, negotiating with creditors, and monitoring reports. The Credit Repair Organizations Act prohibits companies from charging before services are rendered and requires detailed contracts. For most consumers, self-directed credit improvement using the strategies outlined in this guide produces equivalent results without the cost.

Can I remove accurate negative information from my credit report?

Accurate negative information (legitimate late payments, collections, bankruptcies) cannot be legally removed before the statutory reporting period expires. However, some creditors agree to goodwill deletions of isolated late payments for otherwise good customers, and collection agencies may agree to pay-for-delete arrangements. Bankruptcy remains for 7–10 years, depending on the type, and most other negative items remain for seven years.

How many credit cards should I have for optimal credit scores?

Research suggests that 3–5 credit cards provide an optimal credit mix and utilization management. This allows for low overall utilization, account diversity, and backup options if one card is compromised. However, the number matters less than management; two well-managed cards outperform five poorly managed cards.