Picture this: You’re standing at checkout, ready to make an important purchase, when your card gets declined. You know you haven’t maxed out your limit, but somehow the transaction won’t go through. The culprit? A misunderstanding of available credit, one of the most fundamental yet frequently misunderstood concepts in personal finance.

Available credit represents the exact dollar amount you can spend on your credit card right now, calculated by subtracting your current balance from your total credit limit. This simple number carries enormous weight in your financial life, directly influencing 30% of your FICO Score through the credit utilization ratio and serving as a real-time indicator of your borrowing power.

Understanding the math behind available credit isn’t just about avoiding declined transactions. It’s about mastering a core principle of wealth building through strategic credit management. When you grasp how lenders view your available credit, how it fluctuates with every purchase and payment, and how to optimize it for maximum credit score benefit, you gain a powerful tool for financial leverage.

This guide breaks down the data-driven insights behind available credit, showing you the cause-and-effect relationships that determine your creditworthiness and financial flexibility.

Key Takeaways

- Available credit equals your credit limit minus your current balance—this dynamic number changes with every transaction and payment you make

- Credit utilization ratio (driven by available credit) comprises 30% of your FICO Score—maintaining utilization below 30% significantly improves creditworthiness

- Higher available credit across all accounts strengthens your overall credit profile—lenders interpret substantial available credit as lower risk and better financial management

- Strategic payment timing and credit limit increases directly boost available credit—understanding payment posting timelines maximizes your usable credit at critical moments

- Monitoring available credit prevents overspending and score damage—regular tracking through issuer apps provides real-time visibility into your financial position

What Is Available Credit?

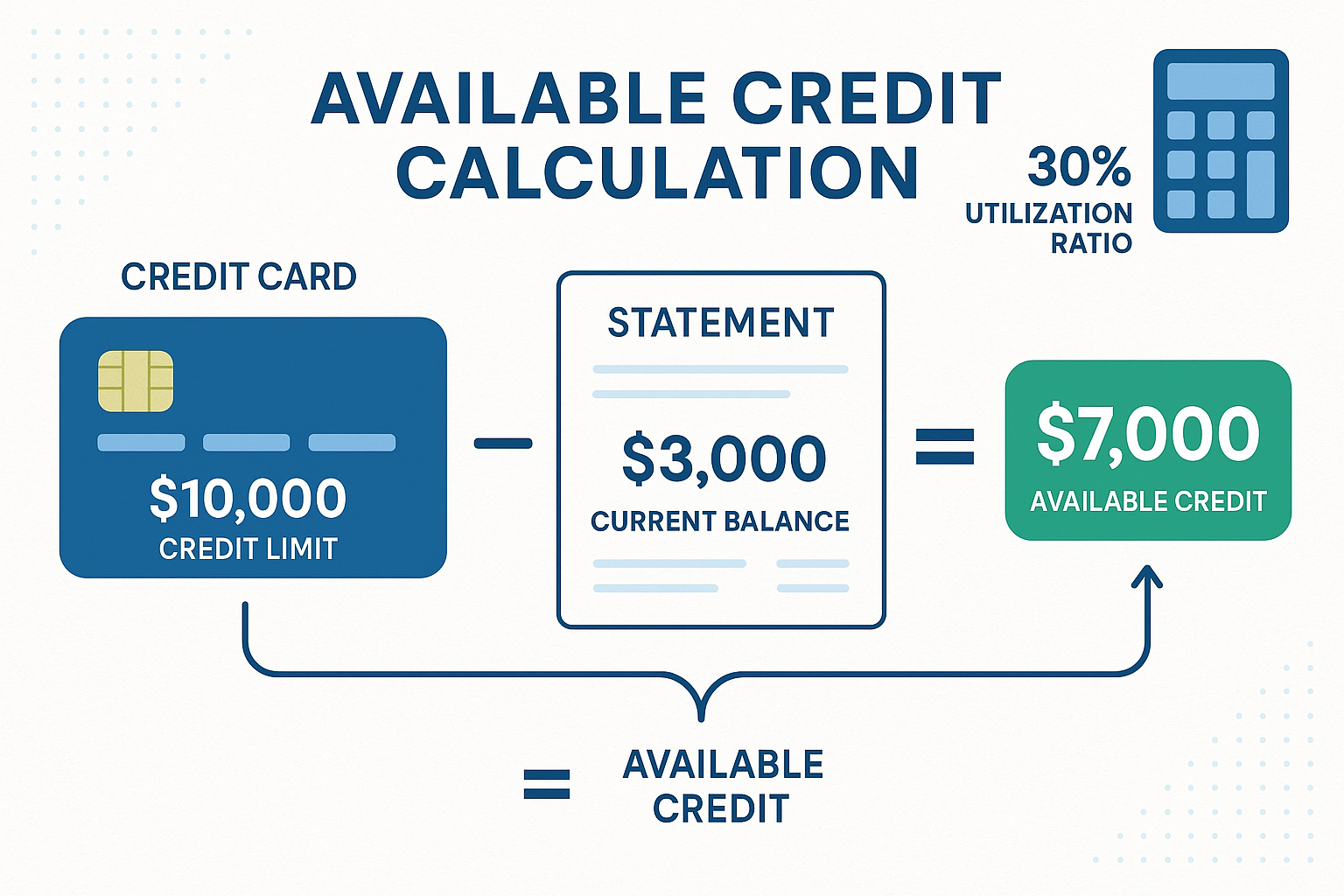

Available credit is the remaining borrowing capacity on your credit card or line of credit at any given moment. It represents the difference between your total credit limit and your current outstanding balance.

The fundamental formula:

Available Credit = Credit Limit – Current Balance

If your credit card has a $10,000 limit and you’ve charged $3,000 in purchases, your available credit is $7,000. This calculation applies to each credit account you hold.

The Dynamic Nature of Available Credit

Unlike your credit limit (which typically remains static unless changed by your issuer), available credit fluctuates constantly. Every purchase reduces it. Every payment increases it.

Consider this timeline:

- Monday morning: You have $7,000 available credit

- Monday afternoon: You charge $500 for groceries → available credit drops to $6,500

- Tuesday: You make a $1,000 payment that posts → available credit rises to $7,500

- Wednesday: You charge $200 for gas → available credit decreases to $7,300

This real-time variability makes available credit a living metric that requires active monitoring, especially if you’re managing multiple credit accounts or planning large purchases.

Available Credit Across Multiple Accounts

Most people carry multiple credit cards, each with its own credit limit and available credit. Your total available credit equals the sum of available credit across all revolving accounts.

Example scenario:

| Card | Credit Limit | Current Balance | Available Credit |

|---|---|---|---|

| Card A | $10,000 | $2,000 | $8,000 |

| Card B | $5,000 | $1,500 | $3,500 |

| Card C | $8,000 | $0 | $8,000 |

| Total | $23,000 | $3,500 | $19,500 |

Your total available credit ($19,500) represents your aggregate borrowing power across all accounts. This total matters significantly when lenders evaluate your overall creditworthiness and when calculating your combined credit utilization ratio.

Understanding your credit limit for each account provides the foundation for tracking available credit accurately.

How Available Credit Is Calculated

The calculation itself is straightforward arithmetic, but several factors influence how and when your available credit changes.

The Core Formula

Available Credit = Credit Limit – (Current Balance + Pending Transactions + Holds)

While the basic formula subtracts only your current balance from your limit, the complete picture includes:

- Current balance: Posted transactions that have cleared

- Pending transactions: Purchases made but not yet posted to your account

- Authorization holds: Temporary holds placed by merchants (common at gas stations and hotels)

A $100 restaurant charge might show as pending for 2-3 days before posting. During this time, it reduces your available credit even though it hasn’t officially been added to your statement balance.

How Credit Limit Changes Affect Available Credit

Your credit limit can change through several mechanisms:

1. Automatic credit limit increases: Issuers periodically review accounts and may increase limits for customers with strong payment history. If your limit increases from $10,000 to $12,000 while your balance remains $3,000, your available credit jumps from $7,000 to $9,000.

2. Requested credit limit increases: You can request higher limits, though this may trigger a hard inquiry on your credit report. The approval increases your available credit proportionally.

3. Credit limit decreases: Issuers can reduce limits due to missed payments, increased risk, or account inactivity. A limit reduction from $10,000 to $8,000 with a $3,000 balance would drop your available credit from $7,000 to $5,000.

4. Temporary limit increases: Some issuers offer temporary increases for specific purchases, which temporarily boost available credit.

Payment Posting Timeline and Available Credit

The timing of when payments restore available credit depends on your issuer’s processing schedule:

Typical payment processing timeline:

- Same-day posting: Some issuers credit payments made before a cutoff time (often 5 PM ET) the same business day

- Next-day posting: Most payments post within 1 business day

- 2-3 day posting: Payments from external banks may take longer

Critical insight: Your available credit increases when the payment posts, not when you initiate it. If you need available credit for an emergency purchase, factor in this processing time.

Example:

- You have $500 available credit on Thursday

- You make a $2,000 payment on Thursday evening

- The payment posts on Friday morning

- Your available credit becomes $2,500 on Friday

Strategic timing of payments before large purchases ensures you have sufficient available credit when needed. This connects directly to understanding your billing cycle and payment processing windows.

Why Available Credit Matters for Your Credit Score

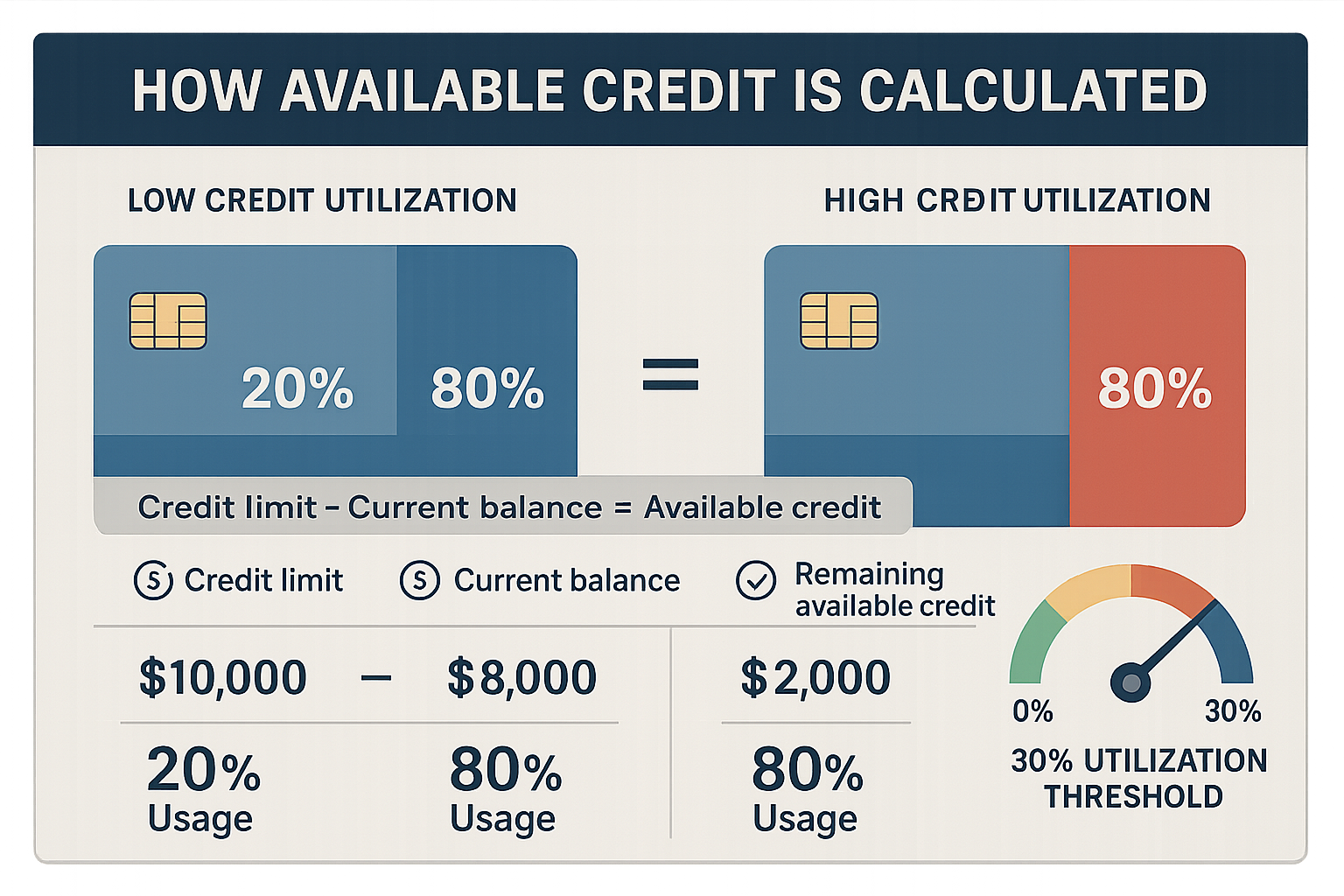

Available credit directly determines your credit utilization ratio—the second most important factor in FICO Score calculations, comprising 30% of your total score.

Credit Utilization Ratio: The Math Behind the Impact

Credit utilization ratio measures the percentage of your total credit limit currently in use:

Credit Utilization Ratio = (Total Balances / Total Credit Limits) × 100

Using the earlier example with $3,500 in balances and $23,000 in total limits:

Utilization = ($3,500 / $23,000) × 100 = 15.2%

This 15.2% utilization rate signals to lenders that you’re using credit responsibly without approaching your limits.

The utilization-score relationship:

- 0-10% utilization: Optimal range; demonstrates excellent credit management

- 10-30% utilization: Good range; maintains positive credit score impact

- 30-50% utilization: Moderate range; begins to negatively affect scores

- 50-70% utilization: High range; significant negative score impact

- 70-100% utilization: Very high range; severe score damage

Research from FICO indicates that individuals with scores above 800 typically maintain utilization below 7%. Those with scores below 650 often exceed 50% utilization.

Cause and effect: Higher available credit with the same balance equals lower utilization, which directly improves your credit score. Conversely, decreased available credit with unchanged balances increases utilization and damages your score.

Per-Card vs. Overall Utilization

Credit scoring models evaluate utilization at two levels:

1. Per-card utilization: The ratio on each account

2. Overall utilization: The aggregate ratio across all revolving accounts

Both matter, but per-card utilization can be particularly impactful. Maxing out a single card (100% utilization) damages your score even if your overall utilization remains low.

Example comparison:

Scenario A: Balanced distribution

- Card 1: $2,000 balance / $10,000 limit = 20%

- Card 2: $1,000 balance / $10,000 limit = 10%

- Overall: $3,000 / $20,000 = 15%

Scenario B: Concentrated usage

- Card 1: $3,000 balance / $10,000 limit = 30%

- Card 2: $0 balance / $10,000 limit = 0%

- Overall: $3,000 / $20,000 = 15%

Both scenarios show 15% overall utilization, but Scenario A typically produces better credit scores because no single card exceeds 30% utilization.

FICO vs VantageScore: Utilization Differences

The two major credit scoring models weigh utilization similarly but with subtle differences:

FICO Score 8:

- Utilization comprises 30% of the total score (labeled “Amounts Owed”)

- Evaluates both per-card and aggregate utilization

- Updates when creditors report (typically monthly)

VantageScore 4.0:

- Utilization falls under the “Credit Utilization” category (highly influential, approximately 20-30%)

- Places slightly more emphasis on recent utilization trends

- More sensitive to utilization changes over time

Both models demonstrate the same fundamental principle: more available credit relative to your balances improves your score.

Common Misconceptions About Utilization and Available Credit

Misconception 1: “Carrying a small balance improves my score.”

Reality: Credit scoring models don’t reward carrying balances. A 0% utilization rate is actually optimal, though 1-10% performs nearly identically. The myth that you must carry balances to build credit is false and costs you interest unnecessarily.

Misconception 2: “Utilization has a memory.”

Reality: Utilization is a point-in-time metric with no memory. If you have 80% utilization one month and pay it down to 10% the next, your score recovers quickly (typically within one reporting cycle). This makes utilization one of the fastest ways to improve your score.

Misconception 3: “Checking available credit hurts my score.”

Reality: Monitoring your own available credit through your issuer’s app or website is a soft inquiry that doesn’t affect your score. Only applications for new credit trigger hard inquiries that may temporarily reduce scores by a few points.

Understanding credit utilization in depth reveals how maximizing available credit through strategic balance management creates measurable score improvements.

Available Credit vs Total Credit Limit vs Remaining Balance

These three related but distinct concepts often create confusion. Understanding the precise differences enables better credit management decisions.

Defining Each Term

Credit Limit: The maximum amount your issuer allows you to borrow on a credit account. This number is set by the lender based on your creditworthiness, income, and other risk factors.

Current Balance: The total amount you currently owe on the account, including posted transactions. This appears on your statement and represents your debt obligation.

Available Credit: The amount you can still borrow, calculated as Credit Limit minus Current Balance (and pending transactions).

Comparison Table

| Metric | Definition | Changes When… | Example (with $10,000 limit) |

|---|---|---|---|

| Credit Limit | The maximum borrowing amount set by the issuer | Issuer increases/decreases limit | $10,000 |

| Current Balance | Amount currently owed | You make purchases or payments | $3,000 |

| Available Credit | Remaining borrowing capacity | You make purchases, payments, or limit changes | $7,000 |

How They Interact

These three metrics form a closed system where changes to one affect the others:

When you make a $500 purchase:

- Credit Limit: Unchanged at $10,000

- Current Balance: Increases from $3,000 to $3,500

- Available Credit: Decreases from $7,000 to $6,500

When you make a $1,000 payment:

- Credit Limit: Unchanged at $10,000

- Current Balance: Decreases from $3,500 to $2,500

- Available Credit: Increases from $6,500 to $7,500

When the issuer increases your limit by $2,000:

- Credit Limit: Increases from $10,000 to $12,000

- Current Balance: Unchanged at $2,500

- Available Credit: Increases from $7,500 to $9,500

Statement Balance vs Current Balance

Adding another layer, your statement balance represents the total amount owed at the end of your billing cycle, which is the amount reported to credit bureaus.

Your current balance includes all transactions since the statement closed, making it higher than your statement balance if you’ve made additional purchases.

Timeline example:

- Day 1 (statement closes): Statement balance = $3,000

- Day 5: You charge $500 → Current balance = $3,500

- Day 10: You make $1,000 payment → Current balance = $2,500

- Day 15: Statement balance still shows $3,000 (until next statement)

Credit bureaus typically receive your statement balance, not your current balance. This creates an opportunity for strategic optimization: paying down balances before your statement closes reduces the utilization reported to bureaus, improving your score even if you charge the same amounts afterward.

Understanding these distinctions helps you manage the relationship between spending, payments, and credit score impact with precision. Your credit score responds to the balances reported, not necessarily your day-to-day spending patterns.

How Lenders View Your Available Credit

From a lender’s perspective, available credit serves as a real-time indicator of financial health, risk level, and borrowing capacity.

Risk Assessment and Creditworthiness

Lenders interpret available credit through a risk management lens:

Highly available credit (low utilization) signals:

- Strong financial management and self-control

- Lower default risk (you’re not desperate for credit)

- Capacity to handle additional debt obligations

- Established credit history with responsible usage

Low available credit (high utilization) signals:

- Potential financial stress or cash flow problems

- Higher default risk (you’re dependent on credit)

- Limited capacity for additional debt

- Possible overextension

Data point: According to Federal Reserve research, consumers with utilization above 80% default at rates 3-4 times higher than those maintaining utilization below 30%[1].

This statistical relationship explains why lenders price risk (through interest rates and approval decisions) based partly on available credit patterns.

Underwriting Decisions and Available Credit

When you apply for new credit—whether a mortgage, auto loan, or additional credit card—lenders examine your available credit across existing accounts:

Mortgage underwriting:

Lenders calculate your debt-to-income ratio (DTI) but also consider available credit as a risk factor. High available credit with low utilization demonstrates you can access funds without using them, suggesting financial discipline.

Auto loan approval:

Available credit on credit cards can influence approval odds and interest rates. Lenders view substantial unused credit capacity as a cushion that reduces default probability.

New credit card applications:

Card issuers analyze your utilization across existing cards. If you’re maximizing available credit on current cards, they may deny the application or offer a lower limit.

Credit Line Decrease Triggers

Issuers monitor available credit usage patterns and may reduce credit limits when they detect increased risk:

Common triggers for limit decreases:

- Consistently high utilization (approaching or exceeding limits)

- Missed or late payments on any credit account

- Significant income reduction reported on credit applications

- Prolonged account inactivity (ironically, never using available credit can trigger decreases)

- Negative changes in credit report (collections, charge-offs, bankruptcies)

The negative spiral effect:

A credit limit decrease reduces available credit, which increases the utilization ratio, which damages the credit score, which may trigger additional limit decreases from other issuers monitoring your credit. This cascade effect demonstrates why maintaining healthy available credit is crucial for financial stability.

The Lender’s Available Credit Calculation

When evaluating your application, lenders perform their own available credit assessment:

Total Available Credit = Σ(All Credit Limits) – Σ(All Current Balances)

They also calculate your available credit as a percentage of total limits:

Available Credit Percentage = (Total Available Credit / Total Credit Limits) × 100

A borrower with $50,000 in total credit limits and $10,000 in balances has:

- Total available credit: $40,000

- Available credit percentage: 80%

Lenders generally view available credit percentages above 70% favorably, while percentages below 30% raise concerns about financial stress.

This institutional perspective reveals why managing available credit strategically, keeping balances low relative to limits, creates tangible benefits when you need credit most. Similar principles apply when lenders evaluate your overall debt-to-equity ratio in business contexts.

How to Increase Your Available Credit (Step-by-Step)

Boosting available credit improves your credit utilization ratio, enhances your credit score, and provides greater financial flexibility. Here are evidence-based strategies with clear cause-and-effect relationships.

Strategy 1: Request a Credit Limit Increase

How it works: Contact your credit card issuer (via phone, website, or app) and request a higher credit limit on existing accounts.

The math: If your limit increases from $10,000 to $15,000 while your balance remains $3,000, your utilization drops from 30% to 20%, and your available credit jumps from $7,000 to $12,000.

Step-by-step process:

- Check your eligibility: Most issuers require 6-12 months of account history before considering increases

- Review your payment history: Ensure you have no late payments in the past 12 months

- Update your income: If your income has increased, report it to your issuer (higher income justifies higher limits)

- Submit the request: Use your issuer’s online portal or call customer service

- Justify: Explain increased income, excellent payment history, or specific needs

Important considerations:

- Hard inquiry risk: Some issuers perform hard credit pulls for limit increase requests, temporarily reducing your score by 3-5 points

- Soft inquiry option: Many issuers now use soft inquiries that don’t affect your score; ask before requesting

- Automatic increases: Maintain excellent payment history, and issuers often grant automatic increases every 6-12 months without inquiries

Success rate factors:

- Payment history (most important)

- Income level and stability

- Current utilization (ironically, lower utilization increases approval odds)

- Account age and relationship with issuer

Strategy 2: Pay Down Existing Balances Strategically

How it works: Reducing your current balances directly increases available credit without changing credit limits.

The math: Paying down a $3,000 balance to $1,000 on a $10,000 limit card increases available credit from $7,000 to $9,000 and drops utilization from 30% to 10%.

Strategic payment approaches:

Approach A: Target high-utilization cards first

Pay down cards with the highest utilization percentages to maximize per-card score impact.

Example:

- Card 1: $4,500 balance / $5,000 limit = 90% utilization

- Card 2: $1,000 balance / $10,000 limit = 10% utilization

Paying $2,000 toward Card 1 drops its utilization to 50%, creating more score improvement than paying $2,000 toward Card 2 (which would drop to 0% but was already optimal).

Approach B: Pay before statement closing

Make payments before your statement closing date to reduce the balance reported to credit bureaus.

Timeline:

- Day 1-25: Make purchases totaling $3,000

- Day 26: Make $2,000 payment

- Day 30 (statement closes): Only $1,000 balance reports to bureaus

- Result: Credit bureaus see 10% utilization instead of 30%

Approach C: Multiple payments per month

Instead of one monthly payment, make weekly or bi-weekly payments to keep balances consistently low.

Frequency impact:

- Monthly payment: Balance may reach $3,000 before the payment drops it to $0

- Weekly payments: Balance never exceeds $750, maintaining lower utilization throughout the month

This strategy particularly benefits those who charge significant amounts but pay in full monthly. Similar budgeting principles apply to the 50/30/20 rule for overall financial management.

Strategy 3: Become an Authorized User

How it works: Being added as an authorized user on someone else’s credit card with high available credit can boost your total available credit and improve your utilization ratio.

The math: If you’re added to a parent’s card with a $20,000 limit and $2,000 balance, your total available credit increases by $18,000 (assuming the account reports to your credit file).

Requirements for maximum benefit:

- Choose accounts with:

- High credit limits

- Low balances (ideally under 10% utilization)

- Long, positive payment history

- On-time payment record

- Verify reporting: Confirm the issuer reports authorized users to all three credit bureaus (most major issuers do)

- Monitor impact: Check your credit report 30-60 days after being added to verify the account appears

Risk considerations:

- If the primary account holder misses payments or maxes out the card, it negatively affects your credit

- Some lenders discount authorized user accounts when evaluating applications

- You can request removal at any time if the account becomes problematic

Effectiveness: Research shows authorized user status can increase credit scores by 10-50 points, depending on the account’s characteristics and your existing credit profile[2].

Strategy 4: Open a New Credit Account (Strategically)

How it works: Applying for and receiving a new credit card increases your total credit limits, thereby increasing total available credit.

The math: Adding a new card with a $5,000 limit to your existing $20,000 in limits increases total available credit by $5,000 (assuming no change in balances).

Before opening new accounts, calculate the impact:

Current state:

- Total limits: $20,000

- Total balances: $6,000

- Utilization: 30%

- Available credit: $14,000

After the new $5,000 limit card:

- Total limits: $25,000

- Total balances: $6,000 (unchanged)

- Utilization: 24%

- Available credit: $19,000

Strategic considerations:

- Hard inquiry cost: New applications trigger hard inquiries, temporarily reducing scores by 3-10 points

- Average age of accounts: New accounts lower your average account age, which can reduce scores

- Timing matters: Space new applications 3-6 months apart to minimize cumulative score impact

- Choose wisely: Select cards with no annual fee and benefits you’ll actually use

When this strategy makes sense:

- You have utilization above 30% and need immediate relief

- You’ve been denied credit due to high utilization

- You can manage additional credit responsibly without overspending

When to avoid:

- You’re applying for a mortgage or auto loan within 6 months (hard inquiries matter more)

- You struggle with overspending (more available credit could worsen debt)

- Your credit score is already below 650 (approval odds are lower)

Strategy 5: Avoid Behaviors That Decrease Available Credit

How it works: Prevention is as important as optimization. Certain actions reduce available credit and should be avoided.

Actions that reduce available credit:

1. Closing credit card accounts

Closing a card with a $5,000 limit removes $5,000 from your total available credit, increasing utilization on remaining accounts.

Example:

- Before closing: $30,000 limits, $6,000 balances = 20% utilization

- After closing $5,000 limit card: $25,000 limits, $6,000 balances = 24% utilization

2. Missing payments

Late payments trigger issuer risk reviews that may result in credit limit decreases.

3. Maxing out cards

Consistently approaching or exceeding limits signals financial stress and may prompt limit reductions.

4. Leaving accounts inactive

Not using a card for 12+ months may lead issuers to reduce limits or close accounts due to inactivity.

Prevention strategy: Use each card for a small recurring charge (like a streaming subscription) and set up autopay to maintain activity without manual intervention.

5. Requesting balance transfers without considering limits

Balance transfers move debt between accounts but don’t change total balances. If you transfer $5,000 to a card with a $6,000 limit, you’ve suddenly created 83% utilization on that card.

Strategy 6: Reallocate Credit Limits Between Cards

How it works: Some issuers allow you to move credit limit amounts from one card to another within the same issuer’s portfolio.

Example: You have two cards from the same bank:

- Card A: $10,000 limit, $8,000 balance (80% utilization)

- Card B: $8,000 limit, $1,000 balance (12.5% utilization)

Request to move $3,000 in limit from Card B to Card A:

- Card A: $13,000 limit, $8,000 balance (61.5% utilization) ✓

- Card B: $5,000 limit, $1,000 balance (20% utilization) ✓

Result: Both cards now show healthier utilization without changing total available credit or requiring new applications.

Availability: Not all issuers offer this feature. Chase, American Express, and Citi typically allow reallocation; others may not.

Takeaway: Increasing available credit through any combination of these strategies directly improves your credit utilization ratio, creating measurable credit score improvements within 30-60 days. The most effective approach combines multiple strategies: request limit increases on existing accounts, pay down balances strategically, and avoid actions that reduce available credit.

Case Study: Two Borrowers With the Same Debt but Different Available Credit

Real-world scenarios demonstrate how available credit differences create divergent financial outcomes even when debt levels are identical.

The Setup: Meet Sarah and Michael

Both borrowers have:

- Total credit card debt: $6,000

- Annual income: $60,000

- Payment history: Excellent (no late payments)

- Credit age: 5 years average

The difference lies in their total credit limits and the resulting available credit.

Sarah’s Credit Profile

Credit cards:

- Card 1: $15,000 limit, $2,000 balance

- Card 2: $10,000 limit, $2,000 balance

- Card 3: $8,000 limit, $2,000 balance

Calculations:

- Total credit limits: $33,000

- Total balances: $6,000

- Total available credit: $27,000

- Overall utilization: $6,000 / $33,000 = 18.2%

- Per-card utilization: 13.3%, 20%, 25%

Credit score impact: 760

Michael’s Credit Profile

Credit cards:

- Card 1: $5,000 limit, $3,000 balance

- Card 2: $3,000 limit, $2,000 balance

- Card 3: $2,000 limit, $1,000 balance

Calculations:

- Total credit limits: $10,000

- Total balances: $6,000

- Total available credit: $4,000

- Overall utilization: $6,000 / $10,000 = 60%

- Per-card utilization: 60%, 66.7%, 50%

Credit score impact: 640

The Outcome Differences

Despite identical debt amounts and payment histories, the 120-point credit score gap creates dramatically different financial realities:

| Financial Product | Sarah (760 score, $27K available) | Michael (640 score, $4K available) |

|---|---|---|

| New credit card approval | Approved with $10,000+ limit | Denied or approved with $1,000 limit |

| Auto loan (5-year, $25,000) | 5.5% APR, $474/month, $3,440 total interest | 12.5% APR, $561/month, $8,660 total interest |

| Mortgage ($300,000, 30-year) | 6.5% APR, $1,896/month | 7.5% APR, $2,098/month |

| Personal loan ($10,000) | Approved at 8% APR | Denied or 18%+ APR |

Cost difference over time:

For just the auto loan and mortgage examples:

- Sarah’s total interest (auto + 5 years mortgage): $3,440 + $113,760 = $117,200

- Michael’s total interest (auto + 5 years mortgage): $8,660 + $125,880 = $134,540

- Difference: $17,340 in additional interest costs for Michael over just 5 years

Root cause: The difference in available credit (driven by total credit limits) created a 60% vs. 18% utilization gap, which produced the 120-point score difference, which resulted in tens of thousands of dollars in additional interest costs.

The Path to Convergence

Michael’s action plan to match Sarah’s profile:

Month 1-3: Request limit increases

- Request increases on all three cards

- Target: Increase total limits from $10,000 to $15,000

- Result: Utilization drops from 60% to 40%

- Expected score increase: +20-30 points

Month 4-6: Pay down the highest utilization cards

- Focus $2,000 in extra payments toward Card 2 (66.7% utilization)

- Result: Card 2 drops to 0% utilization

- Overall utilization: $4,000 / $15,000 = 26.7%

- Expected score increase: +30-40 points

Month 7-9: Apply for one new card strategically

- Apply for a card offering $5,000+ limit

- Assume approval for $5,000 limit

- New totals: $20,000 limits, $4,000 balances = 20% utilization

- Expected score increase: +10-20 points (after hard inquiry recovery)

Month 10-12: Maintain and optimize

- Keep utilization below 20%

- Make payments before statement closing

- Expected score: 720-740 range

Result: Within one year, Michael can close most of the gap by strategically increasing available credit through multiple approaches.

Key insight: The borrower with higher available credit enjoys better financial terms not because they’re more responsible with debt (both carried $6,000 in balances), but because they demonstrated better credit management through lower utilization ratios. This case study illustrates the tangible financial value of maximizing available credit.

Understanding how credit mix also contributes to overall credit health provides additional optimization opportunities.

Risks and Downsides to Managing Available Credit

While maximizing available credit generally benefits credit scores and financial flexibility, several risks and potential downsides require consideration.

Risk 1: Credit Limit Decreases Without Warning

The scenario: Issuers can reduce credit limits at any time, often without advance notice, if they perceive increased risk.

Common triggers:

- Economic downturns (issuers reduce exposure across customer portfolios)

- Negative information on your credit report from other creditors

- Decreased income or employment changes

- Prolonged inactivity on the account

The cascade effect:

Imagine you maintain $30,000 in total limits with $6,000 in balances (20% utilization). Your issuer reduces one card’s limit from $15,000 to $8,000:

- Before: $30,000 limits, $6,000 balances = 20% utilization

- After: $23,000 limits, $6,000 balances = 26% utilization

This single action increased your utilization by 6 percentage points, potentially dropping your credit score by 10-20 points. If you were near a threshold (like 30%), this could trigger additional limit decreases from other issuers monitoring your credit.

Mitigation strategy:

- Maintain activity on all cards (even small monthly charges)

- Monitor credit reports for changes that might trigger issuer reviews

- Keep utilization well below 30% to absorb potential limit decreases

- Diversify across multiple issuers (don’t concentrate all credit with one bank)

Risk 2: Hard Inquiries from Limit Increase Requests

The scenario: Requesting credit limit increases or applying for new cards generates hard inquiries that temporarily reduce credit scores.

Impact magnitude:

- Single hard inquiry: -3 to -10 points (typically -5 points average)

- Multiple inquiries within 6 months: Cumulative effect can reach -20 to -30 points

- Recovery timeline: Impact diminishes after 6 months, disappears after 12 months

When hard inquiries matter most:

- Applying for a mortgage (lenders scrutinize recent inquiries)

- Borderline credit scores near approval thresholds

- Multiple applications in short timeframes (suggests financial distress)

Strategic approach:

- Ask issuers if they use soft inquiries for limit increases before requesting

- Space applications 3-6 months apart

- Avoid new applications 6-12 months before major loan applications

- Use pre-qualification tools that only perform soft inquiries

Risk 3: Overspending Temptation

The psychological risk: Higher available credit can create a false sense of financial capacity, leading to increased spending beyond actual means.

The data: Research from the Federal Reserve Bank of New York found that consumers increase spending by approximately $150-$200 for every $1,000 increase in available credit[3].

Example scenario:

A borrower receives a credit limit increase from $10,000 to $15,000, increasing available credit by $5,000. The psychological effect of “having more available” leads to $1,000 in additional discretionary purchases over the next three months.

Result:

- Intended outcome: Lower utilization through higher limits

- Actual outcome: Higher balances offsetting the limit increase, maintaining similar utilization

Prevention strategies:

- Set personal spending limits below available credit

- Use budgeting apps that track spending against income, not available credit

- Implement the 50/30/20 budgeting rule based on income

- Automate savings before discretionary spending

Risk 4: Issuer Account Reviews and Closures

The scenario: Credit card issuers periodically review accounts and may close them due to inactivity or perceived risk, immediately eliminating that card’s available credit.

Closure triggers:

- Inactivity: No purchases for 6-12+ months

- Profitability: You never carry balances (issuers prefer customers who pay interest)

- Risk changes: Negative information from other creditors

- Business decisions: Issuer exits certain product lines or customer segments

Impact example:

You have five credit cards totaling $40,000 in limits with $8,000 in balances (20% utilization). One card with a $10,000 limit that you haven’t used in 18 months gets closed:

- Before: $40,000 limits, $8,000 balances = 20% utilization

- After: $30,000 limits, $8,000 balances = 26.7% utilization

Additional impact: Average age of accounts may decrease if the closed account was one of your oldest, further damaging your score.

Prevention:

- Use each card at least once every 3-6 months

- Set up small recurring charges (subscriptions, utilities) on cards you don’t actively use

- Enable autopay to ensure charges are paid without manual intervention

Risk 5: False Security in Emergencies

The scenario: Relying on available credit as an emergency fund creates vulnerability if issuers reduce limits or close accounts during financial crises.

Historical precedent: During the 2008 financial crisis, credit card issuers reduced total credit limits by over $1.5 trillion across the industry, eliminating available credit for millions of consumers precisely when they needed it most[4].

Better approach:

- Build a cash emergency fund covering 3-6 months of expenses

- Treat available credit as a backup to cash reserves, not a replacement

- Understand that available credit can disappear without warning

Risk 6: Balance Transfer Traps

The scenario: Using available credit for balance transfers can create unexpected utilization problems.

Example:

You have two cards:

- Card A: $10,000 limit, $7,000 balance (70% utilization)

- Card B: $10,000 limit, $0 balance (0% utilization)

- Overall: $20,000 limits, $7,000 balances = 35% utilization

You transfer the $7,000 from Card A to Card B to take advantage of a 0% APR promotional rate:

After transfer:

- Card A: $10,000 limit, $0 balance (0% utilization)

- Card B: $10,000 limit, $7,000 balance (70% utilization)

- Overall: Still 35% utilization

The problem: While overall utilization remains unchanged, Card B now shows 70% utilization, which negatively impacts per-card utilization scoring. Additionally, balance transfer fees (typically 3-5%) reduce your available credit by the fee amount.

Better approach:

- Calculate the impact on per-card utilization before transferring

- Transfer only amounts that keep the receiving card below 30% utilization

- Factor in balance transfer fees when calculating available credit

Takeaway: Available credit is a powerful financial tool, but it requires active management and awareness of risks. The goal is to maximize available credit while maintaining discipline in spending, monitoring for issuer actions, and building true financial resilience through cash reserves and income growth.

Frequently Used Terms Related to Available Credit

Understanding related terminology strengthens your overall credit management knowledge:

Credit Limit: The maximum borrowing amount an issuer extends on a credit account. Unlike available credit, this number remains static unless the issuer changes it. Learn more about credit limits.

Credit Line: Functionally identical to credit limit; the terms are used interchangeably. Some issuers prefer “line of credit” for revolving accounts. Explore credit lines.

Credit Utilization Ratio: The percentage of total credit limits currently in use, calculated as (Total Balances / Total Limits) × 100. This metric comprises 30% of FICO Scores. Deep dive into credit utilization.

Revolving Credit: Credit that replenishes as you pay down balances (like credit cards), as opposed to installment loans with fixed payment schedules.

Statement Balance: The total amount owed at the end of your billing cycle, which typically gets reported to credit bureaus and determines your minimum payment.

Current Balance: Your real-time balance, including all posted transactions, which may differ from your statement balance.

Pending Transactions: Purchases that have been authorized but not yet posted to your account; these reduce available credit but don’t yet appear in your current balance.

Authorization Hold: A temporary hold placed on available credit by merchants to ensure funds are available; common at gas stations and hotels.

Hard Inquiry: A credit check performed when you apply for new credit, which may temporarily reduce your credit score by 3-10 points.

Soft Inquiry: A credit check that doesn’t affect your score, such as checking your own credit or pre-qualification offers.

Credit Mix: The variety of credit account types (revolving, installment, mortgage) in your credit profile, comprising 10% of FICO Scores. Understanding credit mix.

Billing Cycle: The period between statement closing dates, typically 28-31 days, during which transactions accumulate. Billing cycle details.

Grace Period: The time between your statement closing date and payment due date during which you can pay your balance without incurring interest charges.

Credit Cycling: The practice of making multiple payments within a billing cycle to keep balances and utilization low. Credit cycling strategies.

Interactive Tool: Available Credit & Utilization Calculator

💳 Available Credit Calculator

Calculate your available credit, utilization ratio, and credit score impact

📊 Your Credit Summary

Conclusion

Available credit represents far more than a simple number on your credit card statement. It’s a dynamic metric that directly influences 30% of your credit score through the utilization ratio, serves as a real-time indicator of financial health to lenders, and determines your borrowing power across all credit products.

The fundamental math is straightforward: Available Credit = Credit Limit – Current Balance. But the implications extend into every corner of your financial life—from credit card approvals to mortgage rates to auto loan terms.

The evidence-based strategies covered in this guide provide clear cause-and-effect pathways to optimization:

- Request credit limit increases on existing accounts to boost available credit without new applications

- Pay down balances strategically, targeting high-utilization cards first and timing payments before statement closing

- Monitor utilization across all accounts, maintaining aggregate ratios below 30% and individual card ratios below 30%

- Avoid actions that reduce available credit, including closing accounts, missing payments, or leaving cards inactive

- Understand lender perspectives on available credit to position yourself favorably for future credit applications

The case study demonstrated the real-world cost of low available credit: Two borrowers with identical $6,000 debt loads experienced a 120-point credit score gap based solely on available credit differences, translating to over $17,000 in additional interest costs over just five years.

Next steps to implement immediately:

Week 1: Audit your current position

- Calculate total available credit across all revolving accounts

- Determine the overall utilization ratio

- Identify cards with utilization above 30%

Week 2-4: Optimize existing accounts

- Request credit limit increases on cards with good standing

- Make strategic payments to reduce high-utilization cards below 30%

- Set up account alerts for balance thresholds

Month 2-3: Establish monitoring systems

- Check available credit weekly through issuer apps

- Review credit reports monthly for accuracy

- Track utilization trends in a spreadsheet or budgeting app

Month 4+: Maintain and refine

- Keep utilization below 30% consistently

- Make payments before statement closing when possible

- Use each card minimally to prevent closures

The wealth-building connection: Managing available credit effectively is a foundational element of financial literacy that enables access to lower-cost credit when opportunities arise. Whether financing a home, starting a business, or handling emergencies, the borrower with higher available credit and lower utilization enjoys better terms, lower costs, and greater financial flexibility.

Understanding the math behind money means recognizing that available credit isn’t just about spending capacity—it’s about demonstrating financial discipline that translates into tangible economic advantages measured in thousands or tens of thousands of dollars over time.

Master available credit management, and you master a critical component of the credit system that determines your cost of capital for decades to come.

References

[1] Federal Reserve Board. (2023). “Consumer Credit – G.19.” Federal Reserve Statistical Release. https://www.federalreserve.gov/releases/g19/

[2] Consumer Financial Protection Bureau. (2020). “Authorized User Status and Credit Scores.” CFPB Research Report. https://www.consumerfinance.gov/

[3] Federal Reserve Bank of New York. (2022). “Quarterly Report on Household Debt and Credit.” Center for Microeconomic Data. https://www.newyorkfed.org/microeconomics/hhdc

[4] Federal Reserve Bank of San Francisco. (2010). “Credit Card Limit Reductions During the Great Recession.” FRBSF Economic Letter. https://www.frbsf.org/

[5] FICO. (2024). “Understanding FICO Scores.” myFICO Consumer Education. https://www.myfico.com/credit-education/credit-scores

Author Bio

Max Fonji is the founder of The Rich Guy Math, a data-driven financial education platform dedicated to teaching the math behind money. With a background in financial analysis and a commitment to evidence-based investing principles, Max breaks down complex financial concepts into clear, actionable insights. His work focuses on helping individuals understand credit management, compound growth, and wealth-building strategies through quantitative frameworks and real-world data. Max believes that financial literacy begins with understanding cause-and-effect relationships in money management, and his teaching emphasizes the mathematical foundations that drive long-term financial success.

Educational Disclaimer

This article is provided for educational and informational purposes only and does not constitute financial, legal, or credit repair advice. The information presented represents general principles of credit management and may not apply to every individual situation.

Credit scores are determined by multiple factors beyond credit utilization and available credit, including payment history, credit age, credit mix, and recent inquiries. Individual results will vary based on personal credit profiles, issuer policies, and economic conditions.

Before making financial decisions, including requesting credit limit increases, opening new accounts, or closing existing accounts, consult with a qualified financial advisor or credit counselor who can evaluate your specific circumstances.

The Rich Guy Math and its authors do not guarantee specific credit score improvements or financial outcomes from implementing the strategies discussed in this article. All financial decisions carry risk and should be made based on thorough personal research and professional guidance.

Credit card terms, interest rates, fees, and issuer policies vary by institution and change over time. Always review current terms and conditions directly with your credit card issuer before making decisions.

This content is current as of 2025 and reflects credit scoring models and industry practices as of the publication date. Credit industry standards and regulations may change over time.

Frequently Asked Questions

What happens if I go over my available credit?

Exceeding your available credit typically results in declined transactions at the point of sale. However, if a transaction does process, you may experience:

- Over-limit fees (often $25–$35, though many issuers removed these)

- Credit score damage from utilization exceeding 100%

- Possible APR increases due to higher perceived risk

- Credit limit reductions

- Account restrictions or closures with repeated overages

Prevention tip: Monitor available credit before large purchases and set up alerts when balances approach limits.

Does checking my available credit hurt my credit score?

No. Checking your available credit through your issuer’s website, app, or customer service is a soft inquiry and does not impact your credit score.

What does affect your score:

- Hard inquiries from new credit applications

- Late or missed payments

- High utilization ratios

Best practice: Check available credit weekly or before large purchases.

How often does available credit update?

Available credit updates in real time as purchases authorize and as payments post.

For purchases:

- Authorization reduces available credit instantly

- Pending charges usually post within 1–3 days

For payments:

- Same-day posting for payments before cutoff times

- Most payments finalize within 1 business day

- External bank payments may take 2–3 days

Tip: Your issuer’s app shows the most accurate real-time available credit.

Can I increase available credit without getting a new card?

Yes. You can increase available credit by:

- Requesting credit limit increases

- Paying down balances

- Paying before your statement closes

- Maintaining strong payment history for automatic increases

Best method: Pay down balances while also requesting limit increases.

Does available credit affect my ability to get a mortgage?

Yes, indirectly. Available credit impacts:

- Credit score: Your utilization ratio makes up 30% of your FICO Score.

- DTI ratio: Mortgage lenders review minimum payments on all accounts.

Example:

- 760 score (18% utilization) → ~6.5% APR

- 640 score (60% utilization) → ~7.5% APR

Strategy: Maximize available credit 6–12 months before applying.

Should I close credit cards I don’t use to reduce available credit?

Generally, no. Closing cards reduces available credit, increases utilization, and lowers your credit score.

Negative consequences include:

- Higher utilization after losing a credit limit

- Lower average account age

- Reduced credit mix

Better alternative: Keep the card open and use it once every 3–6 months.

How much available credit should I maintain?

Optimal available credit is 70–90% of your total credit limits (10–30% utilization). The ideal target is ~10% utilization for top credit score performance.

Example:

- $30,000 limits → Ideal balance: $3,000 (90% available credit)

- $30,000 limits → Acceptable balance: $9,000 (70% available)

- $30,000 limits → Concerning: $15,000+ (50%+ utilization)

Fact: FICO reports top 800+ scorers average ~7% utilization.