Choosing between a Roth IRA and a 401(k) feels like standing at a financial crossroads with your entire retirement on the line. One path promises tax-free withdrawals decades from now. The other delivers immediate tax savings and free money from your employer today.

The truth? This isn’t an either-or decision for most people; it’s a sequencing problem.

The Roth IRA vs 401k debate centers on one fundamental question: when do you want to pay taxes on your retirement savings? Pay taxes on contributions now and withdraw tax-free later (Roth IRA), or defer taxes now and pay them in retirement (401(k))? The math behind this choice depends on your current income, future tax expectations, employer match availability, and investment timeline.

Both accounts use compound growth to build wealth over decades, and both shelter investment gains from annual taxation. But the structural differences, contribution limits, employer matching, withdrawal rules, and income restrictions create distinct advantages depending on your financial situation.

This guide breaks down the data-driven logic behind each account, shows you exactly when to use each one, and provides a clear decision framework based on the math behind money, not generic advice.

Key Takeaways

- Employer match always comes first: Contribute enough to your 401(k) to capture the full employer match before funding any other retirement account—this is an immediate, guaranteed return on investment

- Tax treatment is the core difference: Roth accounts use after-tax dollars for tax-free withdrawals; traditional 401(k)s use pre-tax dollars, but withdrawals are taxed as ordinary income

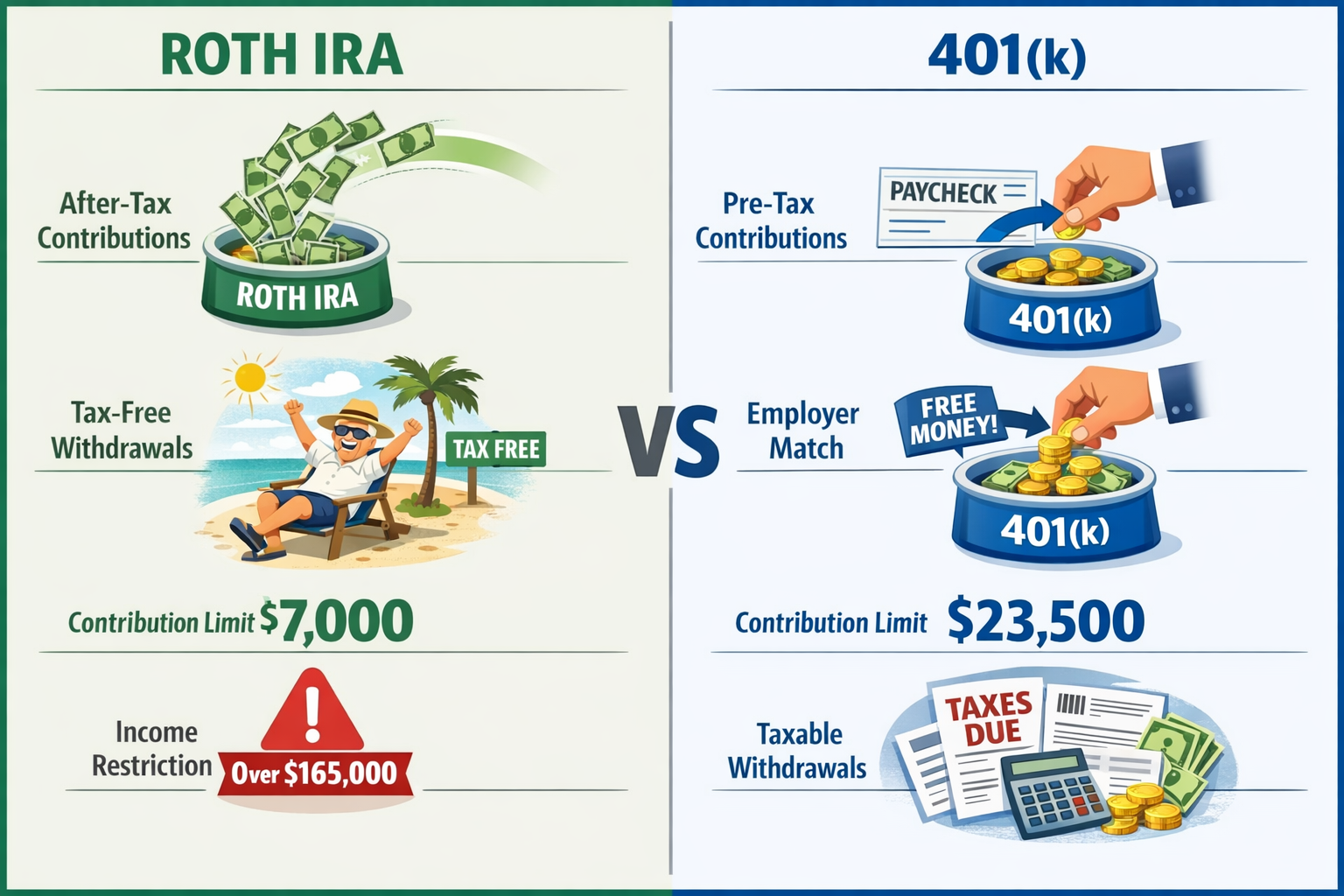

- Contribution limits favor 401(k)s: The 2025 limit is $23,500 for 401(k)s versus $7,000 for Roth IRAs, allowing significantly higher annual savings through employer plans

- Income restrictions apply only to Roth IRAs: High earners above $165,000 (single) or $246,000 (joint) cannot contribute directly to Roth IRAs, but Roth 401(k)s have no income limits

- Optimal strategy uses both accounts: Most investors benefit from tax diversification—maxing employer match in 401(k), then funding Roth IRA, then returning to maximize 401(k) contributions

Roth IRA vs 401(k): Key Differences at a Glance

The Roth IRA and 401(k) serve the same ultimate purpose, building retirement wealth through tax-advantaged compound growth, but they operate under fundamentally different rules.

Understanding these structural differences matters because each creates specific mathematical advantages depending on your income level, career stage, and tax situation.

What Is a Roth IRA?

A Roth IRA is an individual retirement account you open and manage yourself, funded with after-tax dollars.

You contribute money you’ve already paid income tax on. That money grows tax-free inside the account. When you withdraw in retirement (after age 59½ and five years of account ownership), you pay zero taxes on contributions or earnings.

This creates a powerful advantage: tax-free compound growth over decades.

Key Roth IRA characteristics:

- 2025 contribution limit: $7,000 ($8,000 if age 50+)

- Income limits restrict high earners (phaseout begins at $146,000 single, $230,000 joint)

- No employer involvement, you choose the brokerage and investments

- Contributions (not earnings) can be withdrawn anytime, tax and penalty-free

- No required minimum distributions (RMDs) during your lifetime

- Wide investment selection: stocks, bonds, ETFs, mutual funds, REITs

The Roth IRA works best for investors who expect higher tax rates in retirement than they pay today, or who value tax-free withdrawal flexibility.

What is a 401(k)?

A 401(k) is an employer-sponsored retirement plan that typically allows both traditional (pre-tax) and Roth (after-tax) contribution options.

Traditional 401(k) contributions reduce your taxable income immediately. If you earn $80,000 and contribute $10,000, you only pay income tax on $70,000 that year. The money grows tax-deferred, but you pay ordinary income tax on all withdrawals in retirement.

Key 401(k) characteristics:

- 2025 contribution limit: $23,500 ($31,000 if age 50+)

- Employer matching available (typically 3-6% of salary)

- No income limits for contributions

- Limited investment options are chosen by the employer

- Early withdrawal penalties (10% plus taxes) before age 59½, with some exceptions

- Required minimum distributions begin at age 73

- Loans may be available (typically up to $50,000 or 50% of vested balance)

The 401(k) excels at maximizing total savings through higher contribution limits and employer matching contributions, essentially free money that immediately boosts your retirement wealth.

Many employers now offer Roth 401(k) options, which combine the high contribution limits of a 401(k) with the tax-free withdrawal benefits of a Roth IRA. This creates a powerful hybrid tool, though employer matches on Roth 401(k) contributions go into a traditional pre-tax account.

Roth IRA vs 401(k) Comparison Table

The table below shows the critical structural differences that determine which account makes sense for your situation:

| Feature | Roth IRA | Traditional 401(k) | Roth 401(k) |

|---|---|---|---|

| 2025 Contribution Limit | $7,000 ($8,000 age 50+) | $23,500 ($31,000 age 50+) | $23,500 ($31,000 age 50+) |

| Tax Treatment | After-tax contributions, tax-free withdrawals | Pre-tax contributions, taxed withdrawals | After-tax contributions, tax-free withdrawals |

| Income Limits | Yes ($165,000+ single, $246,000+ joint) | No | No |

| Employer Match | No | Yes (typically 3-6% of salary) | Yes (match goes to traditional account) |

| Early Withdrawal | Contributions anytime; earnings penalized before 59½ | 10% penalty + taxes before 59½ | Contributions after 5 years; earnings penalized before 59½ |

| Required Minimum Distributions | No RMDs during the owner’s lifetime | RMDs begin at age 73 | No RMDs during owner’s lifetime |

| Investment Options | Unlimited (any brokerage) | Limited (employer-selected funds) | Limited (employer-selected funds) |

| Who Controls It | You (individual account) | Employer plan | Employer plan |

Taxes Now vs Taxes Later

The fundamental trade-off in the Roth IRA vs 401(k) decision is the timing of taxation.

Roth IRA: Pay income tax on contributions now, never pay tax on qualified withdrawals later.

Traditional 401(k): Avoid income tax on contributions now, pay ordinary income tax on all withdrawals later.

The math behind this choice depends on your marginal tax rate today compared to your expected tax rate in retirement.

Example calculation:

- Contribute $10,000 to Roth IRA in 22% tax bracket = $2,200 in taxes paid today

- The same $10,000 grows to $100,000 over 30 years

- Withdraw $100,000 tax-free in retirement = $0 additional taxes

Versus:

- Contribute $10,000 to traditional 401(k) in 22% tax bracket = $2,200 tax savings today

- The same $10,000 grows to $100,000 over 30 years

- Withdraw $100,000 in 22% tax bracket = $22,000 in taxes owed

If your tax rate remains constant, the math is identical. But if you expect higher tax rates in retirement (through income, policy changes, or loss of deductions), the Roth wins. If you expect lower rates (common for retirees with reduced income), the traditional 401(k) wins.

This is why understanding your tax situation matters for retirement planning.

Contribution Limits and Eligibility

The 401(k) allows more than 3x the annual contributions of a Roth IRA in 2025.

2025 limits:

- Roth IRA: $7,000 ($8,000 if age 50+)

- 401(k): $23,500 ($31,000 if age 50+)

- Total employer + employee 401(k): $70,000 ($77,500 if age 50+)

This difference compounds dramatically over time. An investor maxing out a 401(k) for 30 years at 8% average returns accumulates approximately $2.9 million, compared to roughly $900,000 from maxing a Roth IRA alone.

Income restrictions:

Roth IRA contributions phase out for 2025 at:

- Single filers: $146,000 – $161,000

- Married filing jointly: $230,000 – $240,000

- Completely ineligible above $161,000 (single) or $240,000 (joint)

Traditional and Roth 401(k)s have no income limits. High earners blocked from direct Roth IRA contributions can still use Roth 401(k)s or backdoor Roth IRA strategies.

Starting in 2026, the SECURE Act 2.0 requires catch-up contributions for employees earning over $145,000 (indexed for inflation) to be made as Roth contributions in most employer plans.

Employer Match and Free Money

The employer match is the single most important factor in the Roth IRA vs 401(k) priority decision.

Employer matching contributions represent an immediate 50-100% return on investment; no other investment delivers guaranteed returns of this magnitude.

Common matching formulas:

- 100% match up to 3% of salary

- 50% match up to 6% of salary

- Dollar-for-dollar up to 4% of salary

Real-world example:

- Salary: $75,000

- Employer match: 50% up to 6% of salary

- Your contribution: $4,500 (6% of salary)

- Employer adds: $2,250 (50% match)

- Total retirement contribution: $6,750

- Immediate return: 50% on your $4,500 = guaranteed gain

This free money only comes through 401(k) participation. Roth IRAs receive no employer contributions because they’re individual accounts, not employer-sponsored plans.

The mathematical priority is clear: always contribute enough to capture the full employer match before funding any other retirement account. This is foundational wealth building logic.

Withdrawal Rules and Penalties

Roth IRAs and 401(k)s impose different penalties for early access to your money.

Roth IRA withdrawal rules:

- Contributions can be withdrawn anytime, tax-free and penalty-free (you already paid tax)

- Earnings withdrawn before age 59½ face 10% penalty + income tax

- Qualified distributions (age 59½ + five-year rule) are completely tax-free

- Exceptions exist for first-home purchase ($10,000), education expenses, and certain medical costs

Traditional 401(k) withdrawal rules:

- Withdrawals before age 59½ incur 10% penalty + ordinary income tax

- Exception: Rule of 55 allows penalty-free withdrawals if you leave your employer at age 55+

- Loans available from some plans (typically up to $50,000 or 50% vested balance)

- Hardship withdrawals permitted for specific financial emergencies

Roth 401(k) withdrawal rules:

- Contributions and earnings withdrawn before age 59½ face a 10% penalty

- Qualified distributions (age 59½ + five-year rule) are tax-free

- Rule of 55 applies (penalty-free access when leaving employer at 55+)

The Roth IRA provides superior flexibility for emergency access because contributions can always be withdrawn without penalty. This makes it function partially as both a retirement savings account and an emergency fund, though using it this way reduces compound growth potential.

Required Minimum Distributions (RMDs)

Traditional 401(k)s force you to begin withdrawing money at age 73, whether you need it or not.

These required minimum distributions (RMDs) exist because the IRS wants to collect deferred taxes. The annual RMD amount is calculated by dividing your account balance by your life expectancy factor.

Example RMD at age 73:

- Account balance: $500,000

- Life expectancy factor: 26.5 years

- Required withdrawal: $18,868

- Taxable income: $18,868 (could push you into a higher bracket)

This forced taxation can be problematic if you don’t need the income, as it increases your taxable income and potentially your Medicare premiums.

Roth IRAs have no RMDs during the owner’s lifetime. The money can continue growing tax-free indefinitely, and you withdraw only when you choose. This creates powerful estate planning advantages and maximizes compound growth over your lifetime.

Roth 401(k)s previously required RMDs, but the SECURE Act 2.0 eliminated this requirement starting in 2024. Roth 401(k)s now match Roth IRAs in this advantage, though many advisors still recommend rolling Roth 401(k)s to Roth IRAs at retirement for broader investment options.

Roth IRA vs 401(k): How Taxes Really Work

Tax treatment determines the long-term value of your retirement accounts more than any other factor.

Understanding the mathematical relationship between current tax rates, future tax rates, and compound growth reveals exactly when each account type wins.

When a Roth IRA Makes More Sense

Roth IRAs deliver superior after-tax wealth when you expect higher tax rates in retirement than you pay today.

This scenario is common for:

Early-career professionals: Someone earning $50,000 in their 20s pays a 12% marginal federal tax rate. If they expect to withdraw $100,000+ annually in retirement (24% bracket), paying the 12% tax now and never again creates substantial savings.

Young investors with decades of growth: The longer your investment timeline, the more valuable tax-free compounding becomes. A 25-year-old with 40 years until retirement benefits more from tax-free growth than a 55-year-old with 10 years.

Those expecting tax policy changes: If federal tax rates increase from current levels, locking in today’s rates through Roth contributions protects against future tax increases.

Investors building tax diversification: Having both pre-tax and after-tax retirement accounts provides flexibility to manage taxable income in retirement by choosing which account to withdraw from.

Mathematical example:

A 25-year-old contributes $7,000 annually to a Roth IRA for 40 years at 8% average return:

- Total contributions: $280,000

- Account value at 65: $1,863,000

- Taxes paid on contributions: ~$61,600 (22% average rate)

- Taxes on withdrawals: $0

- Net after-tax wealth: $1,863,000

Same scenario with traditional 401(k):

- Total contributions: $280,000 (pre-tax)

- Account value at 65: $1,863,000

- Taxes on withdrawals: $447,120 (24% rate in retirement)

- Net after-tax wealth: $1,415,880

The Roth IRA delivers $447,120 more in after-tax wealth because the tax rate increased from 22% to 24%, and the tax was paid on contributions rather than the much larger ending balance.

This is the power of tax-free compound interest over decades.

When a 401(k) Makes More Sense

Traditional 401(k)s deliver superior value when you expect lower tax rates in retirement than you pay today.

This scenario applies to:

High earners in peak earning years: Someone in the 32% or 35% marginal bracket today who expects to withdraw at 22-24% rates in retirement saves substantially by deferring taxes.

Those planning early retirement: Retiring before Social Security and pension income begins often creates years of low-income tax brackets, making traditional 401(k) withdrawals very tax-efficient.

Investors maximizing current tax deductions: The immediate tax savings from 401(k) contributions can be invested elsewhere, potentially creating additional wealth.

Employees with generous matches: The higher contribution limits and employer matching in 401(k)s allow total annual contributions far exceeding Roth IRA limits, even after accounting for future taxes.

Mathematical example:

A 45-year-old earning $200,000 contributes $23,500 to traditional 401(k) for 20 years at 8% return:

- Total contributions: $470,000

- Tax savings at contribution: $150,400 (32% bracket)

- Account value at 65: $1,145,000

- Taxes on withdrawals: $251,900 (22% rate in retirement)

- Net after-tax wealth: $893,100

Same scenario with Roth 401(k):

- Total contributions: $470,000 (after-tax)

- Taxes paid on contributions: $150,400 (32% bracket)

- Account value at 65: $1,145,000

- Taxes on withdrawals: $0

- Net after-tax wealth: $893,100

Wait; they’re identical? Not quite. The traditional 401(k) investor had $150,400 in tax savings available to invest over 20 years. If invested in a taxable brokerage account at 6% after-tax return, that grows to $483,000, creating total wealth of $1,376,100 versus $893,100, a $483,000 advantage.

This demonstrates why high earners expecting lower retirement tax rates benefit from traditional 401(k) contributions.

Why Future Tax Rates Matter

The Roth IRA vs 401(k) decision fundamentally depends on the equation:

Tax rate at contribution × Contribution amount versus Tax rate at withdrawal × Withdrawal amount

If contribution and withdrawal tax rates are identical, the accounts produce identical after-tax wealth. The advantage comes from rate differences.

Factors that increase retirement tax rates:

- Higher account balances generate larger withdrawals

- Social Security taxation (up to 85% of benefits are taxable)

- Required minimum distributions forcing income

- Loss of mortgage interest and other deductions

- Federal tax policy changes

- State tax changes (moving to a higher-tax state)

Factors that decrease retirement tax rates:

- Lower total income than working years

- Strategic withdrawal planning across account types

- Relocating to a no-income-tax state

- Charitable donations reduce taxable income

- Only withdrawing needed amounts (no RMDs from Roth)

Nobody knows future tax rates with certainty. This is why tax diversification, holding both pre-tax and after-tax retirement accounts, provides valuable flexibility.

You can adjust withdrawal strategies based on actual tax law when you retire, rather than betting everything on one tax treatment today.

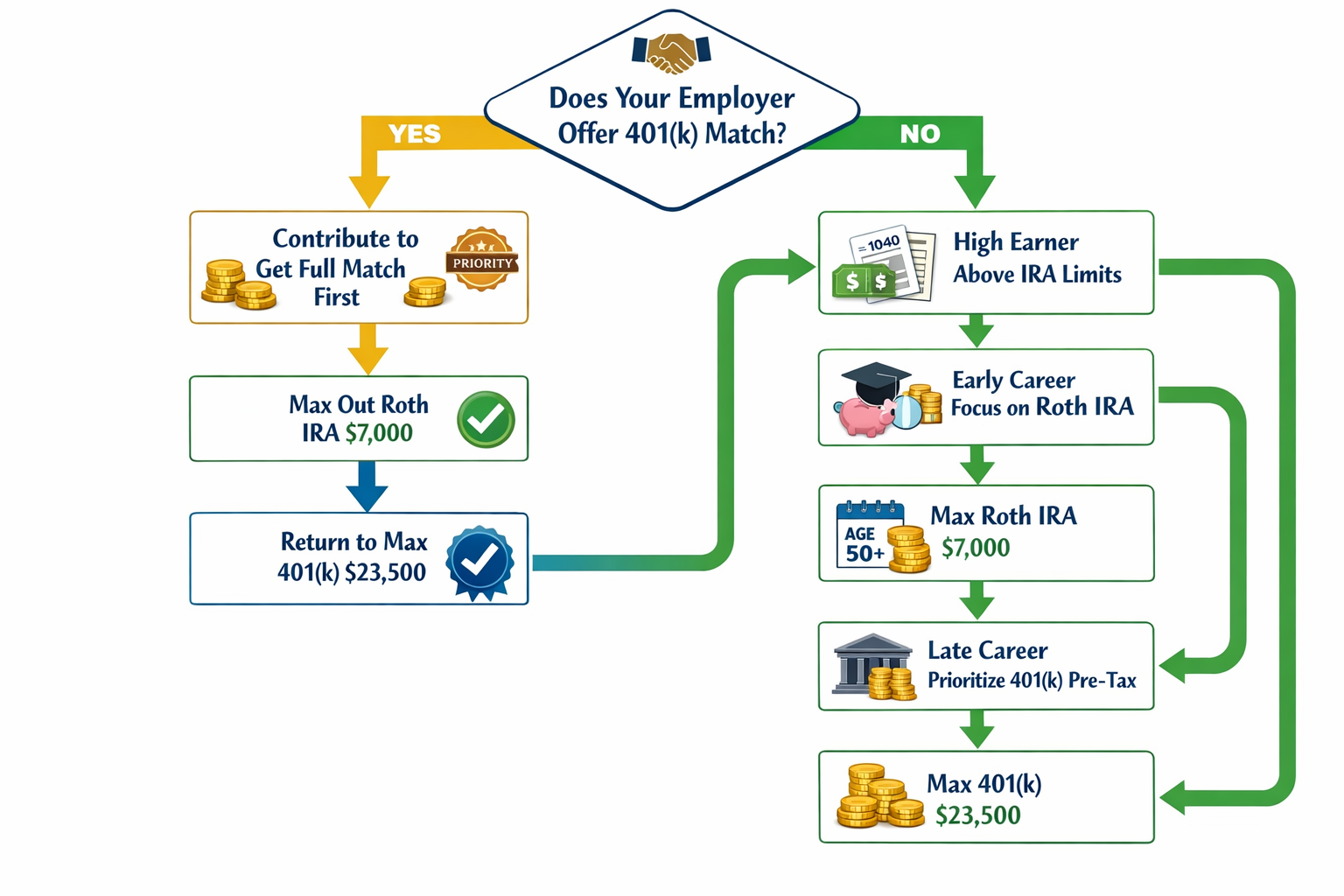

Roth IRA vs 401(k): Which Should You Choose First?

The optimal contribution sequence maximizes both immediate returns (employer match) and long-term tax efficiency.

This decision framework applies to most investors, though individual circumstances may create exceptions.

Employer Match Priority Rule

Step 1: Contribute enough to your 401(k) to capture the full employer match.

This is the highest-return investment available, period.

An employer matching 50% of your contribution up to 6% of your salary delivers an immediate 50% return, guaranteed. No stock, bond, or alternative investment offers this risk-free return.

Example:

- Salary: $60,000

- Employer match: 50% up to 6% of salary

- Minimum contribution to max match: $3,600 (6% of salary)

- Employer adds: $1,800

- Immediate 50% return on $3,600 = $1,800 free money

Even if you prefer Roth taxation, contribute to the traditional 401(k) first to capture this match. The immediate return outweighs tax treatment preferences.

Some employers offer Roth 401(k) options. If available, you can capture the match while using Roth tax treatment; the best of both worlds. Note that employer matching contributions always go into a traditional (pre-tax) account, even when you contribute to a Roth 401(k).

Roth-First Strategy for Beginners

Step 2: Max out your Roth IRA ($7,000 in 2025) after capturing the full employer match.

For most early-to mid-career investors, the Roth IRA becomes the second priority after the employer match because:

Tax rates are likely lower now than later: Early-career professionals typically earn less (and pay lower marginal rates) than they will at peak earnings or in retirement with multiple income sources.

Maximum time for tax-free compounding: Younger investors have 30-40 years for growth, maximizing the value of tax-free earnings.

Withdrawal flexibility: Roth IRA contributions can be accessed without penalty if needed, providing an emergency fund backup while still prioritizing retirement.

Better investment options: Individual Roth IRAs typically offer broader investment selection than employer 401(k) plans, allowing access to low-cost index funds and individual stocks.

No RMDs: Money can remain invested indefinitely without forced withdrawals, maximizing lifetime compound growth.

Example sequence for $65,000 salary:

- Contribute $3,900 to 401(k) (6% to max employer match)

- Contribute $7,000 to Roth IRA (max annual limit)

- If additional savings are available, return to the 401(k) to increase contributions

This sequence captures free money first, then maximizes tax-free growth, then uses remaining savings capacity for additional tax-deferred growth.

High-Income and Late-Career Strategy

Step 3: Return to maximize 401(k) contributions after maxing Roth IRA.

For high earners and late-career investors, the sequence shifts:

High earners above Roth IRA income limits:

- Contribute enough to 401(k) for a full employer match

- Consider a backdoor Roth IRA (contribute to a traditional IRA, immediately convert to Roth)

- Maximize Roth 401(k) or traditional 401(k) to $23,500 limit

- Consider a mega backdoor Roth if the plan allows after-tax contributions

Late-career investors (50+):

- Contribute enough to 401(k) for a full employer match

- Max Roth IRA with catch-up ($8,000 total)

- Max 401(k) with catch-up ($31,000 total)

- Use higher contribution limits to accelerate the final decade of savings

Peak earners (32%+ tax bracket):

- Contribute enough to 401(k) for a full employer match

- Maximize traditional 401(k) to reduce current taxable income

- Consider a Roth IRA if income permits

- Use tax savings to invest in a taxable brokerage for additional diversification

The late-career strategy prioritizes maximum contributions through higher limits and catch-up provisions. With shorter time horizons until retirement, total contribution amounts matter more than tax-free growth duration.

High earners benefit from immediate tax deductions because their current marginal rates (32-37%) likely exceed retirement rates (22-24%), making traditional 401(k) contributions mathematically superior.

This connects to broader budgeting strategies that allocate income across savings, needs, and wants.

Roth IRA vs 401(k): Real-World Examples

Abstract tax calculations matter less than concrete scenarios showing how real people should allocate retirement contributions.

These examples demonstrate the decision framework in action.

Early-Career Worker Example

Profile:

- Age: 26

- Salary: $55,000

- Tax bracket: 12% federal

- Employer match: 100% up to 3% of salary

- Annual savings capacity: $8,000

Optimal strategy:

Step 1: Contribute $1,650 to 401(k) (3% of salary)

- Employer adds $1,650 match

- Total 401(k): $3,300

- Tax savings: $198 (12% of $1,650)

Step 2: Contribute $6,350 to Roth IRA

- Uses remaining savings capacity

- Pays 12% tax now ($762)

- Locks in a low tax rate for decades of growth

Total annual retirement savings: $9,650 ($3,300 in 401(k) + $6,350 in Roth IRA)

Why this works:

The 12% tax bracket is historically low. Paying tax now and never again on decades of compound growth creates enormous value. The employer match provides an immediate 100% return. The Roth IRA contribution grows tax-free for 40+ years.

Projected outcome at age 67 (40 years, 8% average return):

- 401(k) balance: $855,000 (taxable at withdrawal)

- Roth IRA balance: $1,645,000 (completely tax-free)

- After-tax wealth assuming 22% retirement rate: $666,900 + $1,645,000 = $2,311,900

This early-career worker builds over $2.3 million in retirement wealth from consistent $8,000 annual contributions, with 71% completely tax-free.

Mid-Career High Earner Example

Profile:

- Age: 42

- Salary: $180,000

- Tax bracket: 32% federal

- Employer match: 50% up to 6% of salary

- Annual savings capacity: $30,000

Optimal strategy:

Step 1: Contribute $10,800 to traditional 401(k) (6% of salary)

- Employer adds $5,400 match

- Total 401(k): $16,200

- Tax savings: $3,456 (32% of $10,800)

Step 2: Contribute $7,000 to Roth IRA

- Still eligible (income below $230,000 joint filing)

- Pays 32% tax now ($2,240)

- Provides tax diversification

Step 3: Contribute $12,700 to a traditional 401(k)

- Uses remaining savings capacity

- Total 401(k) contribution: $23,500 (2025 max)

- Additional tax savings: $4,064 (32% of $12,700)

Total annual retirement savings: $35,900 ($28,900 in 401(k) + $7,000 in Roth IRA)

Why this works:

The 32% current tax bracket likely exceeds retirement tax rates, making traditional 401(k) contributions valuable. The tax savings ($7,520 annually) can be invested in taxable accounts. The Roth IRA provides tax diversification without sacrificing total contribution volume. The employer match delivers $5,400 in free money.

Projected outcome at age 67 (25 years, 8% average return):

- 401(k) balance: $2,110,000 (taxable at withdrawal)

- Roth IRA balance: $511,000 (completely tax-free)

- After-tax wealth assuming 24% retirement rate: $1,604,000 + $511,000 = $2,115,000

This high earner builds over $2.1 million while reducing current taxable income by $23,500 annually, saving $7,520 in federal taxes each year.

Near-Retirement Scenario

Profile:

- Age: 58

- Salary: $95,000

- Tax bracket: 24% federal

- Employer match: 100% up to 4% of salary

- Annual savings capacity: $25,000

- Current 401(k) balance: $380,000

- Current Roth IRA balance: $85,000

Optimal strategy:

Step 1: Contribute $3,800 to traditional 401(k) (4% of salary)

- Employer adds $3,800 match

- Total 401(k): $7,600

- Tax savings: $912 (24% of $3,800)

Step 2: Max Roth IRA with catch-up contribution ($8,000)

- Provides tax-free income flexibility in early retirement

- Pays 24% tax now ($1,920)

- No RMDs, useful for estate planning

Step 3: Maximize 401(k) catch-up contributions

- Additional $19,700 to reach $31,000 total (age 50+ limit)

- Tax savings: $4,728 (24% of $19,700)

- Accelerates the final years of accumulation

Total annual retirement savings: $42,800 ($35,000 in 401(k) + $8,000 in Roth IRA)

Why this works:

Catch-up contributions allow aggressive final-decade savings. The Roth IRA provides tax-free withdrawal options in early retirement (ages 62-70) before Social Security and RMDs begin. Traditional 401(k) contributions reduce current taxes while maximizing total savings. The employer match continues delivering free money until retirement.

Projected outcome at age 67 (9 years, 7% average return):

- 401(k) balance: $1,038,000 (taxable at withdrawal)

- Roth IRA balance: $252,000 (completely tax-free)

- After-tax wealth assuming 22% retirement rate: $809,640 + $252,000 = $1,061,640

This near-retiree more than doubles their retirement savings in the final decade while creating valuable tax diversification for withdrawal planning.

Can You Use Both a Roth IRA and a 401(k)?

Yes, and most investors should.

Using both account types creates tax diversification that provides valuable flexibility in retirement.

Tax Diversification Strategy

Tax diversification means holding retirement savings in both pre-tax (traditional 401(k)) and after-tax (Roth IRA, Roth 401(k)) accounts.

This strategy delivers three key advantages:

1. Withdrawal flexibility in retirement

Having both account types allows you to strategically choose which account to withdraw from based on annual tax situations.

Example scenario:

- Need $60,000 for living expenses

- Social Security provides $25,000

- Withdraw $20,000 from traditional 401(k) (stays in 12% bracket)

- Withdraw $15,000 from Roth IRA (tax-free, doesn’t increase taxable income)

- Total income: $60,000

- Taxable income: $45,000 (stays in lower bracket)

Versus withdrawing all $35,000 from a traditional 401(k):

- Total income: $60,000

- Taxable income: $60,000 (potentially pushes into higher bracket)

The tax diversification saves money by managing bracket creep and taxable income thresholds.

2. Protection against tax policy uncertainty

Nobody knows what tax rates will be in 20-40 years. Holding both account types protects against both scenarios:

- If rates increase, Roth accounts deliver more value

- If rates decrease, Traditional accounts deliver more value

- Either way, you have options

This is risk management applied to tax planning; diversification reduces dependence on a single outcome.

3. Estate planning advantages

Roth IRAs pass to heirs tax-free and have no RMDs during your lifetime, making them excellent wealth transfer vehicles. Traditional 401(k)s provide current tax deductions and can be strategically depleted in retirement, leaving tax-free Roth assets for heirs.

This connects to broader wealth building principles that balance current needs with long-term legacy goals.

Optimal Contribution Order

The mathematically optimal sequence for most investors:

Priority 1: Employer match (401(k))

- Contribute enough to capture the full match

- Immediate guaranteed return

- Use traditional or Roth 401(k) based on preference

Priority 2: Max Roth IRA

- Contribute $7,000 ($8,000 if 50+)

- Tax-free growth and withdrawals

- Better investment options than most 401(k)s

- Withdrawal flexibility

Priority 3: Max 401(k) contributions

- Increase to $23,500 limit ($31,000 if 50+)

- Higher contribution limits accelerate savings

- Additional tax deductions if using traditional

Priority 4: Taxable brokerage account

- After maxing tax-advantaged space

- Provides pre-retirement access without penalties

- Tax-efficient investments like index funds and qualified dividends

Priority 5: Mega backdoor Roth (if available)

- After-tax 401(k) contributions converted to Roth

- Allows up to $70,000 total annual 401(k) contributions

- Requires specific plan features

This sequence maximizes free money, tax advantages, and total contribution volume in that order.

Exception for high earners: Those in 32%+ tax brackets may prioritize maxing traditional 401(k) before Roth IRA to maximize current tax deductions, then add Roth IRA for diversification if income permits.

Exception for early retirees: Those planning retirement before 59½ may prioritize Roth IRA contributions (accessible without penalty) and Roth conversion ladders for bridge income.

The optimal strategy adapts to individual circumstances, but the general framework, match first, Roth second, max 401(k) third, applies to most investors.

Common Roth IRA vs 401(k) Mistakes to Avoid

Understanding what not to do prevents costly errors that reduce retirement wealth.

Mistake 1: Skipping employer match

Failing to contribute enough to capture full employer matching is leaving free money on the table. This is the single most expensive retirement mistake.

A 50% match on 6% of a $70,000 salary equals $2,100 annually. Over 30 years at 8% return, that’s $244,000 in lost wealth from employer contributions alone.

Mistake 2: Choosing Roth when traditional makes more sense

High earners in peak earning years (32-37% brackets) who expect lower retirement rates benefit more from traditional 401(k) tax deductions.

Paying 35% tax now to avoid 22% tax later is mathematically backwards. The tax savings can be invested to create additional wealth.

Mistake 3: Choosing traditional when Roth makes more sense

Early-career workers in 12% or 22% brackets who expect higher retirement income should use Roth accounts.

Paying 12% tax now and never again on decades of growth creates enormous value. Deferring taxes only to pay higher rates later reduces after-tax wealth.

Mistake 4: Not understanding Roth IRA income limits

High earners who contribute directly to Roth IRAs above income limits ($165,000+ single, $246,000+ joint) face 6% excess contribution penalties annually until corrected[5].

Use backdoor Roth IRA strategies or Roth 401(k)s instead if income exceeds limits.

Mistake 5: Withdrawing early from retirement accounts

Taking early distributions from 401(k)s for non-emergencies triggers 10% penalties plus income taxes, and permanently reduces compound growth potential.

A $20,000 early withdrawal at age 35 costs $2,000 in penalties, $4,400 in taxes (22% bracket), and $216,000 in lost growth by age 65 (8% return over 30 years).

Mistake 6: Ignoring Roth 401(k) options

Many employers now offer Roth 401(k) options that combine high contribution limits with tax-free withdrawals. Ignoring this option means missing the best features of both account types.

Mistake 7: Not rolling over old 401(k)s

Leaving 401(k) accounts at previous employers often means higher fees, limited investment options, and forgotten accounts.

Rolling to an IRA (traditional to traditional IRA, Roth to Roth IRA) provides better investment options and consolidation. This is separate from the Roth conversion decision.

Mistake 8: Failing to rebalance and adjust

Retirement strategy should evolve as income, tax brackets, and life circumstances change. Review annually and adjust contribution types and amounts accordingly.

Mistake 9: Overlooking tax diversification

Putting all retirement savings in one account type (all traditional or all Roth) creates tax risk and reduces flexibility.

Building both pre-tax and after-tax retirement savings provides options regardless of future tax policy.

Mistake 10: Not maximizing catch-up contributions

Investors age 50+ can contribute an extra $7,500 to 401(k)s and $1,000 to Roth IRAs. Failing to use these higher limits in peak earning years reduces total retirement wealth.

🎯 Roth IRA vs 401(k) Priority Calculator

Conclusion

The Roth IRA vs 401(k) decision isn’t about choosing one account over the other—it’s about understanding when to use each one and in what sequence.

The math behind money reveals a clear priority framework:

First, capture every dollar of employer matching through 401(k) contributions. This delivers immediate guaranteed returns that no other investment can match.

Second, fund a Roth IRA to the annual limit if you’re in lower tax brackets or expect higher future rates. This locks in current tax rates and provides decades of tax-free compound growth.

Third, return to maximize 401(k) contributions up to the $23,500 limit (or $31,000 if age 50+) to accelerate total savings through higher contribution limits.

Fourth, consider taxable brokerage accounts and mega backdoor Roth strategies after maxing tax-advantaged space.

The optimal strategy adapts to your specific situation, current income, tax bracket, career stage, and retirement timeline, all matter. But the underlying principle remains constant: maximize free money first, then optimize tax treatment, then maximize contribution volume.

Tax diversification, holding both pre-tax and after-tax retirement accounts, provides valuable flexibility in retirement regardless of future tax policy changes. This is risk management applied to retirement planning.

Actionable next steps:

- Calculate your employer match formula and ensure you’re contributing enough to capture every dollar

- Determine your current marginal tax bracket and expected retirement tax rate to inform Roth vs traditional decisions

- Open a Roth IRA if you don’t have one, and your income permits contributions

- Review your 401(k) investment options and ensure you’re using low-cost index funds aligned with your risk tolerance

- Set up automatic contributions to both accounts to ensure consistent investing regardless of market conditions

- Revisit your strategy annually as income, tax brackets, and life circumstances change

The difference between optimized retirement contributions and random savings can easily exceed $500,000 over a career. The math behind these decisions matters.

Understanding the structural differences between Roth IRAs and 401(k)s, contribution limits, tax treatment, employer matching, withdrawal rules, and RMDs provides the foundation for evidence-based retirement planning.

Both accounts use compound growth to build wealth. Both provide tax advantages. The question is simply when you pay taxes and how much you can contribute. Answer those questions based on data, not assumptions, and your retirement wealth will reflect the precision of your strategy.

Disclaimer

This article provides educational information about retirement account structures and tax treatment based on the 2025 tax law and contribution limits. It is not personalized financial, tax, or investment advice.

Individual circumstances, including income, tax situation, employer plan features, state tax laws, and retirement timeline, significantly impact optimal retirement account strategies. Tax laws change frequently, and future tax rates cannot be predicted with certainty.

Consult with a qualified financial advisor, tax professional, or certified financial planner before making retirement contribution decisions. The author and The Rich Guy Math are not registered investment advisors and do not provide personalized financial advice.

Past performance of investment returns does not guarantee future results. All investments carry risk, including potential loss of principal.

Author Bio

Max Fonji is the founder of The Rich Guy Math, a data-driven financial education platform that explains the math behind money, investing, and wealth building. With a background in financial analysis and a commitment to evidence-based investing principles, Max translates complex financial concepts into clear, actionable insights for investors at all levels.

Max’s approach combines rigorous quantitative analysis with practical application, helping readers understand not just what to do with money, but why specific strategies work based on mathematical principles and historical data. His work focuses on compound growth, valuation frameworks, risk management, and the logical foundations of long-term wealth building.

References

[1] Internal Revenue Service. “Roth IRAs.” IRS.gov, 2025. https://www.irs.gov/retirement-plans/roth-iras

[2] Internal Revenue Service. “401(k) Plans.” IRS.gov, 2025. https://www.irs.gov/retirement-plans/401k-plans

[3] U.S. Congress. “SECURE 2.0 Act of 2022.” Congress.gov, 2022. https://www.congress.gov/bill/117th-congress/house-bill/2954

[4] Internal Revenue Service. “Retirement Plan and IRA Required Minimum Distributions FAQs.” IRS.gov, 2025. https://www.irs.gov/retirement-plans/retirement-plan-and-ira-required-minimum-distributions-faqs

[5] Internal Revenue Service. “Retirement Topics – IRA Contribution Limits.” IRS.gov, 2025. https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-ira-contribution-limits

Frequently Asked Questions

Can I contribute to both a Roth IRA and a 401(k) in the same year?

Yes. The contribution limits are separate and independent. You can contribute up to $23,500 to a 401(k) and $7,000 to a Roth IRA in 2025 (plus catch-up contributions if age 50+), assuming you meet Roth IRA income eligibility requirements.

What happens to my 401(k) if I change jobs?

You generally have four options:

- Leave it with your former employer (if the plan allows)

- Roll it into your new employer’s 401(k)

- Roll it into a traditional IRA or Roth IRA

- Cash it out (not recommended due to taxes and penalties)

Rolling over to an IRA often provides better investment choices and lower fees.

Can I convert my traditional 401(k) to a Roth IRA?

Yes, through a Roth conversion. You’ll owe income tax on the converted amount in the year of conversion, but future growth becomes tax-free.

This strategy is most effective in lower-income years or if you expect higher tax rates in retirement. In-service conversions are only allowed if your employer plan permits them.

Do Roth 401(k) employer matches go into a Roth account?

No. Employer matching contributions always go into a traditional (pre-tax) 401(k), even if your personal contributions are Roth. Taxes will be owed on those matched funds when withdrawn in retirement.

What is the five-year rule for Roth accounts?

Roth IRA earnings are tax-free only after the account has been open for five years and you are age 59½ (or meet another qualifying exception).

Roth 401(k)s have a separate five-year clock. Contributions can always be withdrawn tax-free.

Should I prioritize paying off debt or contributing to retirement accounts?

A common prioritization strategy is:

- Contribute enough to capture full employer 401(k) match

- Pay off high-interest debt (credit cards above ~15%)

- Maximize retirement contributions

- Pay off moderate-interest debt (student loans, auto loans)

The ideal order depends on interest rates, cash flow, and tax brackets.

Can I withdraw from my Roth IRA to buy a house?

Yes. You can withdraw Roth IRA contributions at any time without taxes or penalties. You may also withdraw up to $10,000 of earnings penalty-free for a first-time home purchase, provided the account has been open at least five years.

What is a backdoor Roth IRA?

A backdoor Roth IRA allows high earners to fund a Roth IRA despite income limits. You contribute to a traditional IRA, then convert it to a Roth IRA.

Taxes are owed on any pre-tax amounts converted, and existing IRA balances can trigger the pro-rata rule, making careful execution essential.

Related posts:

What Is SmartPass? Raptor Digital Hall Pass Explained for K-12 Schools

What Is SmartPass? Raptor Digital Hall Pass Explained for K-12 Schools

What Is the 3x Rent Rule & How to Calculate It (With Examples)

What Is the 3x Rent Rule & How to Calculate It (With Examples)

Portfolio Income: Definition, Examples, Tax Rules, and Strategies

Portfolio Income: Definition, Examples, Tax Rules, and Strategies

Tax Filing: A Clear, Step-by-Step Guide for Stress-Free Taxes

Tax Filing: A Clear, Step-by-Step Guide for Stress-Free Taxes

Return on Assets (ROA): Definition, Formula & How to Improve It

Return on Assets (ROA): Definition, Formula & How to Improve It

How to Save Money Fast: A Smart Savings Plan That Actually Works

How to Save Money Fast: A Smart Savings Plan That Actually Works