The average investor loses 1.5% annually to poor portfolio management and emotional decision-making. Robo-advisors address this problem through automated, evidence-based investing, which removes human bias from the equation.

The best robo-advisors in 2026 represent the evolution of passive investing, combining low-cost index fund exposure with algorithmic rebalancing, tax-loss harvesting, and goal-based portfolio construction. These platforms democratize institutional-grade investment strategies, making them accessible to investors with as little as $10. If you’re still deciding how to allocate your money, this in-depth investing guide explains the strategies, risks, and long-term principles you should understand first.

The math behind robo-advisors is straightforward: lower fees compound into significantly higher returns over time. A 0.15% management fee versus a traditional 1% advisor fee creates a 0.85% annual advantage. Over 30 years on a $100,000 portfolio with 7% returns, that difference equals $176,000 in additional wealth.

This comprehensive guide examines the top robo-advisors in 2026, comparing fees, features, minimum investments, and portfolio strategies to help investors select the platform that best aligns with their financial goals.

Key Takeaways

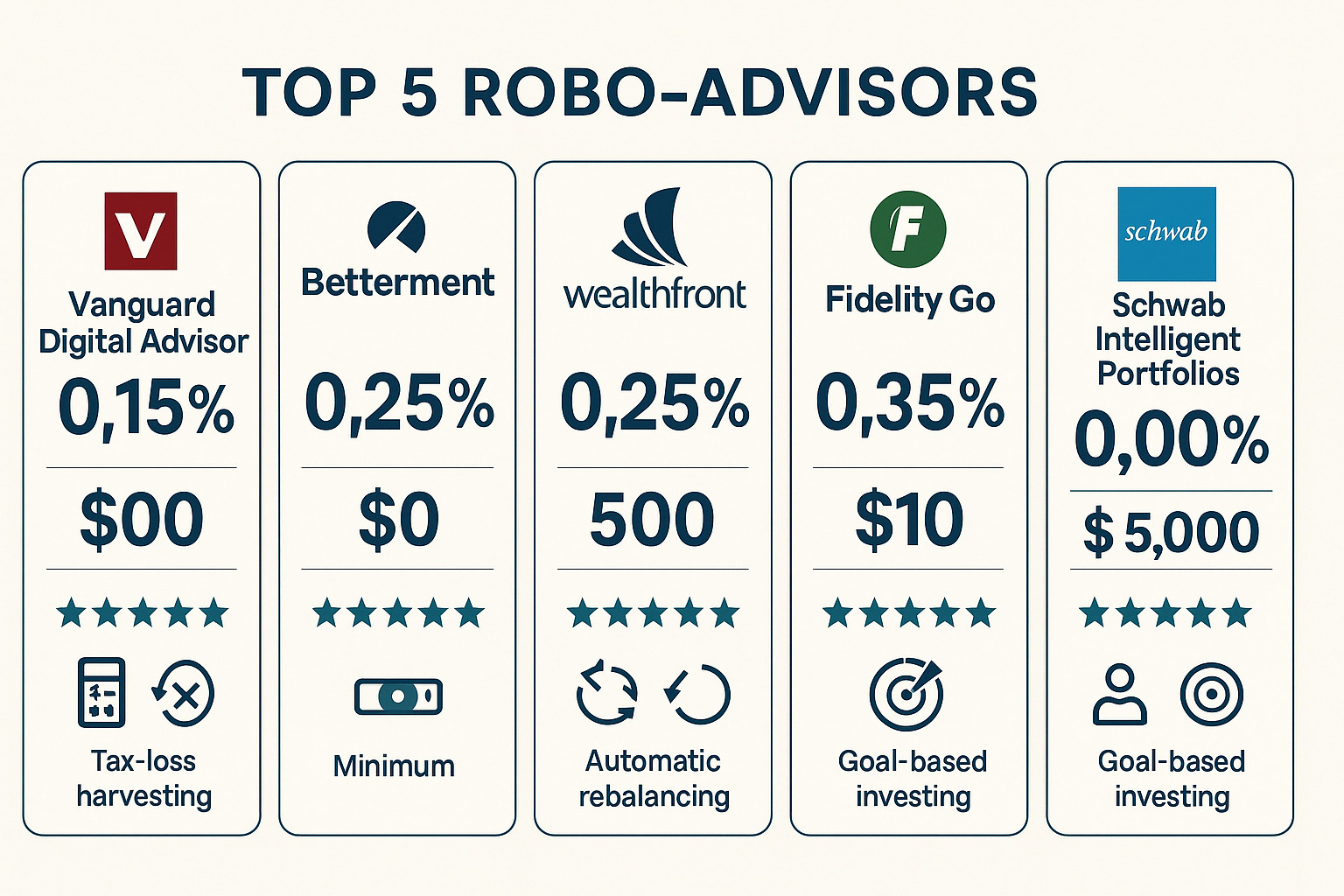

- Vanguard Digital Advisor leads with the lowest management fee at 0.15% annually, making it ideal for cost-conscious investors seeking passive index exposure

- Fee structures vary dramatically, from $0 management fees (Schwab, Fidelity, Go under $25K) to 0.65% for premium human advisor access

- Minimum investments range from $0 to $5,000, with platforms like Betterment and Fidelity Go removing barriers for beginning investors

- Tax-loss harvesting can add 0.77% in annual after-tax returns, making this feature critical for taxable accounts

- Portfolio construction methods differ significantly; some use target-date glide paths while others employ static risk-based allocations

What Are Robo-Advisors and How Do They Work?

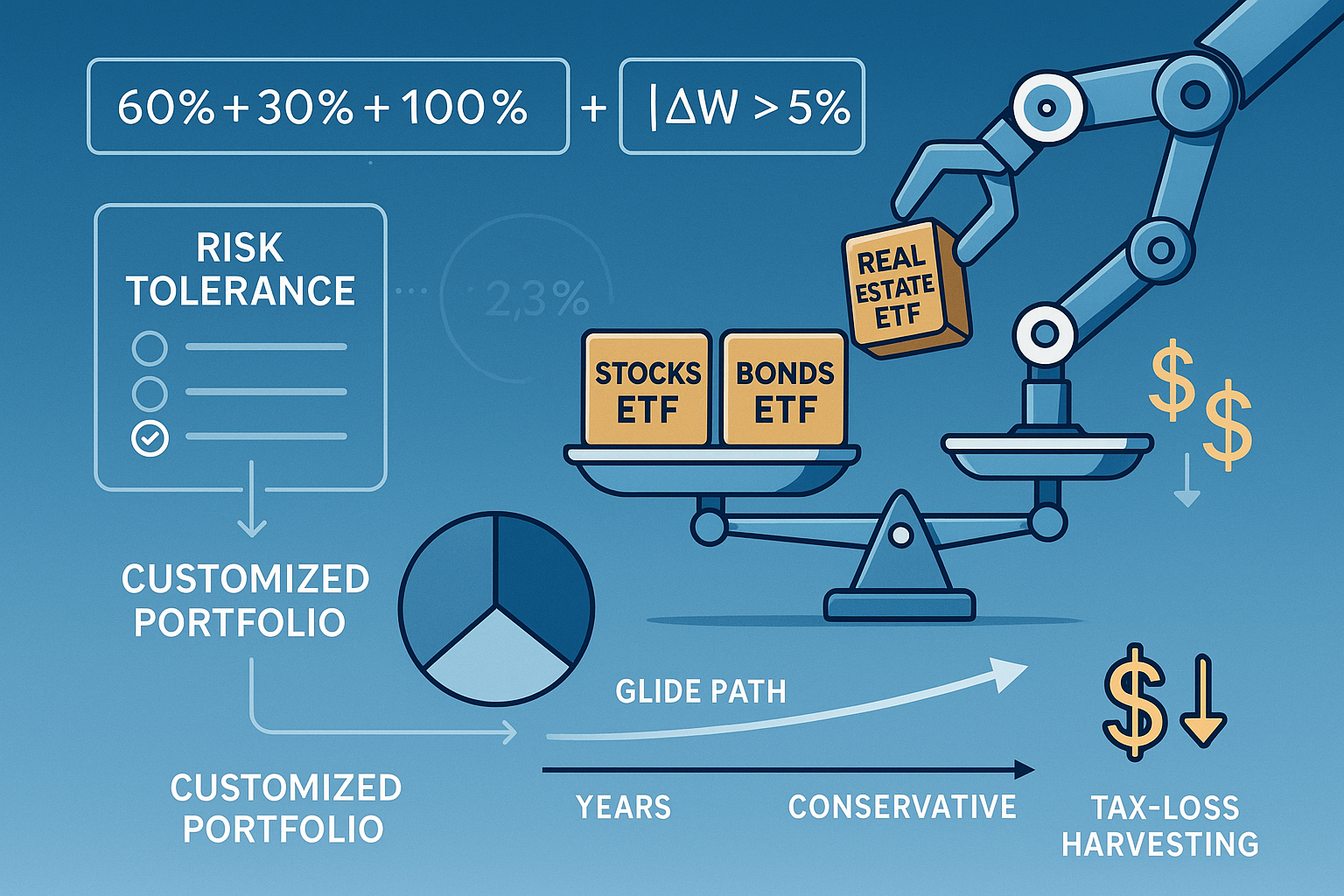

Robo-advisors are automated investment platforms that use algorithms to build, manage, and rebalance portfolios based on investor goals, time horizons, and risk tolerance.

The fundamental process follows a consistent pattern across platforms:

Step 1: Risk Assessment

Investors complete a questionnaire evaluating risk tolerance, investment timeline, and financial objectives. The algorithm assigns a risk score that determines asset allocation.

Step 2: Portfolio Construction

The platform builds a diversified portfolio using low-cost ETFs. Most robo-advisors use Modern Portfolio Theory (MPT) to optimize the risk-return relationship through diversification across asset classes.

Step 3: Automatic Rebalancing

As market movements shift portfolio allocations, the algorithm automatically sells overweight positions and buys underweight ones to maintain target percentages. This enforces the discipline of “buy low, sell high” without emotional interference.

Step 4: Tax Optimization

Advanced platforms implement tax-loss harvesting, selling securities at a loss to offset capital gains while maintaining market exposure through similar investments.

The Mathematical Advantage

The compound effect of lower fees creates exponential wealth differences. Consider two identical portfolios starting with $50,000 and contributing $500 monthly:

| Fee Level | 30-Year Value | Difference |

|---|---|---|

| 0.15% (Robo) | $847,392 | Baseline |

| 1.00% (Traditional) | $671,428 | -$175,964 |

This $175,964 difference represents the cost of higher fees compounded over three decades. The compound interest effect works against investors when fees increase.

Robo-advisors also eliminate behavioral errors. Research shows the average investor underperforms the market by 1.5-2.0% annually due to emotional buying and selling. Automated rebalancing removes this human element.

Top 7 Best Robo-Advisors in 2026

1. Vanguard Digital Advisor — Best for Low-Cost Index Investing

Management Fee: 0.15% annually

Minimum Investment: $100

Promotion: No advisory fees for first 90 days

Vanguard Digital Advisor uses the company’s Life-Cycle Investing Model to create customized portfolios of passive Vanguard ETFs. The platform implements glide path technology, gradually shifting allocations from aggressive growth to conservative income as investors approach their target date.

Portfolio Construction:

The algorithm evaluates investor age, goals, and risk tolerance to select from Vanguard’s extensive ETF lineup. Typical portfolios include:

- Vanguard Total Stock Market ETF (VTI)

- Vanguard Total International Stock ETF (VXUS)

- Vanguard Total Bond Market ETF (BND)

- Vanguard Total International Bond ETF (BNDX)

Key Features:

- Automatic rebalancing when allocations drift 5% from targets

- Tax-efficient fund placement

- Access to Vanguard’s institutional-grade research

- Integration with other Vanguard accounts

Best For: Investors who prioritize ultra-low costs and trust Vanguard’s passive indexing philosophy. The 0.15% fee is the lowest among major robo-advisors, making it ideal for long-term wealth building through index fund exposure.

2. Betterment — Best for Goal-Based Investing

Management Fee: 0.25% (Digital) to 0.65% (Premium with human advisors)

Minimum Investment: $0

NerdWallet Rating: 5.0/5

Founded in 2008 and launched in 2010, Betterment pioneered the robo-advisor industry. The platform excels at goal-based investing, allowing users to create separate portfolios for retirement, emergency funds, major purchases, and general investing.

Portfolio Options:

- Core Portfolio: Diversified global stocks and bonds

- Socially Responsible Investing (SRI): ESG-focused ETFs

- Goldman Sachs Smart Beta: Factor-based investing

- Income Portfolio: Higher bond allocation for cash flow

- Innovative Technology: Exposure to innovation-focused sectors

Tax Optimization:

Betterment’s tax-loss harvesting runs daily, scanning for opportunities to realize losses while maintaining market exposure. The platform claims this feature adds approximately 0.77% in annual after-tax returns [2].

Glide Path Technology:

Portfolios automatically become more conservative as investors approach their goal date. A 30-year retirement portfolio might start at 90% stocks, gradually shifting to 50% stocks by retirement age.

Premium Tier Benefits ($100,000+ accounts):

- Unlimited access to certified financial planners

- Comprehensive financial planning

- Tax coordination across accounts

- Estate planning guidance

Best For: Investors managing multiple financial goals simultaneously who value comprehensive planning tools and optional human advisor access. The goal-based approach aligns well with retirement planning using the 4% rule.

3. Wealthfront — Best for Tax-Loss Harvesting

Management Fee: 0.25%

Minimum Investment: $500

Key Feature: Daily tax-loss harvesting and direct indexing

Wealthfront combines automated portfolio management with advanced tax optimization strategies. The platform won Bankrate’s 2025 Award for its FDIC-insured cash management account offering competitive interest rates with no fees.

Portfolio Construction:

Wealthfront uses 10-12 ETFs across asset classes:

- US stocks (large, mid, small cap)

- International developed markets

- Emerging markets

- US bonds (government, corporate, municipal)

- Real estate (REITs)

- Natural resources

Tax-Loss Harvesting:

The algorithm scans portfolios daily for tax-loss harvesting opportunities. When a security drops below its purchase price, Wealthfront sells it and immediately purchases a correlated but non-identical ETF to maintain market exposure while realizing the tax loss.

Direct Indexing (accounts $100,000+):

Instead of holding ETFs, Wealthfront purchases individual stocks that comprise major indexes. This creates hundreds of additional tax-loss harvesting opportunities, potentially adding 1%+ in annual after-tax returns.

Additional Features:

- Commission-free stock and ETF trading

- Automated rebalancing

- Portfolio Line of Credit (borrow against portfolio at competitive rates)

- 529 college savings plans

- Cryptocurrency exposure through trusts

Best For: High-income investors in taxable accounts who benefit most from aggressive tax optimization. The daily tax-loss harvesting and direct indexing features provide maximum tax efficiency for capital gains management.

4. Fidelity Go — Best for Micro-Investing

Management Fee: $0 for balances under $25,000; 0.35% above

Minimum Investment: $10

Apple App Store Rating: 4.8/5

Fidelity Go removes cost barriers for beginning investors. The $0 fee structure for accounts under $25,000 makes it the most accessible premium robo-advisor for those starting their investment journey.

Portfolio Strategy:

Fidelity constructs portfolios using its proprietary Flex ETFs, low-cost index funds with expense ratios as low as 0.01%. Allocations range from conservative (20% stocks) to aggressive (85% stocks).

Automatic Features:

- Rebalancing when allocations drift 5% from targets

- Dividend reinvestment

- Tax-efficient fund placement

- Integration with Fidelity’s broader ecosystem

Account Access:

Investors can view portfolios through Fidelity’s mobile app or website. The platform provides educational content explaining investment decisions and market movements.

Upgrade Path:

As accounts grow beyond $25,000, the 0.35% fee remains competitive while providing access to Fidelity’s research, tools, and customer service.

Best For: Beginning investors with limited capital who want professional portfolio management without fees. The $10 minimum and zero-fee structure for smaller accounts makes this ideal for learning investing fundamentals through dollar-cost averaging.

5. Schwab Intelligent Portfolios — Best for Zero Management Fees

Management Fee: $0

Minimum Investment: $5,000

Portfolio Options: 12 customized risk profiles

Schwab Intelligent Portfolios stands alone in charging zero management fees. The platform generates revenue through cash allocations and the spread on uninvested cash.

Risk Assessment:

A comprehensive questionnaire evaluates risk tolerance, time horizon, and financial situation. Schwab assigns investors to one of 12 risk profiles ranging from “Income” to “Aggressive Growth.”

Portfolio Construction:

Portfolios include 17-20 asset classes using Schwab ETFs and third-party funds:

- US stocks (large, mid, small, value, growth)

- International developed and emerging markets

- Fixed income (government, corporate, high-yield, international)

- Real estate

- Commodities

- Cash (6-30% depending on risk profile)

Cash Allocation Controversy:

Critics note that required cash allocations (6-30% of portfolios) create opportunity cost. While this cash earns interest for Schwab, investors miss potential market returns. However, the zero management fee offsets this disadvantage for many investors.

Rebalancing:

Automatic rebalancing occurs when allocations drift significantly from targets or when deposits/withdrawals create imbalances.

Premium Option:

Schwab Intelligent Portfolios Premium charges a $300 initial planning fee and $30 monthly for unlimited access to certified financial planners.

Best For: Investors with $5,000+ who prioritize zero management fees and accept higher cash allocations as the trade-off. The diversification strategy across 17-20 asset classes provides comprehensive market exposure.

6. SoFi Automated Investing — Best for Low Minimum Investment

Management Fee: 0.25%

Minimum Investment: $50

NerdWallet Rating: 4.4/5 (October 2025)

SoFi Automated Investing combines robo-advisor functionality with the company’s broader financial ecosystem, including banking, lending, and insurance products.

Portfolio Strategy:

SoFi constructs portfolios using low-cost ETFs across six asset classes. Allocations range from conservative (30% stocks) to aggressive (90% stocks) based on risk tolerance.

Member Benefits:

SoFi members gain access to:

- Career coaching and networking events

- Financial planning consultations

- Unemployment protection (pauses loan payments)

- Exclusive member discounts

Automatic Features:

- Daily rebalancing monitoring

- Dividend reinvestment

- Tax-loss harvesting (for accounts $10,000+)

- Fractional shares

Integration:

SoFi’s ecosystem allows seamless money movement between checking, savings, investing, and loan accounts. This integration simplifies financial management for users by consolidating services.

Best For: Younger investors building comprehensive financial lives who value community features and ecosystem integration alongside automated investing. The $50 minimum removes barriers while the 0.25% fee remains competitive.

7. Acorns — Best for Round-Up Investing

Management Fee: $3-$12 monthly (tiered subscription)

Minimum Investment: $0

Unique Feature: Automatic round-ups from purchases

Acorns pioneered micro-investing through its signature “round-up” feature—automatically investing spare change from everyday purchases.

How Round-Ups Work:

Link credit or debit cards to Acorns. Each purchase rounds up to the nearest dollar, investing the difference. A $3.75 coffee becomes $4.00, with $0.25 invested automatically.

Subscription Tiers:

- Personal ($3/month): Automated investing and round-ups

- Personal Plus ($6/month): Adds retirement account (IRA)

- Premium ($12/month): Adds human advisor access and custodial accounts for children

Portfolio Options:

Five portfolios ranging from conservative to aggressive, constructed using ETFs across stocks, bonds, and real estate.

Additional Features:

- Earn bonus investments from 450+ partner brands

- Educational content on investing fundamentals

- Retirement planning tools

- Banking services with a debit card

Fee Consideration:

The flat monthly fee structure favors investors with larger balances. A $3 monthly fee on a $1,000 account equals 3.6% annually, far higher than percentage-based competitors. However, on a $10,000 account, the same $3 fee equals just 0.36% annually.

Best For: Beginning investors who struggle with consistent saving habits and prefer automatic micro-investing. The round-up feature creates compound growth from money that would otherwise be spent.

Key Features to Compare When Choosing Robo-Advisors

Management Fees and Total Cost of Ownership

Management fees represent the most critical factor in long-term returns. Even small differences compound dramatically over decades.

Fee Structures:

- Percentage-based: 0.15%-0.65% of assets annually

- Flat monthly: $3-$30 per month, regardless of balance

- Zero fee: No management charge (Schwab, Fidelity, Go under $25K)

Hidden Costs:

Beyond management fees, consider:

- Underlying ETF expense ratios: 0.03%-0.20% annually

- Trading costs: Most robo-advisors offer commission-free rebalancing

- Tax inefficiency: Poor tax management can cost 1%+ annually

Total Cost Example:

Vanguard Digital Advisor charges a 0.15% management fee plus approximately 0.07% weighted average ETF expense ratio = 0.22% total annual cost.

The absolute return after fees determines actual wealth accumulation, making fee comparison essential.

Minimum Investment Requirements

Minimum investments range from $0 to $5,000, affecting accessibility for beginning investors.

No Minimum ($0):

- Betterment

- Acorns

- SoFi Automated Investing (effectively $50)

Low Minimum ($10-$500):

- Fidelity Go: $10

- Vanguard Digital Advisor: $100

- Wealthfront: $500

Higher Minimum ($5,000):

- Schwab Intelligent Portfolios: $5,000

Lower minimums democratize investing but may limit advanced features. Wealthfront’s direct indexing requires $100,000, while Betterment’s Premium tier needs $100,000.

Tax-Loss Harvesting Capabilities

Tax-loss harvesting adds significant after-tax returns by offsetting capital gains with realized losses.

How It Works:

- The algorithm identifies securities trading below the purchase price

- Sells the security to realize the loss

- Immediately purchases a correlated but non-identical security

- Maintains market exposure while harvesting the tax benefit

Annual Value:

Studies show tax-loss harvesting adds 0.5%-1.5% in annual after-tax returns, depending on market volatility and tax bracket.

Platform Comparison:

- Daily harvesting: Wealthfront, Betterment

- Periodic harvesting: Most other platforms

- Direct indexing: Wealthfront (accounts $100,000+)

- No tax-loss harvesting: Schwab Intelligent Portfolios, Acorns

For investors in high tax brackets with taxable accounts, this feature justifies higher management fees through superior after-tax performance.

Portfolio Customization and Investment Options

Robo-advisors vary significantly in portfolio flexibility and investment choices.

Standard Portfolios:

Most platforms offer 3-5 pre-built portfolios ranging from conservative to aggressive. Asset allocation shifts based on risk tolerance.

Specialized Portfolios:

- Socially Responsible Investing (SRI): Betterment, Wealthfront

- Halal investing: Wahed Invest

- Smart beta/factor investing: Betterment (Goldman Sachs Smart Beta)

- Income-focused: Betterment Income Portfolio

Customization Levels:

- No customization: Acorns, Fidelity Go

- Limited customization: Adjust risk tolerance

- Moderate customization: Choose from multiple portfolio strategies

- High customization: Wealthfront allows stock/ETF trading alongside automated portfolios

Asset Class Coverage:

Advanced platforms include:

- International developed markets

- Emerging markets

- Real estate (REITs)

- Commodities

- Municipal bonds (for high-income investors)

- Cryptocurrency exposure (select platforms)

Investors seeking the best ETFs across diverse asset classes benefit from platforms offering comprehensive market exposure.

Human Advisor Access

Some robo-advisors provide hybrid models combining algorithmic management with human financial planning.

Advisor Access Tiers:

- No human access: Fidelity Go, Acorns Personal

- Email/chat support: Most platforms

- Phone consultations: Betterment Premium, SoFi

- Unlimited advisor access: Schwab Intelligent Portfolios Premium, Vanguard Personal Advisor Services

Cost of Human Advice:

- Betterment Premium: 0.65% (requires $100,000)

- Schwab Intelligent Portfolios Premium: $300 initial + $30/month

- Vanguard Personal Advisor Services: 0.30% (requires $50,000)

Services Provided:

Certified financial planners help with:

- Comprehensive financial planning

- Tax strategy coordination

- Retirement income planning

- Estate planning basics

- College savings optimization

Value Proposition:

Human advisors add value for complex financial situations, multiple income sources, business ownership, significant assets, or major life transitions. Simple accumulation strategies rarely justify the additional cost.

Account Types and Integration

Robo-advisors support various account types, affecting tax treatment and withdrawal rules.

Standard Account Types:

- Individual taxable accounts: Maximum flexibility, no contribution limits

- Traditional IRA: Tax-deductible contributions, taxed withdrawals

- Roth IRA: After-tax contributions, tax-free growth, and withdrawals

- SEP IRA: Self-employed retirement accounts

- Joint accounts: Shared ownership

- Trust accounts: Estate planning vehicles

Specialized Accounts:

- 529 college savings: Wealthfront, Betterment

- Custodial accounts (UTMA/UGMA): Acorns, Betterment

- 401(k) rollovers: Most platforms accept

Account Integration:

Leading platforms allow linking external accounts to:

- View the complete financial picture

- Coordinate tax strategies across accounts

- Track progress toward multiple goals

- Optimize asset location (tax-efficient fund placement)

Understanding active vs passive income helps determine optimal account types for different income sources.

How to Choose the Right Robo-Advisor for Your Needs

Step 1: Calculate Your Total Investment Costs

Compare the all-in cost, including management fees and underlying fund expenses.

Formula:

Total Annual Cost = Management Fee + Weighted Average ETF Expense Ratio

Example Comparison (on $50,000 portfolio):

| Platform | Management Fee | ETF Expenses | Total Cost | Annual $ Cost |

|---|---|---|---|---|

| Vanguard | 0.15% | 0.07% | 0.22% | $110 |

| Betterment | 0.25% | 0.10% | 0.35% | $175 |

| Wealthfront | 0.25% | 0.08% | 0.33% | $165 |

| Schwab | 0.00% | 0.12% | 0.12% | $60 |

| Fidelity Go | 0.35% | 0.05% | 0.40% | $200 |

Over 30 years with 7% returns and $500 monthly contributions, the difference between 0.22% (Vanguard) and 0.40% (Fidelity Go) equals approximately $48,000 in lost compound growth.

Step 2: Assess Your Tax Situation

Tax optimization features add significant value for high-income investors in taxable accounts.

Questions to Consider:

- What is your marginal tax bracket?

- Are you investing in taxable or retirement accounts?

- Do you have capital gains to offset?

- Will you need to withdraw funds before retirement?

Tax Feature Value by Bracket:

| Tax Bracket | Tax-Loss Harvesting Value | Recommended Platforms |

|---|---|---|

| 10-12% | Low (0.1-0.3% annually) | Any platform acceptable |

| 22-24% | Medium (0.4-0.8% annually) | Platforms with TLH |

| 32%+ | High (0.8-1.5% annually) | Wealthfront, Betterment |

High earners benefit most from daily tax-loss harvesting and direct indexing, justifying slightly higher management fees through superior after-tax returns.

Step 3: Evaluate Your Investment Timeline

Time horizon affects optimal portfolio construction and platform selection.

Short-Term Goals (0-5 years):

- Emergency funds

- Home down payment

- Major purchases

Recommended approach: Conservative allocations (30-40% stocks) with high-quality bond exposure. Consider Betterment’s goal-based investing or high-yield savings alternatives.

Medium-Term Goals (5-15 years):

- College funding

- Early retirement planning

- Business capital accumulation

Recommended approach: Moderate allocations (50-70% stocks) with a gradual glide path. Platforms with 529 plans (Wealthfront, Betterment) or goal-based features excel here.

Long-Term Goals (15+ years):

- Traditional retirement

- Generational wealth building

- Legacy planning

Recommended approach: Aggressive allocations (80-90% stocks) with focus on minimizing fees. Vanguard Digital Advisor’s 0.15% fee maximizes compound growth over decades.

The 50/30/20 budgeting rule helps determine how much to allocate toward long-term investing versus shorter-term goals.

Step 4: Determine Your Need for Human Guidance

Assess whether your financial situation requires professional advice beyond algorithmic management.

DIY-Friendly Situations:

- Single income source

- Straightforward tax situation

- Simple accumulation phase

- Strong financial literacy

Recommended: Pure robo-advisors (Vanguard, Wealthfront, Schwab)

Complex Situations Benefiting from Advisors:

- Multiple income streams (W-2, business, rental, investment income)

- Stock options or equity compensation

- Significant assets requiring estate planning

- Tax-loss carryforwards or complex deductions

- Business ownership

- Approaching retirement with pension decisions

Recommended: Hybrid platforms (Betterment Premium, Schwab Premium, Vanguard Personal Advisor Services)

Cost-Benefit Analysis:

A 0.40% fee increase for advisor access costs $2,000 annually on a $500,000 portfolio. If the advisor saves $2,000+ through tax optimization, Social Security timing, or withdrawal strategies, the service pays for itself.

Step 5: Consider Your Behavioral Tendencies

Robo-advisors provide different levels of engagement and education.

Hands-Off Investors:

Prefer “set and forget” automation with minimal interaction.

Recommended: Fidelity Go, Schwab Intelligent Portfolios, Vanguard Digital Advisor

Engaged Learners:

Want educational content explaining investment decisions and market movements.

Recommended: Betterment (extensive educational resources), SoFi (member education events)

Tinkerers:

Desire the ability to customize alongside automation.

Recommended: Wealthfront (allows stock trading), Betterment (multiple portfolio options)

Behavioral Savers:

Struggle with consistent contributions and benefit from automatic features.

Recommended: Acorns (round-ups), platforms with automatic deposit features

Understanding personal behavioral patterns prevents abandoning the investment strategy during market volatility—the primary cause of underperformance.

The Math Behind Robo-Advisor Performance

Rebalancing Discipline Creates Excess Returns

Automatic rebalancing enforces the fundamental principle of buying low and selling high.

How Rebalancing Works:

A 60/40 stock/bond portfolio starts with $60,000 in stocks and $40,000 in bonds. After a strong stock market year, the portfolio becomes $75,000 stocks / $42,000 bonds (64%/36%).

Rebalancing sells $4,680 in stocks and buys $4,680 in bonds to restore the 60/40 allocation.

The Rebalancing Bonus:

This systematic approach:

- Takes profits from outperforming assets (sells high)

- Adds to underperforming assets (buys low)

- Maintains target risk level

- Captures mean reversion when asset classes cycle

Academic research shows rebalancing adds 0.35%-0.50% annually to returns while reducing volatility.

Rebalancing Frequency:

- Too frequent: Generates unnecessary trading costs and taxes

- Too infrequent: Allows significant drift from target allocation

- Optimal: When allocations drift 5% from targets or quarterly, whichever comes first

Robo-advisors execute this discipline automatically, removing emotional interference.

Tax-Loss Harvesting: The Mathematical Edge

Tax-loss harvesting converts market volatility into tax savings.

The Mechanism:

An investor purchases VTI (Vanguard Total Stock Market ETF) at $200. The price drops to $180. The robo-advisor:

- Sells VTI, realizing a $20 loss

- Immediately purchases SCHB (Schwab Total Stock Market ETF)

- Maintains market exposure to US stocks

- Creates a $20 tax deduction

Tax Savings Calculation:

$20 loss × 32% marginal tax rate = $6.40 tax savings

Annual Impact:

In volatile markets, algorithms identify dozens of harvesting opportunities. A $100,000 portfolio might harvest $5,000-$15,000 in losses annually.

At a 32% tax rate, harvesting $10,000 in losses saves $3,200 in taxes = 3.2% boost to after-tax returns for that year.

Long-Term Consideration:

Tax-loss harvesting defers taxes rather than eliminating them. The lower cost basis means higher taxes when eventually selling. However, deferral provides three advantages:

- Time value of money: Taxes paid decades later are worth less in present value

- Rate arbitrage: Short-term losses offset high-rate ordinary income; eventual gains taxed at lower long-term rates

- Step-up at death: Cost basis resets for heirs, eliminating deferred taxes

The expected return increases when tax drag decreases through systematic harvesting.

Fee Compression and Compound Growth

The relationship between fees and final wealth follows an exponential curve.

30-Year Projection:

Starting balance: $50,000

Monthly contribution: $500

Annual return: 7% (before fees)

| Annual Fee | Final Value | Fees Paid | Wealth Lost to Fees |

|---|---|---|---|

| 0.15% | $847,392 | $36,608 | Baseline |

| 0.25% | $831,147 | $60,853 | $16,245 |

| 0.50% | $799,105 | $120,895 | $48,287 |

| 1.00% | $738,148 | $241,852 | $109,244 |

Key Insight:

A 0.85% fee difference (1.00% vs 0.15%) doesn’t reduce returns by 85%—it reduces final wealth by 12.9% ($109,244 / $847,392).

This non-linear relationship occurs because fees compound negatively. Each year, investors pay fees on the fees from previous years that could have been growing.

The Fee-Free Alternative:

Investors comfortable with DIY portfolio management can replicate robo-advisor strategies using the same ETFs, eliminating management fees. However, this requires:

- Disciplined rebalancing

- Tax-loss harvesting knowledge

- Emotional control during volatility

- Time for portfolio maintenance

For most investors, paying 0.15%-0.25% for automated discipline provides superior results versus attempting DIY management and making behavioral errors.

Advanced Robo-Advisor Strategies

Using Multiple Robo-Advisors for Optimization

Sophisticated investors combine platforms to maximize benefits.

Strategy 1: Tax-Optimized Split

- Taxable account: Wealthfront (daily tax-loss harvesting, direct indexing)

- Roth IRA: Vanguard Digital Advisor (lowest fees for tax-free growth)

- Traditional 401(k): Fidelity Go (zero fees under $25K, low fees above)

Rationale: Tax-loss harvesting only benefits taxable accounts. Retirement accounts prioritize low fees since tax optimization is irrelevant.

Strategy 2: Goal-Based Allocation

- Retirement (30+ years): Vanguard Digital Advisor (aggressive, low-cost)

- Home down payment (5 years): Betterment (conservative goal-based portfolio)

- Emergency fund: High-yield savings (Wealthfront cash account)

Strategy 3: Fee Arbitrage

- Accounts under $25,000: Fidelity Go (zero fees)

- Accounts over $25,000: Vanguard Digital Advisor (0.15% beats Fidelity’s 0.35%)

This approach requires tracking multiple accounts but optimizes for the lowest total cost across the portfolio.

Combining Robo-Advisors with Self-Directed Investing

Hybrid approaches blend automated core holdings with tactical positions.

Core-Satellite Strategy:

- Core (70-80%): Robo-advisor manages a diversified index portfolio

- Satellite (20-30%): Self-directed individual stocks or sector ETFs

Implementation:

Wealthfront allows commission-free stock trading alongside automated portfolios. Investors maintain disciplined core exposure while expressing tactical views through satellite positions.

Risk Management:

The robo-advisor core provides:

- Automatic rebalancing

- Diversification

- Behavioral discipline

The satellite allows:

- Concentrated positions in high-conviction ideas

- Sector rotation

- Individual stock selection

Performance Tracking:

Compare satellite performance against the core portfolio. If satellite positions consistently underperform, reduce allocation and increase automated exposure.

This strategy works best for investors with dividend investing knowledge who want to hold specific dividend growth stocks while maintaining automated diversification.

Maximizing Tax Alpha Through Account Location

Strategic asset placement across account types enhances after-tax returns.

Tax-Efficient Assets (Taxable Accounts):

- Total stock market index funds (qualified dividends, long-term capital gains)

- Municipal bonds (tax-free interest for high earners)

- Growth stocks (no current income, deferred taxation)

Tax-Inefficient Assets (Retirement Accounts):

- REITs (non-qualified dividends taxed as ordinary income)

- High-yield bonds (interest taxed as ordinary income)

- Actively managed funds (frequent capital gains distributions)

Robo-Advisor Implementation:

Most platforms automatically optimize asset location when managing multiple account types. Betterment’s “tax coordination” feature places tax-inefficient assets in IRAs and tax-efficient assets in taxable accounts.

Quantified Benefit:

Proper asset location adds 0.10%-0.30% annually in after-tax returns, depending on tax bracket and asset mix.

Common Robo-Advisor Mistakes to Avoid

Mistake 1: Choosing Based on Fees Alone

The lowest fee doesn’t always produce the highest after-tax returns.

Example:

Schwab Intelligent Portfolios charges 0% management fees but requires 6-30% cash allocations. On a $100,000 portfolio with 20% cash allocation:

- $20,000 sits in cash, earning 4% = $800 annually

- If invested in stocks earning 10% = $2,000 annually

- Opportunity cost: $1,200 annually = 1.2% of portfolio

Meanwhile, Vanguard Digital Advisor charges 0.15% ($150 on $100,000) but maintains full market exposure. The net benefit of Vanguard exceeds Schwab by $1,050 annually despite charging fees.

Lesson: Evaluate total return after all costs, not just management fees.

Mistake 2: Abandoning the Strategy During Volatility

Market downturns trigger emotional selling—the primary destroyer of wealth.

The Behavioral Gap:

Dalbar’s Quantitative Analysis of Investor Behavior shows the average equity investor earned 7.13% annually over the 20 years ending 2019, while the S&P 500 returned 9.96% [6]. The 2.83% gap results from buying high during euphoria and selling low during panic.

Robo-Advisor Protection:

Automated investing removes the sell button during crashes. Portfolios continue rebalancing, buying stocks when they’re cheapest.

2020 Example:

During the March 2020 COVID crash, the S&P 500 dropped 34%. Robo-advisors automatically rebalanced, selling bonds (which held steady) to buy stocks at depressed prices. Investors who maintained their strategy captured the subsequent 68% rally through year-end.

Lesson: Select a risk tolerance you can maintain during 30-40% drawdowns. Switching to conservative allocations after crashes locks in losses.

Mistake 3: Ignoring Account Type Tax Implications

Contributing to the wrong account type costs thousands in unnecessary taxes.

Traditional vs. Roth Decision:

- Traditional IRA/401(k): Tax deduction now, taxed withdrawals later

- Roth IRA/401(k): No deduction now, tax-free withdrawals later

Optimal Strategy:

- Low current tax bracket (10-12%): Roth (pay low taxes now, avoid higher taxes later)

- High current tax bracket (32%+): Traditional (deduct at high rate now, withdraw at lower rate in retirement)

- Peak earning years: Traditional

- Early career: Roth

Robo-Advisor Limitation:

Most platforms don’t provide account type guidance. Investors must determine optimal account selection independently or consult a tax professional.

Quantified Impact:

A 30-year-old in the 12% bracket contributing $6,000 annually to a Roth instead of a Traditional saves approximately $89,000 in lifetime taxes, assuming retirement in the 22% bracket [7].

Mistake 4: Failing to Coordinate with Other Accounts

Robo-advisors optimize individual accounts but can’t manage assets they don’t control.

Common Scenario:

- Robo-advisor manages 60/40 stock/bond allocation in taxable account

- Employer 401(k) holds 100% stocks

- Total portfolio becomes 80/20 stocks/bonds—far more aggressive than intended

Solution:

Link external accounts to robo-advisors offering account aggregation (Betterment, Wealthfront). These platforms view the complete financial picture and adjust managed accounts to achieve the target overall allocation.

Alternative:

Manually calculate total portfolio allocation across all accounts and adjust robo-advisor settings to compensate for external holdings.

Mistake 5: Overlooking Minimum Balance Requirements for Features

Premium features often require higher balances.

Feature Thresholds:

- Tax-loss harvesting: $10,000+ (SoFi)

- Direct indexing: $100,000+ (Wealthfront)

- Human advisor access: $100,000+ (Betterment Premium)

- Lowest fee tier: $25,000+ (Fidelity Go)

Strategy:

Begin with platforms offering full features at low minimums (Betterment, Wealthfront). As balances grow, evaluate whether switching to lower-fee platforms (Vanguard) makes sense.

Switching Costs:

Moving accounts between robo-advisors triggers:

- Potential taxable events (selling positions)

- Brief market exposure gap during transfer

- Administrative hassle

For taxable accounts, switching costs often exceed fee savings unless the balance is substantial. Retirement accounts transfer without tax consequences, making them easier to move.

Conclusion

Best Robo-Advisors in 2025 deliver institutional-grade portfolio management to investors at all wealth levels. The math behind these platforms is clear: low fees, automatic rebalancing, tax optimization, and behavioral discipline combine to produce superior long-term results compared to emotional self-directed investing or high-cost traditional advisors.

Platform Selection Summary:

- Lowest fees: Vanguard Digital Advisor (0.15%) or Schwab Intelligent Portfolios ($0)

- Best tax optimization: Wealthfront (daily tax-loss harvesting, direct indexing)

- Most accessible: Fidelity Go ($10 minimum, $0 fees under $25K)

- Goal-based investing: Betterment (multiple portfolios, glide paths)

- Micro-investing: Acorns (round-ups, automatic saving)

The difference between a 0.15% fee and a 1.00% traditional advisor fee compounds to $175,964 over 30 years on a $50,000 starting balance with $500 monthly contributions. This mathematical reality makes robo-advisors the optimal choice for most investors during wealth accumulation phases.

Next Steps:

- Calculate your total investment costs across current accounts using the formula: Management Fee + ETF Expense Ratios

- Determine your tax situation and whether tax-loss harvesting justifies higher fees

- Assess your timeline for each financial goal and select appropriate risk allocations

- Open an account with the platform that matches your needs and automate monthly contributions

- Link external accounts for comprehensive portfolio coordination

- Set calendar reminders to review performance annually (not daily/weekly)

The evidence is clear: automated, low-cost, diversified investing through robo-advisors produces superior results for investors who maintain discipline through market cycles. The math behind money favors those who minimize costs, maximize tax efficiency, and eliminate emotional decision-making.

Begin with platforms offering zero minimums (Betterment, Fidelity Go) to start building compound growth immediately. As balances grow, optimize fee structures by moving to ultra-low-cost providers like Vanguard Digital Advisor.

The path to wealth building follows a simple formula: consistent contributions + low costs + long time horizons + behavioral discipline = financial independence. Robo-advisors automate this formula, removing the primary obstacles that prevent most investors from achieving their financial goals.

References

[1] Dalbar, Inc. (2020). “Quantitative Analysis of Investor Behavior.” Retrieved from: https://www.dalbar.com/

[2] Betterment. (2024). “Tax-Loss Harvesting White Paper.” Retrieved from: https://www.betterment.com/

[3] Wealthfront. (2024). “The Value of Tax-Loss Harvesting.” Retrieved from: https://www.wealthfront.com/

[4] Vanguard Research. (2023). “The Value of Rebalancing.” Retrieved from: https://investor.vanguard.com/

[5] Morningstar. (2024). “Asset Location Strategies.” Retrieved from: https://www.morningstar.com/

[6] Dalbar, Inc. (2020). “Quantitative Analysis of Investor Behavior – 2020 Edition.” Retrieved from: https://www.dalbar.com/

[7] Internal Revenue Service. (2025). “Retirement Topics – IRA Contribution Limits.” Retrieved from: https://www.irs.gov/

Author Bio

Max Fonji is a data-driven financial educator and the voice behind The Rich Guy Math. With expertise in quantitative analysis and evidence-based investing, Max explains the mathematical principles behind wealth building, helping investors understand how compound growth, risk management, and valuation truly work. His approach combines analytical precision with educational clarity, making complex financial concepts accessible to beginners and intermediate investors.

Educational Disclaimer

This article is provided for educational and informational purposes only. It does not constitute financial, investment, tax, or legal advice. The information presented represents general principles and should not be considered personalized recommendations for any specific individual or situation.

Investing involves risk, including potential loss of principal. Past performance does not guarantee future results. Robo-advisor platforms, fees, features, and minimum investments change frequently; verify current details directly with providers before making investment decisions.

Consult with qualified financial, tax, and legal professionals before making investment decisions. Individual circumstances vary significantly, and professional guidance ensures strategies align with personal goals, risk tolerance, and tax situations.

The Rich Guy Math and its authors do not receive compensation from the robo-advisor platforms mentioned in this article. All analysis represents independent research and educational content.

Frequently Asked Questions

Are robo-advisors safe and secure?

Yes. Robo-advisors are regulated by the SEC and FINRA, maintaining the same legal protections as traditional brokerages. Accounts receive SIPC insurance covering up to $500,000 in securities (including $250,000 in cash) if the firm fails. Major platforms use bank-level encryption, two-factor authentication, and segregated client assets. The investment risk remains (markets can decline), but the platform security matches traditional financial institutions.

Can I lose money with a robo-advisor?

Yes. Robo-advisors invest in market-based securities (stocks, bonds, ETFs) that fluctuate in value. During market downturns, portfolio values decline. However, robo-advisors don’t increase market risk—they simply automate portfolio management. Diversification and automatic rebalancing actually reduce risk compared to concentrated individual stock positions. The primary risk is market risk, not platform risk.

How do robo-advisors make money if fees are so low?

Robo-advisors generate revenue through management fees (percentage of assets), subscription fees (flat monthly charges), or cash spreads (earning interest on uninvested cash). Their business model works because automation dramatically reduces operational costs compared to human advisors. A single algorithm manages thousands of accounts simultaneously, creating economies of scale impossible for traditional advisors.

Should I use a robo-advisor or hire a human financial advisor?

Use a robo-advisor if you have straightforward financial situations—accumulating wealth through regular contributions with standard tax situations. Hire a human advisor for complex scenarios: business ownership, stock options, significant assets requiring estate planning, or approaching retirement with pension decisions. Many investors use robo-advisors during accumulation years (20s–50s) then transition to human advisors near retirement when distribution strategies become critical.

Can I withdraw money from my robo-advisor account anytime?

Yes for taxable accounts—withdraw anytime without penalties (though you’ll owe capital gains taxes on profits). Retirement accounts (IRAs, 401(k)s) follow standard IRS rules: withdrawals before age 59½ typically incur 10% penalties plus ordinary income taxes. Robo-advisors don’t add withdrawal restrictions beyond standard account type rules. Most platforms process withdrawal requests within 3–5 business days.

Do robo-advisors work during market crashes?

Yes, and they often perform better than emotional human investors. During crashes, robo-advisors continue automatic rebalancing—selling bonds (which hold value) to buy stocks (at depressed prices). This enforces “buy low” discipline when humans panic and sell. The 2020 COVID crash demonstrated this: robo-advisor clients who maintained their strategy captured the full recovery, while many self-directed investors sold at the bottom and missed the rebound.

How are robo-advisors different from just buying index funds myself?

Robo-advisors add automatic rebalancing, tax-loss harvesting, diversification across multiple asset classes, and behavioral discipline. DIY index investing requires manually rebalancing (most investors don’t), implementing tax strategies (complex), and avoiding emotional decisions (difficult during volatility). The 0.15%–0.25% fee pays for automation and discipline. Investors with strong financial knowledge and emotional control can replicate robo-advisor strategies independently, but most achieve better results with automated management.