Retire Early isn’t just a dream reserved for lottery winners or tech entrepreneurs who sold their startups. It’s a mathematically achievable goal grounded in specific principles, disciplined execution, and understanding the data-driven relationship between income, expenses, savings rate, and time. The math behind early retirement is surprisingly straightforward: save aggressively, invest systematically, minimize expenses strategically, and let compound growth do the heavy lifting.

The reality, however, reveals a stark contrast between intention and execution. According to 2024 research from the Employee Benefit Research Institute, 58% of American retirees aged 62-75 retired earlier than expected, but only 21% did so because they could afford to. The majority faced forced early retirement due to health issues (38%) or company downsizing (23%). This data exposes a critical truth: retiring early by choice requires deliberate planning, while retiring early by circumstance often leads to financial stress.

This comprehensive guide breaks down the evidence-based strategies, mathematical frameworks, and actionable steps to achieve genuine financial independence, the kind that lets you retire early on your terms, not because circumstances forced your hand.

Key Takeaways

- Financial independence requires 25-30x your annual expenses using the 4% Rule framework, meaning someone spending $40,000/year needs $1-1.2 million invested

- Savings rate matters more than investment returns in the accumulation phase; a 50% savings rate can enable retirement in 17 years, versus 51 years at 10% savings

- Most early retirements are involuntary; only 21% of early retirees left work because they could afford to, highlighting the importance of proactive planning

- Multiple income streams reduce retirement risk; combining dividends, rental income, part-time work, and portfolio withdrawals creates resilience against market volatility

- The gap between retirement expectations and reality is 3 years; workers expect to retire at 65, but the median actual retirement age is 62, requiring earlier preparation

Understanding the Math Behind Early Retirement

Early retirement isn’t about luck or inheritance. It’s about understanding a simple mathematical relationship: your retirement timeline depends on the gap between what you earn and what you spend.

The formula is elegant in its simplicity:

Years to Financial Independence = f(Savings Rate, Investment Returns, Current Assets)

When you save 10% of your income, you fund roughly 5 weeks of retirement expenses per year worked. At a 50% savings rate, you fund an entire year of retirement expenses for each year worked. This exponential relationship explains why increasing your savings rate from 10% to 20% doesn’t just double your progress; it fundamentally transforms your timeline.

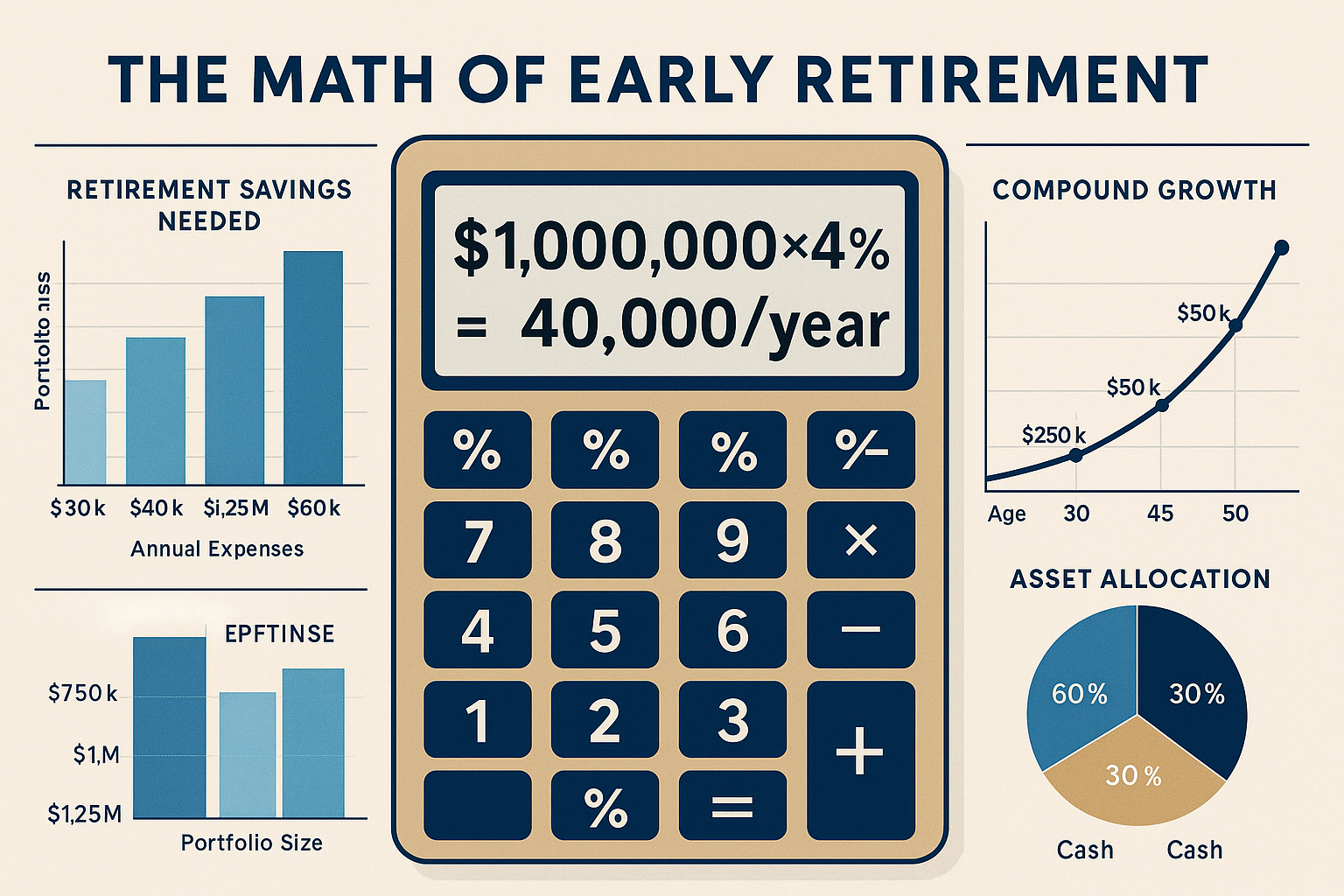

The 4% Rule: Your Retirement Number Foundation

The 4% Rule serves as the cornerstone calculation for early retirement planning. Based on historical market data and the Trinity Study, this principle states that you can safely withdraw 4% of your portfolio annually (adjusted for inflation) with a high probability of not running out of money over a 30-year retirement.

The inverse of this rule gives you your target number:

Required Portfolio = Annual Expenses × 25

If you spend $40,000 annually, you need $1,000,000 invested. Spend $60,000? You need $1,500,000. The math is linear and unforgiving, but also empowering because it gives you a clear target.

For early retirees facing potentially 50+ year retirements, many financial analysts recommend a more conservative 3.5% withdrawal rate (28.6x expenses) or 3% (33.3x expenses) to account for sequence of returns risk and longer time horizons.[2]

Why Savings Rate Trumps Investment Returns

Consider two individuals, both earning $60,000 annually:

Person A: Saves 10% ($6,000/year), spends $54,000/year, needs $1,350,000 to retire

Person B: Saves 50% ($30,000/year), spends $30,000/year, needs $750,000 to retire

Person B needs 44% less money and accumulates savings 5x faster. Even with identical 7% investment returns, Person A requires approximately 51 years to reach their target, while Person B achieves financial independence in roughly 17 years.

This demonstrates a fundamental truth: in the accumulation phase, your savings rate determines your timeline more than your investment returns. You control your savings rate completely. You do not control investment returns at all.

The Current State of Early Retirement in 2025

The landscape of early retirement has shifted dramatically. Northwestern Mutual’s 2025 Planning & Progress Study reveals that Americans now believe they need $1.26 million to retire comfortably, down from $1.46 million in 2024, a $200,000 decrease.[3] This reduction may reflect more realistic expectations or concerns about the underestimation of retirement costs.

Retirement Savings by Generation: The Reality Check

Average 401(k) balances in 2025 paint a sobering picture of retirement preparedness:

| Generation | Average 401(k) Balance | Median Retirement Savings (Ages 55-64) |

|---|---|---|

| Baby Boomers | $249,300 | $185,000 |

| Gen X | $192,300 | $115,000 (ages 45-54) |

| Millennials | $67,300 | $45,000 (ages 35-44) |

| Gen Z | $13,500 | $18,800 (under 35) |

These numbers reveal a critical gap. Even Baby Boomers approaching traditional retirement age have median savings of $185,000, enough to support only $7,400/year using the 4% Rule, far below most retirees’ actual expenses.

More concerning: 58% of American workers report their retirement savings are behind where they should be. This percentage increases with age: 37% of Gen Z, 45% of Millennials, 61% of Gen X, and 72% of Baby Boomers feel behind schedule.[4]

The Confidence Paradox

Despite inadequate savings, 67% of workers and 78% of retirees express confidence in their ability to fund a comfortable retirement. This confidence-reality gap suggests either optimism bias or reliance on income sources beyond traditional retirement accounts (Social Security, pensions, home equity, and continued part-time work).

Yet 51% of Americans believe it’s somewhat or very likely they will outlive their savings, a contradiction that highlights the anxiety underlying surface-level confidence.[5]

Building Your Early Retirement Foundation

Achieving financial independence requires constructing a solid foundation across four pillars: income optimization, expense management, systematic investing, and risk mitigation.

Pillar 1: Maximize Your Income Potential

Active income forms the fuel for your early retirement engine. The faster you earn, the faster you can save, and the sooner you achieve independence.

Career optimization strategies include:

- Skill stacking: Develop complementary skills that increase your market value exponentially rather than linearly

- Strategic job changes: Research shows job switchers earn 10-20% more than those who stay with one employer

- Negotiation: A single successful salary negotiation can add $500,000+ to lifetime earnings

- Side income streams: Freelancing, consulting, or business ventures that leverage existing skills

Understanding the difference between active income and passive income sources becomes crucial as you transition toward financial independence. Early in your journey, maximize active income. As your portfolio grows, gradually shift toward passive income sources that don’t require trading time for money.

Pillar 2: Master the Math of Spending

Every dollar you don’t spend serves double duty: it reduces your required retirement portfolio AND increases your monthly savings contribution.

Consider this powerful example:

Cutting $500/month in expenses:

- Reduces annual spending by $6,000

- Reduces required portfolio by $150,000 (using 4% Rule)

- Increases annual savings by $6,000

- Accelerates timeline by approximately 3-5 years

Strategic expense reduction focuses on the “big three” that consume 60-70% of most budgets:

Housing: The 3x rent rule suggests your monthly rent shouldn’t exceed 1/3 of your monthly gross income. For homebuyers, the 20/4/10 rule (20% down, 4-year loan, 10% of gross income) prevents overextension. House hacking, downsizing, or relocating to lower cost-of-living areas can save $500-2,000+ monthly.

Transportation: Vehicles depreciate rapidly, while insurance, fuel, and maintenance create ongoing drains. The true cost of car ownership often exceeds $700/month. Consider one reliable used vehicle, public transportation, or car-free living in walkable areas.

Food: Meal planning, bulk buying, and reducing restaurant frequency can cut food costs 40-60% without sacrificing nutrition or satisfaction.

The 50/30/20 rule for budgeting provides a starting framework: 50% needs, 30% wants, 20% savings. For early retirement seekers, reverse these percentages, aim for 20-30% on needs, 10-20% on wants, and 50-70% toward savings and investments.

Pillar 3: Invest with Mathematical Precision

Saving money isn’t enough. Inflation erodes purchasing power at 2-3% annually, meaning cash loses half its value every 24-35 years. Compound growth through investing transforms your savings into wealth-building machinery.

The compound interest formula reveals the mathematical magic:

FV = PV × (1 + r)^t

Where:

- FV = Future Value

- PV = Present Value

- r = Annual return rate

- t = Time in years

A $10,000 investment at 7% annual returns grows to:

- $19,672 after 10 years

- $38,697 after 20 years

- $76,123 after 30 years

The same $10,000 at 10% returns reaches $174,494 after 30 years—a $98,371 difference from the 7% scenario. This demonstrates why investment selection matters, but also why time in the market beats timing the market.

Evidence-Based Investment Strategies for Early Retirement

Index Fund Investing: Best index funds provide diversified exposure to entire markets with minimal fees (0.03-0.20% expense ratios). The S&P 500 has delivered approximately 10% average annual returns over the past century, though individual years vary dramatically.

Dividend Growth Investing: Dividend investing creates income streams that can supplement or replace portfolio withdrawals. Dividend aristocrats, companies that have increased dividends for 25+ consecutive years, combine income with growth potential.

ETF Diversification: Best ETFs to buy span asset classes, sectors, and geographies. ETFs versus individual stocks show that for most early retirement seekers, diversified ETFs reduce company-specific risk while maintaining market returns.

Dollar-Cost Averaging: Dollar-cost averaging involves investing fixed amounts at regular intervals regardless of market conditions. This strategy removes emotion from investing and naturally buys more shares when prices are low, fewer when high.

Pillar 4: Build Resilience Through Risk Management

Early retirement amplifies certain risks that traditional retirees face for shorter periods:

Sequence of Returns Risk: A market crash early in retirement can devastate your portfolio. If you retire with $1 million and the market drops 40% in year one while you withdraw $40,000, you’re left with $560,000, requiring a 79% gain just to break even. Mitigation strategies include:

- Maintaining 2-3 years of expenses in cash or bonds

- Flexible spending that decreases during bear markets

- Part-time income to reduce withdrawal pressure

- Portfolio diversification across asset classes

Healthcare Costs: Before Medicare eligibility at 65, early retirees must fund healthcare independently. Average healthcare costs for a couple retiring at 55 can exceed $15,000-20,000 annually. Factor these costs explicitly into your retirement number.

Longevity Risk: Living longer than expected depletes portfolios. A 50-year-old retiring early might need their portfolio to last 40-50 years, far beyond the 30-year horizon the 4% Rule assumes. Consider:

- More conservative withdrawal rates (3-3.5%)

- Delayed Social Security claiming to maximize benefits

- Annuities for guaranteed lifetime income floors

- Continued part-time work in early retirement years

Strategic Paths to Retire Early

Multiple pathways lead to early retirement. Your optimal route depends on your income level, risk tolerance, timeline, and lifestyle preferences.

The Coast FIRE Approach

Coast FI means you’ve saved enough that compound growth alone will reach your full retirement number by traditional retirement age, even if you never save another dollar.

Example: A 35-year-old with $300,000 invested doesn’t need to save more. At 7% annual growth, this becomes $1,187,000 by age 65. They can “coast” in lower-stress, lower-paying work while their existing portfolio grows.

This approach offers psychological benefits, reduced financial pressure while maintaining work engagement, and practical advantages like continued healthcare coverage and Social Security credits.

The Lean FIRE Strategy

Lean FIRE achieves early retirement through aggressive expense minimization. Practitioners typically live on $25,000-40,000 annually, requiring portfolios of $625,000-1,000,000.

This path prioritizes freedom over luxury. Adherents often:

- Live in low-cost-of-living areas or countries (geoarbitrage)

- Embrace minimalism and intentional spending

- Optimize for experiences over possessions

- Utilize geographic flexibility to reduce expenses

Takeaway: Lean FIRE works best for those who genuinely prefer simple living, not those forcing deprivation to escape work they hate.

The Fat FIRE Method

Fat FIRE maintains a higher standard of living in retirement, typically $100,000+ annually, requiring portfolios of $2.5-4+ million.

This approach demands:

- High income ($150,000-500,000+ annually)

- Extended accumulation periods (15-25 years)

- Aggressive savings rates (40-60%) on high incomes

- Sophisticated tax optimization and investment strategies

Fat FIRE appeals to high earners who enjoy their careers but want the option to retire early without lifestyle compromise.

The Barista FIRE Model

Barista FIRE combines part-time work with portfolio withdrawals. The part-time income covers basic expenses and provides healthcare benefits, while the portfolio continues growing or provides supplemental income.

Mathematical advantage: If part-time work generates $20,000 annually and expenses total $45,000, you only need a portfolio supporting $25,000/year ($625,000 using 4% Rule) instead of $1,125,000.

This hybrid approach offers:

- Reduced portfolio size requirements (40-50% less)

- Continued social engagement and purpose

- Healthcare coverage through employment

- Flexibility to stop working entirely later

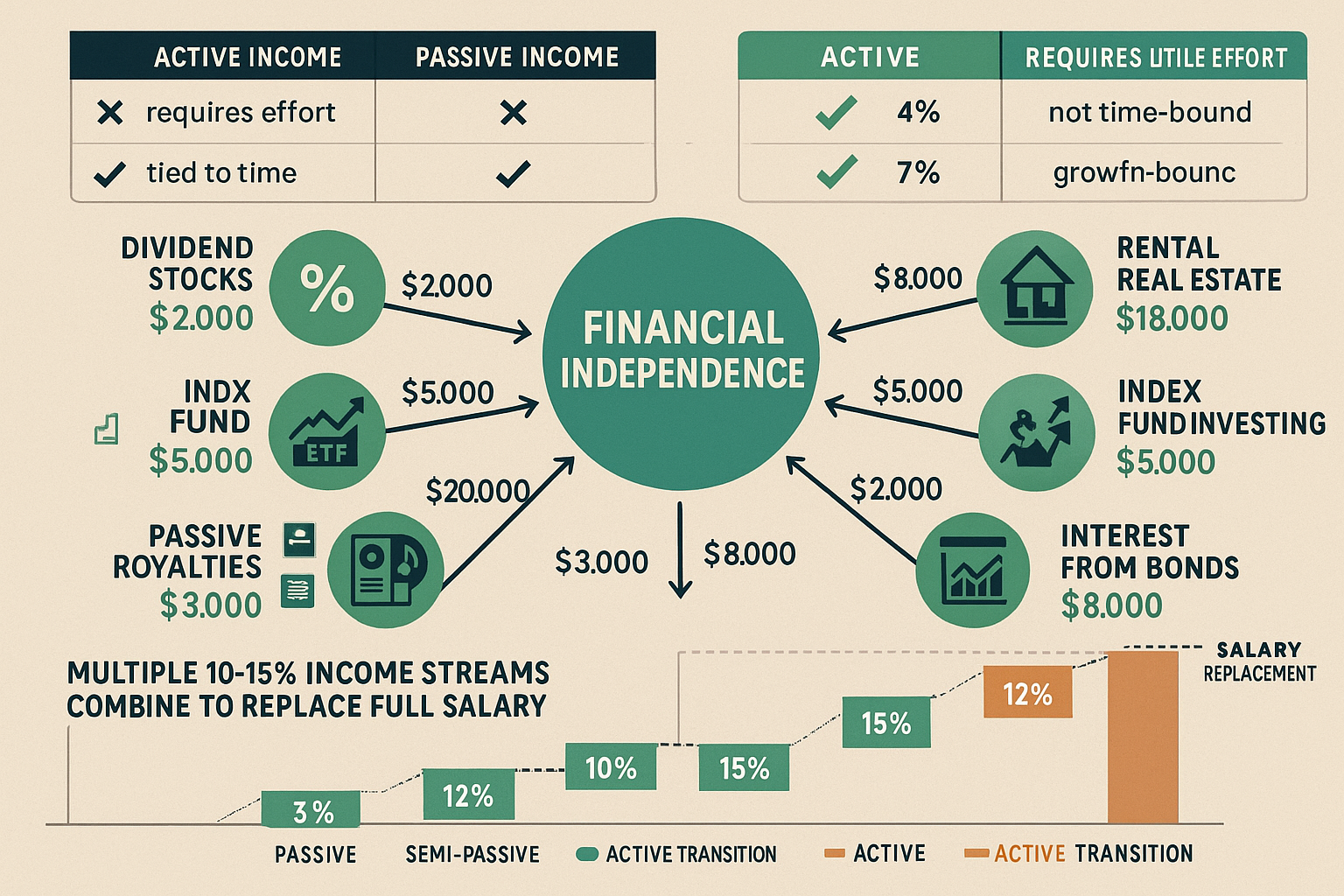

Creating Multiple Income Streams for Financial Independence

Diversification applies to income sources as much as investment portfolios. Multiple income streams create resilience, reduce withdrawal pressure on your portfolio, and provide psychological security.

Portfolio Income: Dividends and Interest

Dividend stocks and dividend ETFs generate cash flow without selling shares. A $1 million portfolio yielding 3% produces $30,000 annually in dividends, covering substantial expenses without touching principal.

Monthly dividend stocks and ETFs provide regular cash flow that aligns with monthly expense cycles, reducing the need for cash reserves.

Strategic consideration: Dividend income faces different tax treatment than capital gains. Qualified dividends receive favorable tax rates (0-20% depending on income), while ordinary dividends face regular income tax rates. Tax-advantaged accounts (Roth IRA, traditional IRA, 401k) shelter dividend income from annual taxation.

Real Estate Income

Rental properties generate monthly cash flow while building equity. REITs (Real Estate Investment Trusts) offer real estate exposure without property management responsibilities.

Example calculation: A rental property purchased for $200,000 (with $40,000 down payment), generating $1,500/month rent with $1,100 in expenses (mortgage, taxes, insurance, maintenance) produces $400/month ($4,800/year) cash flow—a 12% cash-on-cash return on the $40,000 investment.

Real estate income provides:

- Inflation protection (rents typically increase with inflation)

- Leverage advantages (mortgage debt amplifies returns)

- Tax benefits (depreciation, expense deductions)

- Tangible asset diversification

Risk factors: Vacancy, maintenance, property management time, local market dependence, and illiquidity require careful evaluation.

Business and Freelance Income

Skills developed during your career often translate into consulting, freelancing, or small business income. This semi-passive income requires initial effort but can generate substantial returns relative to time invested.

Digital products, online courses, affiliate marketing, and content creation offer scalable income potential with low ongoing time requirements once established.

Social Security Optimization

While not available until age 62 at the earliest, Social Security planning matters for early retirees. Benefits increase 8% annually for each year you delay claiming between ages 62 and 70.

Strategic consideration: Claiming at 62 provides income earlier but reduces lifetime benefits by approximately 30% compared to full retirement age (67 for those born after 1960). Delaying until 70 maximizes monthly benefits.

For early retirees, an optimal strategy often involves:

- Live on portfolio withdrawals ages 50-62

- Claim Social Security at 62-67, depending on health and portfolio status

- Reduce portfolio withdrawals once Social Security begins

In 2025, Social Security benefits increased 2.5%, raising average monthly retirement payments by approximately $48.[6] While modest, this provides some inflation protection.

Tax Optimization Strategies for Early Retirement

Taxes represent one of your largest lifetime expenses. Strategic tax planning can save hundreds of thousands of dollars over an early retirement spanning 40-50 years.

Tax-Advantaged Account Strategies

Traditional 401(k)/IRA: Pre-tax contributions reduce current taxable income. Withdrawals in retirement face ordinary income tax rates. Early withdrawals before age 59½ typically incur 10% penalties plus income tax.

Roth 401(k)/IRA: After-tax contributions receive no immediate tax benefit, but qualified withdrawals (after age 59½ and 5 years) are completely tax-free. Contributions (but not earnings) can be withdrawn anytime without penalty.

Roth Conversion Ladder: This advanced strategy converts traditional IRA funds to Roth IRA in low-income years (early retirement). After a 5-year waiting period, converted amounts can be withdrawn penalty-free before age 59½. This creates a tax-efficient bridge to access retirement funds early.

Example: You retire at 50 with $800,000 in a traditional IRA and $200,000 in taxable accounts. Each year, convert $50,000 from a traditional to a Roth IRA, paying taxes at low rates since you have no employment income. After 5 years, those converted amounts become accessible penalty-free, creating a continuous pipeline of accessible funds.

Capital Gains Tax Optimization

Capital gains tax rates vary based on income. For 2025, single filers with taxable income under $47,025 (married filing jointly: $94,050) pay 0% on long-term capital gains.

Strategic implication: Early retirees with low ordinary income can realize substantial capital gains completely tax-free by staying within these thresholds. A married couple could withdraw $94,050 in capital gains plus $29,200 standard deduction, living on $123,250 with zero federal income tax.

Tax-Loss Harvesting

Selling investments at a loss to offset gains reduces tax liability. You can deduct up to $3,000 in net capital losses against ordinary income annually, with excess losses carrying forward indefinitely.

This strategy works particularly well during market downturns, converting portfolio declines into tax benefits.

Common Pitfalls and How to Avoid Them

Underestimating Healthcare Costs

Healthcare represents one of the largest and most unpredictable retirement expenses. A 55-year-old couple retiring before Medicare eligibility at 65 faces 10 years of private insurance costs averaging $15,000-25,000 annually.

Mitigation strategies:

- Health Savings Accounts (HSAs) offer triple tax advantages: deductible contributions, tax-free growth, and tax-free withdrawals for medical expenses

- Affordable Care Act marketplace plans with premium subsidies for lower-income early retirees

- Healthcare sharing ministries (though not insurance, these reduce costs for some)

- Geographic arbitrage to countries with lower healthcare costs

Failing to Account for Inflation

A $40,000/year lifestyle today requires $72,000 in 30 years at 2.5% inflation. Your retirement plan must account for purchasing power erosion.

Solutions:

- Inflation-protected securities (TIPS)

- Equity exposure for long-term growth above inflation

- Dividend growth stocks that increase payouts faster than inflation

- Flexible spending that adjusts to economic conditions

Sequence of Returns Risk

Retiring into a bear market devastates portfolios through forced selling at depressed prices. The 2008 financial crisis saw portfolios decline 40-50%, and recovery took years.

Protection strategies:

- Bond tent: Increase bond allocation 5 years before and after retirement, then gradually return to a higher equity allocation

- Cash reserves: Maintain 2-3 years of expenses in stable assets

- Flexible withdrawal rates: Reduce spending 10-20% during market downturns

- Part-time income: Reduce portfolio withdrawal pressure during market stress

Lifestyle Inflation

As income increases, spending often rises proportionally—the “hedonic treadmill.” A $20,000 raise becomes $20,000 in new expenses rather than $20,000 in additional savings.

Counter-strategies:

- Automate savings increases when income rises

- Separate lifestyle upgrades from income increases

- Focus on satisfaction per dollar spent

- Regular spending audits to identify unconscious lifestyle creep

Social Isolation and Purpose Loss

Work provides social connection, structure, and purpose. Early retirement can create unexpected psychological challenges when these elements disappear.

Proactive solutions:

- Develop a retirement identity before leaving work

- Build community through volunteering, hobbies, or part-time work

- Create structure and goals for retirement years

- Maintain social connections independent of work

The Psychological Dimensions of Early Retirement

Financial preparation represents only half the early retirement equation. Psychological readiness determines whether early retirement brings fulfillment or regret.

Defining Your “Why”

Retiring early from something (escaping a job you hate) differs fundamentally from retiring early to something (pursuing passions, spending time with family, creative work, service).

The former creates a void. The latter creates purpose.

Reflection questions:

- What will you do with the 40-60 hours per week previously spent working?

- What gives your life meaning beyond career achievement?

- How will you maintain social connections and community?

- What goals or projects excite you more than career advancement?

The Identity Transition

A career often forms a core component of identity. “What do you do?” is typically the second question in social interactions. Early retirees must navigate this identity shift.

Some strategies:

- Develop interests and skills outside work before retiring

- Reframe retirement as “financial independence” or “career optional”

- Maintain some work involvement (consulting, board service, part-time)

- Build identity around values and activities rather than occupation

Trial Retirement

Before making the irreversible decision to retire early, test the experience:

- Take a 3-6 months’ sabbatical if your employer allows

- Use an extended vacation to simulate retirement days

- Experiment with your planned retirement activities while still working

- Assess satisfaction, boredom, and purpose during extended time off

This trial period reveals whether you’re retiring to something meaningful or just from something unpleasant.

Your Early Retirement Action Plan

Achieving financial independence requires systematic execution across multiple domains. Here’s your step-by-step roadmap:

Phase 1: Foundation (Months 1-6)

Calculate your current position:

- Total net worth (assets minus liabilities)

- Current savings rate (savings ÷ gross income)

- Monthly expense tracking to establish a baseline

- Retirement number calculation (annual expenses × 25-30)

Establish an emergency fund:

An emergency fund of 3-6 months’ expenses protects against unexpected costs and prevents portfolio withdrawals during accumulation. This differs from retirement savings in purpose and accessibility.

Eliminate high-interest debt:

Credit card debt at 18-24% APR destroys wealth faster than investments can build it. Prioritize elimination before aggressive investing.

Phase 2: Acceleration (Years 1-3)

Optimize income:

- Negotiate salary increases

- Develop high-value skills

- Pursue promotions or job changes

- Launch side income streams

Maximize savings rate:

- Implement the 50/30/20 rule or more aggressive variants

- Automate savings to investment accounts

- Reduce the “big three” expenses (housing, transportation, food)

- Track spending monthly and identify optimization opportunities

Build investment foundation:

- Max out tax-advantaged accounts (401k, IRA, HSA)

- Establish automated investment contributions

- Implement dollar-cost averaging for consistent market exposure

- Build a diversified portfolio across asset classes

Phase 3: Optimization (Years 3-10)

Sophisticated tax strategies:

- Roth conversions in low-income years

- Tax-loss harvesting in taxable accounts

- Asset location optimization (bonds in tax-advantaged, stocks in taxable)

- Backdoor Roth IRA contributions if income exceeds direct contribution limits

Income diversification:

- Develop passive income streams (dividends, rental income, business income)

- Build skills for potential consulting or freelance work

- Create multiple portfolio withdrawal strategies

- Consider geographic arbitrage opportunities

Continuous optimization:

- Annual spending reviews to eliminate waste

- Investment fee minimization (target expense ratios under 0.20%)

- Portfolio rebalancing to maintain target allocation

- Skill development for career advancement or transition

Phase 4: Transition (Final 2-3 Years)

Financial preparation:

- Shift to more conservative portfolio allocation

- Build 2-3 year cash reserves

- Finalize healthcare coverage strategy

- Complete Roth conversion ladder setup if applicable

Psychological preparation:

- Develop retirement activities and purpose

- Build social connections independent of work

- Test retirement lifestyle through a sabbatical or extended time off

- Create structure and goals for post-work life

Legal and administrative:

- Estate planning (will, power of attorney, healthcare directives)

- Insurance review (life, disability, liability)

- Document investment strategy and withdrawal plan

- Establish systems for ongoing financial management

Measuring Progress: Key Metrics to Track

Data-driven decision making requires tracking specific metrics that indicate progress toward early retirement:

FI Percentage

FI% = (Current Net Worth ÷ Target Retirement Number) × 100

If your target is $1 million and your current net worth is $400,000, you’re 40% financially independent. This single metric provides clear progress visibility.

Savings Rate

Savings Rate = (Gross Income – Expenses) ÷ Gross Income × 100

This determines your timeline more than any other factor. Track monthly and annually to identify trends.

Years to FI

Based on the current savings rate and investment returns, calculate the remaining years to financial independence. Online calculators automate this computation, but the underlying formula considers:

- Current portfolio value

- Monthly contribution amount

- Expected investment return

- Target retirement number

Passive Income Coverage

Coverage Ratio = Monthly Passive Income ÷ Monthly Expenses

When this ratio reaches 1.0 (100%), you’ve achieved financial independence. Track progress from 0% toward 100% as dividend income, rental income, and other passive sources grow.

Withdrawal Rate

In retirement, monitor actual withdrawal rate:

Withdrawal Rate = Annual Withdrawals ÷ Portfolio Value × 100

If this exceeds 4-5%, adjust spending or increase income to prevent portfolio depletion.

🔥 FIRE Calculator

Calculate your path to Financial Independence & Early Retirement

Your FIRE Timeline

💡 Key Insights

Conclusion: Your Path to Financial Independence Starts Today

The data reveals a stark reality: most early retirements happen by circumstance, not choice. Only 21% of early retirees left work because they could afford to, while the majority faced forced retirement through health issues or job loss. This makes proactive planning not just advantageous but essential.

Retire Early isn’t about escaping work you hate; it’s about building the financial foundation that makes work optional. It’s about creating the mathematical relationship between income, expenses, savings, and time that inevitably leads to financial independence.

The framework is straightforward:

- Calculate your number (annual expenses × 25-30)

- Maximize the gap between income and expenses

- Invest systematically in diversified, low-cost index funds

- Build resilience through multiple income streams and conservative planning

- Prepare psychologically for identity transition and purpose development

Your timeline depends entirely on your savings rate. Save 10% and work 51 years. Save 50% and achieve independence in 17 years. Save 70% and retire in under a decade. The math is unforgiving but also empowering; you control the variables that matter most.

Americans believe they need $1.26 million to retire comfortably in 2025, yet median retirement savings for those aged 55-64 sit at just $185,000. This gap doesn’t close through wishful thinking or market timing. It closes through disciplined execution of evidence-based principles.

Your next steps:

- Calculate your current FI percentage today

- Identify one expense category to optimize this month

- Increase your 401(k) contribution by 1-2% this week

- Set up automated investment contributions if you haven’t already

- Define what you’re retiring to, not just what you’re retiring from

Financial independence isn’t reserved for high earners or lucky investors. It’s available to anyone willing to understand the math behind money and execute consistently over time. The question isn’t whether early retirement is possible—it’s whether you’re willing to make the choices that make it inevitable.

Start today. Your future self will thank you.

Sources

[1] Employee Benefit Research Institute (EBRI). (2024). “Retirement Confidence Survey.” Survey of 3,661 retirees aged 62-75.

[2] Bengen, William P. (1994). “Determining Withdrawal Rates Using Historical Data.” Journal of Financial Planning.

[3] Northwestern Mutual. (2025). “Planning & Progress Study 2025.”

[4] Transamerica Center for Retirement Studies. (2025). “Retirement Survey of Workers.”

[5] Federal Reserve. (2024). “Survey of Household Economics and Decisionmaking (SHED).”

[6] Social Security Administration. (2025). “Cost-of-Living Adjustment Announcement.”

Author Bio

Max Fonji is the founder of The Rich Guy Math, a data-driven financial education platform that explains the mathematical principles behind wealth building, investing, and financial independence. With a background in financial analysis and a commitment to evidence-based investing education, Max translates complex financial concepts into clear, actionable insights for investors at all levels. His work emphasizes the cause-and-effect relationships that govern money, helping readers understand not just what to do, but why it works.

Educational Disclaimer

This article provides educational information about early retirement and financial independence strategies. It does not constitute personalized financial advice, investment recommendations, or retirement planning services. Individual financial situations vary significantly based on income, expenses, risk tolerance, timeline, tax circumstances, and personal goals.

Before making significant financial decisions, consult with qualified professionals, including certified financial planners, tax advisors, and investment advisors, who can evaluate your specific circumstances. Past investment performance does not guarantee future results. All investing involves risk, including potential loss of principal.

The strategies, calculations, and frameworks presented represent general principles and historical data, not predictions or guarantees of future outcomes. Your results will vary based on execution, market conditions, and individual circumstances.

Frequently Asked Questions

How much money do I need to retire early?

Your retirement number equals your annual expenses multiplied by 25–30. Someone spending $40,000 per year needs $1–1.2 million invested. The 4% Rule suggests you can withdraw 4% annually with high probability of portfolio longevity. More conservative early retirees use 3–3.5% withdrawal rates (28.6–33.3x expenses) to account for longer retirement horizons.

What is the average age people retire early?

The median retirement age is 62, three years earlier than most workers expect (65). However, only 21% of early retirees leave work because they can afford to—most retire early due to job loss or health issues. Intentional early retirement usually occurs between ages 45–60 for those who plan and invest systematically.

Can I retire early with $500,000?

$500,000 supports about $20,000 per year using the 4% Rule or $15,000 per year at a 3% withdrawal rate. This works for lean FIRE practitioners with minimal expenses, people using geographic arbitrage to low-cost regions, or those combining withdrawals with part-time income (Barista FIRE). For most Americans, $500,000 alone is not sufficient without supplemental income.

What are the biggest risks of retiring early?

The major risks include: (1) sequence of returns risk—market downturns early in retirement causing irreversible damage; (2) high healthcare costs before age 65, often $15,000–25,000 per year for couples; (3) longevity risk—outliving savings over 40–50 years; (4) inflation eroding buying power; (5) emotional challenges such as loss of identity or purpose. You can mitigate these risks by using conservative withdrawal rates, multiple income sources, flexible spending, and planning for meaningful post-retirement activities.

How can I retire early with a low income?

Early retirement is possible even on low income by: (1) aggressively reducing expenses to increase savings rate; (2) improving income through skill-building or career upgrades; (3) relocating to low-cost areas or countries; (4) pursuing lean FIRE with a minimalist lifestyle; (5) extending the timeline—retiring at 55 instead of 45; (6) using hybrid approaches like coast FIRE or barista FIRE. Early retirement math works when savings rate, investment growth, and timeline are aligned realistically.

Do I need to invest in stocks to retire early?

Stocks historically return ~10% annually, far exceeding inflation (2–3%) and bonds (4–6%). Without meaningful stock exposure, early retirement requires extremely high savings rates or much longer timelines. A 100% bond portfolio at 4% versus a balanced portfolio at 7% can add 10 extra years to your retirement date. Some level of equity exposure is essential, but the ideal mix (60/40, 80/20, etc.) depends on your risk tolerance, timeline, and comfort with volatility.

Related posts:

What Is SmartPass? Raptor Digital Hall Pass Explained for K-12 Schools

What Is SmartPass? Raptor Digital Hall Pass Explained for K-12 Schools

What Is the 3x Rent Rule & How to Calculate It (With Examples)

What Is the 3x Rent Rule & How to Calculate It (With Examples)

Portfolio Income: Definition, Examples, Tax Rules, and Strategies

Portfolio Income: Definition, Examples, Tax Rules, and Strategies

Tax Filing: A Clear, Step-by-Step Guide for Stress-Free Taxes

Tax Filing: A Clear, Step-by-Step Guide for Stress-Free Taxes

Return on Assets (ROA): Definition, Formula & How to Improve It

Return on Assets (ROA): Definition, Formula & How to Improve It

How to Save Money Fast: A Smart Savings Plan That Actually Works

How to Save Money Fast: A Smart Savings Plan That Actually Works