Imagine earning passive income from stocks you already own, without selling a single share, without timing the market, and without any active effort on your part.

Stock Lending transforms dormant securities in your portfolio into income-generating assets through a simple mechanism: you allow qualified borrowers to temporarily use your shares in exchange for fees. This practice generates billions of dollars annually in the securities lending market, yet most individual investors remain unaware of this wealth-building opportunity sitting idle in their brokerage accounts.

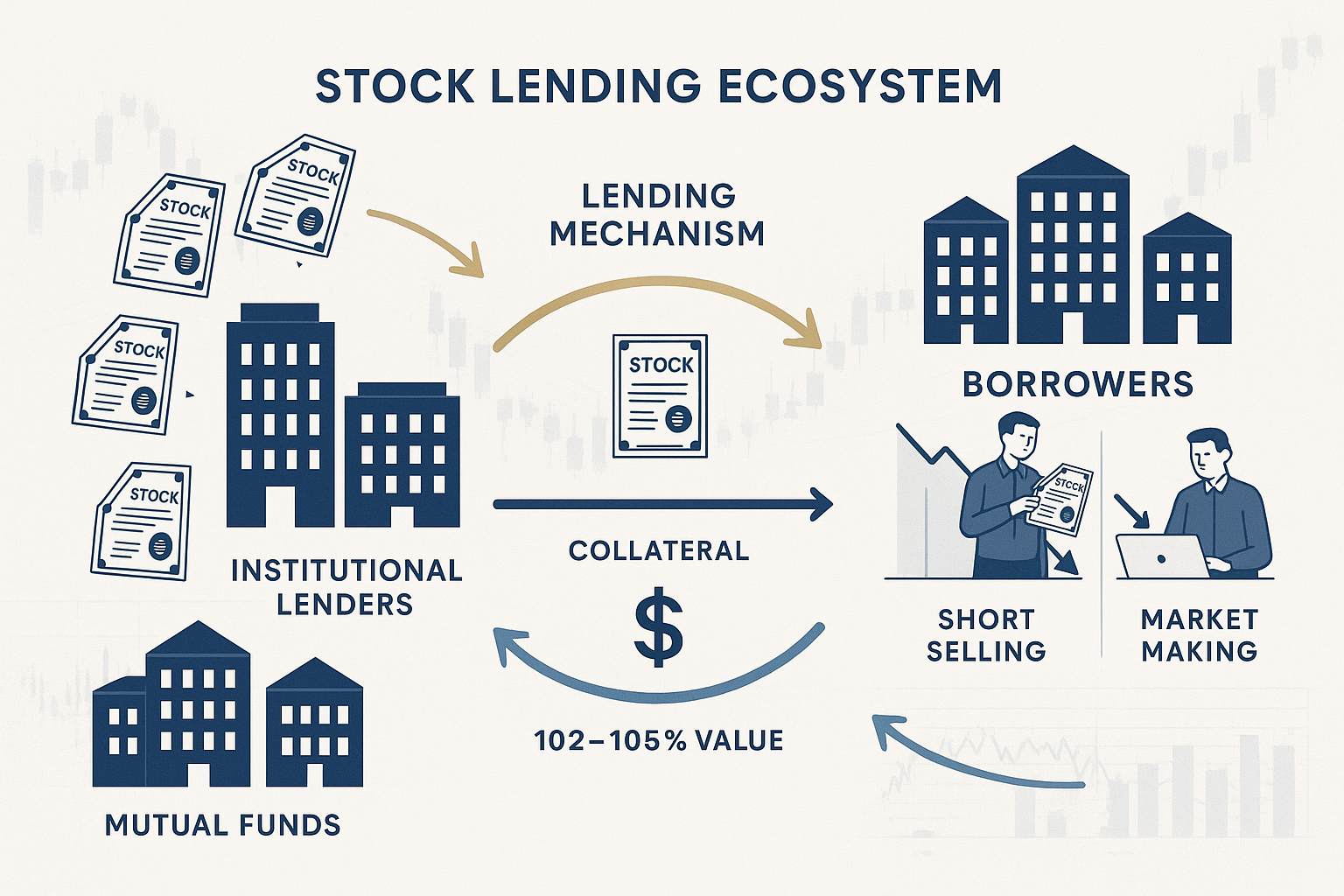

The math behind stock lending reveals a straightforward value exchange. Borrowers need shares for legitimate market activities like short selling and market making. Lenders possess those shares. The result? A fee-based transaction secured by collateral worth more than the borrowed securities; typically 102% to 105% of the loaned shares’ value.

This guide explains the mechanics, income potential, risks, and practical steps for participating in stock lending programs as an individual investor in 2025.

Key Takeaways

Stock lending allows investors to earn passive income by loaning securities to qualified borrowers in exchange for fees, typically split 50/50 with your brokerage.

You maintain ownership and price appreciation rights on loaned shares. If the stock rises 20%, you capture that full gain while earning lending fees.

Borrowers provide collateral worth 102-105% of loaned securities, creating a protective buffer against default risk and ensuring you can recover your shares.

Individual investors access stock lending through fully paid securities lending programs offered by major brokerages, requiring no active management or share selection.

The trade-off involves temporarily losing voting rights on loaned shares, though you retain the ability to sell anytime and continue receiving dividend payments.

What Is Stock Lending?

Stock lending is a financial transaction where securities owners (lenders) temporarily transfer shares to qualified borrowers in exchange for compensation, typically structured as a fee paid monthly or accrued daily as interest.

The practice operates on a simple principle: your shares have value beyond their market price. When certain stocks become difficult to locate, often because many investors want to short them, borrowers will pay substantial fees to access those shares.

The Basic Mechanics

Here’s how the transaction works:

Step 1: A borrower (usually a hedge fund, broker-dealer, or institutional trader) identifies a need for specific securities.

Step 2: The borrower contacts a lending agent or searches a securities lending platform to locate available shares.

Step 3: The lender agrees to loan shares and receives collateral equal to 102% to 105% of the securities’ market value.

Step 4: The borrower pays a lending fee (expressed as an annual percentage) for the duration of the loan.

Step 5: Either party can terminate the arrangement, returning the shares to the lender and the collateral to the borrower.

This cycle continues as long as both parties find the arrangement beneficial. The lending fee fluctuates based on supply and demand; shares that are heavily shorted or hard to locate command higher fees, sometimes exceeding 20% annually for in-demand securities.

Who Participates in Stock Lending?

The securities lending market involves distinct participant categories:

Lenders include:

- Investment companies (mutual funds and ETFs)

- Pension funds and retirement systems

- Sovereign wealth funds

- Insurance companies

- Endowments and foundations

- Individual investors through brokerage programs

Borrowers consist of:

- Hedge funds executing short-sale strategies

- Broker-dealers facilitating market making

- Institutional traders covering failed deliveries

- Arbitrageurs capitalizing on price discrepancies

The Securities and Exchange Commission oversees this market to ensure fair practices and adequate investor protections. According to industry data, the global securities lending market generates approximately $10 billion in annual revenue, with U.S. equity lending representing the largest segment.

Insight: Stock lending represents a mature, regulated market where institutional investors have participated for decades. Individual investor access through brokerage programs democratizes this income opportunity, though the revenue split typically favors brokerages that provide the infrastructure and assume operational risks.

How Stock Lending Generates Income for Investors

The income mechanism in stock lending combines direct fees with potential returns on collateral reinvestment. Understanding both components reveals the complete picture of earning potential.

Primary Income Source: Lending Fees

Borrowers pay fees to access your shares. These fees are expressed as an annual percentage of the securities’ market value and vary dramatically based on several factors:

Supply and demand dynamics drive fee rates. When a stock becomes heavily shorted or difficult to locate, lending fees increase. Conversely, an abundant supply of lendable shares reduces fees.

Typical fee ranges in 2025:

- Low-demand securities: 0.25% to 1.00% annually

- Moderate-demand securities: 1.00% to 5.00% annually

- High-demand securities: 5.00% to 25.00%+ annually

- Exceptional situations: 50.00%+ annually (rare)

Most brokerage programs split these fees between the lender and the brokerage, commonly using a 50/50 split. Some brokerages offer more favorable splits (60/40 or 70/30) to competitive investors or those with larger portfolios.

The Math Behind Stock Lending Income

Let’s calculate realistic earnings using a concrete example:

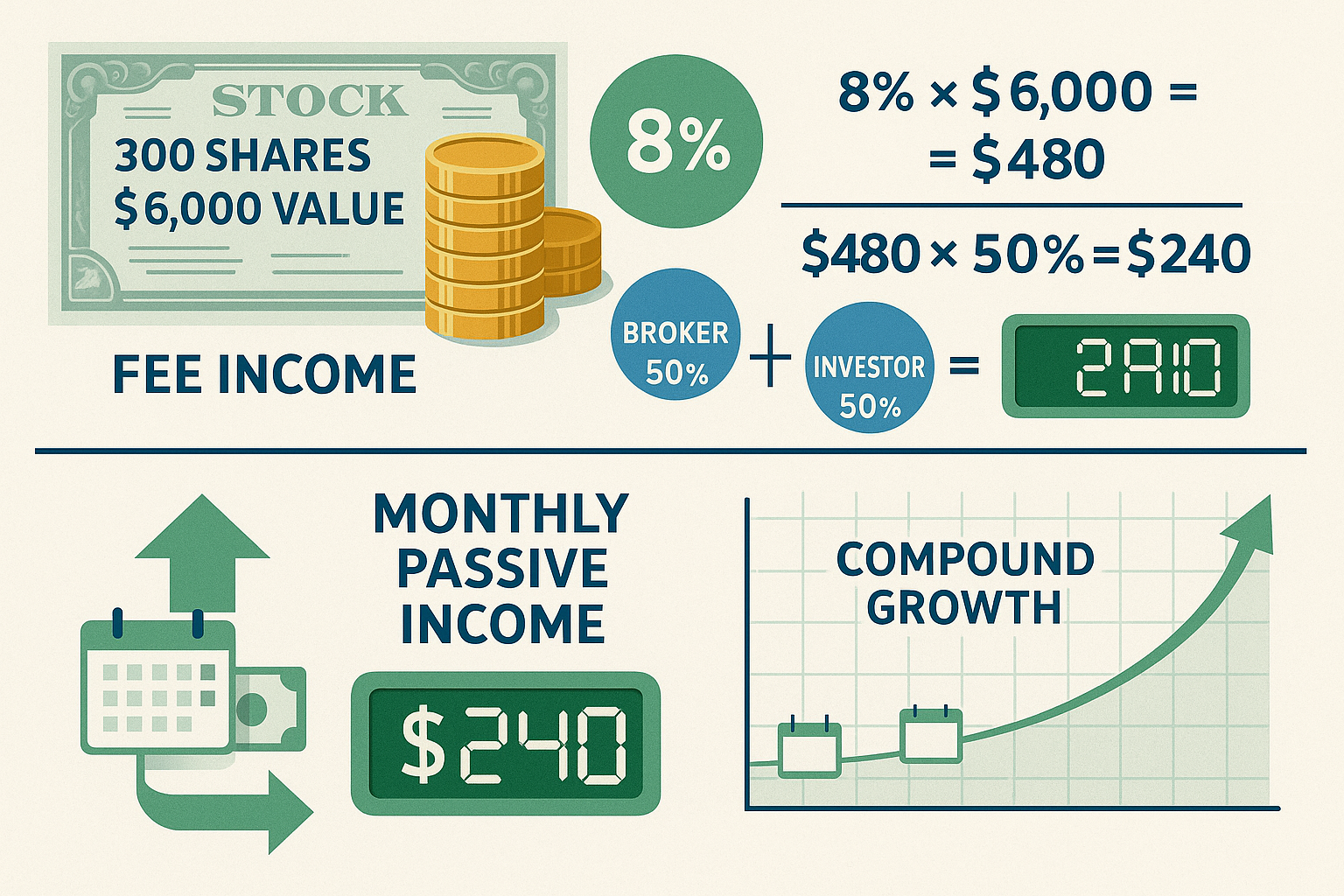

Scenario: You own 300 shares of a stock trading at $20 per share.

- Notional value: 300 shares × $20 = $6,000

- Lending fee rate: 8% annually (moderate demand)

- Gross lending income: $6,000 × 8% = $480 per year

- Revenue split: 50% to you, 50% to brokerage

- Your net income: $480 × 50% = $240 annually

This translates to $20 per month in passive income from shares you already own and plan to hold long-term. The income accrues without requiring any action beyond enrolling in your brokerage’s lending program.

For investors with larger portfolios, the numbers scale proportionally. A $100,000 portfolio earning an average 3% lending fee (after the 50/50 split) generates $1,500 in annual passive income, equivalent to a 1.5% yield enhancement on top of any dividends or capital appreciation.

Secondary Income: Collateral Reinvestment Returns

When borrowers provide cash collateral (rather than securities), lenders can reinvest that cash to generate additional returns. This practice, called “collateral reinvestment,” adds a second income layer.

How it works:

The cash collateral gets invested in short-term, low-risk instruments such as:

- Money market funds

- Treasury bills

- Commercial paper

- Repurchase agreements (repos)

The returns from these investments typically range from 3% to 5% annually in the current interest rate environment. The lender keeps the spread between what they earn on reinvestment and what they pay the borrower as a “rebate” on the collateral.

Example calculation:

- Borrowed securities value: $100,000

- Cash collateral received: $102,000 (102%)

- Reinvestment return: 4.5% annually

- Gross reinvestment income: $102,000 × 4.5% = $4,590

- Rebate paid to borrower: 2.0%

- Rebate amount: $102,000 × 2.0% = $2,040

- Net reinvestment income: $4,590 – $2,040 = $2,550

For individual investors participating through brokerage programs, the brokerage typically manages collateral reinvestment and includes those returns in the overall fee split. This simplifies the process but means you receive a portion of total returns rather than managing reinvestment directly.

Comparing Stock Lending to Other Income Strategies

Stock lending income complements other passive income strategies rather than replacing them:

| Income Strategy | Typical Annual Return | Effort Required | Risk Level |

|---|---|---|---|

| Stock Lending | 0.5% – 3.0% (after split) | None (automated) | Low to Moderate |

| Dividend Stocks | 2.0% – 6.0% | Low (buy and hold) | Moderate |

| Bond Interest | 3.0% – 5.0% | Low | Low to Moderate |

| Covered Calls | 6.0% – 12.0% | Moderate (active management) | Moderate to High |

| Real Estate Income | 4.0% – 8.0% | High (property management) | Moderate to High |

The advantage of stock lending lies in its zero-effort implementation and compatibility with existing long-term holdings. You don’t need to select different securities or alter your investment strategy; you simply activate an income stream from positions you already own.

Insight: Stock lending works best as a portfolio enhancement rather than a primary income strategy. The returns, while modest, require zero active management and don’t interfere with your core investment thesis. Think of it as earning interest on cash sitting in your checking account; it’s not transformative wealth building, but it’s logical to capture available returns on idle assets. For investors focused on compound growth, even small yield enhancements compound significantly over decades.

How Stock Lending Works: The Complete Process

Understanding the operational flow helps investors recognize what happens behind the scenes when they enroll in a securities lending program.

Enrollment and Eligibility

Individual investors access stock lending through fully paid securities lending programs offered by major brokerages. “Fully paid” means you own the shares outright, no margin debt against them.

Enrollment requirements typically include:

- Account minimum (often $25,000 to $250,000, varying by brokerage)

- Agreement to program terms and conditions

- Acknowledgment of risks, particularly voting rights limitations

- Shares held in a cash account or a margin account with no outstanding loans

Once enrolled, the process becomes entirely automated. You don’t select which shares to lend or negotiate terms with borrowers. The brokerage’s lending desk handles all operational aspects.

Share Selection and Loan Initiation

Your brokerage’s securities lending department continuously scans enrolled accounts to identify lendable securities that match borrower demand.

The selection process considers:

- Borrower requests for specific securities

- Current lending fee rates (higher fees prioritized)

- Availability across all enrolled accounts

- Regulatory and operational constraints

When your shares match a borrower’s needs, the brokerage automatically initiates the loan. You receive no notification of individual loan transactions—the activity appears as lending income in your account statements.

This automation ensures efficiency. You don’t need to monitor lending opportunities or make decisions about individual loans. The system optimizes for maximum income generation within your program parameters.

Collateral Requirements and Protection

Borrowers must post collateral to protect lenders against default risk. This requirement creates a fundamental safety mechanism in securities lending.

Collateral standards in the U.S. market:

- Minimum collateral: 102% of borrowed securities’ market value

- Typical collateral: 102% to 105%, depending on security type and volatility

- Mark-to-market: Daily revaluation and collateral adjustments

- Collateral types: Cash (most common) or high-quality securities (government bonds, investment-grade corporate bonds)

The collateral percentage exceeds 100% to create a protective buffer. If the borrowed security increases in value, the borrower must post additional collateral to maintain the required percentage. This daily “marking to market” ensures the collateral always covers the loan value plus the margin.

Example of collateral adjustment:

Day 1:

- Borrowed shares value: $10,000

- Required collateral (102%): $10,200

- Collateral posted: $10,200 ✓

Day 5 (share price increases 10%):

- Borrowed shares value: $11,000

- Required collateral (102%): $11,220

- Previous collateral: $10,200

- Additional collateral needed: $1,020

The borrower must immediately post the additional $1,020 to maintain the loan. Failure to meet margin calls results in loan termination and forced share return.

Fee Calculation and Payment

Lending fees accrue daily based on the borrowed securities’ market value and the agreed-upon annual rate.

Daily fee calculation formula:

Daily Fee = (Market Value × Annual Fee Rate) ÷ 365

Example:

- Borrowed shares value: $50,000

- Annual lending fee: 6%

- Daily fee: ($50,000 × 6%) ÷ 365 = $8.22

These daily fees accumulate in your account, typically paid monthly or quarterly, depending on your brokerage’s schedule. The payment appears as “securities lending income” or a similar designation on your statement.

Because fees are calculated on market value, your income fluctuates with both share price and lending duration. A stock that appreciates while on loan generates higher lending fees—you benefit from both price appreciation and increased fee income.

Loan Termination and Share Return

Either party can terminate a securities loan, typically with minimal notice (often same-day or next-day return).

Common termination triggers:

- The lender decides to sell the shares

- Lender opts out of the lending program

- Lender requests shares back for voting rights

- Borrower no longer needs the shares

- The borrower cannot meet the collateral requirements

- Market conditions make the loan uneconomical

When you sell loaned shares, the transaction executes normally. Your brokerage’s systems automatically recall the necessary shares from borrowers. In the rare situation where shares cannot be immediately recalled, the brokerage typically covers the sale from its own inventory or purchases shares in the market.

This seamless termination process ensures lending doesn’t interfere with your investment decisions. You maintain complete liquidity and trading flexibility despite having shares on loan.

Insight: The operational complexity of securities lending remains invisible to participating investors. Brokerages handle borrower relationships, collateral management, fee calculations, and loan logistics. This infrastructure investment by brokerages justifies their revenue split—they provide the platform, assume operational risks, and manage regulatory compliance while you simply collect passive income from holdings you planned to keep long-term anyway.

Rights, Risks, and Considerations in Stock Lending

Every financial decision involves trade-offs. Stock lending offers income benefits but requires understanding what you temporarily give up and what risks you accept.

What You Keep: Ownership and Economic Rights

Participating in stock lending does not transfer ownership of your securities. You remain the legal owner with several important rights intact:

✓ Price appreciation rights: If your loaned stock increases from $50 to $75, you capture the full $25 gain. The borrower holds the shares but doesn’t benefit from price increases—in fact, they experience a loss if they’re short-selling.

✓ Ability to sell anytime: You can sell loaned shares whenever you choose. The lending agreement terminates for shares you sell, with no restrictions, penalties, or delays on your trading activity.

✓ Dividend payments: You continue receiving dividend payments on loaned securities. The mechanics differ slightly (discussed below), but economically, you receive the same cash flow.

✓ Portfolio value: Your account value reflects the full market value of loaned securities. The shares don’t disappear from your portfolio—they’re simply marked as “on loan” in the brokerage’s systems.

These preserved rights mean stock lending doesn’t fundamentally alter your investment position. You maintain the economic exposure to your chosen securities while earning additional income.

What You Temporarily Lose: Voting Rights

The primary trade-off in stock lending involves voting rights. When shares are on loan, the borrower holds the shares on the record date and therefore receives voting rights for shareholder meetings.

This limitation matters differently depending on your investment approach:

For passive index investors: Voting rights typically hold minimal practical value. Most index fund investors don’t actively participate in corporate governance or attend shareholder meetings.

For active investors in individual stocks: Losing votes on important matters (board elections, merger approvals, executive compensation) may conflict with your investment thesis, particularly if you hold concentrated positions in companies where governance matters.

For ESG-focused investors: Environmental, Social, and Governance investors often view voting rights as essential to influencing corporate behavior. Stock lending conflicts with this objective.

The solution: Most lending programs allow you to recall shares before record dates to regain voting rights. You can opt out temporarily for specific securities when important votes approach, then re-enroll after exercising your voting rights.

This flexibility means voting rights aren’t permanently lost; you simply need to actively manage the trade-off between lending income and voting participation.

Dividend Treatment and Tax Implications

Dividends on loaned securities receive special treatment that creates potential tax consequences.

How dividend payments work:

When a company pays a dividend on loaned shares, the borrower receives the dividend payment (they hold the shares on the record date). However, the borrower must immediately pay an equivalent amount to the lender, called a “payment instead of dividend” or “substitute payment.”

The tax difference:

- Qualified dividends: Taxed at favorable long-term capital gains rates (0%, 15%, or 20% depending on income)

- Payments in lieu: Taxed as ordinary income (up to 37% for high earners in 2025)

This tax treatment difference can significantly impact after-tax returns, particularly for investors in high tax brackets holding dividend-paying stocks.

Example comparison:

Investor in 24% ordinary income tax bracket and 15% qualified dividend rate:

- Qualified dividend: $1,000

- Tax on qualified dividend: $150

- After-tax income: $850

Same investor receiving payment in lieu:

- Payment in lieu: $1,000

- Tax on ordinary income: $240

- After-tax income: $760

- Tax cost difference: $90 (10.6% reduction in after-tax income)

For investors holding high-dividend stocks in taxable accounts, this tax impact can exceed the lending fee income, creating a net negative result.

Mitigation strategies:

- Focus lending programs on growth stocks with minimal dividends

- Concentrate dividend stocks in tax-advantaged accounts (IRAs, 401(k)s) where tax treatment differences don’t matter

- Recall shares before the dividend record dates for high-dividend positions

- Calculate whether lending income exceeds the tax cost before enrolling in dividend-heavy portfolios

Understanding capital gains tax implications helps investors make informed decisions about which accounts and securities to include in lending programs.

Counterparty and Operational Risks

While collateral requirements provide substantial protection, stock lending involves risks that prudent investors should understand:

Borrower default risk: If a borrower fails and cannot return shares, the lender must rely on the collateral. The 102-105% collateral requirement provides a buffer, but in extreme market conditions (rapid price movements, market crashes), collateral might prove insufficient.

Brokerage indemnification: Most major brokerages indemnify (insure) their lending programs, meaning they guarantee to make lenders whole if borrower default results in losses. This protection transfers risk from individual investors to the brokerage, but it depends on the brokerage’s financial strength.

Regulatory risk: Changes in securities lending regulations could affect program economics, tax treatment, or operational requirements. The SEC periodically reviews securities lending practices and may impose new restrictions.

Reinvestment risk: When brokerages reinvest cash collateral, poor investment choices could result in losses. The 2008 financial crisis saw some securities lending programs suffer losses when collateral was invested in mortgage-backed securities that declined in value.

Liquidity risk: In extreme market stress, recalling loaned shares might take longer than normal, potentially delaying your ability to sell. While rare, this scenario occurred during the 2021 “meme stock” volatility when some hard-to-borrow securities couldn’t be immediately recalled.

These risks remain relatively low for investors using established brokerages with robust lending programs and strong indemnification policies. However, they’re not zero—understanding them allows for informed decision-making.

Is Stock Lending Right for Your Portfolio?

Stock lending fits specific investor profiles better than others:

Good candidates for stock lending:

- Long-term buy-and-hold investors who rarely trade

- Investors holding positions in tax-advantaged accounts

- Portfolios concentrated in growth stocks with minimal dividends

- Investors who don’t actively participate in shareholder voting

- Those seeking to enhance returns on stable, core holdings

Poor candidates for stock lending:

- Active traders who frequently buy and sell

- Investors holding high-dividend stocks in taxable accounts

- ESG investors prioritizing corporate governance participation

- Those holding concentrated positions where voting rights matter

- Investors are uncomfortable with any counterparty risk

The decision ultimately depends on your investment philosophy, tax situation, and comfort with the trade-offs involved. For many passive investors following evidence-based investing principles, stock lending represents a logical enhancement to long-term holdings.

Insight: Stock lending doesn’t suit every investor or every portfolio. The key is matching the strategy to your specific circumstances. Calculate the after-tax income potential, consider your voting preferences, and evaluate whether the modest yield enhancement justifies the administrative complexity and risk trade-offs. For investors with substantial holdings in tax-advantaged accounts who don’t actively engage in corporate governance, stock lending often provides attractive risk-adjusted returns with minimal downside.

How to Participate in Stock Lending as an Individual Investor

Accessing stock lending as an individual investor requires selecting the right brokerage and understanding program specifics.

Major Brokerages Offering Securities Lending Programs

Several established brokerages provide fully paid securities lending programs to individual investors in 2025:

Fidelity Investments offers its Fully Paid Lending Program with:

- $250,000 minimum account value

- 50/50 revenue split

- Cash or non-cash collateral at 102-105%

- No fees to participate

- Ability to opt out anytime

Interactive Brokers provides its Stock Yield Enhancement Program, featuring:

- $50,000 minimum account value (among the lowest)

- 50/50 revenue split (can improve to 85/15 for large accounts)

- Real-time lending rate visibility

- Detailed reporting on loaned positions

- Granular control over which securities to lend

E*TRADE (Morgan Stanley) offers securities lending through:

- $250,000 minimum account value

- 50/50 revenue split

- Automated enrollment and management

- Indemnification against borrower default

- Integration with existing account features

Charles Schwab provides its Schwab Stock Lending Program with:

- $250,000 minimum account value

- 50/50 revenue split

- Full indemnification coverage

- Ability to exclude specific securities

- Quarterly income payments

TD Ameritrade (now part of Charles Schwab) historically offered lending programs that are being integrated into Schwab’s platform following the merger.

Each program has distinct features, minimums, and terms. Comparing options helps identify the best fit for your portfolio size and preferences.

Enrollment Process and Requirements

Enrolling in a securities lending program typically follows these steps:

Step 1: Verify eligibility

- Confirm your account value meets the minimum threshold

- Ensure you hold securities outright (fully paid, no margin loans against them)

- Review which account types are eligible (individual, joint, trust, IRA, etc.)

Step 2: Review program documents

- Read the securities lending agreement carefully

- Understand the revenue split, collateral requirements, and risks

- Note any fees (most programs charge no fees to participants)

- Clarify the indemnification policy

Step 3: Complete enrollment

- Submit the enrollment form (usually available online)

- Specify any securities you want to exclude from lending

- Set preferences for notifications and reporting

- Acknowledge understanding of voting rights limitations

Step 4: Monitor and manage

- Review monthly or quarterly statements showing lending activity

- Track income from securities lending separately from dividends and capital gains

- Adjust excluded securities if your priorities change

- Opt out temporarily before important shareholder votes

The entire process typically takes 10-15 minutes online, with program activation occurring within a few business days.

Maximizing Income While Managing Risks

Strategic approaches help optimize lending income while controlling downsides:

Strategy 1: Segment by account type

Concentrate lending in tax-advantaged accounts (IRAs, 401(k)s, Roth IRAs) where substitute dividend payments don’t create adverse tax consequences. Keep high-dividend stocks in taxable accounts outside the lending program.

Strategy 2: Focus on growth stocks

Growth companies that pay minimal or no dividends make ideal lending candidates. You earn lending fees without the tax penalty of substitute dividend payments. Technology stocks, biotech companies, and growth-oriented ETFs often fit this profile.

Strategy 3: Exclude voting-critical positions

If you hold concentrated positions in companies where you want to exercise voting rights, exclude those specific securities from the lending program. You can still lend the remainder of your portfolio while maintaining governance participation where it matters most.

Strategy 4: Monitor lending rates

Some brokerages (particularly Interactive Brokers) provide transparency into current lending rates for specific securities. If you notice certain holdings consistently command high lending fees, you might prioritize holding those positions in your lending-enabled account.

Strategy 5: Understand the revenue split negotiation

Larger accounts sometimes qualify for more favorable revenue splits. If you have a substantial portfolio ($1 million+), ask your brokerage about improved terms. Interactive Brokers, for example, offers tiered splits up to 85/15 for very large accounts.

Strategy 6: Calculate your effective return

Periodically calculate your actual after-tax return from securities lending:

Effective Return = (Lending Income – Tax Cost of Substitute Dividends) ÷ Portfolio Value

If this calculation shows minimal or negative returns, reconsider your participation or adjust which securities you lend.

Alternatives to Direct Stock Lending Programs

Investors below minimum thresholds or preferring indirect participation have alternatives:

ETF lending revenue: Many ETFs participate in securities lending and pass a portion of revenue to shareholders through reduced expense ratios. You benefit indirectly without enrolling in a program. Large-cap index ETFs commonly engage in lending, generating 0.05% to 0.15% in additional returns that offset management costs.

Mutual fund lending: Similar to ETFs, mutual funds often lend securities and retain the revenue to reduce fund expenses. Shareholders benefit through improved fund performance, though the impact is less transparent than direct lending programs.

Robo-advisor programs: Some robo-advisors offer securities lending as an optional feature for larger accounts, handling all logistics automatically within your managed portfolio.

These indirect approaches provide exposure to lending economics without the administrative requirements or minimum account values of direct programs.

Insight: Starting with securities lending requires minimal effort but benefits from strategic thinking. The default approach—enrolling your entire portfolio in a 50/50 split program—works adequately for many investors. However, thoughtful segmentation by account type, security characteristics, and tax implications can meaningfully improve after-tax returns. Treat securities lending as one component of a comprehensive wealth building strategy rather than a standalone tactic, and ensure the income generated justifies any operational complexity or risk trade-offs you accept.

Stock Lending in the Broader Investment Context

Understanding where stock lending fits within comprehensive financial planning helps investors allocate attention and capital appropriately.

Comparing Returns to Core Investment Strategies

Stock lending generates modest supplemental income but doesn’t replace fundamental wealth-building strategies:

Primary wealth drivers:

- Equity appreciation: Historical average of 10% annually (S&P 500 long-term average)

- Dividend reinvestment: Adds 2-6% annually, depending on strategy

- Compound growth: The exponential effect of reinvesting returns over decades

Secondary enhancements:

- Stock lending: Adds 0.5-3% annually (after revenue split and taxes)

- Tax-loss harvesting: Saves 0.2-1% annually through strategic realization of losses

- Expense ratio optimization: Saves 0.5-1% annually by choosing low-cost funds

The mathematics of compound interest demonstrates that primary wealth drivers deserve the majority of investor attention and effort. A 1% annual enhancement from stock lending, while valuable, pales in comparison to the impact of maintaining a disciplined investment strategy through market cycles.

30-year compound growth comparison on $100,000:

| Strategy | Annual Return | 30-Year Value | Difference |

|---|---|---|---|

| Base portfolio | 8.0% | $1,006,266 | Baseline |

| + Stock lending (1%) | 9.0% | $1,326,768 | +$320,502 |

| + Stock lending (2%) | 10.0% | $1,744,940 | +$738,674 |

Even a modest 1-2% enhancement compounds to substantial additional wealth over investment lifetimes. This justifies including stock lending in your toolkit while maintaining perspective on its role as a supplement rather than a foundation.

Integration with Passive Income Strategies

Stock lending complements other passive income approaches:

Dividend investing: Combine stock lending with dividend growth stocks by lending non-dividend-paying growth positions while keeping dividend aristocrats outside the program to avoid substitute payment tax treatment.

Index fund investing: Enhance returns on core index fund holdings through lending programs, particularly for positions you plan to hold indefinitely, regardless of market conditions.

REIT holdings: Real estate investment trusts often generate substantial dividends, making them poor candidates for lending in taxable accounts. However, REITs held in IRAs work well in lending programs since tax treatment doesn’t matter in tax-deferred accounts.

Bond portfolios: While less common, some lending programs accept high-quality bonds. The lending fees on bonds typically run lower than equities, but every incremental return contributes to total portfolio performance.

The key is viewing stock lending as one component of a diversified income strategy rather than a complete solution. Combining multiple passive income sources creates resilience and reduces dependence on any single mechanism.

Risk Management and Portfolio Construction

Stock lending introduces minimal additional risk when implemented thoughtfully:

Diversification principle: Don’t concentrate lending in a few positions. Broad-based lending across many securities reduces the impact if any individual borrower defaults or any specific security experiences lending-related complications.

Collateral verification: Choose brokerages with strong indemnification policies and robust risk management. The brokerage’s financial strength matters; you’re relying on their guarantee if borrower default occurs.

Liquidity maintenance: Ensure your portfolio maintains adequate liquidity outside loaned positions. While you can sell loaned shares anytime, extreme market conditions could theoretically delay recalls. Maintaining cash reserves prevents forced selling during volatility.

Tax efficiency: Structure lending to minimize tax drag. This often means concentrating lending in tax-advantaged accounts or limiting taxable account lending to non-dividend-paying securities.

These risk management principles align with broader portfolio construction best practices. Stock lending shouldn’t require abandoning sound investment principles—it should integrate seamlessly with existing strategies.

The Role of Financial Education

Understanding stock lending demonstrates the value of comprehensive financial literacy. Most investors miss opportunities like securities lending simply because they don’t know such programs exist.

Continuous learning priorities for 2025:

- Investment fundamentals: Master investing fundamentals before pursuing advanced strategies

- Tax optimization: Understand how different income types are taxed, and structure accounts accordingly

- Fee awareness: Recognize how fees and expenses compound negatively over time

- Risk assessment: Develop frameworks for evaluating risk-return trade-offs across strategies

Stock lending represents one example of the “math behind money”—understanding the quantitative relationships that drive financial outcomes. Investors who develop this analytical mindset consistently identify opportunities others miss and avoid pitfalls that derail wealth accumulation.

The 4% rule for retirement withdrawals, dollar-cost averaging for systematic investing, and stock lending for yield enhancement all share a common foundation: mathematical frameworks that guide decision-making based on evidence rather than emotion.

Insight: Stock lending fits within a comprehensive wealth-building framework as a modest but meaningful enhancement to long-term holdings. It doesn’t replace disciplined saving, strategic asset allocation, or patient capital appreciation as primary wealth drivers. Instead, it represents the type of optimization that separates investors who achieve financial independence from those who merely participate in markets. The difference between a good financial outcome and an excellent one often comes from consistently implementing small improvements across multiple dimensions—and stock lending represents one such improvement available to investors willing to understand its mechanics and trade-offs.

📊 Stock Lending Income Calculator

Calculate your potential passive income from securities lending based on portfolio value, lending rates, and revenue split

Income Breakdown

Conclusion

Stock lending transforms idle securities into income-generating assets through a straightforward mechanism: qualified borrowers pay fees to temporarily access your shares, secured by collateral worth more than the borrowed securities.

The mathematics support participation for appropriate investor profiles. A $100,000 portfolio earning a conservative 1.5% after-split lending income generates $1,500 annually—$12,500 over a decade, $37,500 over 25 years—without requiring any active management or altering your investment strategy.

The decision framework:

✓ Consider stock lending if you:

- Hold long-term positions you rarely trade

- Maintain substantial holdings in tax-advantaged accounts

- Own growth stocks with minimal dividends

- Don’t actively participate in shareholder voting

- Seek modest yield enhancement on stable holdings

✗ Avoid or limit stock lending if you:

- Trade frequently or maintain short holding periods

- Hold high-dividend stocks primarily in taxable accounts

- Prioritize voting rights and corporate governance participation

- Feel uncomfortable with any counterparty risk

- Have portfolio values below program minimums

The evidence suggests that stock lending represents a logical optimization for passive investors following evidence-based investing principles. It doesn’t require abandoning sound investment fundamentals or accepting outsized risks. Instead, it captures available returns from an existing asset, similar to earning interest on cash balances or reinvesting dividends for compound growth.

Action steps to begin:

- Evaluate your eligibility: Check whether your portfolio value meets minimum thresholds at major brokerages ($50,000 to $250,000).

- Calculate potential income: Use the calculator above to estimate realistic earnings based on your portfolio size and typical lending rates.

- Consider tax implications: Determine whether substitute dividend payments would create adverse tax consequences in your specific situation.

- Compare brokerage programs: Review terms, revenue splits, and indemnification policies across Fidelity, Interactive Brokers, Schwab, and E*TRADE.

- Start strategically: Begin with tax-advantaged accounts and non-dividend-paying securities to optimize after-tax returns.

- Monitor and adjust: Review quarterly statements to track lending income and adjust excluded securities based on changing priorities.

Stock lending won’t revolutionize your financial situation, but it represents the type of incremental optimization that separates good outcomes from excellent ones over investment lifetimes. The math behind money rewards those who consistently implement small improvements across multiple dimensions—and stock lending offers one such improvement available to investors willing to understand its mechanics.

The opportunity exists. The infrastructure is established. The risks are manageable. The decision is yours.

References

[1] Securities Lending Times. (2024). “Global Securities Lending Market Revenue Report.” Industry Analysis. www.securitieslendingtimes.com

[2] U.S. Securities and Exchange Commission. (2023). “Securities Lending by U.S. Open-End and Closed-End Investment Companies.” Investor Bulletin. https://www.sec.gov/investor/pubs/securitieslending.htm

[3] Financial Industry Regulatory Authority (FINRA). (2025). “Understanding Securities Lending.” Investor Education. https://www.finra.org/investors/insights/securities-lending

[4] Federal Reserve Bank of New York. (2023). “Securities Lending and the Run on Repo.” Staff Report on Market Structure. www.newyorkfed.org

Author Bio

Max Fonji is a data-driven financial educator and the voice behind The Rich Guy Math, where he explains the mathematical principles that drive wealth building, investing, and financial independence. With expertise in valuation analysis, portfolio construction, and evidence-based investing strategies, Max translates complex financial concepts into clear, actionable frameworks that empower investors to make informed decisions. His work focuses on teaching the cause-and-effect relationships in finance—helping readers understand not just what to do, but why it works and how to measure results.

Educational Disclaimer

This article provides educational information about stock lending and should not be construed as personalized financial, investment, or tax advice. Securities lending involves risks, including potential loss of voting rights, adverse tax treatment of substitute dividend payments, and counterparty default risk. Past performance does not guarantee future results. Lending fee rates vary significantly based on market conditions, security demand, and brokerage terms.

Individual circumstances differ substantially in terms of tax situations, investment objectives, risk tolerance, and financial goals. Before participating in any securities lending program, consult with qualified financial advisors, tax professionals, and legal counsel who can evaluate your specific situation and provide personalized recommendations.

The Rich Guy Math and its authors do not receive compensation from brokerages mentioned in this article and maintain editorial independence in all content. All data, calculations, and examples are provided for illustrative purposes only.

Investing involves risk, including possible loss of principal. Always conduct thorough due diligence and understand all terms, conditions, and risks before making financial decisions.

Frequently Asked Questions About Stock Lending

Can I lose my shares if I participate in stock lending?

No, you cannot permanently lose ownership of your shares through securities lending. Borrowers must post collateral worth 102–105% of your loaned securities’ value, which protects you against default. Most major brokerages also provide indemnification guarantees, ensuring you will be made whole if a borrower fails to return shares. You maintain legal ownership throughout the lending period and can terminate the loan at any time.

How does stock lending affect my ability to sell shares?

Stock lending does not restrict your ability to sell shares. You can place a sell order at any time, just as you would with non-loaned securities. When you sell, your brokerage automatically recalls the necessary shares from borrowers. In the rare event the recall cannot be completed immediately, the brokerage will typically fill your sale from its inventory or buy shares on the market to complete your order.

What happens to dividends on loaned stocks?

You still receive dividend payments, but through a different mechanism. The borrower receives the actual dividend but must pay you an equivalent amount called a “payment in lieu of dividend.” The cash amount is the same, but taxes differ — payments in lieu are taxed as ordinary income instead of qualified dividends, which can result in a higher tax liability.

Do I need a large portfolio to participate in stock lending?

Most brokerages require minimum account values ranging from $50,000 to $250,000 for enrollment in their securities lending programs. Interactive Brokers offers one of the lowest minimums at $50,000, while Fidelity, Schwab, and E*TRADE usually require $250,000. Investors with smaller portfolios can still benefit indirectly through ETFs and mutual funds that lend securities and reduce expense ratios as a result.

Is stock lending safe for long-term investors?

Stock lending is generally considered low risk when conducted through reputable brokerages offering strong indemnification policies. Collateral requirements (102–105% of the stock’s value) provide protection, and brokerages guarantee to compensate you if a borrower defaults. The main considerations are temporary loss of voting rights and differing tax treatment on dividends. For long-term investors, especially in tax-advantaged accounts, stock lending can be a safe way to earn passive income.

How much can I realistically earn from stock lending?

Most investors earn between 0.5% and 3% of their portfolio value annually after revenue splits and taxes. Earnings depend on which stocks you hold, demand for shorting those stocks, your brokerage’s revenue share (often 50/50), and your tax bracket. For example, a $100,000 portfolio may generate $500 to $3,000 per year. Hard-to-borrow stocks can produce significantly higher yields, though such opportunities are uncommon and unpredictable.