A single number on your credit card determines whether you build wealth or damage your financial future, yet most cardholders never understand how it works.

Your credit limit isn’t just the maximum you can spend. It’s a mathematical signal that lenders use to calculate your creditworthiness, influence your credit score, and assess your financial risk. Understanding the mechanics behind credit limits reveals how banks make lending decisions and how you can optimize your credit profile for better rates, higher limits, and long-term financial flexibility.

For a broader context, see our credit education guide.

This guide breaks down the math behind credit limits, the underwriting factors lenders use, and the precise formulas that connect your spending to your credit score. By the end, you’ll know exactly how to manage your credit limit strategically, with data, not guesswork.

Key Takeaways

Credit limit is the maximum amount a lender allows you to borrow on a revolving credit account—it directly impacts your credit utilization ratio, which accounts for 30% of your FICO score.

Lenders determine your credit limit using credit score, income, debt-to-income ratio (DTI), payment history, and proprietary risk algorithms—not arbitrary decisions.

Credit utilization formula: (Total Credit Card Balances ÷ Total Credit Limits) × 100—keeping this below 30% (ideally below 10%) protects your credit score.

Higher credit limits improve your utilization ratio without changing spending behavior—but only if you maintain discipline and avoid lifestyle inflation.

Credit limit decreases trigger immediate utilization spikes—a $10,000 limit cut to $5,000 doubles your utilization percentage, potentially dropping your score 20-50 points.

What Is a Credit Limit? (Simple Definition)

A credit limit is the maximum dollar amount a lender authorizes you to borrow on a revolving credit account, such as a credit card or line of credit.

Unlike installment loans (mortgages, auto loans) with fixed repayment schedules, revolving credit allows you to borrow, repay, and borrow again, up to your credit limit, without reapplying. The limit represents the lender’s assessment of your ability and willingness to repay based on your financial profile and credit history.

Why Lenders Set Limits

Lenders use credit limits to manage risk exposure. By capping the amount you can borrow, they limit potential losses if you default. The limit also serves as a behavioral signal: responsible borrowers who stay well below their limits demonstrate financial discipline, while those who max out cards signal higher default risk.

Credit limits are not static. Lenders review accounts periodically and adjust limits based on payment behavior, income changes, and overall credit market conditions. This dynamic process reflects ongoing risk assessment.

Credit Limit vs Available Credit vs Credit Line

These terms are related but distinct:

- Credit Limit: The total borrowing capacity authorized by the lender (e.g., $10,000).

- Available Credit: The unused portion of your credit limit after subtracting your current balance (e.g., $10,000 limit – $2,000 balance = $8,000 available).

- Credit Line: Often used interchangeably with credit limit, but technically refers to the revolving nature of the account (you can “draw” from the line repeatedly).

Understanding this distinction matters because available credit is what you can actually spend right now, while your credit limit determines your utilization ratio, the key metric that impacts your credit score.

How Lenders Determine Your Credit Limit

Credit limit decisions aren’t arbitrary. Lenders use quantitative models that weigh multiple risk factors to calculate the optimal limit that maximizes profit while minimizing default risk.

Credit Score Ranges and Typical Limits

Your credit score is the primary determinant of your initial credit limit. Higher scores correlate with higher limits because they signal lower default probability.

Typical Credit Limit Ranges by Credit Score (2025):

| Credit Score Range | Risk Category | Typical First Card Limit | Typical Prime Card Limit |

|---|---|---|---|

| 300-579 | Poor | $200-$500 (secured) | Not approved |

| 580-669 | Fair | $500-$2,000 | $2,000-$5,000 |

| 670-739 | Good | $2,000-$7,000 | $5,000-$15,000 |

| 740-799 | Very Good | $7,000-$15,000 | $15,000-$25,000 |

| 800-850 | Exceptional | $15,000-$30,000+ | $25,000-$50,000+ |

Source: Experian, FICO, and major credit card issuer data (2025)

These ranges vary by issuer and card type. Premium rewards cards typically require higher scores and offer higher limits than basic cards.

Income, Employment, and Debt-to-Income (DTI)

Lenders verify your ability to repay by analyzing your income and existing debt obligations.

Debt-to-Income Ratio (DTI) Formula:

DTI = (Total Monthly Debt Payments ÷ Gross Monthly Income) × 100

Example:

- Monthly debt payments: $2,150 (mortgage, car loan, student loans)

- Gross monthly income: $6,000

- DTI = ($2,150 ÷ $6,000) × 100 = 35.8%

Most credit card issuers prefer DTI ratios below 43% for new credit approvals. Lower DTI ratios signal more capacity to take on additional debt, resulting in higher credit limits.

Lenders also consider:

- Employment stability: Longer tenure at current employer reduces risk

- Income verification: W-2s, pay stubs, or tax returns confirm stated income

- Income trends: Rising income over time suggests lower default risk

The 50/30/20 rule budgeting framework helps maintain healthy DTI ratios by allocating 50% of income to needs, 30% to wants, and 20% to savings and debt repayment.

Credit History and Repayment Behavior

Length of credit history and payment patterns provide behavioral evidence of creditworthiness.

Key factors lenders analyze:

- Payment History (35% of FICO score): Late payments, especially 30+ days past due, significantly reduce credit limits. Consistent on-time payments increase limit approval odds.

- Credit Age: The Average age of accounts matters. A 10-year credit history with no derogatory marks signals stability. New borrowers with thin files receive lower initial limits.

- Account Mix: Diverse credit types (revolving credit, installment loans, mortgages) demonstrate experience managing different debt structures. Understanding credit mix helps optimize this factor.

- Recent Credit Inquiries: Multiple hard inquiries in short periods suggest credit-seeking behavior, which lenders interpret as financial stress. This reduces the limit approval amounts.

Internal Bank Risk Models and Algorithms

Beyond standardized credit scores, each lender uses proprietary algorithms that incorporate:

- Internal account performance: How you’ve managed previous accounts with that specific lender

- Behavioral scoring: Transaction patterns, payment timing, balance trends

- Market segmentation: Industry-specific risk models (e.g., healthcare professionals vs. gig workers)

- Economic conditions: Recession periods trigger tighter credit standards across all score ranges

- Competitive positioning: Lenders may offer higher limits to acquire customers from competitors

These models use machine learning to predict default probability with greater precision than credit scores alone. As a result, two applicants with identical credit scores may receive different limits based on these nuanced factors.

Takeaway: Credit limit decisions combine objective data (score, income, DTI) with subjective risk modeling. Optimizing the controllable factors, payment history, utilization, and income documentation maximizes your limit potential.

How Your Credit Limit Affects Your Credit Score

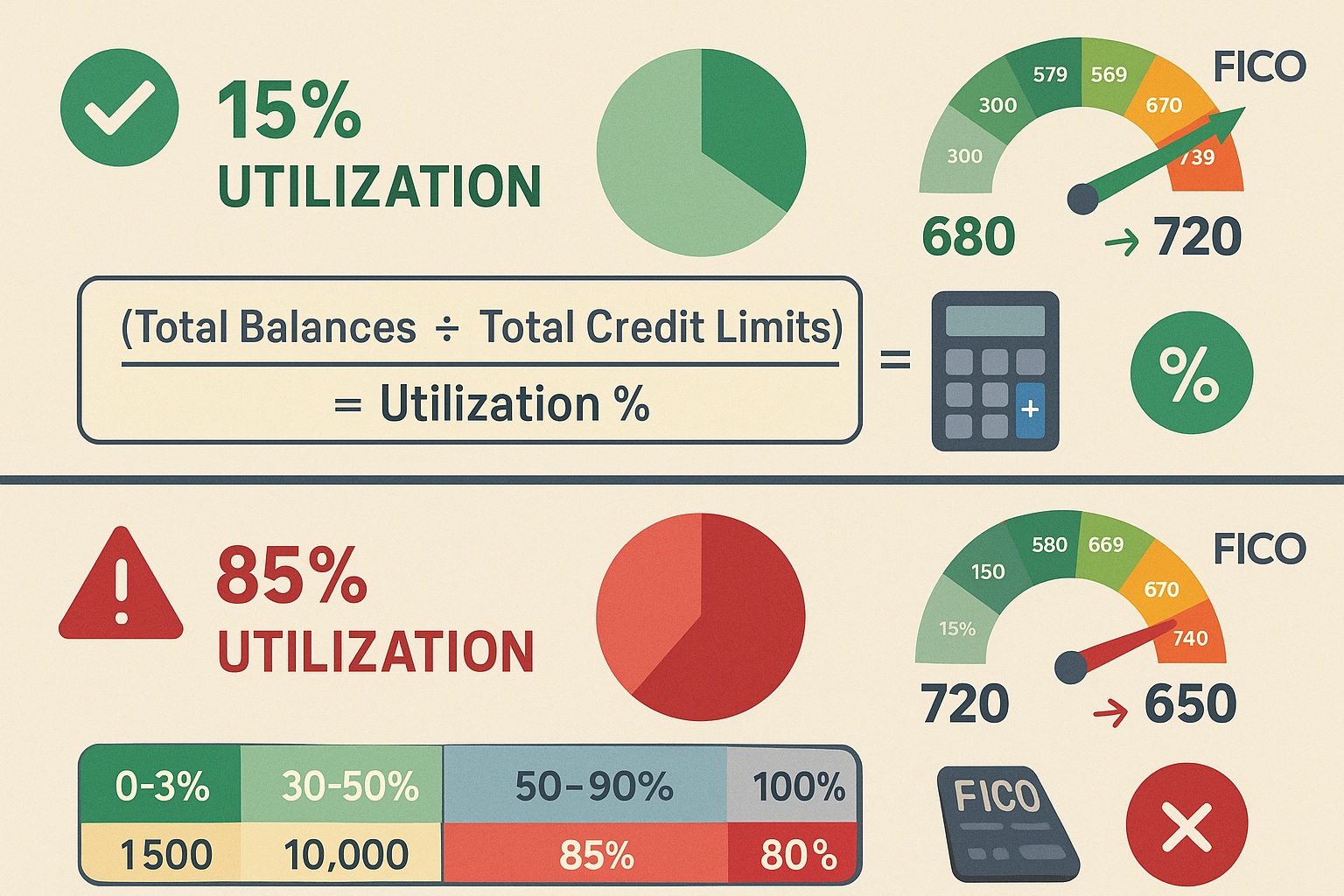

Your credit limit directly influences your credit score through one critical metric: the credit utilization ratio.

Credit Utilization Formula (With Examples)

Credit Utilization Ratio = (Total Credit Card Balances ÷ Total Credit Limits) × 100

This ratio accounts for approximately 30% of your FICO credit score—the second-largest factor after payment history (35%).

Example 1: Low Utilization (Optimal)

- Total credit limits: $20,000

- Total balances: $2,000

- Utilization: ($2,000 ÷ $20,000) × 100 = 10%

- Impact: Positive—signals responsible credit management

Example 2: Moderate Utilization (Acceptable)

- Total credit limits: $15,000

- Total balances: $4,500

- Utilization: ($4,500 ÷ $15,000) × 100 = 30%

- Impact: Neutral to slightly negative—approaching risk threshold

Example 3: High Utilization (Damaging)

- Total credit limits: $8,000

- Total balances: $7,200

- Utilization: ($7,200 ÷ $8,000) × 100 = 90%

- Impact: Severely negative—can drop scores 50-100 points

Optimal utilization targets:

- Under 10%: Excellent credit score impact

- 10-30%: Acceptable, minimal negative impact

- 30-50%: Moderate damage to credit score

- 50%+: Severe damage, signals financial distress

The math is straightforward: lower utilization percentages correlate with higher credit scores because they demonstrate you’re not dependent on credit to fund your lifestyle.

For a comprehensive breakdown of utilization mechanics, see our detailed credit utilization guide.

How Credit Limit Increases Impact Utilization

Increasing your credit limit while maintaining the same balance automatically lowers your utilization ratio, improving your credit score without changing spending behavior.

Example: Credit Limit Increase Scenario

Before the increase:

- Credit limit: $5,000

- Balance: $2,000

- Utilization: ($2,000 ÷ $5,000) × 100 = 40%

- Estimated credit score: 680

After $5,000 limit increase to $10,000:

- Credit limit: $10,000

- Balance: $2,000 (unchanged)

- Utilization: ($2,000 ÷ $10,000) × 100 = 20%

- Estimated credit score: 710-720

Result: 30-40 point score increase with zero behavioral change.

This mathematical relationship explains why strategic credit limit increases are powerful tools for credit optimization—but only if you resist the temptation to increase spending proportionally.

What Happens If Your Credit Limit Is Decreased

Credit limit decreases have the opposite effect: they spike your utilization ratio, potentially causing significant score damage.

Example: Credit Limit Decrease Scenario

Before decrease:

- Credit limit: $10,000

- Balance: $3,000

- Utilization: ($3,000 ÷ $10,000) × 100 = 30%

- Credit score: 720

After the lender reduces the limit to $5,000:

- Credit limit: $5,000

- Balance: $3,000 (unchanged)

- Utilization: ($3,000 ÷ $5,000) × 100 = 60%

- Credit score: 670-680

Result: 40-50 point score drop with zero behavioral change.

Why lenders decrease limits:

- Missed payments or late payments on any credit account

- Significant income reduction or job loss

- High utilization on other credit accounts (cross-default risk)

- Economic downturns (banks reduce overall credit exposure)

- Account inactivity (use-it-or-lose-it policies)

Mitigation strategy: If you receive notice of a limit decrease, immediately pay down balances to restore a healthy utilization ratio. Contact the lender to request reconsideration if you can demonstrate stable income and a responsible payment history.

Understanding your credit score mechanics helps you anticipate and respond to limit changes strategically.

How to Increase Your Credit Limit

Credit limit increases occur through two channels: automatic increases initiated by lenders and manual requests initiated by cardholders.

Automatic vs Manual Limit Increases

Automatic Increases:

Lenders periodically review accounts (typically every 6-12 months) and grant increases to customers who demonstrate:

- Consistent on-time payments (no late payments in the review period)

- Low utilization ratios (typically under 30%)

- Income growth or stable employment

- No new derogatory marks on credit reports

Automatic increases typically don’t trigger hard credit inquiries, preserving your credit score.

Manual Requests:

Cardholders can request limit increases through:

- Online account portal

- Phone calls to customer service

- Mobile banking apps

Manual requests may trigger hard inquiries (depending on issuer policy), which can temporarily reduce your credit score by 3-5 points. However, the utilization benefit usually outweighs the inquiry impact within 2-3 months.

What Lenders Check (Hard vs. Soft Inquiry)

Soft Inquiry (No Credit Score Impact):

- Internal account review using existing data

- Pre-qualification checks

- Automatic limit increase evaluations

- Some manual requests (issuer-dependent)

Hard Inquiry (Temporary Credit Score Impact):

- Formal credit applications

- Some manual limit increase requests

- New account openings

- Refinancing applications

Strategy: Before requesting a manual increase, ask the issuer whether they’ll perform a hard or soft inquiry. If it’s a hard inquiry, ensure the potential limit increase justifies the temporary score reduction.

Income Updates and Responsible Usage

Updating your income information can trigger automatic limit increases.

How to update income:

- Log in to your credit card account online

- Navigate to profile or account settings

- Update annual income with current figures

- Save changes

Lenders use this updated income to recalculate your debt-to-income ratio and credit capacity. If your income has increased since account opening, updating this information signals greater repayment ability.

Responsible usage patterns that trigger increases:

- Paying the statement balances in full each month

- Maintaining utilization below 30% (ideally below 10%)

- Regular card usage (not letting accounts sit dormant)

- No returned payments or NSF fees

- Tenure of 6+ months with current issuer

Best Practices for Approval

Timing your request:

- Wait at least 6 months after account opening

- Request increases after income raises or bonuses

- Avoid requests immediately after large purchases or balance spikes

- Don’t request during economic downturns or personal financial stress

Optimal request amounts:

- Request 10-25% increases for conservative approval odds

- Request a 50-100% increase if you have a strong payment history and income growth

- Avoid requesting specific dollar amounts that exceed realistic underwriting thresholds

Documentation preparation:

- Recent pay stubs or W-2s (if requested)

- Updated employment information

- Explanation for income increases (promotion, new job, side business)

What to avoid:

- Multiple requests within 6 months (signals desperation)

- Requesting increases while carrying high balances

- Requesting increases after missed payments

- Providing inaccurate income information (fraud risk)

Takeaway: Credit limit increases are mathematical tools for optimizing utilization ratios. Strategic timing and documentation maximize approval probability while minimizing credit score impact.

Pros and Cons of a Higher Credit Limit

Higher credit limits offer mathematical advantages but introduce behavioral risks. Understanding both sides enables informed decision-making.

| Pros of Higher Credit Limits | Cons of Higher Credit Limits |

|---|---|

| Lower utilization ratio: Automatically improves credit score if spending remains constant | Temptation to overspend: Higher limits can trigger lifestyle inflation and debt accumulation |

| Emergency financial cushion: Provides backup funding for unexpected expenses without high-interest loans | False sense of wealth: Available credit isn’t income—treating it as such creates debt spirals |

| Improved credit score: Lower utilization (30% weight in FICO) can increase scores 20-50+ points | Harder to recover from mistakes: Larger balances take longer to pay down and accrue more interest |

| Better rewards earning potential: More spending capacity on rewards cards maximizes cash back, points, or miles | Increased approval odds for other credit: Demonstrates lenders trust in you with larger amounts |

| Increased approval odds for other credit: Demonstrates lenders’ trust in you with larger amounts | Account closure risk: Unused high-limit accounts may be closed during economic downturns |

| Flexibility for large purchases: Enables big-ticket purchases without maxing out cards (preserving utilization) | Potential for hard inquiries: Manual limit requests may temporarily reduce credit score by 3-5 points |

When higher limits help:

- You maintain strict spending discipline regardless of available credit

- You pay your statement balances in full monthly

- You use credit strategically for rewards optimization

- You need emergency backup funding without accessing high-interest alternatives

- You’re actively building a credit score for major purchases (mortgage, auto loan)

When higher limits hurt:

- You struggle with impulse spending or lifestyle inflation

- You carry revolving balances month-to-month

- You view available credit as “extra money.”

- You lack emergency savings (credit shouldn’t replace compound interest accounts)

- You’re recovering from debt or bankruptcy

The mathematical benefit is clear: higher limits improve utilization ratios. The behavioral risk is equally clear: higher limits enable larger debt accumulation if discipline fails.

Insight: Credit limits are financial tools, not financial goals. The objective isn’t maximizing limits—it’s optimizing the utilization ratio while maintaining zero or minimal interest-bearing debt.

Real-World Examples

Theory becomes actionable through concrete scenarios. These examples demonstrate how credit limits function across different financial profiles.

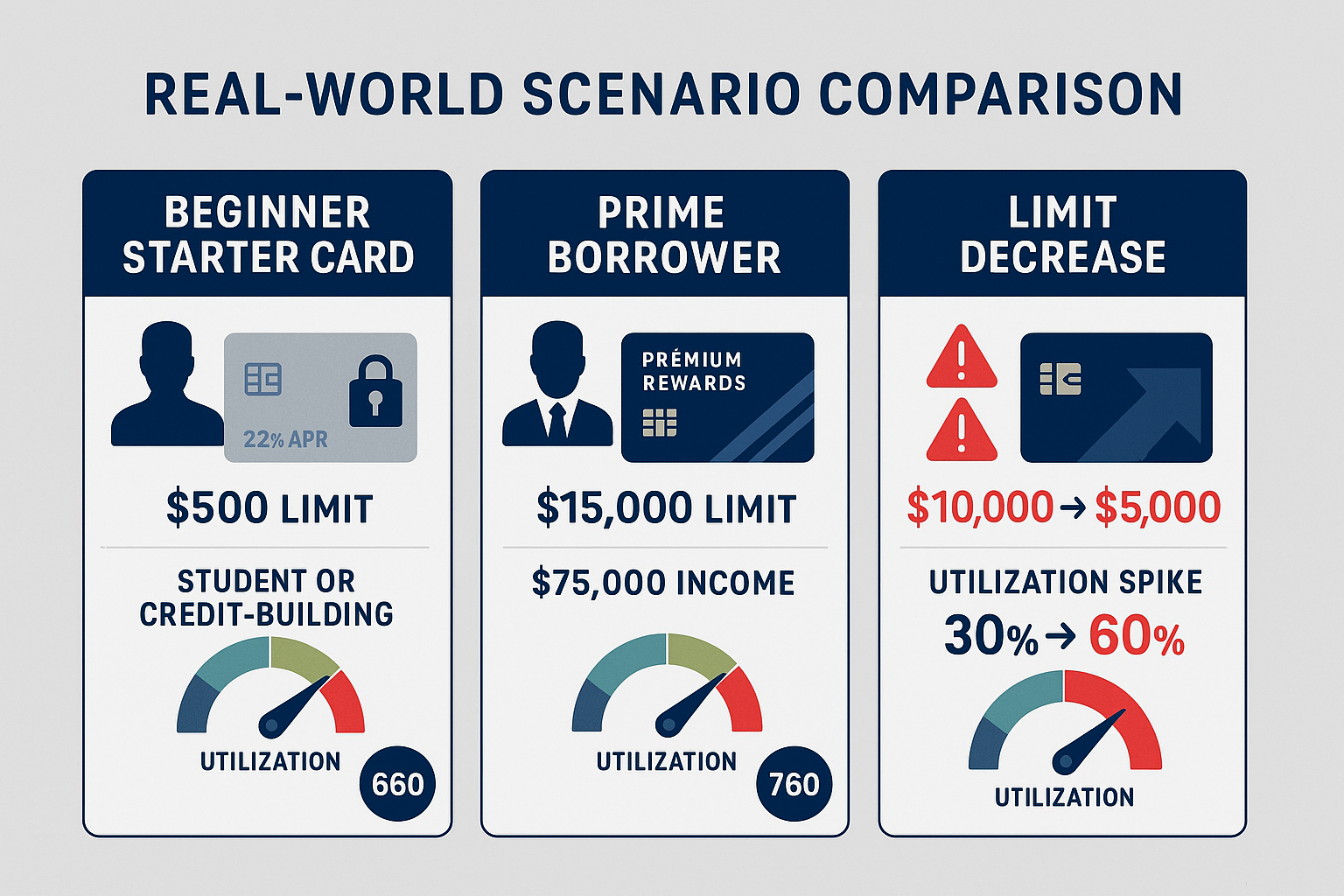

Example: $500 Starter Credit Limit

Profile:

- Credit score: 620 (fair)

- Age: 22, recent college graduate

- Income: $35,000/year

- Credit history: 6 months (one secured credit card)

- Debt: $8,000 student loans

Credit card approval:

- Card type: Secured credit card (requires $500 deposit)

- Credit limit: $500

- APR: 24.99%

- Annual fee: $0

Utilization management:

- Monthly spending: $150 (gas, groceries)

- Statement balance: $150

- Utilization: ($150 ÷ $500) × 100 = 30%

- Strategy: Pay in full monthly to avoid interest

12-month outcome:

- Consistent on-time payments establish a positive payment history

- Credit score increases to 670-680

- Issuer automatically increases limit to $1,000 after 8 months

- New utilization with same spending: ($150 ÷ $1,000) × 100 = 15%

- Credit score reaches 690-700

Lesson: Low initial limits require disciplined spending to maintain healthy utilization. Consistent payments trigger automatic increases, creating a positive feedback loop.

Example: $15,000 Prime Borrower Credit Limit

Profile:

- Credit score: 760 (very good)

- Age: 35, established professional

- Income: $95,000/year

- Credit history: 12 years (multiple cards, auto loan, mortgage)

- Debt: $280,000 mortgage, $12,000 auto loan

- DTI: 32%

Credit card approval:

- Card type: Premium rewards card

- Credit limit: $15,000

- APR: 16.99% (variable)

- Annual fee: $95

Utilization management:

- Monthly spending: $2,500 (all expenses for rewards optimization)

- Statement balance: $2,500 (paid in full)

- Utilization: ($2,500 ÷ $15,000) × 100 = 16.7%

- Strategy: Maximize rewards while maintaining low utilization

Additional cards:

- Card 2: $10,000 limit, $500 balance

- Card 3: $8,000 limit, $0 balance

- Total limits: $33,000

- Total balances: $3,000

- Overall utilization: ($3,000 ÷ $33,000) × 100 = 9.1%

24-month outcome:

- Credit score remains stable at 760-780

- Earns $800/year in rewards (2% cash back on $40,000 annual spend)

- Issuer increases limit to $20,000 after 18 months

- New utilization: ($3,000 ÷ $38,000) × 100 = 7.9%

Lesson: High credit limits combined with disciplined spending create optimal utilization ratios while maximizing rewards. Multiple cards with low individual utilization improve the overall credit profile.

This scenario aligns with principles of delayed gratification, using credit strategically rather than impulsively.

Example: When Your Limit Drops

Profile:

- Credit score: 710 (good)

- Age: 42, small business owner

- Income: $68,000/year (variable)

- Credit history: 18 years

- Debt: $15,000 business line of credit, $5,000 credit card balance

Initial situation:

- Card 1: $12,000 limit, $3,000 balance (25% utilization)

- Card 2: $8,000 limit, $2,000 balance (25% utilization)

- Total: $20,000 limits, $5,000 balances (25% overall utilization)

- Credit score: 710

Triggering event:

- Economic downturn in 2025

- Business revenue declines 30%

- Misses one credit card payment (30 days late)

- Payment history now shows a derogatory mark

Lender response:

- Card 1 limit reduced from $12,000 to $6,000

- Card 2 limit reduced from $8,000 to $5,000

- Total limits now: $11,000

- Balances unchanged: $5,000

- New utilization: ($5,000 ÷ $11,000) × 100 = 45.5%

Credit score impact:

- Late payment: -60 to -80 points

- Utilization spike: -20 to -30 points

- New credit score: 610-630

Recovery strategy:

- Immediately pay down balances: Reduce total balances to $2,200 (20% utilization)

- Contact lenders: Request reconsideration based on payment history (one-time mistake)

- Document income stability: Provide recent bank statements showing recovered revenue

- Establish payment plan: Set up automatic payments to prevent future late payments

- Monitor credit reports: Dispute any inaccurate information

6-month outcome:

- Balances reduced to $1,500

- Utilization: ($1,500 ÷ $11,000) × 100 = 13.6%

- No additional late payments

- Credit score recovers to 660-670

- One lender restores partial limit ($8,000 on Card 1)

Lesson: Credit limit decreases compound the damage from payment mistakes. Immediate action to reduce balances and restore payment consistency mitigates long-term impact. Prevention through budgeting frameworks and emergency funds is far more effective than recovery.

💳 Credit Utilization Calculator

Calculate your credit utilization ratio and its impact on your credit score

📊 Your Credit Utilization Analysis

Conclusion

Credit limits are not arbitrary numbers—they're mathematical tools that directly influence your credit score, borrowing capacity, and financial flexibility.

The formula is simple: (Total Balances ÷ Total Credit Limits) × 100 = Utilization Ratio. This ratio accounts for 30% of your FICO score, making it the second-most important factor after payment history.

Understanding how lenders determine credit limits—through credit scores, income verification, debt-to-income ratios, and proprietary risk models—enables you to optimize your credit profile strategically. Higher limits improve utilization ratios automatically, but only if spending discipline remains constant.

Actionable next steps:

- Calculate your current utilization ratio across all credit cards using the formula above

- Pay down balances to achieve utilization below 30% (ideally below 10%)

- Request credit limit increases on cards with good payment history (after 6+ months)

- Update income information with card issuers to trigger automatic limit reviews

- Monitor credit reports quarterly to verify accurate limit reporting and catch unauthorized changes

- Maintain active card usage with small recurring charges to prevent account closures

- Avoid closing old, high-limit cards that improve your overall utilization ratio

Credit limits represent lender trust expressed in mathematical terms. By managing utilization strategically, maintaining consistent payment history, and documenting income growth, you transform credit limits from constraints into wealth-building tools.

The math behind money reveals that credit optimization isn't about maximizing limits—it's about minimizing utilization while maintaining access to emergency liquidity. Master this balance, and your credit score becomes a compound growth engine for lower interest rates, better loan terms, and accelerated wealth building.

For comprehensive credit management strategies, explore our guides on credit utilization, credit scoring mechanics, and evidence-based budgeting frameworks.

References

[1] FICO. (2025). "Understanding FICO Scores." myFICO.com. https://www.myfico.com/credit-education/credit-scores

[2] Experian. (2025). "What Is a Good Credit Limit?" Experian.com. https://www.experian.com/blogs/ask-experian/what-is-a-good-credit-limit/

[3] Consumer Financial Protection Bureau. (2025). "What is a credit utilization rate or ratio?" ConsumerFinance.gov. https://www.consumerfinance.gov/ask-cfpb/what-is-a-credit-utilization-rate-en-1795/

[4] Federal Reserve. (2025). "Consumer Credit - G.19." FederalReserve.gov. https://www.federalreserve.gov/releases/g19/current/

[5] Equifax. (2025). "How Credit Limits Are Determined." Equifax.com. https://www.equifax.com/personal/education/credit/score/how-credit-limits-are-determined/

[6] TransUnion. (2025). "Credit Utilization and Your Credit Score." TransUnion.com. https://www.transunion.com/credit-utilization

Disclaimer

Educational Content Only: This article provides educational information about credit limits and credit scoring mechanics. It is not financial advice, credit counseling, or a recommendation to apply for specific credit products.

Individual Circumstances Vary: Credit limit determinations, credit score impacts, and optimal utilization strategies depend on individual financial situations, credit histories, and lender-specific underwriting criteria. The examples provided are illustrative and may not reflect your specific outcomes.

No Guarantee of Results: Following the strategies outlined in this article does not guarantee credit limit increases, credit score improvements, or loan approvals. Credit decisions remain at the lender's discretion based on a comprehensive risk assessment.

Consult Professionals: For personalized credit advice, debt management strategies, or financial planning, consult licensed credit counselors, certified financial planners, or qualified financial advisors who can evaluate your specific circumstances.

Data Accuracy: While this article references authoritative sources, including FICO, Experian, and the Consumer Financial Protection Bureau, credit industry practices and scoring models evolve. Verify current information with official sources before making financial decisions.

Risk Acknowledgment: Credit products involve financial risk. Mismanagement of credit limits can result in debt accumulation, interest charges, credit score damage, and long-term financial harm. Use credit responsibly and within your repayment capacity.

The Rich Guy Math provides data-driven financial education to build financial literacy and evidence-based decision-making. All content reflects research and analysis current as of 2025.

About the Author

Max Fonji is the founder of The Rich Guy Math, a data-driven financial education platform that explains the math behind money, wealth building, and evidence-based investing.

With a background in financial analysis and a commitment to teaching financial literacy through numbers and logic, Max translates complex financial concepts into clear, actionable frameworks. His work focuses on helping beginners and intermediate learners understand how credit, investing, and risk management truly work through data, formulas, and cause-and-effect relationships.

Max's educational approach combines analytical precision with approachable teaching, demonstrating that financial success follows mathematical principles, not luck or speculation. The Rich Guy Math serves readers seeking to build wealth through compound growth, valuation principles, and disciplined financial decision-making.

Connect with The Rich Guy Math:

- Website: https://therichguymath.com

- Educational Focus: Credit optimization, compound interest, dividend investing, valuation analysis, and evidence-based wealth building

The Rich Guy Math: Where financial literacy meets mathematical precision.

Frequently Asked Questions

Does requesting a credit limit increase hurt my credit score?

It depends on the type of inquiry the lender performs. Soft inquiries (used by many issuers for existing customers) don't affect your credit score. Hard inquiries may reduce your score by 3–5 points temporarily, but the utilization benefit typically outweighs this impact within 2–3 months.

Before requesting an increase, ask your issuer whether they'll perform a hard or soft pull. Many issuers now use soft inquiries for existing customers with good payment history.

What's the ideal credit utilization ratio?

Under 10% is optimal for maximizing credit scores. Utilization between 10–30% is acceptable with minimal negative impact. Above 30%, credit scores begin declining noticeably. Above 50%, scores drop significantly.

The formula is straightforward: (Total Balances ÷ Total Limits) × 100. Keep this percentage as low as possible while maintaining active card usage (complete inactivity can trigger account closures).

Can I have too high of a credit limit?

From a credit score perspective, no—higher limits improve utilization ratios. From a behavioral perspective, yes—if high limits trigger overspending or debt accumulation.

The risk is psychological, not mathematical. If you treat available credit as income or struggle with impulse spending, high limits enable larger mistakes. If you maintain spending discipline regardless of limits, higher is always better for credit scoring purposes.

How often should I request credit limit increases?

Wait at least 6 months between requests to the same issuer. More frequent requests signal financial distress and typically result in denials.

Optimal timing:

- After income increases (raise, promotion, new job)

- After 6–12 months of perfect payment history

- When utilization exceeds 30% despite responsible spending

- Before applying for major loans (mortgage, auto) to optimize credit score

Do credit limit increases trigger automatic spending increases?

They shouldn't, but behavioral economics research shows they often do—a phenomenon called “mental accounting” or “lifestyle inflation.”

Prevention strategies:

- Maintain fixed monthly budgets regardless of available credit

- Track spending in absolute dollars, not percentages of limits

- Use credit for planned purchases only, not impulse buys

- Implement the 50/30/20 budgeting rule

- Pay balances in full monthly to avoid interest charges

What happens to my credit score if I close a high-limit credit card?

Closing a card reduces your total available credit, which increases your utilization ratio if you carry balances on other cards.

Example:

Before closure: $30,000 total limits, $3,000 balances = 10% utilization

After closing a $10,000 limit card: $20,000 total limits, $3,000 balances = 15% utilization

This can cause a 10–20 point score drop.

Closing old accounts also reduces your average credit age, which is 15% of your FICO score.

Strategy: Keep old, high-limit cards open even if unused. Put small recurring charges on them and enable autopay.

Can lenders reduce my credit limit without warning?

Yes, but they must provide notice—typically 45 days—before the reduction takes effect under the Credit CARD Act of 2009. However, the decision often occurs before you receive the notice.

Common triggers:

- Late or missed payments

- High utilization on other accounts

- Income reduction or job loss

- Economic downturns

- Extended account inactivity

Protection strategy: Maintain low utilization, make on-time payments, use cards regularly, and update income information when it increases.

How do credit limits affect mortgage approval?

Mortgage lenders calculate your debt-to-income ratio (DTI) using your minimum required payments, not your credit limits. However, high available credit can be viewed as potential future debt.

Impact on approval:

- Low utilization (under 30%) signals responsible credit management

- High total available credit with zero balances is neutral to positive

- High utilization (over 50%) signals financial stress

- Recent credit limit increases may require explanation letters

Strategy: Before applying for a mortgage, reduce utilization to under 10% and avoid requesting new credit for 6 months.

Related posts:

Credit Utilization Ratio Explained: What It Is, How It Works, And How To Improve It

Credit Utilization Ratio Explained: What It Is, How It Works, And How To Improve It

How Long Do Late Payments Stay on Credit Report? The Complete 7-Year Timeline Explained

How Long Do Late Payments Stay on Credit Report? The Complete 7-Year Timeline Explained

Statement Balance vs Current Balance: Which One Should You to Pay

Statement Balance vs Current Balance: Which One Should You to Pay

Current Balance vs Available Balance: What’s the Difference?

Current Balance vs Available Balance: What’s the Difference?

Credit Card APR Explained: What It Is And How Interest Really Works

Credit Card APR Explained: What It Is And How Interest Really Works

How Long Does It Take to Build Credit? Real Timeline Explained

How Long Does It Take to Build Credit? Real Timeline Explained