Net credit represents one of the most fundamental calculations in personal finance and business accounting, yet many people overlook its power to reveal financial health at a glance. For a more comprehensive guide, dive deep into our investing basics guide

Understanding net credit provides clarity on whether money is flowing into or out of accounts, helping individuals and businesses make smarter decisions about cash management, budgeting, and financial planning. This comprehensive guide breaks down the math behind money when it comes to net credit, explaining the formula, providing real-world examples, and offering actionable strategies to optimize this critical financial metric.

Whether tracking personal bank accounts or managing complex business transactions, mastering net credit calculations builds the foundation for stronger financial literacy and evidence-based decision-making.

Key Takeaways

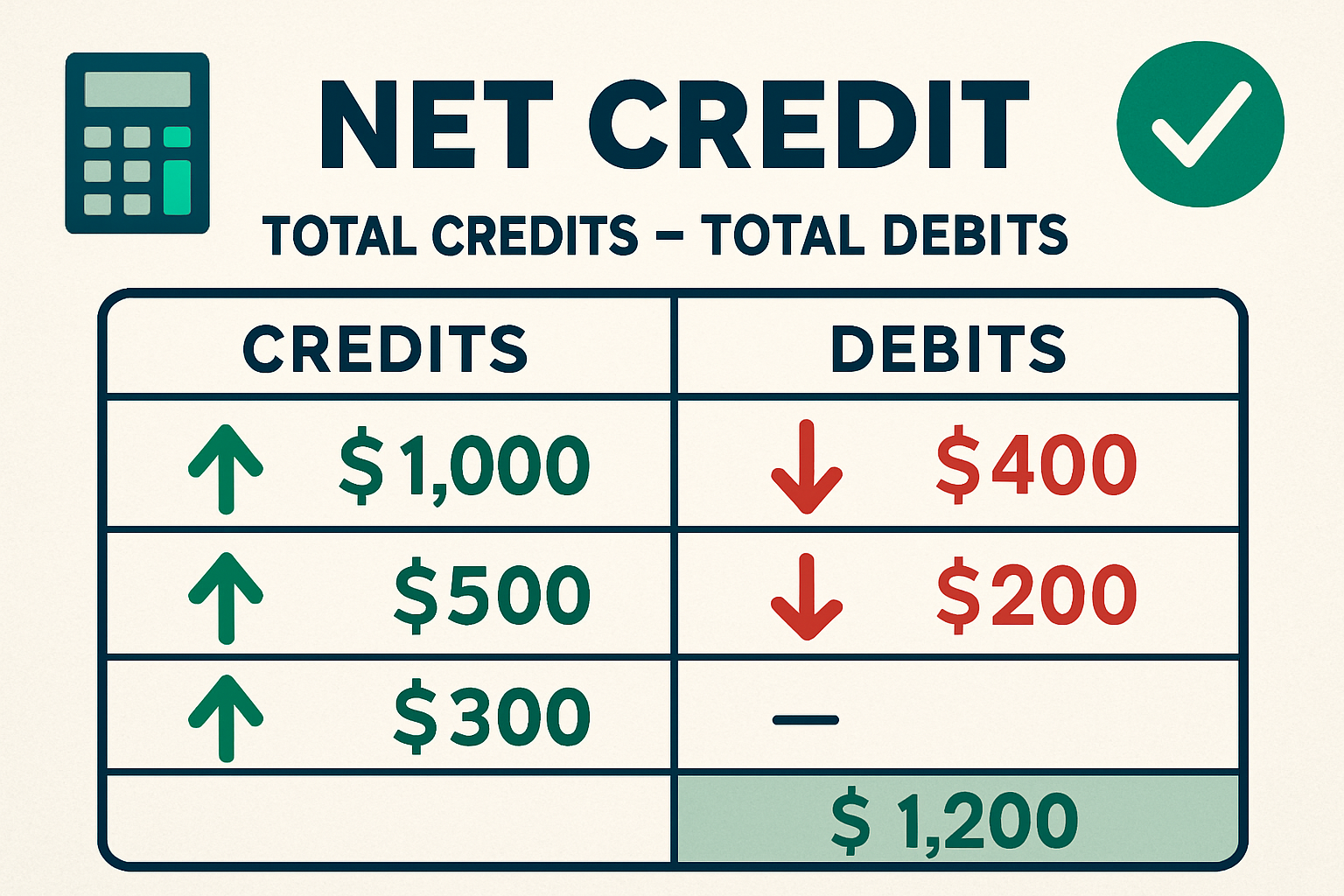

Net credit equals total credits minus total debits—a simple formula that reveals cash flow direction and financial position.

Net credit differs from cash balance—it focuses on transaction flows rather than static account values.

Positive net credit indicates more money coming in than going out—essential for liquidity and financial stability.

Strategic net credit management improves cash flow forecasting—helping both individuals and businesses plan effectively.

Avoiding common calculation errors prevents financial mismanagement—especially when dealing with accrued or pending transactions.

What Is Net Credit?

Net credit is the difference between total credits (money received or incoming) and total debits (money paid or outgoing) over a specific period.

In plain English, net credit tells you whether you’re taking in more money than you’re spending. When total credits exceed total debits, the result is a positive net credit. When debits exceed credits, the result is negative—technically called a net debit.

This calculation appears across multiple financial contexts:

- Personal banking: Tracking deposits versus withdrawals

- Business accounting: Managing accounts receivable versus accounts payable

- Investment trading: Calculating option spreads and trading positions

- Credit card management: Understanding available credit changes

The importance of net credit lies in its simplicity and immediate actionability. Unlike complex financial ratios, net credit provides a straightforward snapshot of financial momentum—whether money is accumulating or depleting.

Gross Credit vs Net Credit

Gross credit represents the total amount of credits without any deductions. It shows all incoming money before accounting for outflows.

Net credit subtracts debits from gross credit, revealing the actual financial position after all transactions.

Example:

- Gross credit: $5,000 (total deposits)

- Total debits: $3,200 (total withdrawals)

- Net credit: $1,800 ($5,000 – $3,200)

This distinction matters because gross credit can appear healthy while net credit reveals financial strain. A business might show $100,000 in gross credit from sales but have a negative net credit of -$20,000 after accounting for supplier payments and operating expenses.

Net Credit vs Net Debit

| Metric | Definition | Indication | Example |

|---|---|---|---|

| Net Credit | Credits > Debits | Positive cash flow; money accumulating | $10,000 credits – $7,000 debits = +$3,000 |

| Net Debit | Debits > Credits | Negative cash flow; money depleting | $5,000 credits – $8,000 debits = -$3,000 (net debit) |

Identifying net credit in financial statements requires examining the cash flow statement or transaction ledger. Look for:

- Operating activities section: Shows credits from revenue and debits from expenses

- Transaction summaries: Display total credits and debits by category

- Bank statements: List deposits (credits) and withdrawals (debits) separately

The key is recognizing that net credit focuses on flows rather than balances. Your bank account might show a $10,000 balance (current balance), but if you had $15,000 in credits and $14,000 in debits this month, your net credit is only $1,000.

Why Net Credit Matters in Finance

Net credit serves as a leading indicator of financial health because it reveals trends before they become problems.

Liquidity implications: Consistent positive net credit builds cash reserves, improving the ability to meet short-term obligations. Negative net credit depletes reserves, potentially creating liquidity crises.

Risk management: Monitoring net credit helps identify unsustainable spending patterns early. A business with declining net credit may need to adjust pricing, reduce costs, or accelerate collections.

Strategic planning: Net credit data informs budgeting decisions and growth strategies. Positive net credit creates investment opportunities, while negative net credit signals the need for operational adjustments.

Example: How Net Credit Affects Cash Flow

Consider a small business over three months:

| Month | Total Credits | Total Debits | Net Credit | Cash Impact |

|---|---|---|---|---|

| January | $50,000 | $45,000 | +$5,000 | Building reserves |

| February | $48,000 | $52,000 | -$4,000 | Depleting reserves |

| March | $55,000 | $49,000 | +$6,000 | Rebuilding reserves |

The February net debit of -$4,000 signals a temporary cash flow problem. Without tracking net credit, management might not notice until cash reserves run dangerously low. This early warning enables proactive responses like adjusting payment terms or accelerating invoicing.

Understanding the relationship between accounts receivable versus accounts payable becomes crucial here—timing of credits and debits directly impacts net credit calculations.

Net Credit Formula

The net credit formula is elegantly simple:

Net Credit = Total Credits – Total Debits

Where:

- Total Credits = Sum of all incoming money or positive transactions

- Total Debits = Sum of all outgoing money or negative transactions

This formula applies universally across personal finance, business accounting, and investment contexts. The result can be positive (net credit), negative (net debit), or zero (balanced).

Alternative expression:

Net Credit = Σ(Credits) – Σ(Debits)

The sigma (Σ) notation emphasizes that you’re summing all credit transactions and all debit transactions before calculating the difference.

Step-by-Step Calculation Example

Let’s walk through a practical net credit calculation for a personal checking account over one week.

Transaction Record:

| Date | Description | Credit ($) | Debit ($) |

|---|---|---|---|

| Monday | Paycheck deposit | 2,500 | 0 |

| Tuesday | Grocery shopping | 0 | 150 |

| Wednesday | Freelance payment received | 400 | 0 |

| Thursday | Rent payment | 0 | 1,200 |

| Friday | Utility bill | 0 | 85 |

| Saturday | Cash deposit | 100 | 0 |

| Sunday | Restaurant | 0 | 60 |

Step 1: Sum all credits

Total Credits = $2,500 + $400 + $100 = $3,000

Step 2: Sum all debits

Total Debits = $150 + $1,200 + $85 + $60 = $1,495

Step 3: Calculate net credit

Net Credit = $3,000 – $1,495 = +$1,505

Result interpretation: The positive net credit of $1,505 indicates this person accumulated $1,505 more than they spent during the week—a healthy financial position.

Common beginner mistakes to avoid:

Confusing credits with debits: Remember that credits represent incoming money (deposits, payments received), while debits represent outgoing money (withdrawals, payments made)

Missing transactions: Failing to include pending transactions or forgetting cash expenditures leads to inaccurate calculations

Wrong time period: Mixing transactions from different periods distorts the net credit calculation

Ignoring signs: Forgetting that debits should be subtracted (not added) produces incorrect results.

Following the 50/30/20 rule budgeting framework, this person’s net credit of $1,505 could be allocated strategically: $752.50 to savings (50%), $451.50 to wants (30%), and $301 to debt repayment (20%).

Alternative Formulas / Variations

Multi-period net credit calculation:

When tracking net credit across multiple periods, use the cumulative approach:

Cumulative Net Credit = Σ(Period₁ Net Credit + Period₂ Net Credit + … + Periodₙ Net Credit)

Example over three months:

- January net credit: +$1,200

- February net credit: -$300

- March net credit: +$800

- Cumulative net credit: $1,700

This shows overall financial direction despite month-to-month fluctuations.

Adjusted net credit (accounting for accruals):

In business accounting, accrued items affect net credit calculations:

Adjusted Net Credit = (Total Credits + Accrued Revenue) – (Total Debits + Accrued Expenses)

This variation provides a more accurate picture when revenue has been earned but not yet received, or expenses have been incurred but not yet paid.

Example:

- Recorded credits: $10,000

- Accrued revenue (invoiced but unpaid): $2,000

- Recorded debits: $7,000

- Accrued expenses (received but unpaid): $1,500

- Adjusted net credit: ($10,000 + $2,000) – ($7,000 + $1,500) = $3,500

Understanding these variations helps when analyzing balance sheet basics and reconciling cash versus accrual accounting methods.

Real-Life Examples of Net Credit

Example 1: Personal Finance (Monthly Budget)

Sarah tracks her personal finances monthly to ensure she’s building wealth consistently.

March 2025 Transactions:

| Category | Credits ($) | Debits ($) |

|---|---|---|

| Salary (after tax) | 4,200 | 0 |

| Side hustle income | 600 | 0 |

| Rent | 0 | 1,400 |

| Groceries | 0 | 450 |

| Transportation | 0 | 200 |

| Utilities | 0 | 150 |

| Entertainment | 0 | 180 |

| Dining out | 0 | 220 |

| Insurance | 0 | 300 |

| Miscellaneous | 0 | 100 |

Calculation:

- Total Credits: $4,200 + $600 = $4,800

- Total Debits: $1,400 + $450 + $200 + $150 + $180 + $220 + $300 + $100 = $3,000

- Net Credit: $4,800 – $3,000 = +$1,800

Analysis: Sarah’s positive net credit of $1,800 represents 37.5% of her total income—an excellent savings rate. This surplus can be allocated to emergency funds, investments, or debt repayment.

By maintaining consistent positive net credit and following principles from compound interest calculators, Sarah can project significant wealth accumulation over time.

Example 2: Business Accounting (Quarterly Operations)

TechStart LLC, a software consulting firm, analyzes Q1 2025 net credit to assess operational efficiency.

Q1 2025 Summary:

| Transaction Type | Credits ($) | Debits ($) |

|---|---|---|

| Client payments received | 125,000 | 0 |

| Consulting fees (outstanding) | 15,000 | 0 |

| Employee salaries | 0 | 65,000 |

| Office rent | 0 | 12,000 |

| Software licenses | 0 | 8,500 |

| Marketing expenses | 0 | 6,200 |

| Professional services | 0 | 4,300 |

| Utilities & supplies | 0 | 2,800 |

Calculation:

- Total Credits: $125,000 + $15,000 = $140,000

- Total Debits: $65,000 + $12,000 + $8,500 + $6,200 + $4,300 + $2,800 = $98,800

- Net Credit: $140,000 – $98,800 = +$41,200

Analysis: TechStart’s net credit of $41,200 represents a 29.4% profit margin on total credits—indicating healthy operations. This positive net credit enables reinvestment in growth initiatives, building cash reserves, or distributing profits.

The firm’s management of accounts receivable (the $15,000 outstanding) versus the timely payment of accounts payable demonstrates effective working capital management.

Example 3: Investment Trading (Options Strategy)

Michael executes a credit spread options strategy on a stock position.

Trade Details:

- Sell 1 call option at strike price $50 → Credit: $300

- Buy 1 call option at strike price $55 → Debit: $150

Calculation:

- Total Credits: $300

- Total Debits: $150

- Net Credit: $300 – $150 = +$150

Analysis: Michael’s net credit of $150 represents the immediate cash received from this options spread. This is his maximum profit if both options expire worthless (stock stays below $50). His maximum risk is $350 (the $5 strike difference × 100 shares – $150 net credit received).

This strategy demonstrates how net credit applies beyond traditional accounting—in trading, positive net credit means receiving money upfront, which is the goal of certain options strategies.

Visual Example Table: Personal Banking Scenario

| Transaction | Date | Credit ($) | Debit ($) | Running Net Credit ($) |

|---|---|---|---|---|

| Opening balance | 3/1/2025 | 0 | 0 | 0 |

| Paycheck deposit | 3/1/2025 | 3,500 | 0 | +3,500 |

| Rent payment | 3/2/2025 | 0 | 1,200 | +2,300 |

| Grocery shopping | 3/5/2025 | 0 | 150 | +2,150 |

| Freelance payment | 3/10/2025 | 800 | 0 | +2,950 |

| Car payment | 3/15/2025 | 0 | 400 | +2,550 |

| Utility bills | 3/20/2025 | 0 | 180 | +2,370 |

| Tax refund | 3/25/2025 | 1,200 | 0 | +3,570 |

| Credit card payment | 3/28/2025 | 0 | 500 | +3,070 |

| Monthly Total | 3/31/2025 | 5,500 | 2,430 | +3,070 |

This running calculation shows how net credit accumulates throughout the month, providing ongoing visibility into financial health. The final net credit of +$3,070 represents genuine wealth accumulation—money that can be saved, invested, or used to build financial security.

Strategies to Optimize Net Credit

Optimizing net credit requires a systematic approach to increasing credits while controlling debits—the fundamental equation of financial success.

Strategy 1: Efficient Invoicing & Accounts Receivable Management

For businesses, the speed of converting sales into actual cash directly impacts net credit.

Actionable tactics:

Implement immediate invoicing: Send invoices within 24 hours of delivering services or products. Delayed invoicing extends the time between earning revenue and receiving payment.

Offer early payment incentives: Provide 2% discount for payment within 10 days (2/10 net 30 terms). This accelerates cash collection and improves net credit.

Automate payment reminders: Use accounting software to send automatic reminders at 7, 14, and 21 days for unpaid invoices.

Accept multiple payment methods: Enable credit cards, ACH transfers, and digital payments to remove friction from the payment process.

Example calculation:

Before optimization:

- Average collection period: 45 days

- Monthly sales: $100,000

- Uncollected revenue at month-end: $150,000 (1.5 months)

- Net credit impact: -$150,000 (tied up in receivables)

After optimization:

- Average collection period: 20 days

- Monthly sales: $100,000

- Uncollected revenue at month-end: $66,667 (0.67 months)

- Net credit improvement: +$83,333

This $83,333 improvement in net credit provides working capital for operations without borrowing—a significant competitive advantage.

Strategy 2: Strategic Payables Management

Controlling the timing of debits without damaging vendor relationships optimizes net credit.

Actionable tactics:

Negotiate extended payment terms: Request 60-day terms instead of 30-day terms from suppliers. This keeps cash in your accounts longer.

Schedule payments strategically: Pay bills on the due date (not early) to maximize the time value of money. Use autopay to ensure timely payments without manual effort.

Prioritize high-impact expenses: Pay critical suppliers promptly to maintain relationships while extending payment on less critical items.

Leverage billing cycles: Make purchases early in the billing cycle to maximize the interest-free period before payment is due.

Example: Credit Card Float Strategy

- Purchase made: April 2

- Billing cycle closes: April 30

- Payment due: May 25

- Interest-free period: 53 days

By strategically timing purchases, you create a positive net credit position—using goods/services while keeping cash in interest-bearing accounts.

⚠️ Important: This strategy requires disciplined tracking to avoid late payments and interest charges that would negate the benefit.

Strategy 3: Using Net Credit for Financial Planning & Forecasting

Net credit trends reveal future financial position more accurately than static balance sheets.

Actionable tactics:

Calculate rolling 3-month net credit average: Smooth out monthly variations to identify true trends.

Project future net credit: Use historical patterns to forecast cash positions 3-6 months ahead.

Set net credit targets: Establish minimum acceptable net credit levels as financial guardrails.

Create scenario models: Calculate net credit under different revenue/expense scenarios to prepare for contingencies.

Example: Net Credit Forecasting Model

| Month | Historical Net Credit | Trend | Forecast (Next Quarter) |

|---|---|---|---|

| January | +$12,000 | Baseline | +$12,500 |

| February | +$11,500 | -4.2% | +$12,000 |

| March | +$13,200 | +14.8% | +$13,800 |

| Average | +$12,233 | +3.5% | +$12,767 |

This forecast suggests the business should maintain approximately $12,767 in positive net credit monthly—information critical for planning investments, hiring, or expansion.

Combining net credit analysis with tools like the 4% rule helps determine sustainable withdrawal rates for retirement planning based on actual cash flow patterns.

Strategy 4: Avoiding Common Net Credit Pitfalls

Mistake 1: Confusing net credit with profitability

Net credit measures cash flow; profit includes non-cash items like depreciation and accrued revenue. A profitable business can have negative net credit if customers pay slowly.

Solution: Track both metrics separately. Use net credit for liquidity planning and profit for performance evaluation.

Mistake 2: Ignoring seasonal variations

Many businesses experience seasonal fluctuations that create misleading month-to-month comparisons.

Solution: Compare net credit to the same period in previous years, not just the previous month.

Mistake 3: Overlooking pending transactions

Modern banking includes pending debits that haven’t cleared, creating a false sense of positive net credit.

Solution: Always account for pending transactions when calculating available balance versus net credit.

Mistake 4: Failing to separate personal and business finances

Mixing personal and business transactions makes accurate net credit calculation impossible.

Solution: Maintain separate accounts and calculate net credit independently for each.

Advanced Strategy for Businesses: Net Credit Ratio Analysis

Beyond simple net credit calculations, sophisticated businesses use net credit efficiency ratios to benchmark performance.

Net Credit to Revenue Ratio:

Net Credit Ratio = (Net Credit / Total Revenue) × 100

This ratio shows what percentage of revenue converts to actual cash flow.

Example:

- Total Revenue: $500,000

- Net Credit: $125,000

- Net Credit Ratio: 25%

Interpretation: For every dollar of revenue, $0.25 becomes available cash after expenses, a strong indicator of operational efficiency.

Industry benchmarks:

- Excellent: 20-30%

- Good: 15-20%

- Concerning: Below 10%

Scenario Analysis: Improving Cash Flow Through Strategic Credit Management

A retail business wants to improve its net credit from $15,000 to $25,000 monthly.

Current state:

- Monthly revenue: $100,000

- Monthly expenses: $85,000

- Net credit: $15,000

- Average collection period: 40 days

- Average payment period: 25 days

Intervention strategies:

| Strategy | Action | Impact on Net Credit |

|---|---|---|

| Accelerate collections | Increase the payment period to 35 days | +$5,000 |

| Extend payables | Increase payment period to 35 days | +$3,500 |

| Reduce operating expenses | Cut non-essential costs by 5% | +$4,250 |

| Combined effect | All strategies | +$12,750 |

New net credit: $15,000 + $12,750 = $27,750 (exceeds $25,000 target)

This scenario demonstrates how strategic management of both credits and debits creates significant improvements in financial position without increasing revenue.

Understanding the relationship between assets and liabilities helps contextualize how net credit improvements strengthen the overall balance sheet.

Common Mistakes to Avoid

Mistake #1: Confusing Net Credit with Cash Balance

The error: Assuming net credit and bank account balance are the same thing.

The reality: Net credit measures the change in cash position over a period, while cash balance represents the total amount in the account at a point in time.

Example:

- Starting balance: $10,000

- Monthly credits: $5,000

- Monthly debits: $4,000

- Net credit: +$1,000

- Ending balance: $11,000

The net credit of $1,000 shows the increase during the month, not the total cash available.

Why it matters: You might have a positive net credit but still face cash shortages if your starting balance was low. Conversely, negative net credit doesn’t mean bankruptcy if you have substantial reserves.

Solution: Track both metrics. Use net credit to understand trends and cash balance to ensure adequate liquidity.

Mistake #2: Ignoring Accrued Debits

The error: Calculating net credit based only on cleared transactions while ignoring pending or accrued expenses.

The reality: Accrued debits—expenses incurred but not yet paid—will eventually reduce net credit when they clear.

Example:

- Visible credits: $8,000

- Visible debits: $5,000

- Apparent net credit: +$3,000

- Pending credit card charges: $1,200

- Scheduled automatic payments: $800

- Actual net credit: +$1,000

Why it matters: Ignoring accrued debits creates a false sense of financial security, potentially leading to overdrafts or insufficient funds.

Solution: Maintain a transaction register that includes pending items. Many banking apps show both “current balance” and “available balance”—use the available balance for accurate net credit calculations.

Mistake #3: Miscalculating Multi-Period Transactions

The error: Double-counting or omitting transactions when calculating net credit across multiple periods.

The reality: Transactions must be assigned to exactly one period to avoid distortion.

Example of double-counting:

- Invoice sent December 30, 2024

- Payment received January 5, 2025

- Error: Counting as credit in both December 2024 and January 2025

Correct approach: Use either the cash basis (count when money moves) or the accrual basis (count when earned/incurred), but be consistent.

Cash basis for this example:

- December 2024 credit: $0 (payment not received)

- January 2025 credit: $5,000 (payment received)

Accrual basis for this example:

- December 2024 credit: $5,000 (revenue earned)

- January 2025 credit: $0 (already counted)

Why it matters: Inconsistent period assignment inflates or deflates net credit, making trend analysis impossible.

Solution: Establish clear rules for transaction dating and stick to them. For personal finance, the cash basis is simpler. For business accounting, the accrual basis provides a more accurate financial picture.

Understanding the difference between cash versus accrual accounting prevents these multi-period errors.

Mistake #4: Forgetting Non-Cash Credits and Debits

The error: Including non-cash items like depreciation or stock-based compensation in net credit calculations.

The reality: Net credit should reflect only actual cash movements, not accounting adjustments.

Example:

- Cash revenue: $50,000

- Depreciation expense: $5,000 (non-cash)

- Cash operating expenses: $30,000

- Incorrect net credit: $50,000 – $5,000 – $30,000 = $15,000

- Correct net credit: $50,000 – $30,000 = $20,000

Why it matters: Including non-cash items distorts the actual cash flow position, making it impossible to assess true liquidity.

Solution: When reviewing financial statements, separate cash from non-cash items. Focus net credit calculations exclusively on transactions that move money.

Mistake #5: Neglecting Currency Timing

The error: Treating all credits and debits as if they occur simultaneously.

The reality: Timing differences between when credits arrive and when debits leave affect actual cash availability.

Example:

- Large payment due: March 1 ($5,000 debit)

- Expected client payment: March 15 ($6,000 credit)

- Monthly net credit: +$1,000 (positive)

- Cash crisis on March 1: Insufficient funds to cover $5,000 payment

Why it matters: Positive monthly net credit doesn’t guarantee liquidity at every point during the month.

Solution: Create cash flow calendars showing when specific credits and debits occur. Maintain buffer reserves to cover timing gaps.

This concept relates directly to understanding the cash conversion cycle—the time between paying for inventory and collecting customer payments.

💰 Net Credit Calculator

Calculate your net credit by tracking credits and debits

Conclusion

Net credit represents one of the most accessible yet powerful tools in financial analysis—a simple calculation that reveals the fundamental truth about whether wealth is building or eroding.

By mastering the formula (Total Credits - Total Debits), understanding real-world applications across personal finance and business contexts, and implementing strategic optimization techniques, anyone can gain clearer visibility into their financial trajectory.

The math behind money becomes transparent when tracking net credit consistently. Positive net credit creates the foundation for compound growth, enabling systematic wealth building through disciplined cash flow management.

Actionable next steps:

- Calculate your current net credit: Review last month's transactions and determine whether you achieved positive or negative net credit

- Set a net credit target: Based on your income and essential expenses, establish a minimum monthly net credit goal

- Implement one optimization strategy: Choose accelerating credits or managing debits, then execute one specific tactic this week.

- Track trends monthly: Create a simple spreadsheet tracking monthly net credit to identify patterns over time

- Adjust and iterate: Use net credit data to inform budgeting decisions and financial planning.

Understanding net credit provides the analytical foundation for making evidence-based financial decisions—whether managing personal budgets, operating a business, or evaluating investment strategies. The clarity gained from this simple metric transforms financial management from guesswork into systematic, data-driven decision-making.

For a deeper exploration of related financial concepts, consider reading about accounting profit, current ratio analysis, and cash flow statement fundamentals.

References

[1] Corporate Finance Institute. "Accounting Basics." CFI Education. https://corporatefinanceinstitute.com/resources/accounting/

[2] Investopedia. "Credit Definition." Investopedia Financial Terms. https://www.investopedia.com/terms/c/credit.asp

[3] Financial Accounting Standards Board. "Statement of Cash Flows." FASB Accounting Standards. https://www.fasb.org/

[4] U.S. Securities and Exchange Commission. "Beginners' Guide to Financial Statements." SEC Investor Publications. https://www.sec.gov/reportspubs/investor-publications/investorpubsbegfinstmtguidehtm.html

[5] CFA Institute. "Cash Flow Analysis." CFA Program Curriculum. https://www.cfainstitute.org/

Author Bio

Written by Max Fonji — Your trusted source for data-driven financial education. We explain the math behind money with precision and authority, helping beginners and intermediate investors understand wealth building, investing fundamentals, and risk management through numbers, logic, and evidence. Every article is backed by authoritative sources, including the SEC, CFA Institute, and leading financial institutions.

Learn more about our mission at The Rich Guy Math.

Educational Disclaimer

This article is for educational purposes only and does not constitute financial, investment, tax, or legal advice. Net credit calculations should be used as one tool among many for financial analysis. Individual circumstances vary significantly, and what works for one person or business may not be appropriate for another.

Always consult with qualified financial professionals, certified public accountants, or financial advisors before making significant financial decisions. The examples provided are hypothetical and for illustrative purposes only. Past performance does not guarantee future results.

The Rich Guy Math provides educational content to improve financial literacy, but does not provide personalized financial advice. Readers are responsible for their own financial decisions and should conduct thorough research and seek professional guidance appropriate to their specific situations.

Frequently Asked Questions

How do I calculate net credit in my bank account?

Add all deposits (credits) for the period, add all withdrawals and payments (debits), then subtract total debits from total credits. The result is your net credit. Most banking apps provide transaction summaries that categorize deposits and withdrawals, making this calculation straightforward. For accuracy, include pending transactions that haven't cleared yet.

Is net credit the same as profit?

No. Net credit measures cash flow (actual money in minus money out), while profit includes non-cash items like depreciation, accrued revenue, and stock-based compensation. A business can be profitable on paper but have negative net credit if customers pay slowly. Conversely, positive net credit doesn't guarantee profitability if the business is liquidating assets. Track both metrics for complete financial understanding.

Can net credit be negative?

Yes. Negative net credit (technically called net debit) occurs when total debits exceed total credits during a period. This indicates money is flowing out faster than it's coming in—a warning sign requiring immediate attention. Occasional negative net credit isn't necessarily problematic (such as when making a large planned purchase), but sustained negative net credit depletes reserves and creates financial instability.

How does net credit affect business liquidity?

Net credit directly impacts liquidity by determining whether cash reserves are growing or shrinking. Positive net credit builds cash reserves, improving the ability to meet short-term obligations and seize opportunities. Negative net credit depletes reserves, potentially creating liquidity crises where the business cannot pay bills despite being profitable on paper. The current ratio and cash ratio complement net credit analysis for comprehensive liquidity assessment.

Does net credit appear on the balance sheet?

No. Net credit is a flow metric calculated from the cash flow statement or transaction ledger, not a balance sheet item. The balance sheet shows point-in-time positions (assets, liabilities, equity), while net credit shows changes over time. However, cumulative net credit over multiple periods affects the cash and cash equivalents line item on the balance sheet. Understanding balance sheet basics helps contextualize where net credit impacts appear.

How can I improve my net credit efficiently?

Improve net credit through three primary levers:

- Increase credits: Accelerate collections, add income streams, or raise prices

- Decrease debits: Reduce expenses, negotiate better terms, or eliminate waste

- Optimize timing: Collect faster and pay strategically

The most efficient approach combines all three—even small improvements in each area compound to significant net credit gains. Start with the highest-impact, lowest-effort changes first.

What's the difference between net credit and available credit?

Net credit measures the difference between credits and debits over a time period (a flow metric), while available credit represents the unused portion of a credit line at a specific moment (a capacity metric). For example, if you have a $10,000 credit card with a $3,000 balance, your available credit is $7,000. Your monthly net credit on that card would be the difference between payments made (credits) and new charges (debits) during the month.

How often should I calculate net credit?

For personal finance, monthly calculations provide sufficient insight for budgeting and planning. For businesses, weekly or even daily net credit calculations enable proactive cash management. The optimal frequency depends on transaction volume and financial volatility—higher volume and greater variability require more frequent monitoring. At minimum, calculate net credit monthly and review trends quarterly to identify patterns and make strategic adjustments.