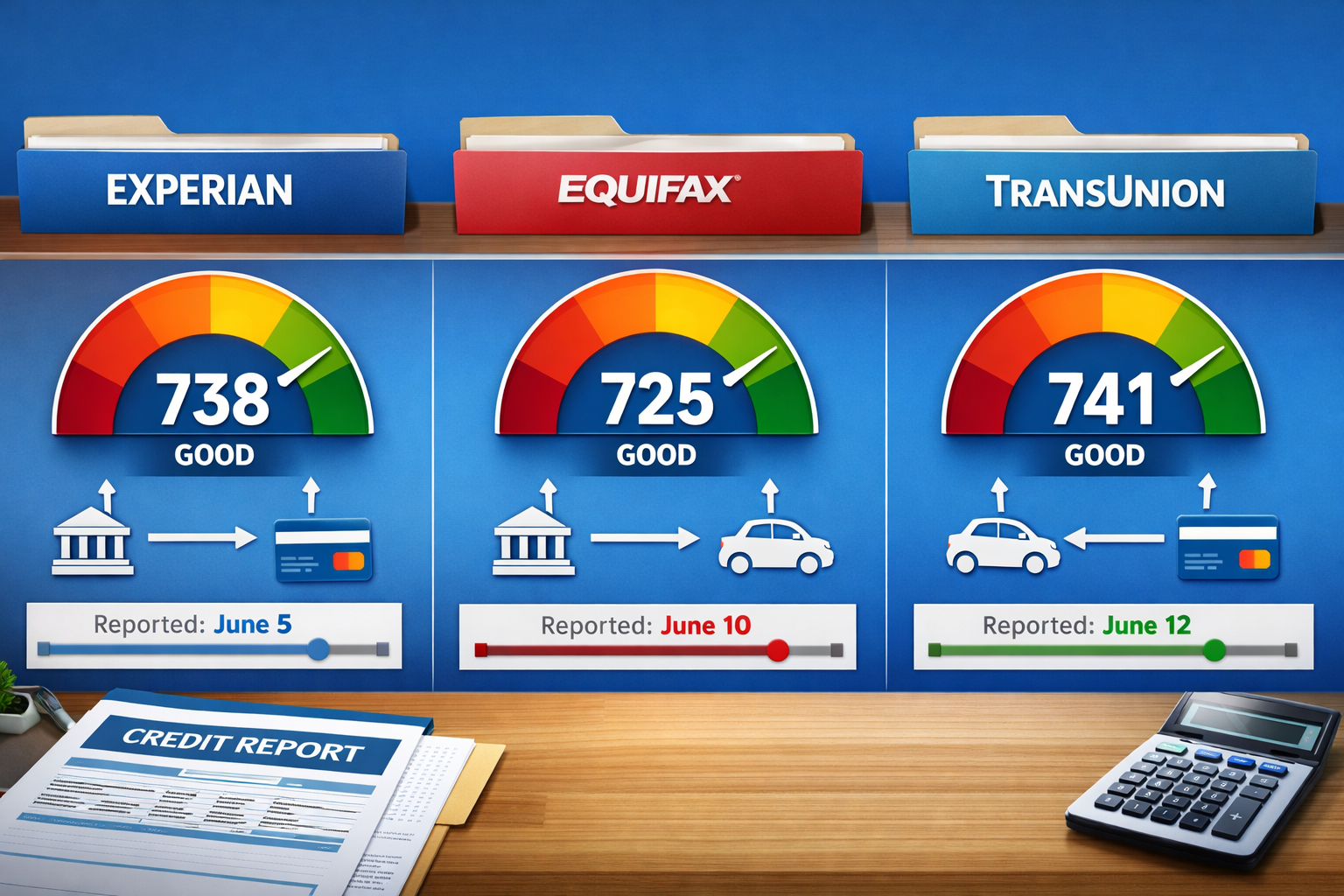

You check your credit score through your bank app and see 740. Then you check through another service and see 722. A mortgage lender pulls your score and tells you it’s 731. Three different numbers, supposedly about the same person. What’s going on?

Here’s the answer: banks don’t create your credit score. Credit bureaus do, and there are three major ones in the United States, each collecting data independently. A credit bureau is a company that collects and organizes your borrowing and repayment history, then shares that information with lenders who want to evaluate your risk. They are record keepers, not lenders. They don’t approve or deny anything.

In this guide, you’ll learn exactly what credit bureaus do, how they affect loan approvals, and why your scores differ across all three. By the end, the math behind money and credit will make a lot more sense.

Key Takeaways

Credit bureaus are private companies (Experian, Equifax, and TransUnion) that collect your borrowing data and sell it to lenders. They are not government agencies.

They don’t approve or deny loans. They provide the information; lenders make the decisions.

Your three credit reports can differ because not all lenders report to all three bureaus, and reporting timelines vary.

You can check all three reports for free once per year at AnnualCreditReport.com, and errors can be disputed directly with each bureau.

Your behavior drives your report, your report drives your score, and your score influences approvals. Managing the data recorded about you is the real path to financial literacy and better credit outcomes.

What a Credit Bureau Is

A credit bureau (also called a consumer reporting agency) is a company that collects financial data about how you borrow and repay money. It gathers this data from lenders, credit card companies, and other financial institutions. It then compiles that data into a credit report, which is essentially your financial track record.

Lenders, landlords, and other businesses purchase these reports to evaluate how risky it would be to extend credit to you. The bureaus do not make lending decisions. They do not approve or deny your applications. They simply organize and distribute the data. Think of them as financial librarians: they catalog the information, but they don’t write the books

The Three Major Credit Bureaus

The United States has three major credit bureaus: Experian, Equifax, and TransUnion. All three are private, for-profit companies. This is a common misconception worth clearing up immediately: they are not government agencies, and they are not regulated as public utilities. They operate as independent businesses competing in the consumer data industry [4].

Experian

Experian is headquartered in Dublin, Ireland, with major U.S. operations in Costa Mesa, California. It is one of the largest consumer credit reporting companies in the world, maintaining credit data on hundreds of millions of consumers globally. Experian also offers credit monitoring, identity protection, and data analytics services.

Equifax

Equifax is based in Atlanta, Georgia, and has been in operation since 1899, making it the oldest of the three bureaus. Equifax collects data on over 800 million consumers worldwide. It made headlines in 2017 after a massive data breach exposed the personal information of approximately 147 million Americans, which led to significant industry reforms around data security.

In 2026, Equifax is also playing a notable role in the mortgage credit scoring landscape. It is offering VantageScore 4.0 at $4.50 per score through 2027 and providing free VantageScore 4.0 access through the end of 2026 for customers who also purchase FICO scores [5].

TransUnion

TransUnion is headquartered in Chicago, Illinois. It maintains credit records on roughly 1 billion consumers in over 30 countries. Like its competitors, TransUnion provides credit reports, credit scores, and fraud prevention tools. TransUnion is similarly offering VantageScore 4.0 for mortgage purposes at competitive rates as the industry adjusts to rising FICO pricing [7].

Insight: Because each bureau operates independently, they may have slightly different data about you. No single bureau has a “more official” or “more accurate” version of your credit history. All three matter.

What Credit Bureaus Actually Do

Credit bureaus collect, organize, and distribute consumer credit data. That’s the core function. But understanding how they get that data is important.

Data Furnishers

The companies that send your account information to the bureaus are called data furnishers. These include:

Credit card issuers (Chase, Capital One, Discover, etc.)

Each month, data furnishers send updated information about your accounts to one, two, or all three bureaus. This includes your current balance, whether your payment was on time, your credit limit, and your account status (open, closed, in collections).

The Reporting Cycle

Most data furnishers report to the bureaus on a monthly cycle, but the exact date varies by lender. Your credit card company might report to Experian on the 5th of the month, to Equifax on the 12th, and to TransUnion on the 18th, or it might only report to two of the three.

This staggered reporting is one of the main reasons your credit data differs across bureaus. It’s not an error; it’s simply how the system works.

If you’re working to understand how credit utilization and payment timing affect your profile, our credit utilization guide breaks down the math.

What Information Credit Bureaus Collect

Credit bureaus collect specific categories of data. Not everything about your financial life ends up on a credit report. Here’s what does and what doesn’t.

Personal Information

Each bureau maintains basic identifying information:

Full name (and any aliases or previous names)

Date of birth

Social Security number

Current and previous addresses

Current and previous employers

What’s NOT included: Your income, bank account balances, investment accounts, race, religion, or political affiliation. Many people assume income appears on a credit report. It does not. Lenders may ask for income separately during an application, but the bureaus don’t track it.

Account History (Tradelines)

This is the core of your credit report. Each account you’ve ever opened (or that’s been opened in your name) appears as a tradeline. Each tradeline includes:

When you apply for credit, the lender checks your report. This creates an inquiry. There are two types:

Hard inquiries happen when you apply for a loan or credit card. These can slightly lower your score and remain on your report for two years.

Soft inquiries happen when you check your own credit, when a company pre-approves you for an offer, or when an employer runs a background check. Soft inquiries do not affect your score.

Public Records and Collections

Credit reports can also include:

Bankruptcies (Chapter 7 stays for 10 years; Chapter 13 for 7 years)

Collection accounts (debts sold to collection agencies)

Civil judgments and tax liens were removed from credit reports in 2018 following policy changes by all three bureaus.

Credit reports aren’t generated by a single event. They’re built over time, one data point at a time, as lenders voluntarily report your account activity.

Here’s the keyword: voluntarily. There is no federal law requiring lenders to report your data to any credit bureau. Most major banks and credit card companies do report to all three, but smaller lenders, credit unions, and some fintech companies may only report to one or two.

This means:

A credit card you opened with a small credit union might appear on your Experian report but not on your TransUnion report.

A personal loan from an online lender might show up on Equifax and TransUnion but not Experian.

A medical collection might be reported to only one bureau.

Because reporting is voluntary and varies by institution, no two credit reports are guaranteed to be identical, even for the same person at the same point in time.

Common Mistake: Assuming that paying off a debt with one lender automatically updates all three bureaus simultaneously. It doesn’t. The lender reports to each bureau on its own schedule, so updates may appear days or even weeks apart.

Why Your Three Credit Scores Are Different

This is one of the most frequently asked questions in personal finance, and the answer involves three separate factors working together.

1. Different Data

As explained above, not all lenders report to all three bureaus. If TransUnion has a collection account that Experian doesn’t, your TransUnion-based score will likely be lower.

2. Different Reporting Timing

Even when all three bureaus have the same accounts, the balances and statuses may differ because lenders report on different dates. If your credit card balance was $3,000 when reported to Equifax on the 10th but you paid it down to $500 before it was reported to Experian on the 20th, the resulting scores will differ.

3. Different Scoring Models

The bureaus don’t calculate scores themselves. Scores are generated by scoring models, primarily FICO and VantageScore. Each model has multiple versions, and each bureau may use a different version.

In 2026, the scoring landscape is shifting significantly. FICO raised its prices to $10 per score, a 100% increase, which is creating cost pressures across the mortgage industry [2][9]. In response, Fannie Mae and Freddie Mac have accepted VantageScore 4.0 as an alternative, though full operational implementation is still rolling out [3][5].

This structural change means lenders may increasingly use different scoring models depending on cost and availability, which could further explain why the score you see from one source doesn’t match another.

Takeaway: Score differences of 20 to 40 points across bureaus are normal and expected. A difference of 100+ points usually signals missing data or an error on one report.

Who Uses Credit Bureau Data

Credit bureau data isn’t just for banks. A wide range of organizations access your credit information, each for different reasons.

Who

What They Use

Why

Mortgage lenders

Full credit reports + scores from all 3 bureaus

To determine loan eligibility and interest rates

Credit card issuers

Reports + scores (often from 1 bureau)

To approve applications and set credit limits

Auto lenders

Reports + scores

To set loan terms and interest rates

Landlords

Credit reports

To evaluate rental applications

Insurance companies

Credit-based insurance scores

To set premiums (in most states)

Utility companies

Credit reports

To determine if a deposit is required

Employers

Credit reports only (not scores)

For background checks (with your written consent)

Note that employers can only access a modified version of your credit report and cannot see your credit score. They also need your explicit written permission before pulling the report.

For mortgage lenders specifically, credit report costs are a growing concern in 2026. Industry estimates suggest mortgage credit report costs could jump as much as 50% due to combined FICO and bureau fee increases [3][9]. This cost is typically passed through to borrowers as part of closing costs.

Understanding who accesses your data reinforces why maintaining accurate reports matters. It affects far more than just loan approvals. If you’re thinking about broader wealth building, your credit profile is one piece of the puzzle alongside understanding what wealth really means.

Do Credit Bureaus Approve or Deny Applications?

No. This is worth stating clearly because it’s one of the most common misunderstandings in consumer finance.

Credit bureaus provide information. Lenders make decisions.

Here’s a simple analogy: a credit bureau is like a weather service. It collects atmospheric data, organizes it, and distributes forecasts. But the weather service doesn’t decide whether you should carry an umbrella. That decision is yours. Similarly, the bureau provides your credit data, but the lender decides whether to approve your application, what interest rate to offer, and what terms to set.

When a lender denies your application, the denial comes from the lender’s own criteria, not from the bureau. The lender is required by law (under the Fair Credit Reporting Act) to tell you which bureau’s report was used and the specific reasons for the denial. You then have the right to request a free copy of that report within 60 days.

How to Check Your Credit Reports for Free

Every consumer in the United States is entitled to one free credit report from each of the three bureaus every 12 months. The official (and only federally authorized) source is AnnualCreditReport.com.

Steps to Check Your Reports

Go to AnnualCreditReport.com. This is the only site authorized by federal law. Avoid lookalike sites that may charge fees.

Verify your identity. You’ll need to provide your name, address, Social Security number, and date of birth. You may also need to answer security questions about your accounts.

Select which reports to request. You can request all three at once or stagger them throughout the year (for example, one every four months) to monitor your credit more frequently.

Review each report carefully. Look for accounts you don’t recognize, incorrect balances, wrong personal information, and any negative items that seem inaccurate.

Before checking, it helps to understand what you’re looking at. Our guide on what a credit report is covers the structure and terminology in detail.

Tip: Since 2020, the three bureaus have offered free weekly online reports through AnnualCreditReport.com. As of 2026, this expanded access remains available, making it easier than ever to monitor your credit regularly.

What to Do If Your Credit Report Has an Error

Credit report errors are more common than most people realize. Errors can include accounts that don’t belong to you, incorrect payment statuses, wrong balances, or outdated personal information.

Step-by-Step Dispute Process

Step 1: Identify the error. Review your report line by line. Flag anything that looks wrong: an account you never opened, a late payment you know you made on time, a balance that doesn’t match your records, or a collection account that’s already been paid.

Step 2: File a dispute. You can dispute errors directly with the credit bureau that has the incorrect information. All three bureaus accept disputes online:

Include supporting documentation: bank statements, payment confirmations, account correspondence, or identity theft reports.

Step 3: Wait for the investigation. Under the Fair Credit Reporting Act (FCRA), the bureau must investigate your dispute within 30 days (45 days in some circumstances). The bureau contacts the data furnisher, which must verify, correct, or delete the disputed information.

Step 4: Review the results. The bureau will send you the results of the investigation. If the item is corrected or removed, request an updated copy of your report to confirm.

Step 5: Escalate if necessary. If the dispute is denied and you believe the error persists, you can file a complaint with the Consumer Financial Protection Bureau (CFPB) or add a 100-word consumer statement to your report explaining the dispute.

Correcting inaccurate information can improve your credit and help you start building it properly. Our guide on how to increase your credit score covers the data-driven strategies that move the needle.

Credit Bureaus and Identity Theft

Because credit bureaus hold sensitive personal and financial data, they are a critical line of defense (and a potential vulnerability) when it comes to identity theft.

Fraud Alerts

If you suspect someone has used your identity to open accounts, you can place a fraud alert on your credit file. You only need to contact one bureau; it’s required to notify the other two.

Initial fraud alert: Lasts one year. Requires lenders to take extra steps to verify your identity before opening new accounts.

Extended fraud alert: Lasts seven years. Available to confirmed identity theft victims who file an FTC identity theft report.

Credit Freeze (Security Freeze)

A credit freeze is stronger than a fraud alert. It blocks access to your credit report entirely, which means no one (including you) can open new credit accounts until the freeze is lifted. Freezing and unfreezing are free under federal law.

You must freeze your report with each bureau separately:

All three bureaus offer credit monitoring services, some free and some paid. These services alert you when new accounts are opened, when inquiries are made, or when significant changes appear on your report.

Takeaway: A credit freeze is the single most effective tool to prevent unauthorized accounts from being opened in your name. It costs nothing and takes minutes to set up. If you’re not actively applying for credit, there’s little reason not to have one in place.

Why Credit Bureaus Matter for Your Credit Score

Understanding the relationship between your behavior, your credit report, and your credit score is the foundation of financial literacy when it comes to borrowing.

Here’s the chain:

Your financial behavior → Gets reported to credit bureaus → Becomes your credit report → Gets scored by FICO or VantageScore → Influences lender decisions

You don’t directly control your credit score. You control your behavior. Your behavior determines what gets reported. What gets reported determines your score. And your score influences whether you get approved, what interest rate you receive, and how much you pay over the life of a loan.

The five major factors in most scoring models are:

Payment history (~35% of FICO score): Whether you pay on time [6][8]

Credit utilization (~30%): How much of your available credit are you using

Length of credit history (~15%): How long your accounts have been open

Credit mix (~10%): The variety of account types you have

New credit (~10%): Recent applications and new accounts

Each of these factors is derived from the data in your credit report. Therefore, improving your score means improving the data the bureaus have about you.

The credit scoring industry is undergoing its most significant structural shift in over two decades. In October 2025, FICO introduced its “Mortgage Direct License Program,” allowing mortgage lenders to license credit scores directly from FICO rather than through the three bureaus [2]. Combined with FICO’s 100% price increase to $10 per score in 2026, this has created substantial cost pressure on the mortgage industry [9].

As a result, VantageScore 4.0 is gaining traction. Equifax is offering it at $4.50 per score (with free access through the end of 2026 for customers also purchasing FICO scores), and TransUnion is offering it at $4 for mortgage purposes [5][7]. For consumers, this means the score your mortgage lender uses in 2026 may be different from the one used even a year ago.

Data-driven insight: The shift toward VantageScore 4.0 could benefit consumers with thin credit files (fewer than five accounts) because VantageScore can score consumers with as little as one month of credit history, while FICO typically requires six months.

Credit Bureau Comparison Tool

Credit Bureau Comparison Tool

Click each tab to explore the three major credit bureaus

Experian

Equifax

TransUnion

Compare All

Ex

Experian

HQ: Dublin, Ireland · US Ops: Costa Mesa, CA

Founded

1996 (current form)

Global Reach

37 countries

Free Score Access

Yes (Experian.com)

Dispute Method

Online, phone, mail

Key Features

✓ Offers free FICO Score 8 through Experian.com account

✓ Experian Boost lets you add utility and streaming payments

✓ Largest consumer credit database in the U.S.

✓ Provides free dark web surveillance for email addresses

✓ Online dispute portal with document upload

Eq

Equifax

HQ: Atlanta, Georgia

Founded

1899

Global Reach

24 countries

Free Score Access

Yes (myEquifax)

Dispute Method

Online, phone, mail

Key Features

✓ Oldest of the three bureaus (125+ years)

✓ Maintains data on 800+ million consumers worldwide

✓ Offering VantageScore 4.0 at $4.50/score through 2027

✓ Free credit report lock/unlock through myEquifax

✓ Provides 6 free Equifax reports per year via myEquifax

Note: Equifax experienced a major data breach in 2017 affecting ~147 million consumers. Enhanced security measures have been implemented since.

TU

TransUnion

HQ: Chicago, Illinois

Founded

1968

Global Reach

30+ countries

Free Score Access

Yes (TransUnion.com)

Dispute Method

Online, phone, mail

Key Features

✓ Maintains records on 1 billion+ consumers globally

✓ Offers free VantageScore 3.0 through TransUnion.com

✓ Offering VantageScore 4.0 for mortgage at $4/score

✓ TrueVision credit report format for easier reading

✓ Free credit freeze and fraud alert placement online

Side-by-Side Comparison

Feature

Experian

Equifax

TransUnion

Founded

1996

1899

1968

Headquarters

Dublin / Costa Mesa

Atlanta, GA

Chicago, IL

Global consumers

Hundreds of millions

800+ million

1+ billion

Free score type

FICO Score 8

VantageScore 3.0

VantageScore 3.0

VantageScore 4.0 (mortgage, 2026)

Available

$4.50/score

$4.00/score

Credit lock tool

Yes (CreditLock)

Yes (Lock & Alert)

Yes (TrueIdentity)

Online disputes

Yes

Yes

Yes

Credit freeze

Free

Free

Free

Unique feature

Experian Boost

Oldest bureau

Largest global reach

All three bureaus are private companies, not government agencies. Each may have different data about you because lenders report voluntarily and on different schedules.

Conclusion

Credit bureaus are not mysterious institutions. They are private companies that perform a specific function: collecting your borrowing data, organizing it into reports, and selling those reports to businesses that want to evaluate your creditworthiness.

The three major bureaus, Experian, Equifax, and TransUnion, operate independently. They may have different data about you, report on different timelines, and produce different scores. This is normal. It's how the system is designed.

The most important takeaway is this: you don't manage a credit score. You manage the information recorded about you. Every on-time payment, every balance you keep low, every account you maintain responsibly gets reported to the bureaus and reflected in your score over time. The bureaus track reliability, and lenders reward it.

Understanding this cause-and-effect chain is the foundation of evidence-based financial decision-making. The math behind money starts with knowing what's being measured and who's doing the measuring.

Your Next Steps

Pull your free reports from AnnualCreditReport.com and review all three.

Check for errors and dispute anything inaccurate.

Place a credit freeze if you're not actively applying for credit.

Focus on behavior: pay on time, keep utilization low, and let your history grow.

Learn the scoring factors so you know exactly which behaviors matter most.

This article is for informational and educational purposes only. It does not constitute financial, legal, or credit advice. Credit laws, scoring models, and bureau practices can change. Always consult with a qualified financial professional before making decisions that affect your credit or finances. The Rich Guy Math is an educational resource and does not provide credit repair services.

About the Author

Max Fonji is the founder of The Rich Guy Math, a data-driven financial education platform that teaches the math behind money with precision and clarity. With a background in financial analysis and a commitment to evidence-based investing principles, Max creates content that fosters reader confidence through understanding, rather than hype.

Frequently Asked Questions (FAQ)

Are credit bureaus government agencies?

No. Experian, Equifax, and TransUnion are private, for-profit companies. They are regulated by federal laws such as the Fair Credit Reporting Act (FCRA) and overseen by the Consumer Financial Protection Bureau (CFPB), but they are not government entities.

Do lenders check all three credit bureaus?

It depends on the lender and the type of credit. Mortgage lenders typically pull reports from all three bureaus and use the middle score. Credit card issuers and auto lenders often pull from just one or two bureaus depending on their internal policies and regional practices.

Why are my credit reports different from each other?

There are three main reasons:

Not all lenders report to all three bureaus

Lenders report on different dates to each bureau

Each bureau processes and updates data slightly differently

A difference of 20 to 40 points between bureau-based credit scores is common and expected.

Can I contact a credit bureau directly?

Yes. All three bureaus provide online portals, phone support, and mailing addresses. You can request your credit report, file a dispute, place a fraud alert, or initiate a credit freeze directly through each bureau’s official website.

How often do credit bureaus update my information?

Most lenders report account information on a monthly cycle, though the exact timing varies by lender and bureau. Some items, such as a collection account or bankruptcy filing, may appear within days. In general, expect updates approximately every 30 to 45 days for each account.

Does checking my own credit report hurt my score?

No. Checking your own credit report or credit score is considered a soft inquiry and has no impact on your score. You may check as often as you want without penalty. Only hard inquiries — when you formally apply for credit — can affect your credit score.