The math behind money doesn’t require thousands of dollars to get started. In 2025, you can begin building real wealth with just $100, no special connections, no finance degree, and no waiting until you “have more saved up.”

This guide explains how to start investing with $100 using data-driven insights and evidence-based strategies. You’ll learn the exact steps to take today, which investment options make sense for small amounts, and what realistic returns look like over time.

The cost of waiting is higher than most beginners realize. Because of compound growth, starting with $100 today beats waiting five years to invest $1,000. The habit you build matters more than the initial amount.

Key Takeaways

- You can start investing with $100 thanks to fractional shares and zero-commission brokerages that have eliminated traditional barriers.

- Index ETFs offer the best risk-adjusted returns for beginners because they provide instant diversification across hundreds of companies.

- Consistency beats timing—investing $100 monthly outperforms waiting to invest larger lump sums due to compound growth mechanics.

- Avoid high-interest debt first—credit card interest (18-24% APR) mathematically outweighs average market returns (10% annually)

- Small amounts build wealth habits—the psychological momentum from starting creates discipline that compounds alongside your money.

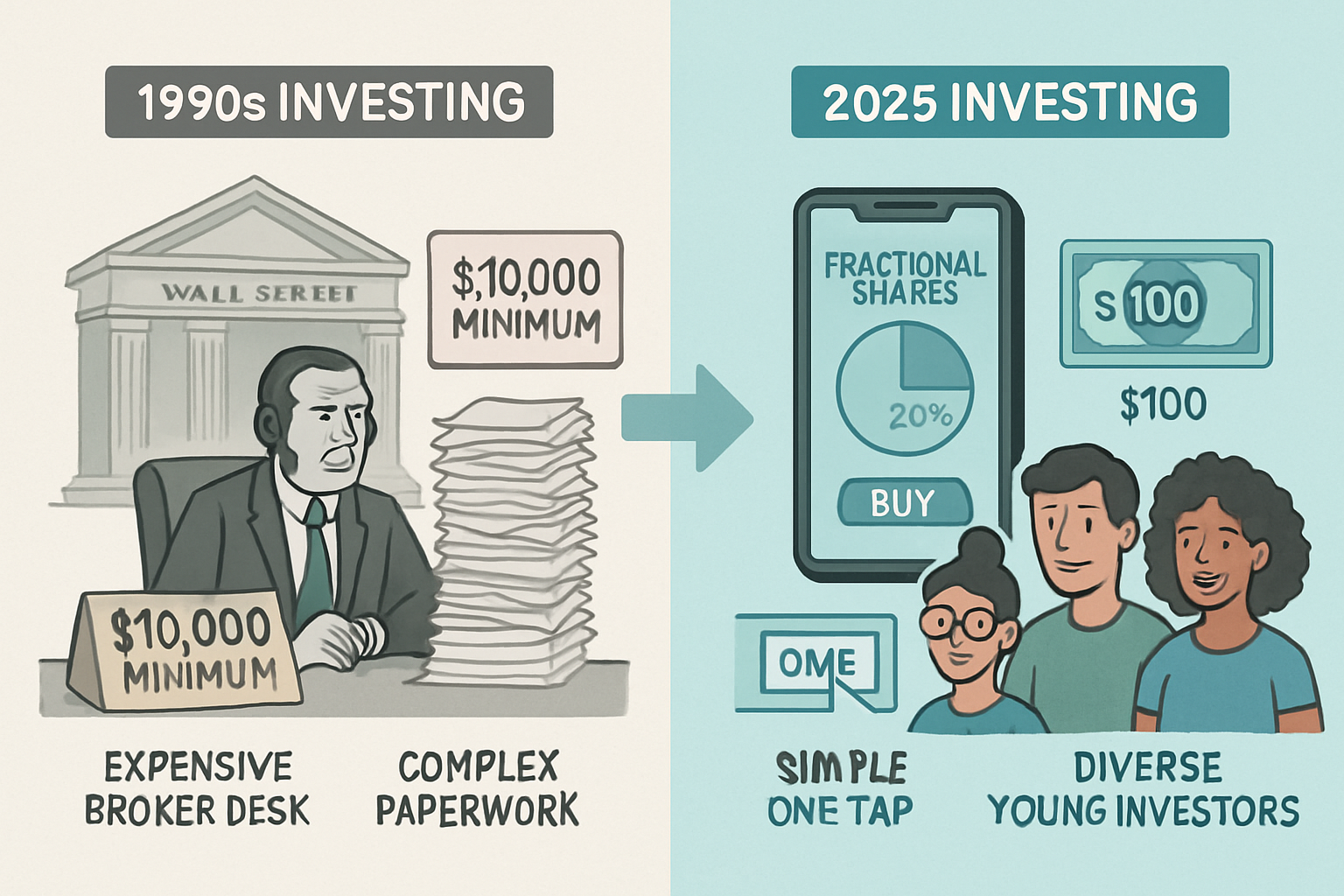

Can You Really Start Investing with $100?

Yes. The barrier to entry for investing has dropped from thousands of dollars to as little as $1.

Modern investing platforms removed three historical obstacles:

- Minimum account balances (previously $500-$3,000)

- Trading commissions ($7-$10 per trade)

- Whole share requirements (one share of expensive stocks costs hundreds)

Fractional shares changed the game. This innovation allows you to own a portion of a single share based on dollar amount rather than share count.

Example: If a company’s stock trades at $500 per share, your $100 buys 0.2 shares. You own that percentage of the stock and receive proportional returns.

As a result, $100 now provides access to the same investments previously reserved for wealthy investors—S&P 500 index funds, blue-chip stocks, and diversified portfolios.

The Old vs New Investing Landscape

| Barrier | 1990s Requirements | 2025 Reality |

|---|---|---|

| Minimum Investment | $2,500-$10,000 | $1-$100 |

| Trading Fees | $7-$50 per trade | $0 (most platforms) |

| Share Purchase | Whole shares only | Fractional shares available |

| Account Minimums | $500-$1,000 | $0 |

| Professional Management | $100,000+ | $100 (robo-advisors) |

The data proves accessibility has democratized. According to Federal Reserve research, the percentage of households owning stocks increased from 48.6% in 1989 to 58.2% in 2022, driven largely by lower barriers to entry[1].

Takeaway: Technology eliminated the excuse that “you need money to make money.” The question isn’t whether $100 is enough—it’s what you do with it.

What to Do Before You Invest Your First $100

Investing before addressing foundational financial issues creates unnecessary risk. The math behind money requires a specific sequence.

Build a Small Cash Buffer

An emergency fund prevents forced selling during market downturns.

Why this matters: If your $100 represents your only savings and an unexpected $200 expense appears, you’ll need to sell investments—potentially at a loss—to cover the cost.

Minimum recommendation: $500-$1,000 in a high-yield savings account before investing. This amount covers most minor emergencies (car repair, medical copay, urgent home fix) without touching investments.

The opportunity cost is minimal. High-yield savings accounts currently offer 4-5% APY, which provides growth while maintaining liquidity.

Action step: If you have less than $500 saved, split your $100—put $50 into savings and $50 into your first investment. This builds both safety and investing habits simultaneously.

Pay Off High-Interest Debt First

Credit card debt mathematically destroys wealth faster than investing creates it.

The numbers:

- Average credit card APR: 20.09% (2025 Federal Reserve data)[2]

- Average annual stock market return: 10.26% (S&P 500, 1957-2024)[3]

- Net loss from investing while carrying credit card debt: -9.83% annually

Paying down a 20% APR balance guarantees a 20% “return” on that money. No investment offers guaranteed double-digit returns without extreme risk.

Exception: If your debt carries interest below 5% (federal student loans, mortgage), investing while making minimum payments makes mathematical sense because market returns likely exceed the interest cost.

Calculation example:

- $1,000 credit card balance at 20% APR = $200 annual interest

- $1,000 invested at 10% return = $100 annual gain

- Net result: -$100 loss

Therefore, eliminate high-interest debt before investing. The guaranteed “return” from debt payoff exceeds probable investment gains.

Takeaway: Financial literacy means understanding cause and effect. Investing in high-interest debt actively creates negative compound growth—the opposite of wealth building.

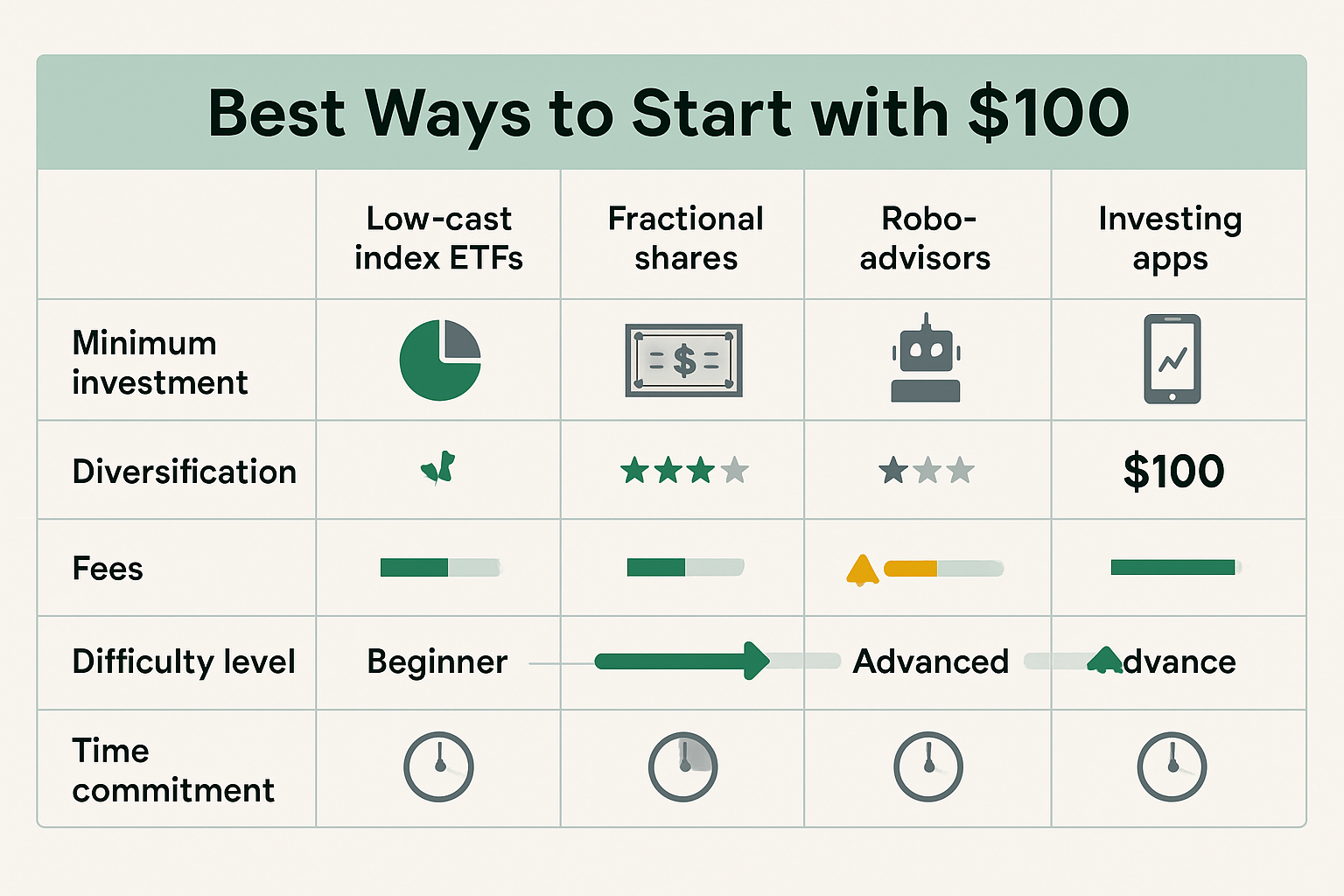

Best Ways to Start Investing with $100 (Ranked)

Not all investment options suit small-dollar beginners equally. These rankings consider risk, diversification, fees, and learning curve.

Option #1 – Low-Cost Index ETFs (Best for Beginners)

What it is: An Exchange-Traded Fund (ETF) that tracks a market index (like the S&P 500) by holding all or representative stocks from that index.

Plain English explanation: Instead of picking individual companies, you buy a basket containing hundreds of companies in one transaction. If the overall market grows, your investment grows proportionally.

Why this works for $100:

- Instant diversification across 500+ companies

- Low expense ratios (0.03-0.20% annually)

- Fractional shares are available on most platforms

- Historically reliable returns (10% average annually)

Example: The Vanguard S&P 500 ETF (VOO) tracks America’s 500 largest companies. One share costs approximately $400 (as of 2025), but you can buy $100 worth (0.25 shares) through fractional investing.

Your $100 now owns tiny pieces of Apple, Microsoft, Amazon, Google, and 496 other companies. This diversification reduces single-company risk dramatically.

Risk management principle: Diversification doesn’t eliminate risk, but it reduces unsystematic risk (company-specific problems). You still face systematic risk (overall market declines), but history shows markets recover and grow over long periods.

Best index funds provide a detailed analysis of the top options for beginners.

ETF Benefits vs Individual Stocks

| Factor | Index ETF | Individual Stock |

|---|---|---|

| Diversification | 500+ companies | 1 company |

| Risk Level | Lower (market risk only) | Higher (company-specific risk) |

| Research Required | Minimal | Extensive |

| Emotional Difficulty | Easier to hold long-term | Harder (volatility stress) |

| Learning Curve | Beginner-friendly | Intermediate-advanced |

| Time Commitment | 5 minutes to buy | Hours of analysis |

Recommended ETFs for $100:

- VOO (Vanguard S&P 500): 0.03% expense ratio

- VTI (Vanguard Total Stock Market): 0.03% expense ratio

- SCHD (Schwab U.S. Dividend Equity): 0.06% expense ratio

Takeaway: Index ETFs provide the highest probability of positive returns for beginners because they eliminate stock-picking risk and minimize fees. This is evidence-based investing—following what data shows works over decades.

Option #2 – Fractional Shares of Stocks

What it is: Purchasing a percentage of a single company’s share based on dollar amount rather than share quantity.

When this makes sense:

- You want to learn about individual companies

- You’re willing to accept higher risk for potentially higher returns

- You have a specific conviction about certain businesses

- You plan to study financial statements and business models

Pros:

- Educational value (learning to analyze businesses)

- Potential for above-market returns

- Direct ownership in companies you understand

- Builds valuation skills over time

Cons:

- Concentration risk (one company’s problems = significant loss)

- Requires ongoing research and monitoring

- Greater emotional difficulty during volatility

- No guarantee of beating index returns (most don’t)

Example scenario: You invest $100 in a single technology stock trading at $250 per share. You own 0.4 shares. If the stock rises 20%, your investment becomes $120. If it falls by 20%, you have $80.

Compare this to an S&P 500 ETF, where your $100 is spread across 500 companies. One company’s 20% decline barely impacts your total return because it represents just 0.2% of your holdings.

Risk calibration: Professional investors recommend no more than 5-10% of your portfolio in any single stock. With $100 total, buying individual stocks means 100% concentration—maximum risk.

Better approach: Start with ETFs until you have $1,000+, then allocate 10-20% to individual stocks while maintaining a diversified core.

Takeaway: Fractional shares democratized access, but access doesn’t equal wisdom. Use this option for learning, not for your entire $100.

Option #3 – Robo-Advisors (Hands-Off Option)

What it is: Automated investment platforms that build and manage diversified portfolios based on your risk tolerance and goals.

How it works:

- You answer questions about age, goals, and risk comfort

- The algorithm creates a portfolio (usually 5-10 ETFs)

- The platform automatically rebalances and reinvests dividends

- You contribute regularly without making decisions

Who should use robo-advisors:

- Complete beginners who want professional-style management

- People who lack time for investment research

- Those who want to avoid emotional decision-making

- Investors seeking automatic rebalancing

Fee structure explained:

- Management fee: 0.25-0.50% of assets annually

- Underlying ETF fees: 0.05-0.15% annually

- Total cost: 0.30-0.65% per year

Math example: $100 invested with a 0.25% management fee = $0.25 annual cost. As your balance grows to $10,000, the fee becomes $25 annually.

Trade-off analysis:

- Benefit: Professional portfolio construction, automatic optimization

- Cost: 0.25% fee on $100 = $0.25 (negligible)

- Cost: 0.25% fee on $100,000 = $250 (significant over decades)

Top robo-advisors for small accounts:

- Betterment: $0 minimum, 0.25% fee

- Wealthfront: $500 minimum, 0.25% fee

- Schwab Intelligent Portfolios: $5,000 minimum, $0 advisory fee

For $100 specifically, Betterment offers the most accessible entry point.

Best robo-advisors 2025 provides comprehensive platform comparisons.

Takeaway: Robo-advisors make sense for hands-off investors, but DIY index ETF investing costs less and provides similar diversification. The convenience premium is 0.25% annually—decide if that’s worth the automation.

Option #4 – Investing Apps (What to Watch Out For)

What they are: Mobile-first platforms designed to make investing accessible and engaging through simplified interfaces.

Popular examples:

- Robinhood

- Webull

- Public

- Acorns

The appeal: Sleek design, easy signup, fractional shares, zero commissions, social features.

The risks:

1. Gamification creates bad habits

Confetti animations, push notifications, and leaderboards trigger dopamine responses similar to casino games. This encourages frequent trading rather than long-term investing.

Research evidence: A 2021 study found Robinhood users trade 88% more frequently than traditional brokerage users, resulting in lower returns due to poor timing and overtrading[4].

2. Trading vs investing confusion

These apps make buying and selling feel like a game, not a wealth-building strategy. The ease of trading encourages speculation rather than patient compound growth.

Distinction:

- Trading: Frequent buying/selling to profit from short-term price movements

- Investing: Buying quality assets and holding for years to capture long-term growth

3. Limited educational resources

Most investing apps provide minimal financial education. They teach you how to buy, not what to buy or why certain strategies work.

4. Payment for order flow concerns

Many “free” apps sell your order information to high-frequency trading firms. While this doesn’t directly cost you money, it creates potential conflicts of interest.

When these apps work:

- You need fractional shares and zero commissions

- You have the discipline to ignore gamification features

- You use them like traditional brokerages (buy and hold)

- You supplement with quality financial education

Better alternatives: Fidelity, Charles Schwab, and Vanguard offer zero-commission trading, fractional shares, and robust educational resources without gamification tactics.

Takeaway: The platform matters less than your behavior. If an investing app helps you start but encourages overtrading, it’s causing more harm than good. Choose platforms that support evidence-based investing, not speculation.

Step-by-Step: How to Start Investing with $100 Today

This checklist removes decision paralysis. Follow these steps in order.

Step 1: Choose the Right Platform

Criteria for beginners:

- Zero account minimums

- Zero trading commissions

- Fractional share availability

- Educational resources

- User-friendly interface

Recommended platforms:

For hands-on investors:

- Fidelity: Excellent research tools, fractional shares, $0 minimums

- Charles Schwab: Strong customer service, comprehensive education

- Vanguard: Lowest-cost index funds, investor-focused philosophy

For hands-off investors:

- Betterment: Automated portfolios, $0 minimum, 0.25% fee

Decision framework:

- Want to pick investments yourself → Fidelity or Schwab

- Want automated management → Betterment

- Want the lowest possible fees → Vanguard

Step 2: Open a Brokerage Account

Account type: Start with a standard taxable brokerage account (not retirement accounts yet).

Why: Taxable accounts offer complete flexibility—withdraw anytime without penalties. Once you understand investing mechanics, then explore tax-advantaged accounts like Roth IRAs.

Required information:

- Social Security number

- Bank account for transfers

- Employment information

- Basic personal details

Time required: 10-15 minutes

Verification: Most platforms verify identity instantly, though some require 1-2 business days for bank linking.

Step 3: Fund Your Account

Transfer method: Link your bank account and initiate an electronic transfer.

Timeline: Transfers typically complete in 2-3 business days.

Pro tip: While waiting for funds to clear, use the time to research your first investment. Read about index funds, watch educational videos, and understand what you’re buying.

Step 4: Pick Your First Investment

Recommended first investment: A low-cost S&P 500 index ETF.

Specific choice: VOO (Vanguard S&P 500 ETF)

Why this exact fund:

- 0.03% expense ratio (lowest available)

- Tracks the 500 largest U.S. companies

- $500+ billion in assets (highly liquid)

- Decades of performance history

- Fractional shares available

How to buy:

- Search “VOO” in your brokerage platform

- Select “Buy”

- Choose “Dollar amount” (not share quantity)

- Enter “$100.”

- Review order (should show ~0.25 shares based on current price)

- Confirm purchase

Order type: Use “market order” for your first purchase. This executes immediately at the current price.

Confirmation: You’ll receive an email confirming your purchase and showing the exact share quantity based on the execution price.

Step 5: Automate Future Contributions

The most important step: Set up automatic monthly investments.

Why automation works:

- Removes emotional decision-making

- Creates dollar-cost averaging (buying at various prices)

- Builds wealth through consistency

- Prevents “waiting for the right time” paralysis

How to automate:

- Navigate to “Automatic investments” or “Recurring transfers.”

- Select VOO (or your chosen investment)

- Choose frequency: Monthly (recommended)

- Set amount: $100 or whatever fits your budget

- Select start date: Next month

Dollar-cost averaging explained: By investing the same amount monthly, you buy more shares when prices are low and fewer when prices are high. This averages your cost per share over time, reducing the impact of market volatility.

Example:

- Month 1: $100 buys 0.25 shares at $400/share

- Month 2: $100 buys 0.27 shares at $370/share (market dip)

- Month 3: $100 buys 0.24 shares at $420/share (market rise)

- Result: You own 0.76 shares with an average cost of $394.74/share

This strategy removes the impossible task of timing the market. You simply invest consistently regardless of market conditions.

Complete Checklist

Choose platform (Fidelity, Schwab, or Betterment)

Open brokerage account (15 minutes)

Link your bank account and transfer $100

Research while funds clear (2-3 days)

Buy first investment (VOO recommended)

Set up automatic monthly contributions

Ignore account for 6+ months (let compound growth work)

Takeaway: The hardest part is starting. These six steps transform you from someone who “wants to invest someday” to an actual investor building wealth through evidence-based strategies.

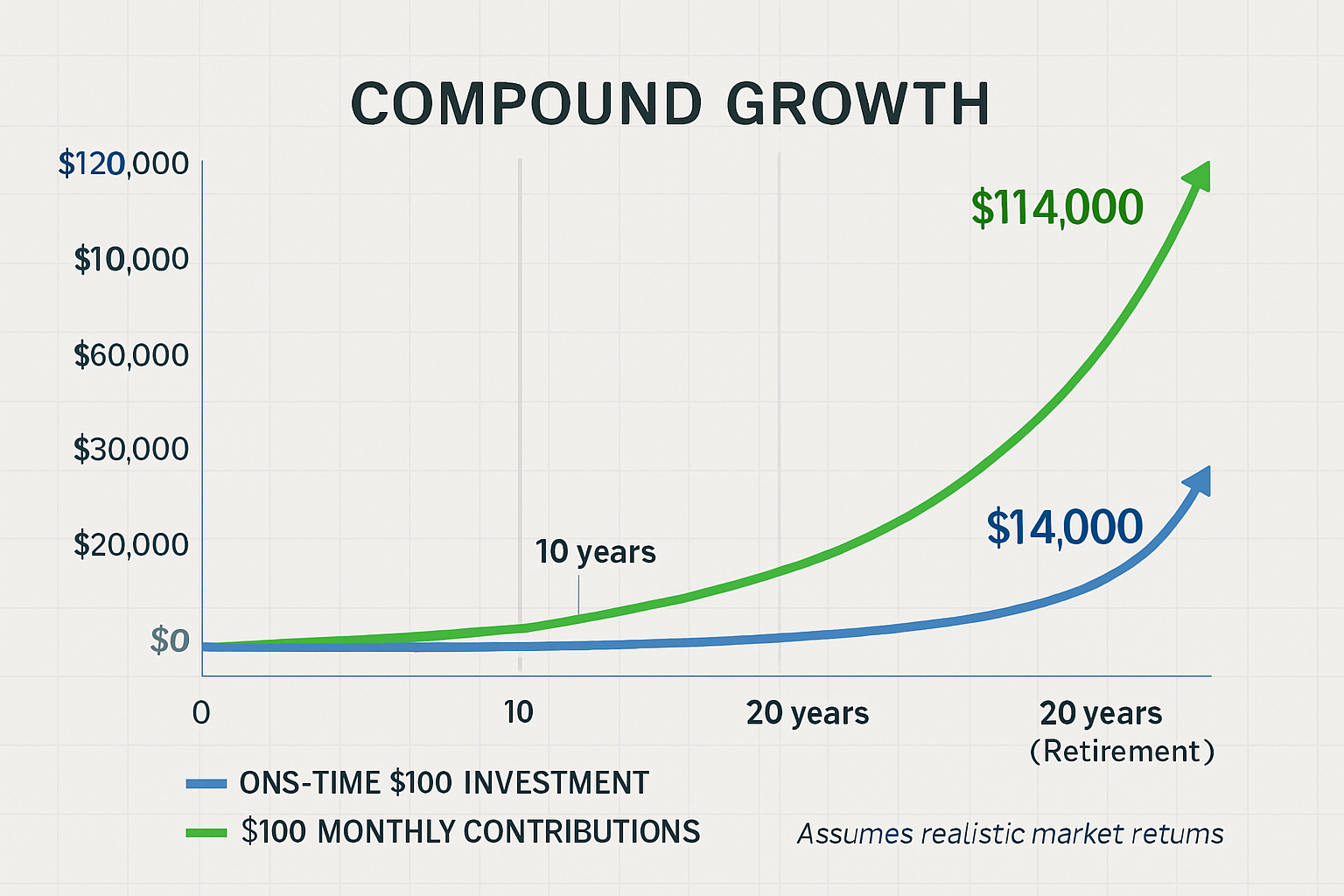

What $100 Invested Can Grow Into (Realistic Examples)

Understanding realistic expectations prevents disappointment and maintains long-term commitment.

Scenario 1: One-Time $100 Investment

Assumptions:

- Initial investment: $100

- Annual return: 10% (S&P 500 historical average)

- No additional contributions

- Dividends reinvested

Growth timeline:

| Years | Value | Total Gain |

|---|---|---|

| 5 | $161 | $61 (61%) |

| 10 | $259 | $159 (159%) |

| 20 | $673 | $573 (573%) |

| 30 | $1,745 | $1,645 (1,645%) |

| 40 | $4,526 | $4,426 (4,426%) |

Formula: Future Value = Present Value × (1 + rate)^years

Insight: Even without adding money, $100 becomes $4,526 over 40 years through compound growth alone. This demonstrates why starting early matters more than starting big.

Scenario 2: $100 Monthly Contributions

Assumptions:

- Initial investment: $100

- Monthly contribution: $100

- Annual return: 10%

- Time horizon: 30 years

- Total invested: $36,100

Growth timeline:

| Years | Value | Total Invested | Investment Gains |

|---|---|---|---|

| 5 | $7,808 | $6,100 | $1,708 |

| 10 | $20,655 | $12,100 | $8,555 |

| 20 | $75,603 | $24,100 | $51,503 |

| 30 | $217,132 | $36,100 | $181,032 |

Key observation: In year 30, your $100 monthly contribution adds $1,200 to your account, but compound growth adds approximately $19,700. Your money works harder than you do.

Formula: This uses the future value of an annuity formula:

FV = PMT × [((1 + r)^n – 1) / r]

Where:

- PMT = monthly payment ($100)

- r = monthly rate (0.10/12 = 0.00833)

- n = number of months (360)

Comparison insight:

- One-time $100: $1,745 after 30 years

- Monthly $100: $217,132 after 30 years

- Difference: $215,387 (124x more)

This proves consistency beats timing. Regular contributions harness compound growth’s full power.

The Compound Growth Curve

Years 1-10: Growth feels slow. Your contributions matter more than returns.

Years 11-20: Returns begin matching contributions. Momentum builds.

Years 21-30: Returns dwarf contributions. Compound growth dominates.

Years 31-40: Exponential acceleration. Your money generates more annual growth than you can contribute.

Behavioral insight: Most beginners quit during years 1-10 because progress feels insignificant. Understanding this curve prevents premature abandonment.

Realistic expectations:

- Year 1: Don’t expect life-changing wealth

- Year 5: You’re building the foundation

- Year 10: Momentum becomes visible

- Year 20+: Compound growth creates substantial wealth

According to Federal Reserve historical data, the S&P 500 has delivered 10.26% average annual returns from 1957-2024, including dividends[3]. However, this includes significant volatility—some years see 30% gains, others 30% losses.

Risk acknowledgment: Past performance doesn’t guarantee future results. Use 7-8% for conservative projections, 10% for historical average, and understand that actual results will vary significantly year-to-year.

The compound interest calculator guide provides tools to model your specific scenarios.

Takeaway: Small amounts invested consistently create substantial wealth over decades. The math behind money rewards patience and discipline more than large initial investments.

Common Mistakes Beginners Make with $100

Avoiding these errors increases your probability of long-term success.

Mistake #1: Day Trading

What it is: Buying and selling investments within hours or days to profit from short-term price movements.

Why beginners try it: Social media and YouTube highlight successful trades while hiding the 90% who lose money.

The reality:

- 90% of day traders lose money within the first year[5]

- Transaction costs and taxes eliminate most gains

- Requires full-time attention and advanced technical analysis

- Creates short-term capital gains (taxed at higher rates)

Math example:

- You buy $100 of stock at $10/share (10 shares)

- Stock rises 5% to $10.50

- You sell for $105 (before fees)

- Short-term capital gains tax (22% bracket): $1.10

- Net gain: $3.90 (3.9%)

Now compare to holding that same stock for 20 years at 10% annual growth: $673 (573% gain).

Opportunity cost: Day trading’s 3.9% gain costs you 569% in foregone long-term returns.

Takeaway: Trading is speculation, not investing. With $100, you can’t afford the learning curve that costs most day traders thousands in losses.

Mistake #2: Chasing Hype Stocks

What it looks like:

- Buying whatever’s trending on social media

- Following “hot tips” from influencers

- Investing in companies you don’t understand

- FOMO (fear of missing out) is driving decisions

Recent examples:

- Meme stocks (GameStop, AMC)

- Cryptocurrency speculation

- Penny stocks promoted in forums

- IPOs with massive hype but no profits

Why this fails:

- By the time you hear about it, sophisticated investors have already bought

- Hype creates inflated prices disconnected from value

- Volatility exceeds beginner risk tolerance

- No fundamental analysis supports the investment

Case study: GameStop (GME) in January 2021:

- Price on Jan 1: $17.25

- Peak on Jan 28: $347.51 (1,915% gain)

- Price on Feb 19: $40.59 (88% loss from peak)

Beginners who bought during the hype (around $300) lost 85%+ of their investment within weeks.

Alternative approach: Ignore trends. Buy boring, diversified index funds. Let compound growth create wealth while others chase excitement and lose money.

Behavioral finance insight: Humans are wired for recency bias—we assume recent trends continue forever. Markets exploit this cognitive error ruthlessly.

Mistake #3: Overchecking Your Account

The problem: Logging in daily (or hourly) to check investment performance creates emotional volatility that leads to poor decisions.

Psychological impact:

- Daily checking increases anxiety during normal market fluctuations

- Short-term losses feel more painful than long-term gains feel good (loss aversion)

- Frequent monitoring encourages panic selling during downturns

Research evidence: A study by Benartzi and Thaler found that investors who checked accounts frequently were more likely to sell during market dips and achieved lower long-term returns than those who checked quarterly or annually[6].

The math: Markets decline approximately 1 in every 4 days. If you check daily, you’ll see losses 25% of the time—even though annual returns are positive 75% of the time.

This creates a perception that investing is risky and volatile, when the actual long-term trend is reliably upward.

Recommended frequency:

- First month: Check once to confirm everything is working correctly

- Months 2-6: Monthly check-ins to build comfort

- After 6 months: Quarterly reviews (or less)

- Ideal: Annual reviews with rebalancing if needed

Action step: Delete investing apps from your phone’s home screen. Make checking your portfolio slightly inconvenient to reduce impulsive monitoring.

Mistake #4: Ignoring Fees

Why fees matter: A 1% difference in annual fees costs you 25% of your wealth over 40 years.

Fee comparison example:

Scenario A: Low-cost index fund (0.03% expense ratio)

- $100 monthly for 30 years at 10% gross return

- Fees reduce the return to 9.97%

- Final value: $216,360

Scenario B: High-fee mutual fund (1.00% expense ratio)

- $100 monthly for 30 years at 10% gross return

- Fees reduce the return to 9.00%

- Final value: $183,764

Difference: $32,596 lost to fees (15% of final value)

Fee types to understand:

- Expense ratio: Annual fee for fund management (0.03-2.00%)

- Trading commissions: Cost per transaction ($0-$10)

- Advisory fees: Robo-advisor or financial advisor charges (0.25-1.50%)

- Load fees: Sales charges on mutual funds (0-5.75%)

Rule: Keep total annual fees below 0.30% for optimal wealth building.

How to check fees:

- Look up your fund’s ticker symbol (e.g., VOO)

- Find “expense ratio” on the fund’s page

- Calculate annual cost: Investment amount × expense ratio

Example: $1,000 in VOO (0.03% expense ratio) = $0.30 annual fee

Takeaway: Fees compound negatively just like returns compound positively. Minimizing costs is one of the few guaranteed ways to improve investment performance.

Mistake #5: Stopping After the First Investment

The pattern: Beginners invest $100, feel accomplished, then never add more money.

Why does this happen:

- Lack of automation (manual investing requires ongoing discipline)

- Waiting to “save up more” before the next investment

- Forgetting about the account

- Getting discouraged by slow initial growth

The cost: Without regular contributions, you miss compound growth’s most powerful phase.

Comparison:

- $100 one-time, 30 years, 10% return = $1,745

- $100 one-time + $50 monthly, 30 years, 10% return = $109,311

- Difference: $107,566 (6,163% more)

Solution: Set up automatic monthly investments immediately after your first purchase. Even $25 monthly makes a substantial difference over decades.

The 50/30/20 rule budgeting helps identify money for consistent investing within your budget.

Takeaway: Your first $100 investment should be the beginning of a system, not a one-time event. Automation transforms good intentions into wealth-building reality.

Is Investing $100 Worth It?

The question reveals a misunderstanding about how wealth builds.

The Math Says Yes

Scenario: $100 monthly from age 25 to 65 (40 years)

- Total invested: $48,000

- Value at 10% annual return: $632,407

- Wealth created: $584,407 from $100 monthly investments

That’s more than half a million dollars in investment gains—from amounts most people spend on coffee and streaming services.

Comparison to waiting:

Person A: Starts investing $100 monthly at age 25

- Age 65 value: $632,407

Person B: Waits until age 35, invests $200 monthly (double the amount)

- Age 65 value: $474,970

Result: Person A has $157,437 more despite investing $24,000 less total. Starting 10 years earlier with half the monthly amount creates 33% more wealth.

This is the power of compound growth over time. The math doesn’t care about your feelings—it rewards early action.

The Psychology Matters More

Behavioral wealth building: The habit you create matters more than the initial amount.

Psychological benefits of starting with $100:

- Removes analysis paralysis: You learn by doing instead of endlessly researching

- Creates skin in the game: Real money invested makes you pay attention to financial education

- Builds confidence: Successfully investing $100 proves you can invest $1,000 or $10,000 later

- Establishes identity: You become “an investor” rather than someone who “wants to invest someday.”

Research insight: A study on habit formation found that small, consistent actions create stronger long-term behavior change than sporadic large actions[7]. Investing $100 monthly builds a wealth-building identity more effectively than waiting to invest $10,000 once.

The momentum principle: Starting creates psychological momentum that makes the second, third, and hundredth investment easier.

What $100 Won’t Do

Realistic expectations:

- Won’t replace your income within 5 years

- Won’t make you a millionaire in a decade

- Won’t eliminate the need for career development

- Won’t solve immediate financial emergencies

What $100 will do:

- Start compound growth working in your favor

- Build financial literacy through experience

- Create wealth-building habits

- Provide optionality in future decades

- Reduce financial stress about retirement

The Waiting Cost

Every month you delay costs you compound growth.

Example: Waiting one year to start investing $100 monthly:

- 30-year value if you start today: $217,132

- 29-year value if you wait 12 months: $197,690

- Cost of waiting: $19,442

That one year of delay costs you nearly $20,000 in future wealth. The “perfect time” to start doesn’t exist—the best time is now, the second-best time is today.

Takeaway: The question isn’t whether $100 is “worth it”—it’s whether you want to harness compound growth or let decades of potential wealth creation pass by. The math is clear: start now with what you have.

How to Start Investing with $100: Your Action Plan

Knowledge without action creates zero wealth. This section removes remaining barriers.

This Week’s Tasks

Day 1-2: Choose your platform

- Research Fidelity, Schwab, or Betterment

- Read reviews and compare features

- Make a decision (don’t overthink—all three are excellent)

Day 3: Open your account

- Gather required information (SSN, bank details)

- Complete application (15 minutes)

- Link bank account

Day 4-5: Fund your account

- Initiate $100 transfer

- While waiting, research VOO or your chosen first investment

- Read about index funds and diversification

Day 6: Make your first investment

- Once funds clear, buy your chosen ETF

- Start with VOO if uncertain

- Keep it simple—don’t second-guess

Day 7: Automate future contributions

- Set up a monthly automatic investment

- Choose an amount that fits your budget ($50-$200)

- Select the same investment for consistency

Next 6 Months

Month 1: Learn the basics

- Understand what you own (read about index funds)

- Familiarize yourself with your brokerage platform

- Resist the urge to check daily

Months 2-3: Expand knowledge

- Read about dividend investing

- Learn about diversification strategies

- Understand risk management

Months 4-6: Optimize your system

- Review your budget to potentially increase contributions

- Consider tax-advantaged accounts (Roth IRA) once you understand the basics

- Maintain automated investing discipline

Month 6: First portfolio review

- Check total value (should be around $600-700 with $100 monthly contributions)

- Review performance (don’t panic about short-term fluctuations)

- Adjust the contribution amount if your financial situation has changed

- Rebalance if needed (probably not necessary yet)

Year 1 Goals

Maintain consistent monthly contributions (most important)

Avoid emotional decisions during market volatility

Build financial literacy through reading and learning

Resist the temptation to day trade or chase hype

Increase the contribution amount if possible

Understand what you own and why you own it

Long-Term Mindset

Years 1-5: Focus on consistency and learning. Returns matter less than building the habit.

Years 5-10: Increase contributions as income grows. Consider diversifying beyond the S&P 500.

Years 10-20: Watch compound growth accelerate. Resist lifestyle inflation—invest raises and bonuses.

Years 20-30: Approach financial independence. Your money works harder than you do.

Years 30+: Enjoy the wealth you built through decades of disciplined investing.

The commitment: Investing $100 today commits you to a decades-long wealth-building journey. The amount doesn’t matter—the decision to start does.

Final action step: Close this article and open a brokerage account within the next hour. Thinking about investing creates zero wealth. Taking action today changes your financial future.

💰 $100 Investment Growth Calculator

See how your $100 can grow over time with compound interest

With consistent $100 monthly contributions, your money grows exponentially. The final years generate more wealth than all your contributions combined—that’s the power of compound growth!

Conclusion

The math behind money proves that how to start investing with $100 isn’t just possible—it’s a powerful wealth-building strategy when combined with consistency and patience.

Modern investing removed historical barriers that prevented small-dollar investors from accessing markets. Fractional shares, zero commissions, and robo-advisors democratized wealth building. The excuse that “you need money to make money” no longer holds.

The evidence-based approach:

- Start with low-cost index ETFs for instant diversification

- Automate monthly contributions to harness compound growth

- Avoid common mistakes (day trading, chasing hype, overchecking accounts)

- Maintain discipline through market volatility

- Let time and compound growth create substantial wealth

The realistic expectation: $100 won’t make you wealthy overnight, but $100 monthly for 30 years creates over $217,000 through the power of compound growth. That’s life-changing wealth built from amounts most people waste on subscription services and impulse purchases.

The psychological truth: Starting with $100 builds the wealth-building identity and habits that matter more than the initial amount. The first investment is the hardest—every subsequent investment becomes easier.

Your next step: Choose a platform, open an account, and invest your first $100 within the next 48 hours. The cost of waiting exceeds the risk of starting. Compound growth rewards action, not intention.

The question isn’t whether you can afford to start investing with $100. The question is whether you can afford not to.

Disclaimer

This article provides educational information about investing strategies and should not be considered personalized financial advice. Investment decisions should be based on individual financial circumstances, risk tolerance, and goals.

All investment involves risk, including the potential loss of principal. Historical returns do not guarantee future performance. The examples and calculations presented use historical average returns (10% annually for the S&P 500), which may not reflect future market conditions.

Before investing, consider:

- Your emergency fund status

- High-interest debt obligations

- Personal risk tolerance

- Investment time horizon

- Tax implications

The Rich Guy Math is an educational platform focused on financial literacy and data-driven insights. We do not provide personalized investment advice, tax guidance, or legal counsel. Consult qualified financial professionals for advice specific to your situation.

Securities investing involves market risk. Read all fund prospectuses and understand fee structures before investing. Past performance does not predict future results.

Author Bio

Max Fonji is the founder of The Rich Guy Math, a data-driven financial education platform dedicated to explaining the math behind money with precision and clarity. With a background in financial analysis and a commitment to evidence-based investing, Max translates complex financial concepts into actionable strategies for beginner and intermediate investors.

The Rich Guy Math focuses on teaching wealth-building fundamentals through numbers, logic, and historical data—helping readers understand not just what to do with money, but why certain strategies work based on mathematical principles and compound growth mechanics.

Max’s approach combines analytical rigor with educational warmth, making sophisticated financial concepts accessible without sacrificing accuracy. Every article demonstrates cause and effect, provides data to support claims, and builds reader confidence through understanding.

Connect with The Rich Guy Math for more data-driven financial insights, valuation principles, and evidence-based investing strategies.

References

[1] Federal Reserve Board. (2023). “Changes in U.S. Family Finances from 2019 to 2022.” Survey of Consumer Finances. https://www.federalreserve.gov/

[2] Federal Reserve Board. (2025). “Consumer Credit – G.19.” Federal Reserve Statistical Release. https://www.federalreserve.gov/

[3] Morningstar. (2024). “S&P 500 Index Historical Returns Analysis, 1957-2024.” Morningstar Direct Database. https://www.morningstar.com/

[4] Barber, B. M., Huang, X., Odean, T., & Schwarz, C. (2021). “Attention-Induced Trading and Returns: Evidence from Robinhood Users.” Journal of Finance, forthcoming.

[5] Securities and Exchange Commission. (2020). “Day Trading: Your Dollars at Risk.” SEC Investor Publications. https://www.sec.gov/

[6] Benartzi, S., & Thaler, R. H. (1995). “Myopic Loss Aversion and the Equity Premium Puzzle.” The Quarterly Journal of Economics, 110(1), 73-92.

[7] Lally, P., van Jaarsveld, C. H. M., Potts, H. W. W., & Wardle, J. (2010). “How are habits formed: Modelling habit formation in the real world.” European Journal of Social Psychology, 40(6), 998-1009.

Frequently Asked Questions

Is $100 enough to invest in the stock market?

Yes, $100 is sufficient to start investing in the stock market. Most modern brokerages offer fractional shares and zero account minimums, allowing you to buy portions of stocks and ETFs.

Investing $100 in an S&P 500 index ETF provides instant diversification across 500 companies. While $100 alone won’t create immediate wealth, consistently investing $100 per month can grow to over $217,000 in 30 years at historical average returns.

Can I lose all my money investing $100?

You can lose money investing, but losing 100% is extremely unlikely if you use diversified investments like index ETFs. Individual stocks can go to zero if a company fails, but diversified funds hold hundreds of companies.

The S&P 500 has never gone to zero, though it has experienced temporary declines of 30–50% during major recessions. Long-term investing and diversification significantly reduce the risk of permanent losses.

Should I invest $100 all at once or monthly?

For beginners, investing $100 monthly using dollar-cost averaging is often more effective than a single $100 investment. Monthly contributions reduce timing risk and take advantage of market fluctuations.

For example, investing $100 per month for 30 years at a 10% return grows to approximately $217,132, compared to just $1,745 from a one-time $100 investment. However, if you already have a lump sum, investing immediately often performs better over long periods.

What’s the safest investment for beginners?

Low-cost index ETFs that track the S&P 500 (such as VOO or SPY) are among the safest stock market investments for beginners. They offer broad diversification, low fees, and long-term historical returns around 10% annually.

For maximum safety with lower returns, high-yield savings accounts or U.S. Treasury bonds provide principal protection. The safest choice depends on your time horizon—stocks are safer for long-term goals, while cash equivalents suit short-term needs.

Can teens or students start investing with $100?

Yes, teens and students can start investing with $100. Minors must use a custodial account (UGMA or UTMA) opened by a parent or guardian, while students over 18 can open brokerage accounts independently.

Starting early dramatically increases compound growth potential. A 16-year-old investing $100 per month until age 65 could accumulate over $1 million at a 10% average annual return.

Is crypto a good idea with $100?

Cryptocurrency is generally not recommended for beginners investing $100 due to extreme volatility. Prices can swing 20–50% in short periods, making crypto highly speculative.

If you want exposure, limit crypto to no more than 5% of your portfolio after establishing a diversified stock foundation. For beginners, proven assets like index ETFs are a more reliable starting point.