Every January, the IRS announces new contribution limits that directly impact how much wealth Americans can build through tax-advantaged accounts. For 2025, these limits have increased across multiple retirement and savings vehicles, creating fresh opportunities to accelerate compound growth and reduce taxable income.

Understanding the IRS Contribution Limits 2025 isn’t just about knowing the numbers. It’s about recognizing the math behind money: every additional dollar contributed to a tax-advantaged account compounds tax-free or tax-deferred for decades, creating exponential differences in retirement wealth. The difference between maxing out contributions and falling short can mean hundreds of thousands of dollars over a 30-year career.

This guide breaks down every major contribution limit for 2025, explains the catch-up rules that reward older savers, and provides the data-driven insights needed to optimize your savings strategy. Whether you’re contributing to a 401(k), IRA, HSA, or SEP, you’ll find the exact figures, eligibility thresholds, and planning frameworks to make informed decisions.

Key Takeaways

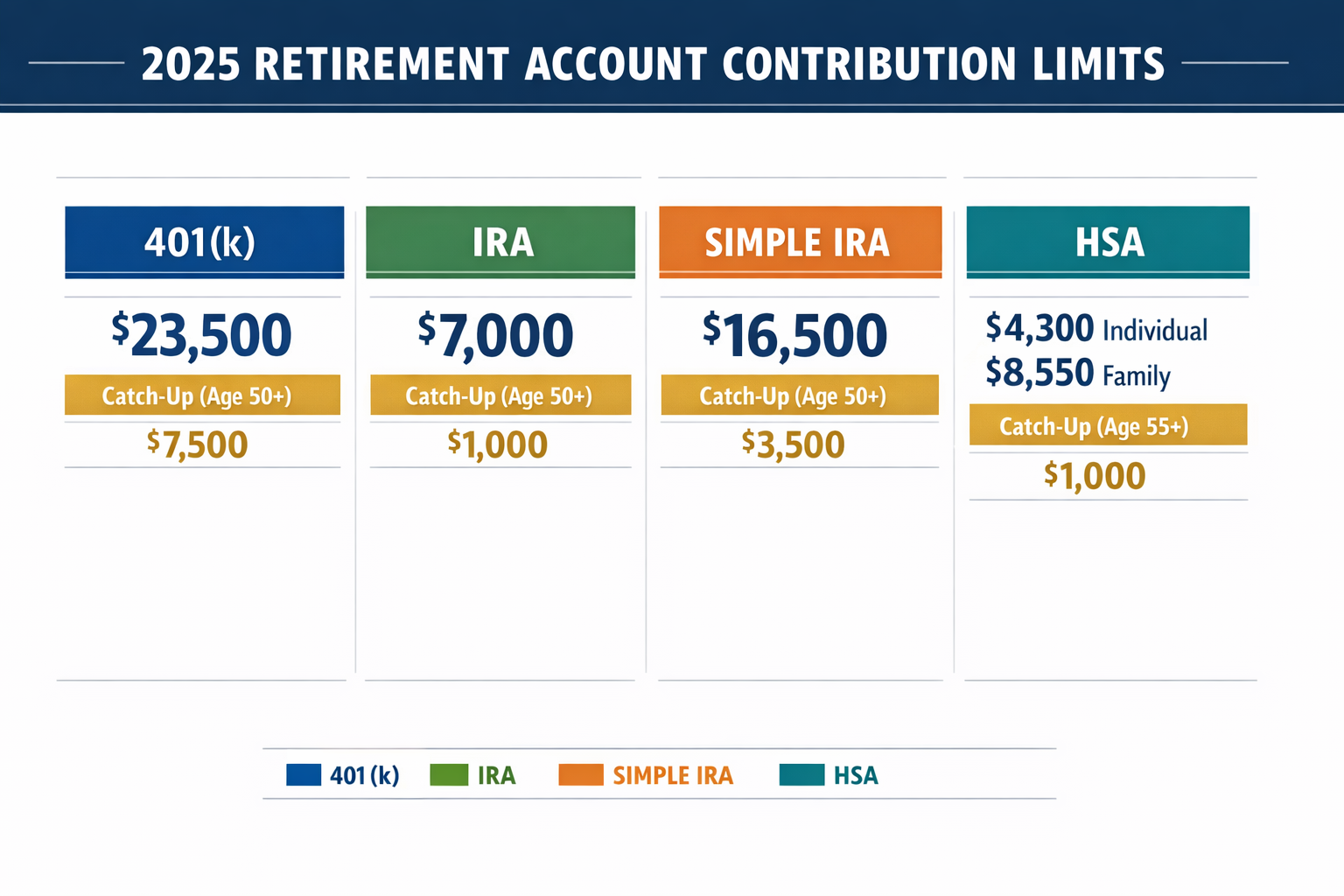

- 401(k) and 403(b) plans allow $23,500 in employee deferrals for 2025, with catch-up contributions of $7,500 for ages 50+ and a new $11,250 “super catch-up” for ages 60-63

- Traditional and Roth IRAs maintain a $7,000 limit with an additional $1,000 catch-up for those 50 and older

- HSA contributions reach $4,300 for individuals and $8,550 for families, offering triple tax advantages for qualified medical expenses

- SIMPLE IRA limits increase to $16,500 with enhanced catch-up provisions under SECURE 2.0

- Combined employer-employee 401(k) contributions can reach $70,000 in 2025 ($77,500 with standard catch-up or $81,250 with super catch-up)

2025 Retirement Account Contribution Limits at a Glance

The IRS adjusts contribution limits annually based on cost-of-living changes, ensuring retirement savers can maintain purchasing power as inflation rises. For 2025, most limits increased by $500 to $1,000 compared to 2024, reflecting the IRS’s commitment to supporting long-term wealth building through tax-advantaged accounts.

These limits represent the maximum amounts individuals can contribute to specific account types. Understanding each limit—and the corresponding catch-up provisions—enables strategic tax planning and maximizes the compound growth potential of retirement savings.

401(k), 403(b) & 457(b) Limits

Employee Salary Deferral Limit: $23,500

For 2025, employees can defer up to $23,500 of their salary into 401(k), 403(b), or governmental 457(b) plans. This represents a $500 increase from the 2024 limit of $23,000.

This elective deferral comes directly from paycheck deductions before income taxes are applied (for traditional contributions), reducing current taxable income while building retirement wealth. The math is straightforward: a worker in the 24% tax bracket who contributes the full $23,500 saves $5,640 in federal income taxes for the year.

Catch-Up Contributions (Age 50+): Additional $7,500

Workers aged 50 and older can contribute an additional $7,500 beyond the standard limit, bringing their total employee deferral to $31,000. This catch-up provision acknowledges that older workers often have higher earnings and fewer years until retirement, requiring accelerated savings.

Super Catch-Up (Ages 60-63): Additional $11,250

A new provision from the SECURE 2.0 Act allows employees aged 60 through 63 to contribute an even larger catch-up amount of $11,250 in 2025. This brings their maximum employee deferral to $34,750—the highest contribution opportunity in 401(k) history.

This super catch-up targets the critical pre-retirement years when many workers reach peak earnings and can most aggressively fund their retirement accounts.

Combined Employee-Employer Limit: $70,000

The total combined contributions from both employee deferrals and employer matching or profit-sharing cannot exceed $70,000 in 2025 (or $77,500 for those using the standard age 50+ catch-up, or $81,250 for those using the super catch-up)[1][2].

This combined limit matters most for highly compensated employees, business owners, and those with generous employer matching programs. Understanding this ceiling helps maximize total retirement contributions when employer contributions are substantial.

| Account Type | Standard Limit | Age 50+ Catch-Up | Age 60-63 Super Catch-Up | Total Maximum |

|---|---|---|---|---|

| 401(k) / 403(b) / 457(b) | $23,500 | +$7,500 | +$11,250 | $34,750 |

| Combined Employee + Employer | $70,000 | $77,500 | $81,250 | $81,250 |

Traditional & Roth IRA Limits

Standard Contribution Limit: $7,000

Both Traditional and Roth IRAs maintain a $7,000 contribution limit for 2025, unchanged from 2024. This limit applies to the total combined contributions across all IRA accounts; you cannot contribute $7,000 to a Traditional IRA and another $7,000 to a Roth IRA in the same year.

Catch-Up Contribution (Age 50+): Additional $1,000

Individuals aged 50 and older can contribute an extra $1,000, bringing their total IRA contribution to $8,000 for 2025. Unlike 401(k) plans, IRAs did not receive a super catch-up provision under SECURE 2.0.

The choice between Traditional and Roth contributions depends on current versus expected future tax rates. Traditional IRA contributions may be tax-deductible now (subject to income limits), while Roth contributions grow tax-free and face no required minimum distributions during the owner’s lifetime.

Income Phase-Out Ranges

Roth IRA contributions phase out for higher earners:

- Single filers: $150,000 – $165,000

- Married filing jointly: $236,000 – $246,000

Traditional IRA deductibility phases out for those covered by workplace retirement plans:

- Single filers: $79,000 – $89,000

- Married filing jointly: $126,000 – $146,000

These phase-outs create planning opportunities. High earners often use backdoor Roth conversion strategies to access Roth benefits despite income limitations.

| IRA Type | Under Age 50 | Age 50+ | Total Maximum |

|---|---|---|---|

| Traditional IRA | $7,000 | +$1,000 | $8,000 |

| Roth IRA | $7,000 | +$1,000 | $8,000 |

| Combined Total | $7,000 | $8,000 | $8,000 |

SIMPLE IRA & SIMPLE 401(k) Limits

Employee Deferral Limit: $16,500

SIMPLE (Savings Incentive Match Plan for Employees) retirement plans allow employee deferrals of up to $16,500 in 2025, representing a $500 increase from 2024’s $16,000 limit[1][5].

SIMPLE plans are designed for small businesses with 100 or fewer employees. They offer easier administration than traditional 401(k) plans but come with lower contribution limits.

Standard Catch-Up (Age 50+): Additional $3,500

Employees aged 50 and older can contribute an additional $3,500, bringing their total SIMPLE IRA contribution to $20,000 for 2025[1][5].

Super Catch-Up (Ages 60-63): Additional $5,250

Under SECURE 2.0 provisions, employees aged 60 through 63 can contribute an enhanced catch-up of $5,250 instead of the standard $3,500, allowing total contributions of $21,750[2].

Employer Contribution Requirements

Employers must either:

- Match employee contributions dollar-for-dollar up to 3% of compensation, OR

- Make a non-elective contribution of 2% of compensation for all eligible employees

This mandatory employer contribution distinguishes SIMPLE plans from Traditional and Roth IRAs, which have no employer component.

| SIMPLE Plan Type | Standard Limit | Age 50+ Catch-Up | Age 60-63 Super Catch-Up |

|---|---|---|---|

| SIMPLE IRA / 401(k) | $16,500 | +$3,500 ($20,000 total) | +$5,250 ($21,750 total) |

SEP IRA Limits

Contribution Limit: Lesser of 25% of Compensation or $70,000

Simplified Employee Pension (SEP) IRAs allow employers to contribute up to 25% of an employee’s compensation or $70,000, whichever is less, for 2025.

SEP IRAs are particularly attractive for self-employed individuals and small business owners because they:

- Allow much higher contributions than Traditional or Roth IRAs

- Require minimal administrative work

- Provide tax-deductible contributions for the business

For self-employed individuals, the calculation is slightly different due to how self-employment income is calculated. The effective contribution rate is approximately 20% of net self-employment income after deducting half of the self-employment tax.

No Employee Contributions

Unlike 401(k) or SIMPLE plans, employees cannot make their own contributions to SEP IRAs. All contributions come from the employer, making this an employer-funded retirement benefit.

Example Calculation:

An employee earning $100,000 could receive a SEP IRA contribution of up to $25,000 (25% × $100,000). A self-employed individual with $200,000 in net self-employment earnings could contribute approximately $40,000.

This makes SEP IRAs powerful tools for high-earning business owners seeking to maximize tax-deferred retirement savings while maintaining operational simplicity.

HSA Contribution Limits

Individual Coverage: $4,300

Health Savings Accounts (HSAs) allow individuals with high-deductible health plans to contribute $4,300 in 2025, up from $4,150 in 2024.

Family Coverage: $8,550

Families with high-deductible health plans can contribute up to $8,550 in 2025, an increase from $8,300 in 2024.

Catch-Up Contribution (Age 55+): Additional $1,000

Individuals aged 55 and older can contribute an extra $1,000 annually. Unlike retirement account catch-ups that begin at age 50, HSA catch-ups start at 55.

Triple Tax Advantage

HSAs offer three distinct tax benefits:

- Tax-deductible contributions reduce current taxable income

- Tax-free growth on investments within the account

- Tax-free withdrawals for qualified medical expenses

This triple tax advantage makes HSAs one of the most powerful wealth-building tools available. After age 65, HSA funds can be withdrawn for any purpose without penalty (though non-medical withdrawals are taxed as ordinary income), effectively functioning as an additional retirement account.

High-Deductible Health Plan Requirement

To contribute to an HSA in 2025, you must be enrolled in a high-deductible health plan (HDHP) with:

- Minimum deductible of $1,650 (individual) or $3,300 (family)

- Maximum out-of-pocket expenses of $8,300 (individual) or $16,600 (family)

For those who can afford to pay medical expenses out-of-pocket and invest HSA contributions, these accounts create exceptional long-term compound growth opportunities. Many financial planners recommend maximizing HSA contributions before even considering taxable investment accounts.

| Coverage Type | 2025 Limit | Age 55+ Catch-Up | Total Maximum |

|---|---|---|---|

| Individual | $4,300 | +$1,000 | $5,300 |

| Family | $8,550 | +$1,000 | $9,550 |

How 2025 Limits Compare to Prior Years

Understanding year-over-year changes in contribution limits reveals the IRS’s inflation adjustments and helps project future planning opportunities. The 2025 increases reflect moderate inflation and the IRS’s commitment to maintaining the real purchasing power of retirement contributions.

2024 → 2025 Changes

401(k) and Similar Plans:

- 2024: $23,000 → 2025: $23,500 (+$500)

- Age 50+ catch-up remained at $7,500

- Age 60-63 super catch-up: $11,250 (new in 2025)

IRA Accounts:

- Standard limit unchanged: $7,000

- Catch-up unchanged: $1,000

SIMPLE Plans:

- 2024: $16,000 → 2025: $16,500 (+$500)

- Standard catch-up unchanged: $3,500

- Age 60-63 super catch-up: $5,250 (new in 2025)

HSA Accounts:

- Individual: $4,150 → $4,300 (+$150)

- Family: $8,300 → $8,550 (+$250)

Combined Employer-Employee Limit:

- 2024: $69,000 → 2025: $70,000 (+$1,000)

The most significant change for 2025 is the introduction of super catch-up contributions for ages 60-63, a direct result of the SECURE 2.0 Act. This provision recognizes that the years immediately before retirement represent a critical window for wealth accumulation.

Cumulative Impact Over Time

These annual increases compound significantly over decades. A worker who contributed the maximum 401(k) amount every year from 2000 to 2025 would have deferred over $450,000 in employee contributions alone—not including employer matches or investment returns.

The math behind money shows that consistent maximum contributions, even with modest annual limit increases, create exponential wealth differences compared to partial contributions.

Looking Ahead to 2026 Adjustments

The IRS typically announces the following year’s contribution limits in late October or early November. Based on current inflation trends and historical patterns, reasonable projections for 2026 include:

Likely Scenarios:

- 401(k) limits: $24,000 – $24,500

- IRA limits: $7,000 – $7,500

- SIMPLE limits: $17,000 – $17,500

- HSA limits: $4,400 – $4,500 (individual)

These projections assume continued moderate inflation of 2-3% annually. Higher inflation would trigger larger increases; lower inflation might result in no changes to certain limits.

Planning Implication:

Don’t wait for next year’s increases to maximize current-year contributions. The time value of money means that contributing $23,500 today generates more compound growth than contributing $24,000 next year. Every month of tax-advantaged growth matters.

For those building comprehensive budgeting strategies, incorporating maximum retirement contributions should take priority over most discretionary spending.

Key Catch-Up Contribution Rules

Catch-up contributions represent the IRS’s acknowledgment that older workers need accelerated savings opportunities as retirement approaches. These provisions create meaningful differences in retirement readiness for those who maximize them.

Standard Age 50+ Catch-Ups

Why Age 50?

The IRS selected age 50 as the catch-up threshold because:

- Most workers reach peak earnings in their 50s

- Children often complete college, freeing up cash flow

- Retirement is 10-15 years away, requiring aggressive saving

- Compound growth still has time to work its exponential math

Available Catch-Ups by Account Type:

- 401(k)/403(b)/457(b): Additional $7,500

- IRA (Traditional/Roth): Additional $1,000

- SIMPLE IRA/401(k): Additional $3,500

- HSA: Additional $1,000 (begins at age 55)

Cumulative Impact Example:

A 50-year-old who maximizes 401(k) contributions ($31,000 including catch-up) for 15 years until age 65, assuming 7% average annual returns, would accumulate approximately $775,000 from contributions alone, plus employer matches.

Without the catch-up, contributing only $23,500 annually would yield approximately $590,000 under the same assumptions. The catch-up provision adds $185,000 in retirement wealth, a 31% increase.

This demonstrates the exponential power of maximizing every available contribution opportunity, particularly when combined with compound growth principles.

Super Catch-Ups for Ages 60-63

The SECURE 2.0 Innovation

The SECURE 2.0 Act, passed in late 2022, introduced enhanced catch-up contributions for employees aged 60, 61, 62, and 63. This provision recognizes that the immediate pre-retirement years represent the last opportunity for meaningful wealth accumulation.

Enhanced Limits:

- 401(k)/403(b)/457(b): Additional $11,250 (instead of $7,500)

- SIMPLE plans: Additional $5,250 (instead of $3,500)

Who Benefits Most:

High earners in their early 60s who:

- Delayed serious retirement saving until later in their careers

- Experienced career interruptions or setbacks

- Want to maximize tax-deferred growth in final working years

- Can afford to live on reduced take-home pay

Example Scenario:

A 60-year-old executive earning $200,000 annually can contribute:

- Employee deferral: $34,750

- Employer match (assuming 6%): $12,000

- Total annual contribution: $46,750

Over four years (ages 60-63), this totals $187,000 in contributions alone. With 7% returns and continued growth until age 70, this four-year contribution burst could grow to over $350,000.

The super catch-up essentially gives late-career savers a “second chance” to build retirement wealth, compensating for earlier years of lower contributions.

Roth vs Pre-Tax Implications

Catch-Up Contribution Tax Treatment

All catch-up contributions can be made on either a pre-tax (traditional) or after-tax (Roth) basis, depending on plan availability. This choice carries significant long-term implications.

Pre-Tax Catch-Ups:

- Reduce current taxable income

- Grow tax-deferred

- Taxed as ordinary income in retirement

- Subject to required minimum distributions (RMDs)

Roth Catch-Ups:

- Made with after-tax dollars (no current deduction)

- Grow completely tax-free

- Withdrawals are tax-free in retirement

- No RMDs during the owner’s lifetime (for Roth IRAs)

Decision Framework:

Choose pre-tax catch-ups if:

- Current tax bracket is high (32%+)

- Expect a lower tax bracket in retirement

- Need the current-year tax deduction

- Want to maximize current contributions through tax savings

Choose Roth catch-ups if:

- Current tax bracket is moderate (24% or lower)

- Expect the same or a higher bracket in retirement

- Want tax-free income flexibility in retirement

- Concerned about future tax rate increases

Many financial planners recommend a hybrid approach: splitting catch-up contributions between pre-tax and Roth to create tax diversification in retirement. This strategy provides flexibility to manage taxable income year-by-year after retirement.

For those implementing comprehensive tax planning strategies, the Roth vs traditional decision represents one of the most impactful choices in retirement planning.

Practical Planning Tips for IRS Contribution Limits 2025

Understanding the limits is only the first step. Implementing a strategic contribution plan that maximizes wealth building while maintaining cash flow requires careful planning and disciplined execution.

Maxing Out Contributions: Benefits & Strategies

Why Maximum Contributions Matter

The math behind money reveals that maximizing tax-advantaged contributions creates three compounding benefits:

- Immediate tax savings: Every pre-tax dollar contributed reduces current-year taxable income

- Tax-deferred or tax-free growth: Decades of compound returns without annual tax drag

- Forced savings discipline: Automatic paycheck deductions prevent lifestyle inflation

Prioritization Framework:

When you cannot max out all available accounts, prioritize in this order:

Tier 1: Employer Match

Contribute enough to your 401(k) to capture the full employer match. This represents an immediate 50-100% return on investment—impossible to replicate elsewhere.

Tier 2: HSA Maximum

If eligible, max out HSA contributions ($4,300 individual / $8,550 family). The triple tax advantage makes this the most tax-efficient account available.

Tier 3: 401(k) Maximum

Increase 401(k) contributions to the $23,500 limit (or higher with catch-ups). This provides the largest absolute tax-deferred contribution opportunity.

Tier 4: IRA Maximum

Contribute $7,000 to a Traditional or Roth IRA, choosing based on current vs. future tax rates.

Tier 5: Mega Backdoor Roth

If your 401(k) allows after-tax contributions and in-service conversions, contribute beyond the $23,500 limit up to the combined $70,000 ceiling, then convert to Roth.

Tier 6: Taxable Brokerage

Only after maximizing all tax-advantaged options should you invest in taxable accounts.

This hierarchy ensures every dollar receives maximum tax efficiency before moving to less favorable account types.

Automation Strategy:

Set up automatic contribution increases annually. Many 401(k) plans offer “auto-escalation” features that increase your contribution percentage by 1% each year. This painless approach gradually moves you toward maximum contributions without requiring active decisions.

For those following the 50/30/20 budgeting framework, retirement contributions should come from the 20% savings allocation before any other savings goals.

Income Phase-Outs for Roth IRA & Deductibility

Roth IRA Phase-Out Ranges (2025)

Roth IRA contribution eligibility phases out at these modified adjusted gross income (MAGI) levels:

Single Filers:

- Full contribution: MAGI below $150,000

- Partial contribution: MAGI $150,000 – $165,000

- No contribution: MAGI above $165,000

Married Filing Jointly:

- Full contribution: MAGI below $236,000

- Partial contribution: MAGI $236,000 – $246,000

- No contribution: MAGI above $246,000

Partial Contribution Calculation:

The reduced contribution limit equals:

- $7,000 × (Phase-out maximum – Your MAGI) / Phase-out range

Example: A single filer with MAGI of $157,500 can contribute:

- $7,000 × ($165,000 – $157,500) / $15,000 = $3,500

Traditional IRA Deductibility Phase-Outs

If you’re covered by a workplace retirement plan, Traditional IRA deduction eligibility phases out at:

Single Filers:

- Full deduction: MAGI below $79,000

- Partial deduction: MAGI $79,000 – $89,000

- No deduction: MAGI above $89,000

Married Filing Jointly:

- Full deduction: MAGI below $126,000

- Partial deduction: MAGI $126,000 – $146,000

- No deduction: MAGI above $146,000

Backdoor Roth Strategy

High earners above the Roth IRA income limits can use the “backdoor Roth” strategy:

- Contribute $7,000 to a Traditional IRA (non-deductible)

- Immediately convert the Traditional IRA to a Roth IRA

- Pay taxes only on any earnings between the contribution and the conversion

This legal workaround allows unlimited-income individuals to access Roth benefits. However, the “pro-rata rule” requires careful planning if you have existing pre-tax IRA balances.

Contribution Deadlines & Tax Filing Tips

401(k) and Similar Plan Deadlines

Employee deferrals to 401(k), 403(b), 457(b), and SIMPLE plans must be made during the calendar year (January 1 – December 31, 2025). There is no extension beyond December 31.

Planning Tip: If you’re behind on contributions in November or December, increase your deferral percentage to catch up. Some employers allow you to contribute up to 100% of your paycheck (up to the annual limit).

IRA Contribution Deadlines

Traditional and Roth IRA contributions for 2025 can be made until the tax filing deadline—typically April 15, 2026. This extended deadline provides flexibility to optimize contributions based on actual annual income.

Strategic Timing:

Many taxpayers wait until early 2026 to make their 2025 IRA contribution because:

- They know their exact 2025 income and tax bracket

- They can optimize Traditional vs. Roth based on the actual tax situation

- They have additional months to gather the funds

However, earlier contributions begin compounding sooner. A $7,000 IRA contribution made in January 2025 has 15 more months of growth potential compared to one made in April 2026.

HSA Deadlines

HSA contributions follow the same April 15 tax filing deadline as IRAs. Contributions made between January 1 and April 15, 2026, can be designated for either the 2025 or 2026 tax year[1].

Employer Contribution Deadlines

Employer contributions to SEP IRAs, profit-sharing plans, and employer matches can typically be made until the business tax return deadline, including extensions. For calendar-year corporations, this could extend to September or October of the following year.

Tax Form Reporting:

- Form 5498: Reports IRA contributions (issued by May following tax year)

- Form W-2: Shows 401(k) deferrals in Box 12

- Form 1099-SA: Reports HSA distributions

- Form 8889: Used to report HSA contributions and distributions on tax return

Understanding these deadlines enables strategic tax planning, particularly for those with variable income or year-end bonuses. For comprehensive guidance on managing tax-advantaged investment strategies, coordinating contribution timing with tax planning creates optimal outcomes.

Additional Account Types & Special Limits

Beyond the major retirement accounts, several specialized savings vehicles offer unique contribution limits and tax advantages for specific situations.

403(b) Plans — Identical to 401(k) Limits

403(b) plans, available to employees of public schools, certain nonprofits, and religious organizations, follow identical contribution limits to 401(k) plans:

- Employee deferral: $23,500

- Age 50+ catch-up: $7,500

- Age 60-63 super catch-up: $11,250

- Combined limit: $70,000

15-Year Rule:

403(b) plans offer a unique additional catch-up provision for employees with 15+ years of service with the same employer. These long-tenured employees can contribute up to an extra $3,000 annually, with a lifetime maximum of $15,000 in additional catch-ups[1][6].

This provision runs independently of age-based catch-ups, potentially allowing a 60-year-old with 15+ years of service to contribute $23,500 + $11,250 + $3,000 = $37,750.

457(b) Plans — Government & Nonprofit Deferred Compensation

Governmental and tax-exempt organization 457(b) plans allow $23,500 in deferrals for 2025, with similar catch-up provisions.

Unique Double-Limit Opportunity:

457(b) plans have separate contribution limits from 401(k)/403(b) plans. Employees who have access to both a 401(k) and a 457(b) can contribute the maximum to both accounts in the same year:

- 401(k) contribution: $23,500

- 457(b) contribution: $23,500

- Total employee deferrals: $47,000

This creates exceptional wealth-building opportunities for government employees and nonprofit workers with access to both plan types.

FSA Limits — Health & Dependent Care

Health FSA: $3,300

Health Flexible Spending Accounts allow $3,300 in contributions for 2025. These accounts provide pre-tax savings for qualified medical expenses but operate on a “use-it-or-lose-it” basis (though many plans offer a $640 carryover or 2.5-month grace period)[1].

Dependent Care FSA: $5,000

Dependent Care FSAs allow $5,000 annually for married couples filing jointly or single filers ($2,500 for married filing separately). These accounts cover qualified childcare and elder care expenses[1].

Strategic Consideration:

FSAs reduce taxable income but require careful planning to avoid forfeiting unused balances. Conservative estimates based on predictable expenses work best.

ABLE Accounts — Special Needs Savings

Standard Limit: $19,000

ABLE (Achieving a Better Life Experience) accounts allow individuals with disabilities to save up to $19,000 annually without jeopardizing eligibility for means-tested benefits like SSI or Medicaid[1].

Enhanced Limit for Working Beneficiaries: $34,060

ABLE account beneficiaries who work and don’t participate in employer retirement plans can contribute an additional amount equal to the lesser of their compensation or the poverty line for a one-person household, bringing the total potential contribution to $34,060[1].

These accounts grow tax-free and can be used for qualified disability expenses, providing crucial financial planning tools for individuals with special needs.

Maximizing Employer Contributions

While employee deferrals receive the most attention, employer contributions represent “free money” that dramatically accelerates retirement wealth accumulation.

Understanding Employer Match Formulas

Common Match Structures:

Dollar-for-Dollar up to X%:

Employer matches 100% of employee contributions up to a percentage of salary.

- Example: “100% match on first 6% of salary”

- Employee earning $100,000 who contributes 6% ($6,000) receives $6,000 match

Partial Match:

Employer matches a percentage of employee contributions.

- Example: “50% match on first 8% of salary”

- An employee earning $100,000 who contributes 8% ($8,000) receives $4,000 match

Tiered Match:

Different match percentages for different contribution levels.

- Example: “100% on first 3%, 50% on next 2%”

- An employee earning $100,000 who contributes 5% receives $4,000 match

Profit-Sharing:

Employer makes discretionary contributions based on company profitability, typically as a percentage of salary for all eligible employees.

The Cardinal Rule:

Always contribute at least enough to capture the full employer match. Failing to do so is equivalent to declining a guaranteed salary increase—a financial planning error with no justification.

Maximizing the Combined $70,000 Limit

The $70,000 combined employee-employer limit (or $77,500/$81,250 with catch-ups) creates planning opportunities for high earners and business owners.

After-Tax 401(k) Contributions:

Some plans allow after-tax (not Roth) contributions beyond the $23,500 employee deferral limit, up to the $70,000 combined ceiling. These contributions:

- Don’t reduce current taxable income

- Grow tax-deferred

- Can often be converted to Roth through in-service conversions

Mega Backdoor Roth Strategy:

- Max out regular 401(k): $23,500

- Receive employer match: ~$6,000

- Contribute after-tax dollars: $40,500 (to reach $70,000)

- Immediately convert after-tax contributions to Roth 401(k)

- Result: $40,500 in Roth contributions beyond normal Roth IRA limits

This advanced strategy requires specific plan features (after-tax contributions and in-service Roth conversions) but creates exceptional Roth wealth accumulation for high earners.

Business Owner Strategies:

Self-employed individuals and business owners can maximize the $70,000 limit through:

- Maximum employee deferral: $23,500

- Employer profit-sharing: Up to 25% of compensation

- Total potential: $70,000 (or higher with catch-ups)

For business owners implementing comprehensive capital allocation strategies, maximizing retirement contributions provides both personal wealth building and business tax deductions.

Strategic Contribution Planning Across Life Stages

Optimal contribution strategies evolve as income, expenses, and time horizons change throughout your career.

Early Career (Ages 22-35)

Financial Reality:

- Lower income

- Student loan debt

- Building an emergency fund

- Establishing a financial foundation

Contribution Strategy:

- Contribute enough for a full employer match (typically 3-6% of salary)

- Build a 3-6 month emergency fund in a high-yield savings account

- Pay off high-interest debt (credit cards, private student loans)

- Increase 401(k) to 10-15% once the emergency fund is complete

- Add Roth IRA contributions when cash flow allows

Roth vs. Traditional:

Early-career workers typically benefit from Roth contributions because:

- The current tax bracket is lower than the future expected bracket

- Decades of tax-free compound growth ahead

- Roth provides tax diversification for retirement

Even small contributions matter enormously at this stage. A 25-year-old who contributes just $5,000 annually to a Roth IRA for 40 years, earning 8% average returns, accumulates over $1.4 million, completely tax-free.

For those establishing foundational budgeting habits, treating retirement contributions as non-negotiable “bills” rather than optional savings creates lasting wealth-building discipline.

Mid-Career (Ages 35-50)

Financial Reality:

- Peak earning years begin

- Family expenses (housing, children, education)

- Increased financial complexity

- Retirement timeline becoming tangible

Contribution Strategy:

- Increase 401(k) to 15-20% of gross income

- Max out HSA if eligible ($4,300/$8,550)

- Max out Roth or Traditional IRA ($7,000)

- Consider a mega backdoor Roth if available

- Begin 529 college savings for children

Balance Competing Priorities:

Mid-career workers often face the “retirement vs. college savings” dilemma. The evidence-based answer: prioritize retirement.

Rationale:

- No loans exist for retirement

- Compound growth time is limited

- Children have more financial aid options than retirees

- You can’t borrow from future earnings in retirement

A balanced approach might allocate 15% to retirement and 5% to 529 plans, rather than splitting evenly.

Tax Optimization:

As income rises into higher brackets (24%+), the value of pre-tax 401(k) contributions increases significantly. A worker in the 32% bracket saves $7,520 in federal taxes by contributing the full $23,500.

Pre-Retirement (Ages 50-65)

Financial Reality:

- Peak earning years

- Children financially independent

- Mortgage potentially paid off

- Retirement 5-15 years away

- Maximum contribution capacity

Contribution Strategy:

- Max out all catch-up contributions ($7,500 401(k), $1,000 IRA)

- Utilize super catch-ups ages 60-63 ($11,250 401(k))

- Maximize HSA and invest (don’t spend) for future medical costs

- Consider Roth conversions in lower-income years

- Coordinate spousal contributions for dual-income couples

The Final Push:

Ages 50-65 represent the last opportunity to meaningfully impact retirement readiness. Maximum contributions during this 15-year window can add $500,000+ to retirement accounts.

Example Scenario:

A 50-year-old couple where both spouses max out their 401(k)s with catch-ups ($31,000 each) for 15 years:

- Total contributions: $930,000

- Value at 7% growth: ~$1.6 million

- With employer matches: ~$2 million+

This demonstrates why catch-up provisions exist; they enable late-career savers to achieve retirement security even if earlier contributions were modest.

For those implementing comprehensive retirement withdrawal strategies, the size of your retirement accounts directly determines sustainable withdrawal rates and retirement lifestyle.

Common Mistakes to Avoid

Understanding contribution limits is only valuable if you avoid the planning errors that undermine wealth accumulation.

Missing Employer Match

The Error:

Contributing less than the amount needed to receive the full employer match.

The Cost:

A $75,000 earner with a 6% match who contributes only 3% loses $2,250 annually in free money—$67,500 over 30 years, or approximately $260,000 with compound growth at 7%.

The Solution:

Calculate your employer’s match formula and contribute at least enough to maximize it. This takes priority over all other savings goals except high-interest debt repayment.

Contribution Timing Errors

The Error:

Making IRA contributions in April of the following year instead of January of the contribution year.

The Cost:

15 months of lost compound growth annually. Over 30 years, this timing difference can cost $50,000+ on a $7,000 annual contribution at 7% returns.

The Solution:

Contribute to IRAs in January rather than waiting until the April deadline. Set up automatic monthly contributions rather than lump-sum year-end deposits.

Ignoring HSA Investment Opportunity

The Error:

Treating HSAs as spending accounts rather than investment accounts, and using contributions immediately for current medical expenses.

The Cost:

Missing decades of triple-tax-advantaged compound growth—arguably the most valuable tax benefit in the entire tax code.

The Solution:

If financially able, pay medical expenses out-of-pocket and invest HSA contributions in low-cost index funds. After age 65, HSAs function like Traditional IRAs but with the added benefit of tax-free medical withdrawals.

A 35-year-old who maxes out HSA contributions ($4,300 annually) and invests for 30 years accumulates approximately $450,000 at 7% returns, all potentially tax-free if used for medical expenses.

Roth vs Traditional Miscalculation

The Error:

Making Roth contributions in high-income years (32%+ tax bracket) when Traditional contributions would provide larger tax savings.

The Cost:

Paying 32% taxes now to avoid potentially lower taxes in retirement, resulting in thousands in unnecessary tax payments.

The Solution:

Use Traditional (pre-tax) contributions when in high tax brackets (24%+) and Roth contributions when in lower brackets (22% or below). Consider tax diversification, splitting contributions between both types.

Decision Framework:

- Current bracket 32%+, expected retirement bracket 24% or lower → Traditional

- Current bracket 22% or lower, expected retirement bracket similar → Roth

- Current bracket 24%, uncertain future → Split 50/50

Exceeding Contribution Limits

The Error:

Contributing more than the annual limit, particularly when changing jobs mid-year and having multiple 401(k) plans.

The Cost:

6% annual penalty on excess contributions until corrected, plus potential double taxation.

The Solution:

Track contributions carefully when changing employers. The $23,500 401(k) limit applies to all 401(k) plans combined—you cannot contribute $23,500 to each employer’s plan in the same year.

If you exceed limits, contact your plan administrator immediately to withdraw excess contributions before the tax filing deadline to avoid penalties.

💰 2025 Retirement Contribution Calculator

Calculate your maximum contribution limits based on age and account type

Your 2025 Contribution Limits

Conclusion

The IRS Contribution Limits 2025 represent more than just regulatory caps—they define the boundaries of your tax-advantaged wealth-building opportunity. Understanding these limits and implementing a strategic contribution plan creates measurable differences in retirement readiness.

The math is unambiguous: maximizing contributions to tax-advantaged accounts, particularly early in your career, generates exponential compound growth that cannot be replicated through taxable investing. A 30-year-old who contributes the maximum to a 401(k) and IRA annually will accumulate hundreds of thousands of dollars more than someone making partial contributions—even if both earn identical investment returns.

The introduction of super catch-up contributions for ages 60-63 under SECURE 2.0 provides unprecedented opportunities for late-career savers to accelerate retirement funding. Combined with standard catch-ups and strategic Roth conversions, these provisions enable workers to achieve retirement security even if earlier savings were modest.

Your action plan:

- Calculate your current contribution rate across all retirement accounts

- Identify your employer match formula and ensure you’re capturing the full match

- Increase contributions by 1-2% annually until you reach maximum limits

- Prioritize HSA contributions if eligible for the triple tax advantage

- Review Roth vs. Traditional allocation based on current and expected future tax brackets

- Set up automatic increases to remove decision fatigue from the process

- Revisit your strategy annually when new limits are announced

The difference between financial security and financial stress in retirement often comes down to consistent execution of these fundamentals over decades. The contribution limits exist to encourage long-term savings, use them fully.

For those seeking to build comprehensive financial literacy and understand the mathematical principles underlying wealth accumulation, maximizing tax-advantaged contributions represents the single most impactful decision within your control.

Every dollar contributed today compounds for decades. Every limit maxed out creates exponential advantages. Every year of delay costs compound growth that can never be recovered.

The 2025 limits are set. The only question remaining is how fully you’ll use them.

References & Resources

[1] IRS. “401(k) limit increases to $23,500 for 2025, IRA limit remains $7,000.” IRS.gov, 2024. https://www.irs.gov/newsroom/401k-limit-increases-to-23500-for-2025-ira-limit-remains-7000

[2] Voya Financial. “2025 IRS contribution limits.” Voya.com, 2024. https://www.voya.com/page/2025-irs-contribution-limits

[3] IRS. “Cost-of-Living Adjustments for retirement plans and IRAs.” IRS.gov, 2024.

[4] SECURE 2.0 Act of 2022. Public Law 117-328, Division T.

[5] IRS. “SIMPLE IRA Plan contribution limits.” IRS.gov, 2024.

[6] IRS. “403(b) contribution limits.” IRS.gov, 2024.

Additional authoritative resources:

- U.S. Department of Labor: Employee Benefits Security Administration

- Financial Industry Regulatory Authority (FINRA): Retirement planning resources

- Social Security Administration: Retirement estimator tools

Author Bio

Max Fonji is the founder of The Rich Guy Math, a data-driven financial education platform that explains the mathematical principles underlying wealth building, investing, and risk management. With a background in financial analysis and a commitment to evidence-based education, Max translates complex financial concepts into clear, actionable insights for investors at all levels. His work focuses on helping readers understand not just what to do with money, but why it works, through numbers, logic, and compound growth principles.

Educational Disclaimer

This article provides educational information about IRS contribution limits and retirement planning strategies. It does not constitute personalized financial, tax, or investment advice.

Tax laws are complex and subject to change. Individual circumstances vary significantly based on income, tax bracket, state of residence, employer plan features, and personal financial goals. Before making contribution decisions, consult with qualified tax professionals and financial advisors who can evaluate your specific situation.

The contribution limits and tax treatment described reflect IRS guidance available as of publication. Always verify current limits and rules with official IRS publications or your tax advisor before making financial decisions.

Past performance and hypothetical examples do not guarantee future results. All investments carry risk, including potential loss of principal.

FAQs — IRS Contribution Limits 2025

What is the maximum 401(k) contribution for 2025?

The maximum employee deferral for 401(k) plans in 2025 is $23,500 for individuals under age 50.

- Ages 50–59 or 64+: additional $7,500 catch-up (total $31,000)

- Ages 60–63: additional $11,250 super catch-up (total $34,750)

The combined employee and employer contribution limit is $70,000, or $77,500 / $81,250 with catch-up contributions.

These limits apply per individual, not per plan. If you have multiple 401(k) accounts, your total employee deferrals across all plans cannot exceed $23,500.

Can I contribute to both a 401(k) and an IRA in 2025?

Yes. You can contribute to both accounts in the same year:

- 401(k): Up to $23,500 (plus catch-ups)

- IRA: Up to $7,000 (plus $1,000 catch-up)

Traditional IRA deductions may be limited if you’re covered by a workplace plan and your income exceeds IRS thresholds.

Roth IRA contributions also phase out at higher income levels. Even if deductions or direct Roth contributions are limited, contributions may still be possible through non-deductible or backdoor strategies.

What are catch-up contributions and who qualifies?

Catch-up contributions allow older workers to save more as they approach retirement.

Standard catch-up (age 50+):

- 401(k)/403(b)/457(b): $7,500

- IRA: $1,000

- SIMPLE: $3,500

- HSA (age 55+): $1,000

Super catch-up (ages 60–63):

- 401(k)/403(b)/457(b): $11,250

- SIMPLE: $5,250

Eligibility is based on your age during the calendar year—even a December 31 birthday qualifies.

How much can I contribute to an HSA in 2025?

- Individual coverage: $4,300

- Family coverage: $8,550

- Age 55+ catch-up: $1,000

You must be enrolled in an HSA-eligible high-deductible health plan (HDHP).

HSAs offer triple tax benefits: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses.

What happens if I exceed contribution limits?

401(k) excess contributions:

- Withdraw excess plus earnings before April 15

- If corrected on time: taxed once

- If not corrected: taxed twice plus possible penalties

IRA excess contributions:

- 6% excise tax annually until corrected

- Withdraw excess plus earnings to stop penalties

Track contributions carefully, especially when changing jobs mid-year.

When is the deadline for IRA contributions for 2025?

The deadline for 2025 IRA contributions is April 15, 2026.

Earlier contributions benefit from more compound growth, even though the deadline is later.

401(k) deadline: December 31, 2025

HSA deadline: April 15, 2026

Can married couples both max out retirement contributions?

Yes. Contribution limits apply per individual, not per household.

Working spouses can each max out their own 401(k), IRA, and other eligible accounts. Non-working spouses may still qualify for a Spousal IRA.

For HSAs, the family contribution limit applies per household, not per person.

Related posts:

What Is SmartPass? Raptor Digital Hall Pass Explained for K-12 Schools

What Is SmartPass? Raptor Digital Hall Pass Explained for K-12 Schools

What Is the 3x Rent Rule & How to Calculate It (With Examples)

What Is the 3x Rent Rule & How to Calculate It (With Examples)

Portfolio Income: Definition, Examples, Tax Rules, and Strategies

Portfolio Income: Definition, Examples, Tax Rules, and Strategies

Tax Filing: A Clear, Step-by-Step Guide for Stress-Free Taxes

Tax Filing: A Clear, Step-by-Step Guide for Stress-Free Taxes

Return on Assets (ROA): Definition, Formula & How to Improve It

Return on Assets (ROA): Definition, Formula & How to Improve It

How to Save Money Fast: A Smart Savings Plan That Actually Works

How to Save Money Fast: A Smart Savings Plan That Actually Works