In 2008, countless investors learned a brutal lesson about leverage when margin calls cascaded through the market, forcing the sale of assets at the worst possible moment. Margin investing amplifies both gains and losses, turning market movements into outsized portfolio swings. Understanding the math behind borrowed money separates confident investors from those who lose more than they started with.

Margin investing allows investors to borrow funds from their brokerage to purchase securities, effectively controlling a larger position than their cash alone permits. This leverage magnifies returns when positions appreciate, but it also accelerates losses and introduces the risk of margin calls when values decline.

The mechanics are straightforward: deposit cash, borrow against it, and invest the combined total. The consequences, however, demand precision and discipline.

Key Takeaways

- Margin investing uses borrowed money from your broker to purchase securities, typically allowing you to borrow up to 50% of the purchase price, effectively doubling your buying power

- Returns and losses are both amplified because gains and losses are calculated on the total position value, not just your initial capital. A 20% stock gain becomes a 40% return on your money with a 50% margin

- Margin calls occur when account value drops below the maintenance margin threshold (usually 25%), forcing you to deposit more cash or sell securities within hours to days

- Regulatory requirements protect and restrict investors through FINRA rules mandating a minimum $2,000 initial deposit and Federal Reserve limits capping initial borrowing at 50% of the purchase price

- Strategic use requires risk management, including position sizing, stop-loss orders, diversification, and maintaining cash reserves to avoid forced liquidation during market volatility

What Is Margin Investing and How Does It Work?

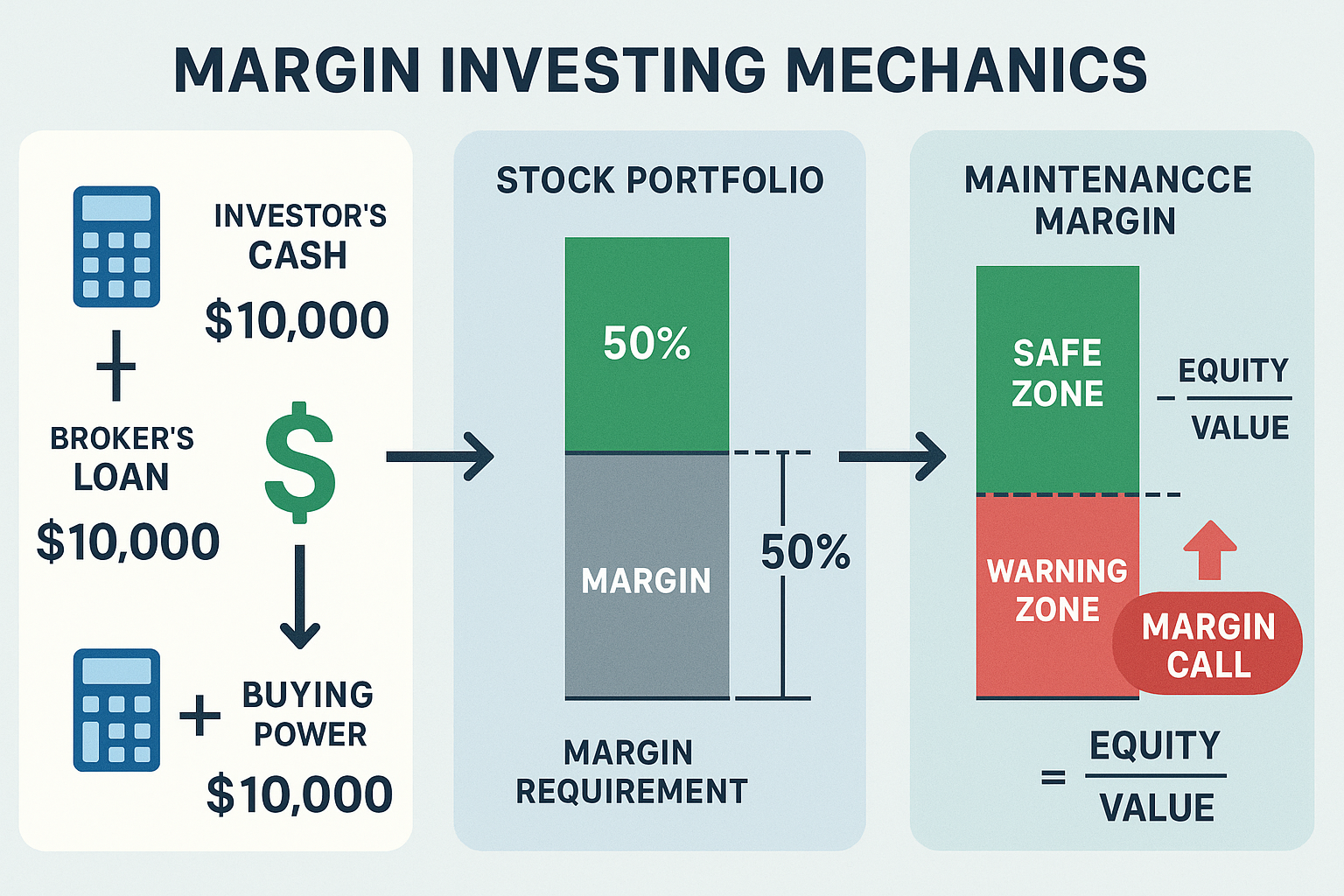

Margin investing transforms a standard brokerage account into a lending facility where the broker provides capital secured by your existing holdings. This arrangement creates leverage: the ability to control assets worth more than your available cash.

The Basic Margin Account Structure

A margin account differs fundamentally from a cash account. In a cash account, investors can only purchase securities with available funds. A margin account, by contrast, allows borrowing against the account’s equity.

Here’s the mathematical framework:

Buying Power = Cash + Borrowed Funds

If an investor deposits $10,000 and the broker permits a 50% initial margin, the total buying power becomes $20,000. The investor owns $10,000 worth of equity, and the broker lends the remaining $10,000.

The broker charges interest on the borrowed amount, typically ranging from 4% to 12% annually in 2025, depending on the amount borrowed and the brokerage firm. This interest expense reduces net returns and must be factored into all margin investment calculations.

Initial Margin Requirements

The Federal Reserve’s Regulation T permits investors to borrow up to 50% of a security’s purchase price. This means the initial margin requirement is 50%; investors must provide at least half the purchase price from their own funds.

Initial Margin Requirement = (Purchase Price × 50%) / Purchase Price = 50%

FINRA requires a minimum initial deposit of $2,000 or 100% of the purchase price, whichever is less. Many brokers establish higher minimums, often requiring $5,000 to $25,000 to open a margin account.

Not all securities qualify for margin trading. Penny stocks, certain IPOs, and over-the-counter bulletin board stocks typically cannot be purchased on margin due to their volatility and liquidity concerns.

Maintenance Margin and Account Monitoring

Once a position is established, the maintenance margin requirement takes effect. This represents the minimum account equity that must be maintained as a percentage of the total market value of securities.

FINRA sets the minimum maintenance margin at 25%, though many brokers require 30% to 40%.[3] This higher threshold provides the broker with a safety buffer against rapid market declines.

Account Equity = Market Value of Securities – Margin Loan

Maintenance Margin = Account Equity / Market Value of Securities

When the maintenance margin falls below the required threshold, the broker issues a margin call. The investor must either deposit additional cash, deposit additional securities, or sell existing positions to restore the account to the required level.

Brokers typically provide 24 to 72 hours to meet a margin call, though they reserve the right to liquidate positions immediately without notice if market conditions warrant.[5]

Understanding risk management becomes essential when using leverage, as positions can deteriorate faster than anticipated.

The Math Behind Margin Investing: Returns and Losses Amplified

Leverage transforms the return profile of any investment. The same percentage price movement generates vastly different outcomes depending on the amount of borrowed capital employed.

Calculating Leveraged Returns

Consider a straightforward example with 50% initial margin:

Scenario: Stock Purchase with Margin

- Initial capital: $10,000

- Margin loan: $10,000 (50% initial margin)

- Total position: $20,000

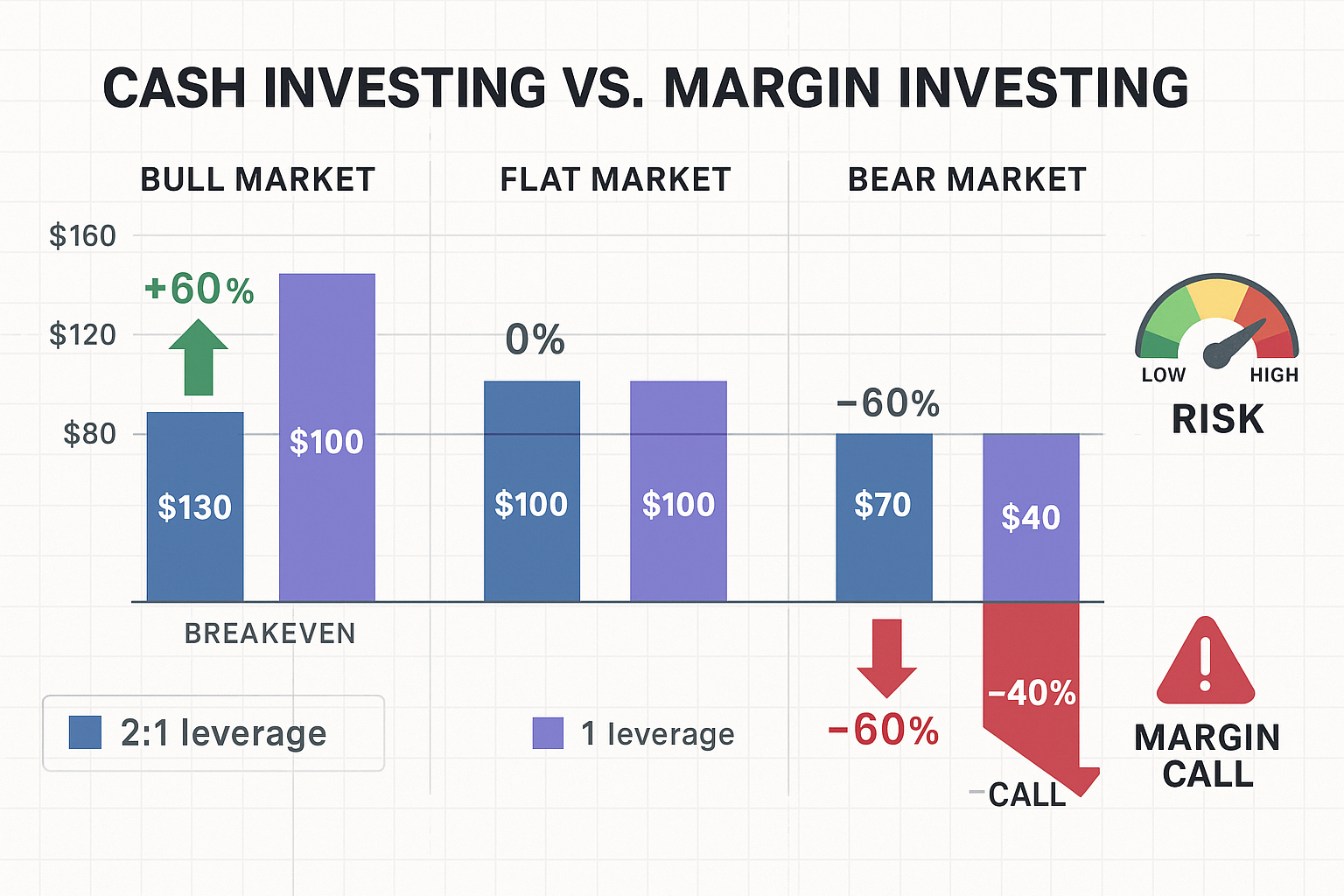

- Stock price increases: 20%

Without Margin:

- Return: $10,000 × 20% = $2,000 gain

- Return on investment: 20%

With Margin:

- Position value after gain: $20,000 × 1.20 = $24,000

- Margin loan repayment: $10,000

- Net equity: $24,000 – $10,000 = $14,000

- Profit: $14,000 – $10,000 = $4,000

- Return on investment: $4,000 / $10,000 = 40%

The 20% stock appreciation generated a 40% return on the investor’s capital, exactly double. This illustrates the fundamental appeal of margin investing.

However, this mathematical relationship works symmetrically in reverse.

The Downside: Amplified Losses

Using the same parameters with a 20% price decline:

Scenario: Stock Decline with Margin

- Position value after loss: $20,000 × 0.80 = $16,000

- Margin loan repayment: $10,000

- Net equity: $16,000 – $10,000 = $6,000

- Loss: $10,000 – $6,000 = $4,000

- Return on investment: -$4,000 / $10,000 = -40%

A 20% stock decline erases 40% of the investor’s capital. The leverage ratio determines the amplification factor, with 2:1 leverage (50% margin), returns and losses are doubled.

This mathematical reality creates asymmetric risk. While gains are amplified, losses can exceed the initial investment if positions decline substantially.

Interest Costs and Break-Even Analysis

Margin loans carry interest charges that accumulate daily. These costs reduce net returns and must be overcome before any position becomes profitable.

Annual Interest Cost = Margin Loan × Interest Rate

If the margin loan is $10,000 at 8% annual interest:

- Annual interest: $10,000 × 8% = $800

- Monthly interest: $800 / 12 = $66.67

For a position held for three months:

- Interest cost: $66.67 × 3 = $200

The investment must appreciate enough to cover both the interest expense and generate a positive return. This creates a higher break-even threshold compared to cash purchases.

Understanding absolute return versus relative return becomes critical when evaluating margin performance after accounting for interest costs.

Margin Calls: What Happens When Positions Move Against You

A margin call represents the broker’s demand for additional collateral when account equity falls below the maintenance margin requirement. This mechanism protects the broker from losses if the investor’s positions continue declining.

The Margin Call Trigger

Using the previous example with a 30% maintenance margin requirement:

Initial Position:

- Securities value: $20,000

- Margin loan: $10,000

- Account equity: $10,000

- Equity percentage: 50%

After Stock Decline to $15,000:

- Securities value: $15,000

- Margin loan: $10,000

- Account equity: $5,000

- Equity percentage: $5,000 / $15,000 = 33.3%

The account remains above the 30% maintenance margin; no margin call occurs.

After Further Decline to $13,000:

- Securities value: $13,000

- Margin loan: $10,000

- Account equity: $3,000

- Equity percentage: $3,000 / $13,000 = 23.1%

The equity percentage has fallen below the 30% maintenance margin. The broker issues a margin call requiring the investor to restore the account to the required level.

Calculating the Margin Call Amount

To determine the required deposit, calculate the equity needed to reach the maintenance margin:

Required Equity = Securities Value × Maintenance Margin Percentage

Required Equity = $13,000 × 30% = $3,900

Current Equity = $3,000

Margin Call Amount = $3,900 – $3,000 = $900

The investor must deposit $900 in cash or eligible securities to meet the margin call. Alternatively, the investor could sell $3,000 worth of securities, using the proceeds to reduce the margin loan.

Forced Liquidation Risks

If the investor fails to meet the margin call within the specified timeframe, the broker has the right to liquidate positions without further notice. The broker selects which securities to sell and at what price, prioritizing the firm’s risk management over the investor’s preferences.

This forced liquidation often occurs at the worst possible moment, during market declines when prices are depressed. Investors lose control over timing and may realize substantial losses that could have been temporary paper losses.

The psychological and financial impact of margin calls during market stress cannot be overstated. In 2020, during the COVID-19 market crash, investors faced margin calls as portfolios declined 30-40% in weeks, forcing sales at market lows.

Maintaining adequate emergency fund reserves separate from margin accounts provides a buffer to meet margin calls without forced liquidation.

Real-World Examples: Margin Investing in Action

Examining concrete scenarios illustrates how margin investing performs across different market conditions and investment approaches.

Example 1: Successful Leveraged Growth Investment

Investor Profile:

- Capital: $50,000

- Strategy: Purchase growth stocks with a 50% margin

- Total position: $100,000

- Margin loan: $50,000

- Interest rate: 7% annually

Year 1 Performance:

- Portfolio appreciation: 25%

- Ending value: $100,000 × 1.25 = $125,000

- Interest cost: $50,000 × 7% = $3,500

- Margin loan repayment: $50,000

- Net equity: $125,000 – $50,000 = $75,000

- Net profit: $75,000 – $50,000 – $3,500 = $21,500

- Return on initial capital: $21,500 / $50,000 = 43%

Without margin, the return would have been 25% minus no interest costs. The leverage added 18 percentage points of return after interest expenses.

This example demonstrates the ideal scenario, strong market performance combined with moderate interest costs generating substantial excess returns.

Example 2: Margin Call During Market Correction

Investor Profile:

- Capital: $30,000

- Strategy: Purchase dividend stocks with a 50% margin

- Total position: $60,000

- Margin loan: $30,000

- Maintenance margin: 30%

Market Correction:

- Portfolio decline: 35%

- New portfolio value: $60,000 × 0.65 = $39,000

- Margin loan: $30,000

- Account equity: $39,000 – $30,000 = $9,000

- Equity percentage: $9,000 / $39,000 = 23.1%

The account has fallen below the 30% maintenance margin, triggering a margin call.

Required equity: $39,000 × 30% = $11,700

Current equity: $9,000

Margin call amount: $11,700 – $9,000 = $2,700

The investor must deposit $2,700 or sell approximately $9,000 worth of securities to reduce the loan and restore the required margin.

If the investor lacks available cash and must sell, the realized loss becomes permanent. The securities sold at depressed prices cannot participate in any subsequent recovery.

This scenario illustrates the critical importance of maintaining cash reserves and understanding worst-case scenarios before employing leverage.

Example 3: Conservative Margin Use for Short-Term Opportunities

Investor Profile:

- Capital: $100,000

- Strategy: Use margin selectively for high-conviction short-term trades

- Typical margin usage: 20% of buying power

- Maintenance margin: 30%

Opportunity Trade:

- Identified undervalued stock post-earnings

- Margin used: $20,000 (20% of $100,000)

- Total position: $120,000

- Position size in target stock: $30,000

Two-Month Outcome:

- Target stock appreciation: 15%

- Position gain: $30,000 × 15% = $4,500

- Interest cost: $20,000 × 8% × (2/12) = $267

- Net profit: $4,500 – $267 = $4,233

The conservative margin usage (only 20% of available credit) provided substantial downside protection. Even a 30% portfolio decline would maintain equity above maintenance margin requirements.

This approach demonstrates disciplined margin use, selective deployment for specific opportunities rather than continuous maximum leverage.

Investors interested in building wealth systematically might also explore dollar cost averaging as a complementary strategy to reduce timing risk.

Risks of Margin Investing: What Every Investor Must Understand

Margin investing introduces multiple risk layers beyond standard equity investing. Recognizing these risks enables informed decision-making and appropriate risk management.

1. Magnified Losses and Capital Erosion

The primary risk is straightforward: leverage amplifies losses. A 50% decline in a fully margined position can eliminate 100% of invested capital.

Mathematical Reality:

- Initial capital: $25,000

- Margin loan: $25,000

- Total position: $50,000

- 50% market decline: $50,000 × 0.50 = $25,000

- Margin loan repayment: $25,000

- Remaining equity: $25,000 – $25,000 = $0

A 50% loss, while severe, is not unprecedented. Individual stocks regularly decline 50-70% during bear markets. Technology stocks in 2022 saw numerous examples of such declines.

2. Margin Call Timing and Forced Liquidation

Margin calls occur precisely when investors least want to sell, during market declines. This forced selling locks in losses and eliminates the opportunity to hold through recovery.

The 2008 financial crisis demonstrated this risk at scale. Investors who maintained cash accounts and held positions through the decline recovered fully by 2013. Those forced to liquidate due to margin calls realized permanent losses.

3. Interest Rate Risk and Carrying Costs

Margin interest rates vary with market conditions and can increase substantially during periods of rising interest rates. In 2022-2023, margin rates at major brokers increased from 4-6% to 8-12% as the Federal Reserve raised rates.

These higher costs reduce net returns and can transform marginally profitable positions into loss-makers. Long-term margin positions face compounding interest costs that erode returns over time.

4. Volatility Amplification

Leverage increases portfolio volatility. A portfolio with 2:1 leverage experiences approximately twice the daily price swings of an unleveraged portfolio.

This heightened volatility creates psychological stress and increases the probability of emotional decision-making during market turbulence. Investors may panic and sell at inopportune moments simply to reduce the discomfort of watching amplified losses.

Understanding the cycle of market emotions helps investors recognize and manage these psychological pressures.

5. Concentration Risk

Margin investing often leads to portfolio concentration, deploying leverage into a limited number of positions to maximize potential returns. This concentration eliminates diversification benefits and increases specific security risk.

If a single leveraged position declines substantially due to company-specific issues (earnings miss, regulatory problems, management changes), the impact on the overall portfolio is magnified.

6. Regulatory and Broker Policy Changes

Brokers can change margin requirements, interest rates, and eligible securities without advance notice. During market stress, brokers frequently increase maintenance margin requirements, potentially triggering margin calls even without price changes.

In March 2020, several brokers increased margin requirements on volatile securities from 30% to 50% or higher, forcing some investors to deposit additional capital or face liquidation despite no change in their positions’ values.

Smart Strategies for Using Margin Investing Responsibly

Margin investing becomes a powerful tool when used strategically rather than recklessly. These evidence-based approaches reduce risk while preserving leverage benefits.

Strategy 1: Conservative Position Sizing

Limit margin usage to 20-30% of available credit rather than maximizing leverage. This approach provides downside protection and reduces margin call probability.

Conservative Framework:

- Total capital: $50,000

- Maximum margin credit: $50,000

- Conservative margin usage: $50,000 × 25% = $12,500

- Total buying power utilized: $62,500

- Effective leverage: 1.25:1 instead of 2:1

This conservative leverage still amplifies returns but provides a substantial buffer against margin calls. The portfolio can decline approximately 40% before triggering a margin call at a 30% maintenance margin.

Strategy 2: Maintain Substantial Cash Reserves

Keep 15-25% of the portfolio in cash or cash equivalents specifically to meet potential margin calls. This reserve prevents forced liquidation during temporary market declines.

Cash Reserve Calculation:

- Invested capital: $40,000

- Margin loan: $20,000

- Cash reserve: $10,000 (25% of invested capital)

- Total account value: $50,000

If a margin call requires $5,000, the cash reserve covers it without forced selling. The investor maintains positions through volatility and participates in subsequent recovery.

This approach aligns with broader emergency fund principles—maintaining liquidity for unexpected requirements.

Strategy 3: Use Stop-Loss Orders

Implement stop-loss orders on margined positions to automatically exit if prices decline beyond acceptable thresholds. This approach limits maximum loss and prevents margin calls.

Stop-Loss Framework:

- Entry price: $100

- Maximum acceptable loss: 15%

- Stop-loss price: $100 × 0.85 = $85

- Position size: $30,000 (50% margin)

- Maximum loss: $30,000 × 15% = $4,500

The stop-loss automatically sells the position if the price reaches $85, limiting total loss to $4,500 regardless of further declines. This prevents the position from deteriorating to margin call levels.

Strategy 4: Margin for Short-Term Opportunities Only

Reserve margin for specific, time-limited opportunities rather than maintaining permanent leverage. This approach reduces interest costs and limits exposure to extended market declines.

Tactical Margin Use:

- Identify a specific catalyst (earnings, product launch, acquisition)

- Deploy margin for a 30-90 day position

- Exit position after the catalyst, regardless of the outcome

- Return to unleveraged portfolio

This tactical approach captures the benefits of leverage for high-conviction opportunities while avoiding the compounding risks of permanent leverage.

Strategy 5: Diversification Across Uncorrelated Assets

When using margin, diversify across asset classes and sectors with low correlation. This reduces the probability that multiple positions decline simultaneously, triggering margin calls.

Diversified Margin Portfolio:

- Large-cap growth stocks: 30%

- Dividend-paying value stocks: 25%

- REITs: 20%

- International equities: 15%

- Bonds: 10%

This diversification reduces portfolio volatility compared to concentrated positions, lowering margin call probability even with leverage.

Investors building diversified portfolios might explore the best ETFs to buy for efficient diversification.

Strategy 6: Monitor and Rebalance Regularly

Review margin positions daily or weekly, monitoring equity percentages and distance from maintenance margin thresholds. Proactive rebalancing prevents emergencies.

Monitoring Framework:

- Daily: Check equity percentage and margin call distance

- Weekly: Review position performance and interest costs

- Monthly: Rebalance to target leverage ratio

- Quarterly: Evaluate whether the margin remains appropriate

Regular monitoring enables gradual adjustments rather than crisis-driven decisions. If equity percentage approaches maintenance margin, the investor can reduce positions methodically rather than facing forced liquidation.

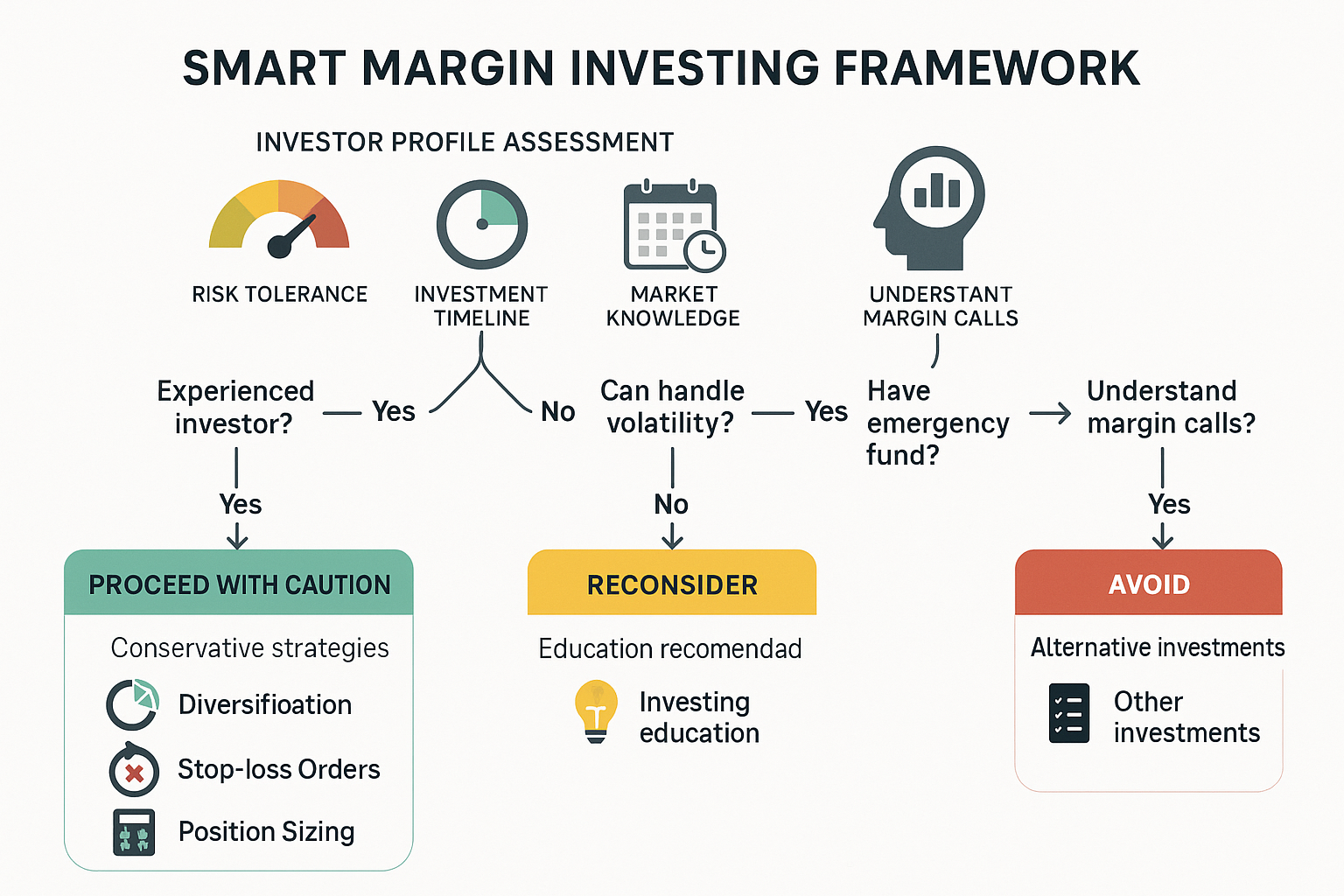

Who Should Consider Margin Investing?

Margin investing suits specific investor profiles while remaining inappropriate for others. Honest self-assessment prevents costly mistakes.

Suitable Investor Characteristics

Experienced Investors: Those with 5+ years of active investing experience who understand market cycles, volatility, and their own risk tolerance. Experience provides the context to recognize when leverage amplifies risk excessively.

High Risk Tolerance: Investors are comfortable with substantial portfolio volatility and potential for significant losses. Margin investing requires emotional resilience to maintain discipline during market stress.

Strong Financial Position: Individuals with substantial income, emergency reserves, and net worth beyond investment accounts. The ability to meet margin calls without financial hardship is essential.

Active Portfolio Management: Investors who monitor positions regularly and can respond quickly to changing conditions. Passive investors who check accounts quarterly are unsuitable for margin investing.

Specific Tactical Opportunities: Those using margin selectively for high-conviction, time-limited positions rather than permanent leverage. Strategic deployment differs fundamentally from continuous maximum leverage.

Unsuitable Investor Characteristics

Beginning Investors: Those with less than 3-5 years of investing experience lack the context to understand how leverage performs across market cycles. Starting with unleveraged investing builds essential experience.

Retirement-Focused Portfolios: Investors approaching or in retirement cannot afford the magnified losses that margin creates. Capital preservation becomes more important than amplified returns.

Insufficient Cash Reserves: Those without substantial emergency funds and liquidity to meet potential margin calls face forced liquidation risk. Margin investing requires financial buffers.

Emotional Decision-Makers: Investors who panic during market declines or make impulsive decisions will amplify these tendencies with leverage. Margin magnifies both market volatility and emotional responses.

Long-Term Buy-and-Hold Investors: Those following passive indexing strategies gain no benefit from margin. The interest costs and margin call risks contradict the buy-and-hold philosophy.

Investors focused on long-term wealth building might instead explore compound interest accounts that grow wealth without leverage risk.

Margin Investing vs Other Leverage Strategies

Margin investing represents one of several leverage approaches available to investors. Understanding alternatives enables informed strategy selection.

Margin vs Options Leverage

Options provide leverage through contracts rather than borrowed money. A call option controls 100 shares with capital far less than purchasing those shares on margin.

Comparison:

- Margin: Continuous interest costs, unlimited loss potential, margin call risk

- Options: No interest costs, limited loss (premium paid), defined expiration, time decay

Options suit short-term directional trades with defined risk, while margin works better for medium-term positions in quality securities.

Margin vs Leveraged ETFs

Leveraged ETFs use derivatives to provide 2x or 3x daily returns of an index without requiring a margin account.

Comparison:

- Margin: Flexible position sizing, any security, interest costs

- Leveraged ETFs: Fixed leverage ratio, index exposure only, daily reset issues, expense ratios

Leveraged ETFs experience value decay during volatile sideways markets due to daily rebalancing. Margin provides more control but requires active management.

Margin vs Portfolio Margin

Portfolio margin uses sophisticated risk modeling to determine margin requirements, often allowing higher leverage for diversified portfolios.

Comparison:

- Standard Margin: Fixed 50% initial and 25% maintenance requirements

- Portfolio Margin: Risk-based requirements, potentially lower margins for hedged positions, require $125,000 minimum

Portfolio margin suits sophisticated traders with complex strategies. Standard margin works for straightforward long positions.

Regulatory Framework and Investor Protections

Understanding the regulatory environment governing margin investing provides context for broker requirements and investor rights.

Federal Reserve Regulation T

Regulation T, established by the Federal Reserve, sets the initial margin requirement at 50% for most securities.[3] This regulation prevents excessive leverage, which contributed to the 1929 market crash.

The 50% requirement means investors must provide at least half the purchase price from their own funds. Brokers may require higher initial margins, but cannot go lower than 50% without Fed approval.

FINRA Rule 4210

FINRA (Financial Industry Regulatory Authority) Rule 4210 establishes margin account standards, including:

- Minimum initial deposit: $2,000 or 100% of purchase price, whichever is less[3]

- Minimum maintenance margin: 25% of current market value

- Broker authority to establish higher requirements

- Customer notification requirements for margin calls

This rule provides the framework that all U.S. brokers must follow, though individual firms often impose stricter standards.[6]

Broker-Specific Requirements

Individual brokers establish their own margin policies within regulatory minimums. Common broker requirements include:

- Higher initial deposits ($5,000-$25,000)

- Higher maintenance margins (30-40%)

- Restricted securities lists (stocks ineligible for margin)

- Concentrated position surcharges (higher margins for large positions in single securities)

- Volatility-based margin increases during market stress

Investors should review their specific broker’s margin agreement to understand the exact requirements and broker rights.

Investor Rights and Protections

While margin accounts involve borrowing, investors retain certain protections:

- Right to notification before forced liquidation (though not guaranteed during extreme volatility)

- Right to choose which securities to sell to meet margin calls (if time permits)

- Right to dispute margin interest calculations

- SIPC protection for account assets (though not protection against investment losses)

Understanding these rights enables more effective communication with brokers during margin-related situations.

📊 Margin Investing Calculator

(+30% gain)

(0% change)

(-30% loss)

Alternatives to Margin Investing for Amplifying Returns

Investors seeking enhanced returns without margin risks can explore several alternative strategies that provide different risk-reward profiles.

Index Fund Investing with Consistent Contributions

Rather than using leverage, investors can amplify returns through consistent contributions and compound growth over extended periods. This approach eliminates interest costs and margin call risks while building substantial wealth.

A $500 monthly contribution to an S&P 500 index fund averaging 10% annual returns grows to approximately $380,000 over 20 years—without any leverage risk. This dollar cost averaging approach provides market exposure with built-in volatility reduction.

Dividend Growth Investing

Dividend growth stocks provide increasing income streams that compound over time. Reinvesting dividends creates a form of organic leverage—using the investment’s own returns to purchase additional shares.

A portfolio of dividend aristocrats with 3% initial yield and 7% annual dividend growth doubles its income every 10 years. After 20 years, the yield on original cost exceeds 12%, creating substantial cash flow without borrowing.

Tax-Advantaged Account Maximization

Maximizing contributions to 401(k), IRA, and HSA accounts provides tax leverage—reducing current taxes while enabling tax-deferred or tax-free growth. The tax savings effectively amplify returns without market risk.

A $6,500 IRA contribution for someone in the 24% tax bracket saves $1,560 in current taxes, a guaranteed 24% return before any investment gains. Over decades, tax-deferred compounding significantly exceeds the benefit of modest leverage.

Real Estate Investment Trusts (REITs)

REITs provide exposure to leveraged real estate portfolios without individual investors needing to borrow. The REIT itself employs leverage, passing through the benefits while professional management handles the risks.

REITs typically operate with 30-50% loan-to-value ratios, providing moderate leverage with diversification across multiple properties. Investors gain leveraged real estate exposure through simple stock purchases.

Growth Stock Concentration

Rather than leveraging broad market exposure, investors can concentrate portfolios in high-growth sectors or companies. This approach increases potential returns through selection rather than borrowing.

A concentrated portfolio of 10-15 carefully researched growth stocks can significantly outperform broad indices without leverage costs or margin call risks. The concentration itself provides return amplification through higher volatility and growth potential.

Conclusion: Using Margin Investing Wisely in 2025

Margin investing transforms capital efficiency, enabling investors to control larger positions and potentially amplify returns. The mathematical reality is straightforward: leverage magnifies both gains and losses proportionally to the amount borrowed.

The difference between successful margin use and catastrophic losses lies in discipline, risk management, and honest self-assessment. Conservative position sizing, substantial cash reserves, stop-loss protection, and regular monitoring create the framework for responsible margin use.

For most investors, particularly those building long-term wealth, unleveraged investing through consistent contributions to diversified portfolios provides superior risk-adjusted returns without the stress and complexity of margin management. The compounding of returns over decades, enhanced by dividend reinvestment and tax-advantaged accounts, builds substantial wealth without borrowing.

For experienced investors with specific tactical opportunities, high risk tolerance, and strong financial positions, selective margin use can enhance returns when deployed strategically. The key is treating margin as a tool for specific situations rather than a permanent portfolio feature.

Next Steps:

- Assess your risk tolerance honestly using historical market scenarios—could you maintain discipline during a 40% portfolio decline?

- Build substantial cash reserves equal to 15-25% of your investment capital before considering margin

- Start with conservative leverage if you proceed—use only 20-30% of available margin credit initially

- Implement stop-loss orders on all margined positions to define maximum acceptable losses

- Monitor positions daily and maintain distance from maintenance margin thresholds

- Consider alternatives, including index fund investing, dividend growth strategies, and tax-advantaged account maximization

The math behind margin investing is precise and unforgiving. Understanding that math, respecting the risks, and implementing disciplined strategies separates confident investors from those who learn expensive lessons during market stress.

References

[1] Federal Reserve Board. (2025). “Regulation T: Credit by Brokers and Dealers.” Federal Reserve System.

[2] Financial Industry Regulatory Authority (FINRA). (2025). “Margin Account Requirements.” FINRA Investor Education.

[3] Investopedia. (2025). “Margin Trading: How It Works, Risks, and Benefits.” Investopedia Financial Education.

[4] Securities and Exchange Commission (SEC). (2025). “Investor Bulletin: Understanding Margin Accounts.” U.S. Securities and Exchange Commission.

[5] FINRA. (2025). “Margin Calls: What Happens When Your Account Is Underfunded.” FINRA Investor Alerts.

[6] FINRA. (2025). “Rule 4210: Margin Requirements.” FINRA Rulebook.

[7] Federal Reserve Bank of New York. (2025). “Historical Margin Debt Statistics.” Federal Reserve Economic Data.

[8] CFA Institute. (2025). “Leverage and Portfolio Management.” CFA Program Curriculum.

[9] U.S. Securities and Exchange Commission. (2025). “Margin Account Disclosure Statement.” SEC Investor Publications.

Author Bio

Max Fonji is the founder of The Rich Guy Math, a data-driven financial education platform dedicated to teaching the mathematical principles behind wealth building. With a background in economic analysis and a passion for evidence-based investing, Max translates complex financial concepts into clear, actionable insights. His work focuses on helping investors understand the cause-and-effect relationships that drive investment returns, risk management, and long-term wealth accumulation.

Educational Disclaimer

This article is provided for educational and informational purposes only and does not constitute financial, investment, or legal advice. Margin investing involves substantial risks, including the potential for losses exceeding your initial investment. The examples and scenarios presented are hypothetical and provided for illustration purposes only; actual results may vary based on market conditions, timing, and individual circumstances.

Before engaging in margin trading, investors should carefully review their broker’s margin agreement, understand all fees and interest charges, and honestly assess their risk tolerance and financial capacity to meet potential margin calls. Consider consulting with qualified financial advisors, tax professionals, and legal counsel before making margin investment decisions.

Past performance does not guarantee future results. All investments carry risk, and leveraged investments carry amplified risk. The Rich Guy Math and its authors do not accept liability for any financial losses or damages resulting from the use of information presented in this article.

Frequently Asked Questions About Margin Investing

What is the minimum amount needed to open a margin account?

FINRA requires a minimum initial deposit of $2,000 or 100% of the purchase price, whichever is less. However, most brokers set higher minimums—often between $5,000 and $25,000—to ensure investors have enough capital to manage margin risks effectively.

Can I lose more money than I invest when using margin?

Yes. Margin investing can create losses greater than your initial investment. A steep decline in a margined position can erase your equity and still leave you owing the margin loan plus interest. In highly leveraged scenarios, losses can exceed 100% of your starting capital.

How quickly must I respond to a margin call?

Brokers generally allow 24 to 72 hours to meet a margin call, but timelines vary. During volatile markets, brokers may require immediate action or liquidate positions without warning. Margin agreements permit brokers to sell securities at their discretion to protect the firm’s capital.

Does margin interest compound?

Yes. Margin interest typically compounds daily on the outstanding loan balance. This daily accumulation increases the total amount owed and reduces net returns, especially for long-term margin positions.

What happens if I can’t meet a margin call?

If you cannot provide additional cash or securities, your broker will liquidate positions in your account. You do not choose which positions are sold or when. The broker’s priority is protecting the loan, not optimizing your returns.

Are there tax implications for margin interest?

Margin interest may be tax-deductible as investment interest expense, subject to limits. The deduction cannot exceed your net investment income. Because tax rules vary, investors should consult a qualified tax professional.

Can I use margin to buy any stock?

No. Brokers restrict margin eligibility. Penny stocks, OTC stocks, certain IPOs, and highly volatile securities are usually excluded. Even within eligible securities, brokers may assign higher margin requirements to concentrated or risky positions.

Related posts:

Dividend Portfolio: How to Build One for Steady Passive Income

Dividend Portfolio: How to Build One for Steady Passive Income

Why Should You Invest? The Benefits of Long-Term Investing Explained

Why Should You Invest? The Benefits of Long-Term Investing Explained

Types of Investors: Understanding Who Drives the Market

Types of Investors: Understanding Who Drives the Market

What Is a Hedge Fund? How It Works, Strategies, and Risks Explained

What Is a Hedge Fund? How It Works, Strategies, and Risks Explained

S&P 500 Total Return 2024: Full Performance Breakdown

S&P 500 Total Return 2024: Full Performance Breakdown

Robinhood vs Fidelity: Which Brokerage Is Better for Investors?

Robinhood vs Fidelity: Which Brokerage Is Better for Investors?