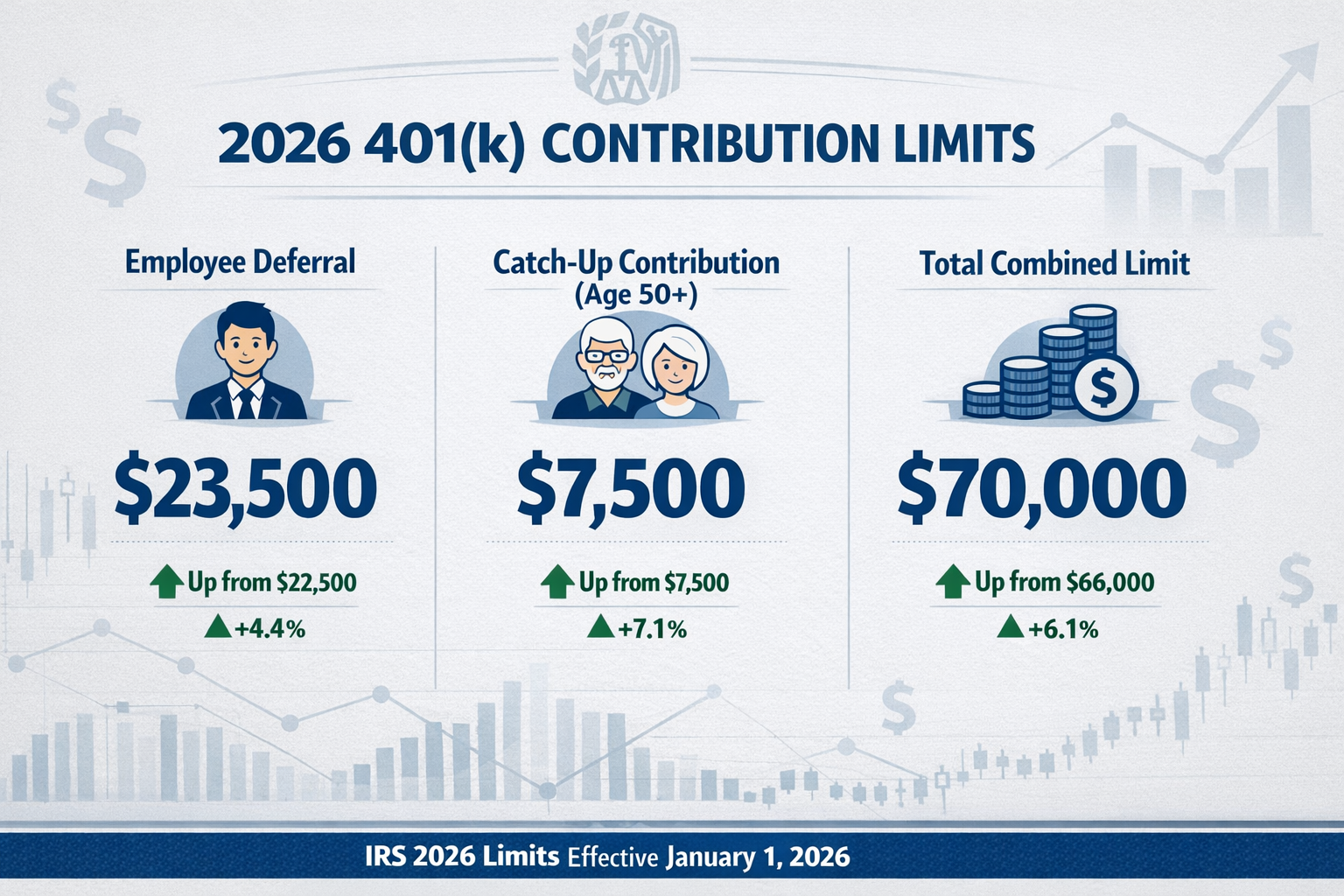

The 2026 max 401k contribution limit is $23,500 for employee deferrals, with an additional $7,500 catch-up contribution allowed for individuals age 50 and older. This brings the total potential contribution to $31,000 for eligible savers, while the combined employee-employer limit reaches $70,000 ($77,500 with catch-up contributions).

Understanding these limits is critical for retirement planning. The IRS adjusts these caps annually based on cost-of-living changes, and 2026 brings modest increases that directly impact how much you can shelter from taxes while building long-term wealth.

The math is simple: maximize your contributions early, compound growth does the heavy lifting, and you build financial independence through systematic, tax-advantaged savings.

Key Takeaways

- Employee deferral limit for 2026: $23,500 (up from $23,000 in 2025)

- Catch-up contribution for age 50+: Additional $7,500, totaling $31,000 maximum

- Total contribution cap (employee + employer): $70,000 ($77,500 with catch-up)

- No income limits apply to 401(k) contributions, unlike Roth IRAs

- Both Traditional and Roth 401(k) share the same contribution limits

What is the 401(k) Contribution Limit for 2026?

The 401k contribution limit refers to the maximum amount you can contribute to your workplace retirement account in a given tax year. The IRS sets these limits and adjusts them annually to account for inflation and changes in the cost of living.

For 2026, the employee deferral limit is $23,500. This is the amount you contribute directly from your paycheck through salary deferrals.

There are three distinct contribution caps to understand:

Employee Deferral Limit: This is the money you contribute from your salary. For 2026, it’s $23,500. This applies whether you choose a Traditional 401(k) (pre-tax) or a Roth 401(k) (after-tax).

Employer Match: Your employer may contribute to your 401(k) through matching or profit-sharing. These contributions do not count against your $23,500 employee limit, but they do count toward the total contribution cap.

Total Contribution Cap: The combined limit for employee deferrals plus employer contributions is $70,000 in 2026 ($77,500 if you’re 50 or older and making catch-up contributions).

The distinction matters because you control your employee deferrals, but employer contributions depend on your company’s plan design and matching formula.

Most employers match a percentage of your contributions—commonly 50% to 100% of the first 3-6% of your salary. This is free money that accelerates your compound interest growth and should always be prioritized in your savings strategy.

2026 401k Contribution Limits Table

| Contribution Type | 2026 Limit |

|---|---|

| Employee Deferral (under 50) | $23,500 |

| Catch-Up Contribution (age 50+) | $7,500 |

| Total Employee Contribution (50+) | $31,000 |

| Employer + Employee Total (under 50) | $70,000 |

| Employer + Employee Total (50+) | $77,500 |

| Roth 401(k) Employee Limit | $23,500 |

This table provides a clear snapshot of the 2026 max 401k contribution limits across all categories. Notice that Roth and Traditional 401(k) plans share the same employee deferral limits—the difference lies in tax treatment, not contribution caps.

Catch-Up Contribution Rules for Age 50+ in 2026

If you are 50 or older as of December 31, 2026, you qualify for catch-up contributions. This provision allows older workers to contribute an additional $7,500 beyond the standard $23,500 limit.

Who qualifies: Anyone who turns 50 or older during the calendar year. You don’t need to be 50 on January 1—you qualify as long as you reach 50 by December 31, 2026.

How it works: The catch-up contribution is an additional allowance. You contribute the standard $23,500 first, then add up to $7,500 more, for a total of $31,000.

Deadline: Contributions must be made by December 31, 2026, or your employer’s payroll cutoff date (which may be earlier). Unlike IRA contributions, you cannot make 401(k) contributions for 2026 after the calendar year ends.

Why it exists: The catch-up provision recognizes that many workers in their 50s and 60s have higher earning potential and may need to accelerate retirement savings as they approach retirement age.

The SECURE 2.0 Act introduced enhanced catch-up rules for individuals aged 60-63, but these provisions phase in over time. For 2026, the standard catch-up limit of $7,500 applies universally to anyone 50 and older.[1]

Tax benefit: If you contribute the full $31,000 to a Traditional 401(k), that amount is deducted from your taxable income, potentially saving you $7,440 to $11,470 in federal taxes (assuming a 24-37% tax bracket).

The math favors maximizing catch-up contributions if you can afford it. The combination of tax savings and compound growth creates significant long-term wealth accumulation.

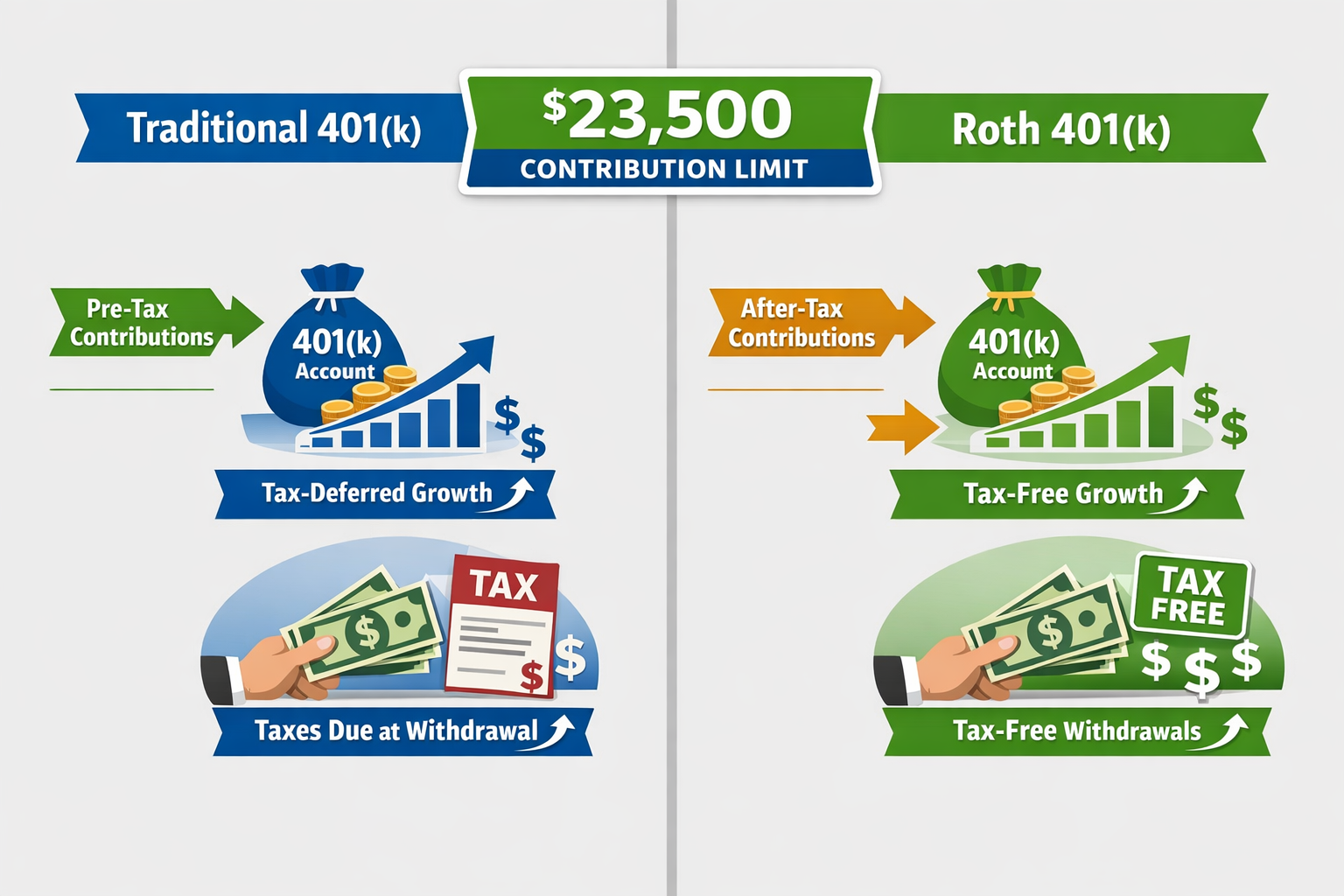

Roth 401k vs Traditional 401(k) Contribution Limits

Both Roth and Traditional 401k plans share the same contribution limits for 2026: $23,500 for employee deferrals and $7,500 for catch-up contributions.

The limits are identical. The difference lies in tax treatment, not contribution caps.

Traditional 401(k): Contributions are made with pre-tax dollars. Your taxable income is reduced by the amount you contribute, providing an immediate tax deduction. You pay taxes on withdrawals in retirement.

Roth 401k: Contributions are made with after-tax dollars. You receive no immediate tax deduction, but qualified withdrawals in retirement are completely tax-free—including all growth and earnings.

Which should you choose?

If you expect to be in a higher tax bracket in retirement, Roth contributions make sense. You pay taxes now at a lower rate and withdraw tax-free later.

If you expect to be in a lower tax bracket in retirement, Traditional contributions are optimal. You defer taxes now at a high rate and pay them later at a lower rate.

Many savers use a hybrid approach: contribute enough to a Traditional 401(k) to maximize employer matching, then direct additional contributions to a Roth 401(k) for tax diversification.

Unlike Roth IRAs, Roth 401k plans have no income limits. High earners who are phased out of Roth IRA contributions can still contribute to a Roth 401(k) without restriction.

For a detailed comparison of tax strategies, see our guide on Roth vs Traditional 401(k) comparison.

Employer Match Rules: What Counts Toward the Max?

Employer contributions do not count toward your $23,500 employee deferral limit. They count only toward the total combined limit of $70,000 ($77,500 with catch-up).

Example:

- You contribute: $23,500 (employee deferral)

- Your employer contributes: $5,000 (50% match on 6% of $100,000 salary)

- Total contributions: $28,500

- Remaining room for additional employer contributions: $41,500 (to reach the $70,000 cap)

Most employees will never approach the $70,000 total limit unless they work for an employer with generous profit-sharing or non-elective contributions.

Employer match types:

Matching contributions: Your employer matches a percentage of your contributions (e.g., 50% of the first 6% you contribute).

Non-elective contributions: Your employer contributes a fixed percentage of your salary regardless of whether you contribute.

Profit-sharing: Your employer makes discretionary contributions based on company profitability.

All employer contributions are made with pre-tax dollars and grow tax-deferred, even if you’re contributing to a Roth 401(k). You’ll pay taxes on employer contributions when you withdraw them in retirement.

Vesting schedules: Some employers require you to work for a certain number of years before you fully own their contributions. If you leave before you’re fully vested, you may forfeit some or all of the employer match.

Always contribute at least enough to capture the full employer match. It’s an immediate 50-100% return on your money—an unbeatable investment that compounds over decades.

Income Limits and 401k Eligibility in 2026

There are no income limits for contributing to a 401(k) plan. Whether you earn $50,000 or $500,000, you can contribute the full $23,500 employee deferral limit (plus catch-up contributions if eligible).

This is a significant advantage over Roth IRAs, which phase out for high earners. In 2026, Roth IRA contributions are limited or eliminated for individuals earning above $150,000 (single) or $236,000 (married filing jointly).

Highly Compensated Employee (HCE) Rules:

If you’re classified as a highly compensated employee, your employer’s 401(k) plan may impose additional restrictions to ensure the plan doesn’t disproportionately benefit high earners.

The IRS defines an HCE as someone who:

- Earned more than $155,000 in 2025 (indexed annually), or

- Owned more than 5% of the business at any time during the year

If your plan fails IRS nondiscrimination testing, HCEs may face reduced contribution limits or be required to receive refunds of excess contributions.

Employer plan restrictions:

Some employers impose eligibility requirements before you can participate in the 401(k) plan:

- Minimum age (typically 21)

- Minimum service period (e.g., 6 months or 1 year)

- Full-time employment status

Once you meet these requirements, you can contribute up to the IRS limits regardless of your income level.

What Happens If You Exceed the 401k Limit?

Exceeding the 401(k) contribution limit creates serious tax consequences. The IRS imposes penalties, and you risk double taxation on the excess amount.

IRS Penalty:

Excess contributions are subject to a 6% excise tax per year until corrected. If you contribute $25,000 instead of the $23,500 limit, you’ll owe 6% tax on the $1,500 excess—$90 annually until you fix it.

Double Taxation Risk:

If you don’t correct the excess by the tax filing deadline, you’ll be taxed twice:

- Once you earn the money (since excess contributions aren’t deductible)

- Again, when you withdraw it in retirement

Correction Deadline:

You must withdraw excess contributions—plus any earnings on those contributions—by April 15 of the following year (or October 15 if you file for an extension).

If you withdraw by the deadline:

- The excess contribution is returned to you

- Any earnings on the excess are taxable in the year earned

- You avoid the 6% penalty

How to fix excess contributions:

- Notify your plan administrator immediately: Contact your HR or benefits department as soon as you realize you’ve over-contributed.

- Request a return of excess: Your plan administrator will calculate the excess amount plus any earnings and return it to you.

- Report on your tax return: The returned excess is taxable income in the year it was earned. Earnings are taxable in the year they’re distributed.

- Adjust future contributions: Reduce your deferral percentage to avoid exceeding the limit in future years.

Common causes of excess contributions:

- Changing jobs mid-year and contributing to multiple 401(k) plans without tracking the combined total

- Employer error in payroll deductions

- Not accounting for bonuses or commission income that push you over the limit

If you have multiple 401(k) plans from different employers in the same year, you are responsible for ensuring your combined contributions don’t exceed the limit. The IRS doesn’t care that it was across multiple plans—the limit applies to you as an individual.

How Much Should You Contribute to Your 401k?

The optimal contribution amount depends on your financial situation, but a few principles guide the decision.

Priority 1: Capture the full employer match

Always contribute at least enough to receive the maximum employer match. If your employer matches 50% of the first 6% you contribute, you should contribute at least 6% of your salary. This is an immediate 50% return—far better than any investment.

Priority 2: Aim for 15-20% total savings rate

Financial planners typically recommend saving 15-20% of your gross income for retirement. This includes both your contributions and your employer’s match.

If you earn $100,000 and your employer matches 3%, you should contribute 12-17% yourself to reach the 15-20% total.

Priority 3: Max out if possible

If you can afford to contribute the full $23,500 (or $31,000 with catch-up), do it. The tax benefits and compound growth are substantial.

Over 30 years, contributing $23,500 annually at a 7% average return grows to approximately $2.36 million. The same amount in a taxable account would be reduced by annual taxes on dividends and capital gains.

Budgeting connection:

Use the 50/30/20 budgeting rule as a framework: 50% for needs, 30% for wants, 20% for savings and debt repayment. Your 401(k) contribution should be part of that 20% savings allocation.

When to contribute less:

- If you have high-interest debt (credit cards, personal loans above 7-8%), prioritize paying that off first

- If you have no emergency fund, build 3-6 months of expenses in a high-yield savings account before maximizing retirement contributions

- If you’re saving for a near-term goal (home down payment, wedding), balance retirement contributions with other savings needs

Long-term investing strategy:

Your 401(k) is a vehicle for long-term wealth building. Contributions should be invested in a diversified portfolio aligned with your risk tolerance and time horizon. Most plans offer target-date funds, index funds, and other options.

For guidance on building a diversified portfolio, explore our investing basics guide.

The key is consistency. Contributing $1,958 per month ($23,500 annually) may seem daunting, but starting with what you can afford and increasing contributions with each raise builds the habit and maximizes compound growth over time.

2026 401(k) Contribution Deadlines

401(k) contributions must be made during the calendar year by December 31, 2026. Unlike IRA contributions, you cannot make 401(k) contributions for 2026 after the year ends.

Payroll cutoff dates:

Your employer’s payroll processing schedule determines the actual deadline. Most employers require you to make your final contribution election by mid-to-late December to ensure it’s processed before year-end.

Check with your HR or benefits department for your company’s specific cutoff date. Missing the deadline means you lose that contribution room forever—it doesn’t roll over to the next year.

Employer contribution deadlines:

Employers have more flexibility. They can make matching or profit-sharing contributions for 2026 up until their tax filing deadline (typically March 15 or April 15, depending on business structure, plus extensions).

However, employee deferrals must be deposited into your 401(k) account within a short timeframe after each payroll period—usually 7 business days for small employers, immediately for large employers.

Mid-year job changes:

If you change jobs during the year, your contributions stop when you leave your employer. You cannot make additional contributions to your old employer’s plan, even if you haven’t reached the annual limit.

You can, however, start contributing to your new employer’s plan (subject to their eligibility requirements). The $23,500 limit applies to you as an individual across all employers, so track your total contributions carefully.

Catch-up contribution timing:

Catch-up contributions can be made throughout the year or in a lump sum, as long as they’re completed by December 31. Some employers automatically enable catch-up contributions once you turn 50; others require you to make a separate election.

2026 401(k) Contribution Calculator

Calculate your maximum contribution and potential tax savings

Conclusion

The 2026 max 401k contribution limit is $23,500 for employee deferrals, with an additional $7,500 catch-up for those 50 and older. The total combined employee-employer limit is $70,000 ($77,500 with catch-up).

Understanding these limits allows you to build a tax-efficient retirement strategy. Maximize employer matching first, then contribute as much as your budget allows. The combination of tax benefits and compound growth creates substantial long-term wealth.

The math is clear: consistent contributions over decades, invested in diversified portfolios, compound into financial independence. Start where you are, increase contributions with each raise, and let time do the heavy lifting.

Review your contribution strategy annually as IRS limits adjust and your financial situation evolves. The earlier you maximize contributions, the more compound growth works in your favor. Retirement planning guide

Disclaimer

This article is for educational and informational purposes only and does not constitute financial, tax, or legal advice. The Rich Guy Math is not a registered investment advisor or financial planner. Retirement contribution limits, tax rules, and regulations are subject to change. Consult with a qualified financial advisor, tax professional, or certified public accountant before making retirement planning decisions. Individual circumstances vary, and strategies discussed may not be suitable for all readers.

Author Bio

Max Fonji is the founder of The Rich Guy Math, a data-driven financial education platform that explains the math behind money. With a background in financial analysis and a commitment to evidence-based investing principles, Max breaks down complex financial concepts into clear, actionable insights. His work focuses on helping readers understand how wealth building, compound growth, and risk management truly work—through numbers, logic, and evidence.

References

[1] Internal Revenue Service. (2025). “401(k) limit increases to $23,500 for 2026, IRA limit remains $7,000.” IRS.gov

[2] U.S. Department of Labor. (2026). “401(k) Plans for Small Businesses.” DOL.gov

[3] Congressional Research Service. (2025). “The SECURE 2.0 Act of 2022: Changes to Retirement Plan Rules.” CRS Reports

Frequently Asked Questions

Can I max out my 401(k) early in the year?

Yes, you can contribute the full $23,500 in the first few months of the year if your cash flow allows. This strategy is often called front-loading your 401(k).

However, there is a potential downside. If your employer matches contributions on a per-paycheck basis rather than providing a true-up match at year-end, you may miss out on employer matching contributions after you hit the annual limit.

Before front-loading, review your plan’s matching policy or ask HR whether your employer offers a year-end true-up.

Does a Roth 401(k) have different contribution limits than a Traditional 401(k)?

No. Roth and Traditional 401(k) accounts share the same contribution limits. For 2026, the employee deferral limit is $23,500, with an additional $7,500 catch-up contribution allowed for those age 50 and older.

The difference between the two is tax treatment. Traditional 401(k) contributions are pre-tax, while Roth 401(k) contributions are made with after-tax dollars and grow tax-free.

Can I contribute to both an IRA and a 401(k)?

Yes. The 401(k) contribution limit is completely separate from IRA limits. In 2026, you can contribute up to $23,500 to a 401(k) and up to $7,000 to an IRA ($8,000 if age 50 or older).

Keep in mind that if you’re covered by a workplace retirement plan, your ability to deduct Traditional IRA contributions may be limited based on your income. Roth IRA eligibility is also subject to income phaseouts.

What happens if I change jobs mid-year?

Your 401(k) contribution limit follows you as an individual, not your employer. If you contribute to multiple employers’ plans in the same year, the combined total cannot exceed the annual limit.

For example, if you contribute $10,000 at your first job and then switch employers, you can contribute up to $13,500 at your new job (assuming you’re under age 50).

It’s your responsibility to track total contributions across all plans to avoid excess contributions and IRS penalties.

Are employer contributions included in the $23,500 limit?

No. Employer matching and profit-sharing contributions do not count toward the $23,500 employee deferral limit.

Employer contributions count toward the overall combined limit, which is $70,000 in 2026 ($77,500 if age 50 or older).

Can I contribute to a 401(k) if I’m self-employed?

Yes. Self-employed individuals can open a Solo 401(k) and contribute as both the employee and the employer.

For 2026, you can contribute up to $23,500 as the employee, plus up to 25% of your net self-employment income as the employer, for a combined maximum of $70,000 ($77,500 if age 50 or older).

Solo 401(k) plans are one of the most powerful retirement tools for business owners due to their high contribution limits and flexibility.

Related posts:

Dividend Portfolio: How to Build One for Steady Passive Income

Dividend Portfolio: How to Build One for Steady Passive Income

Why Should You Invest? The Benefits of Long-Term Investing Explained

Why Should You Invest? The Benefits of Long-Term Investing Explained

What Is a Hedge Fund? How It Works, Strategies, and Risks Explained

What Is a Hedge Fund? How It Works, Strategies, and Risks Explained

Best Robo-Advisors in 2026: Top Picks & Comparison

Best Robo-Advisors in 2026: Top Picks & Comparison

Margin Investing: How It Works, Risks, Examples, and Smart Strategies

Margin Investing: How It Works, Risks, Examples, and Smart Strategies

Robinhood vs Fidelity: Which Brokerage Is Better for Investors?

Robinhood vs Fidelity: Which Brokerage Is Better for Investors?