Current balance is the total amount of money in your account right now, including all posted transactions such as deposits, withdrawals, purchases, and payments. It reflects your most up-to-date account activity but may still include pending charges that haven’t fully settled, which means it can differ from your available balance.

This article is part of our complete Credit Cards Guide, where we break down APRs, interest, rewards, fees, and how to use credit cards the smart way.

Understanding your What Is Current Balance? Understanding Credit Cards & Bank Accounts Explained isn’t just about knowing how much money you have; it’s about avoiding overdraft fees, managing credit card debt strategically, and making informed financial decisions that protect your wealth. The math behind balance calculations directly impacts your spending power, credit utilization, and ultimately, your financial health.

This guide breaks down everything you need to know about current balance in both bank accounts and credit cards, using clear definitions, real-world examples, and data-driven insights that empower you to take control of your finances.

Key Takeaways

- Current balance represents the total amount in your account or owed on your credit card at the exact moment you check, updating in real-time as transactions post

- Current balance differs from available balance (what you can actually spend) and statement balance (what you owed at the end of your last billing cycle)

- Pending transactions reduce available funds but may not immediately appear in your current balance, creating a gap that causes overdrafts and declined purchases

- Paying your current balance on credit cards eliminates all debt, including recent charges, while paying only the statement balance leaves new purchases subject to interest

- Understanding balance types prevents costly mistakes: the average overdraft fee in 2025 is $35, and credit card interest averages 21.47% APR on unpaid current balances

Current Balance Definition

Current balance is the total amount of money in your bank account or the total amount you owe on your credit card at the precise moment you check your account. It represents the most up-to-date snapshot of your financial position, incorporating all transactions that have been processed and posted to your account.

For bank accounts (checking or savings), your current balance shows:

- All deposits that have cleared

- All withdrawals and purchases that have been posted

- Any fees charged by your financial institution

- Interest earned (if applicable)

For credit cards, your current balance displays:

- All purchases that have been posted to your account

- Any payments you’ve made

- Interest charges assessed

- Credits from returns or refunds

The current balance is dynamic; it changes throughout the day as your bank or credit card issuer processes new transactions. This real-time nature makes it different from other balance types you’ll encounter in your financial accounts.

How Your Current Balance Updates in Real Time

Your current balance updates automatically as transactions move from “pending” to “posted” status. Here’s the typical timeline:

Transaction Processing Flow:

- Authorization (instant): When you swipe your card, the merchant requests authorization from your bank or card issuer

- Pending (0-3 days): The transaction appears as pending, but may not reduce your current balance yet (depends on your institution)

- Posted (1-5 days): The transaction fully processes and officially updates your current balance

- Settlement (complete): The money has been transferred between accounts

Different financial institutions handle pending transactions differently. Some banks immediately subtract pending transactions from your current balance, while others only reflect posted transactions. This inconsistency creates confusion and potential overdraft scenarios.

According to Federal Reserve data, the average transaction takes 1-3 business days to post completely, though same-day ACH transfers and real-time payment networks are accelerating this timeline in 2025.

Pending vs Posted Transactions

The distinction between pending and posted transactions is critical for understanding your true current balance:

Pending Transactions:

- Authorized but not yet finalized

- May or may not appear in your current balance (institution-dependent)

- Always reduce your available balance

- Can be canceled or adjusted before posting

- Typical examples: restaurant tips, gas station holds, hotel reservations

Posted Transactions:

- Fully processed and finalized

- Always included in your current balance

- Cannot be reversed without a formal dispute or refund

- Permanent record on your account statement

Real-world scenario: You have a $1,000 current balance. You buy groceries for $150 on Monday morning. Your bank might show:

- Current balance: $1,000 (if pending transactions aren’t included)

- Available balance: $850 (always reflects pending transactions)

- Posted balance: $1,000 (until the transaction clears)

By Wednesday, when the transaction posts:

- Current balance: $850

- Available balance: $850

- Posted balance: $850

This lag creates the illusion of having more money than you actually control, a dangerous trap that leads to overdrafts.

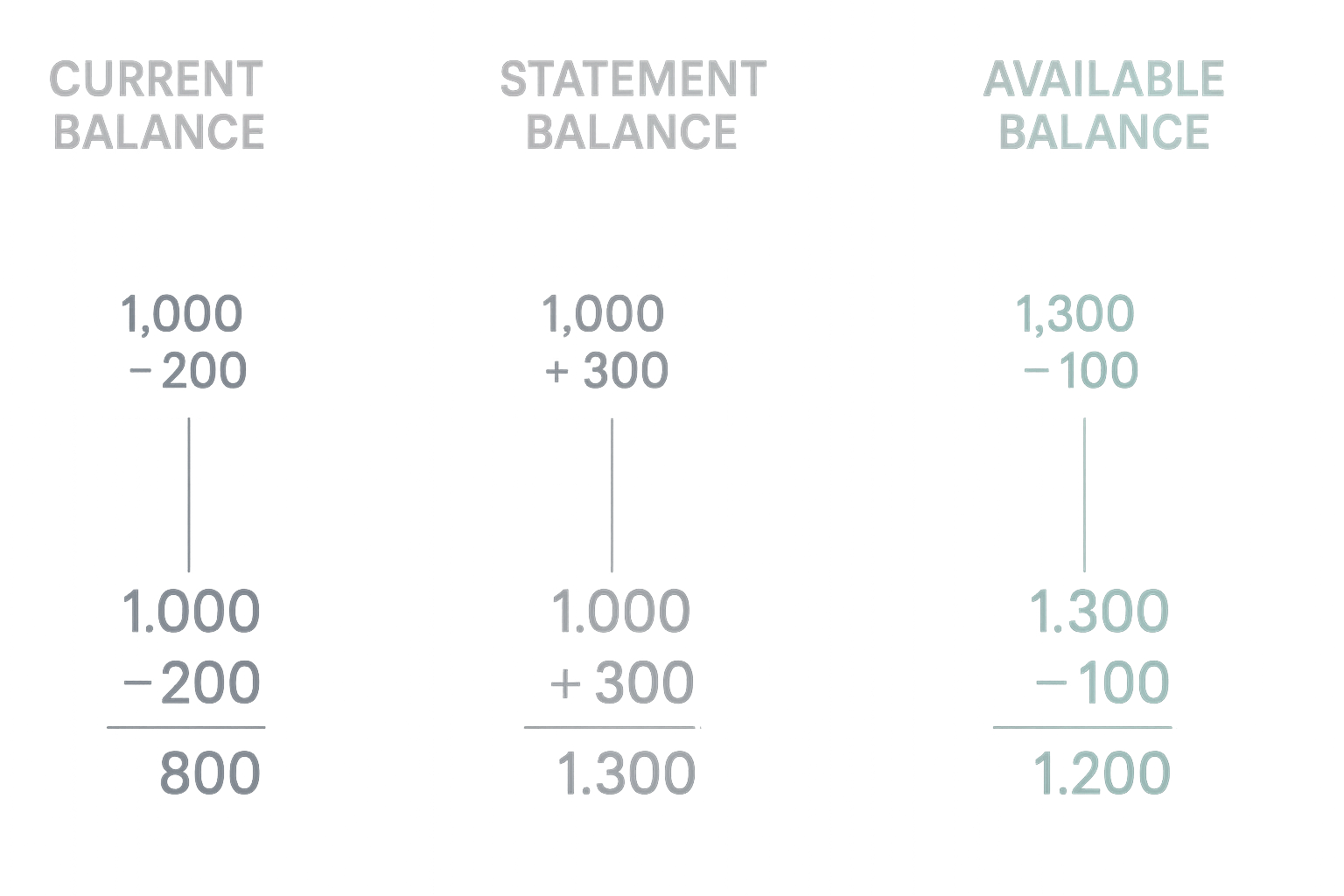

Current Balance vs Statement Balance vs Available Balance

Understanding the three primary balance types prevents costly financial mistakes. Each serves a distinct purpose and updates on different schedules.

Side-by-Side Comparison Table

| Balance Type | What It Shows | Update Frequency | Best Used For | Includes Pending? |

|---|---|---|---|---|

| Current Balance | Total in account or owed right now | Real-time (as transactions post) | Knowing the minimum payment to avoid interest | Sometimes (varies by bank) |

| Statement Balance | Amount owed at the end of the last billing cycle | Monthly (fixed until next statement) | No (only posted transactions before the closing date) | Amount owed at end of the last billing cycle |

| Available Balance | Actual funds you can spend/withdraw | Real-time (including all holds) | Making purchases without overdrafts | Yes (always includes pending) |

Why the Differences Matter

Each balance type serves a specific financial management purpose:

The Current Balance indicates your overall position, but doesn’t account for checks you’ve written that haven’t cleared or automatic payments scheduled for tomorrow. Relying solely on the current balance leads to overspending.

Statement Balance determines whether you’ll pay interest on credit cards. Paying the full statement balance by the due date triggers the grace period, meaning you pay zero interest on purchases made during that billing cycle. The statement balance remains fixed; it’s your target payment amount for interest-free credit card use.

Available Balance represents your true spending power. This is the number that matters when deciding whether you can afford a purchase today. Available balance accounts for:

- Pending debit card transactions

- Outstanding checks

- Scheduled automatic payments

- Merchant holds (gas stations often hold $75-$125, hotels may hold an estimated total plus 15-20%)

- ATM withdrawal limits

Critical insight: A 2024 Consumer Financial Protection Bureau study found that 23% of overdraft fees occur when consumers check their current balance but ignore their available balance, assuming they have more spendable funds than actually accessible.

For effective budget management, always reference your available balance before making purchases, but monitor your current balance to understand your overall financial trajectory.

How Interest Is Calculated Using Your Current Balance

Credit card companies use your current balance (specifically, your average daily balance) to calculate interest charges, a mathematical reality that costs Americans over $120 billion annually in credit card interest.

Daily Periodic Rate Formula

Credit card interest isn’t calculated monthly; it compounds daily. Here’s the math:

Step 1: Calculate Daily Periodic Rate (DPR)

Daily Periodic Rate = Annual Percentage Rate (APR) ÷ 365 days

Example: 21.47% APR ÷ 365 = 0.0588% per dayStep 2: Calculate Average Daily Balance

Your card issuer tracks your current balance every single day of the billing cycle, then calculates the average:

Average Daily Balance = Sum of daily balances ÷ Number of days in billing cycleStep 3: Calculate Interest Charge

Interest Charge = Average Daily Balance × Daily Periodic Rate × Days in billing cycleExample: How $1,200 Current Balance Generates Interest

Let’s walk through a realistic scenario:

Your situation:

- Credit card APR: 21.47%

- Billing cycle: 30 days

- Starting current balance: $1,200

- No new purchases or payments during the cycle

The calculation:

- Daily Periodic Rate: 21.47% ÷ 365 = 0.0588% per day

- Average Daily Balance: $1,200 (constant throughout the month)

- Interest Charge: $1,200 × 0.0588% × 30 days = $21.17

Your current balance at the end of the billing cycle becomes $1,221.17, and next month’s interest will be calculated on this higher amount. This is compound interest working against you.

More complex scenario: What if you made a $500 payment on day 15?

- Days 1-14: Current balance = $1,200 (14 days × $1,200 = $16,800)

- Days 15-30: Current balance = $700 (16 days × $700 = $11,200)

- Total balance-days: $16,800 + $11,200 = $28,000

- Average Daily Balance: $28,000 ÷ 30 days = $933.33

- Interest Charge: $933.33 × 0.0588% × 30 = $16.47

By making a mid-cycle payment, you reduced your interest charge by $4.70 ($21.17 – $16.47). This demonstrates why paying down your current balance as quickly as possible, even before the due date, saves money through the power of daily compounding.

Understanding APY vs APR helps clarify why credit card interest accumulates faster than many borrowers expect.

Grace Period and When Interest Starts

The grace period is your interest-free window—typically 21-25 days between your statement closing date and payment due date. Here’s the critical rule:

If you pay your full statement balance by the due date, you will not incur interest charges on purchases made during that billing cycle. Your current balance might be higher than your statement balance (due to new purchases), but you won’t pay interest on the statement amount.

If you pay less than the full statement balance, Interest begins accruing immediately on your entire current balance, calculated from each transaction’s posting date. There is no grace period on the remaining balance.

Cash advances and balance transfers: These transactions typically have no grace period; interest starts accruing from day one, regardless of payment behavior.

Example timeline:

- March 1-31: Billing cycle (you make $2,000 in purchases)

- March 31: Statement closes with $2,000 statement balance

- April 1-10: You make $500 in new purchases (current balance now $2,500)

- April 25: Payment due date

Scenario A: You pay $2,000 (full statement balance) → Zero interest on the $2,000, grace period preserved for next cycle

Scenario B: You pay $1,500 (partial payment) → Interest charges on the entire $2,000 from each purchase date, no grace period next month

This mathematical reality makes paying your full statement balance, not just the minimum payment, essential for avoiding the compound interest trap.

How Your Current Balance Affects Credit Score

Your credit card current balance directly impacts 30% of your FICO credit score through a metric called credit utilization ratio, making it the second-most important factor after payment history.

Credit Utilization Impact

Credit utilization measures how much of your available credit you’re currently using:

Credit Utilization Ratio = (Total Current Balances ÷ Total Credit Limits) × 100Example:

- Credit Card A: $1,500 current balance, $5,000 limit

- Credit Card B: $800 current balance, $3,000 limit

- Total current balances: $2,300

- Total credit limits: $8,000

- Utilization ratio: ($2,300 ÷ $8,000) × 100 = 28.75%

Optimal utilization targets:

- Under 10%: Excellent (maximizes credit score)

- 10-30%: Good (minimal score impact)

- 30-50%: Fair (begins lowering score)

- 50-70%: Poor (significant score reduction)

- Over 70%: Very poor (major score damage)

Credit scoring models evaluate utilization both per-card and across all accounts. Maxing out even one card while keeping others at zero utilization still damages your score because the individual card shows 100% usage.

Data-driven insight: Experian research shows that consumers with credit scores above 800 maintain an average utilization ratio of just 7%, while those with scores below 600 average 75% utilization.

Reducing your current balance by even $500 can boost your score by 20-40 points if it moves you from above 30% utilization to below. This mathematical relationship between current balance and credit score makes strategic balance management a powerful wealth-building tool.

When Balances Are Reported to Bureaus

Here’s a critical detail most consumers miss: Credit card issuers don’t report your current balance to credit bureaus daily; they report once per month, typically on your statement closing date.

The reporting timeline:

- Throughout the month, your current balance fluctuates daily

- On your statement closing date (e.g., the 15th of each month), your issuer captures your current balance

- That balance gets reported to Equifax, Experian, and TransUnion within 30 days

- Credit scoring models use the reported balance to calculate your utilization ratio

Strategic implication: You could carry a $5,000 current balance for 29 days, pay it down to $500 on day 30 (your statement closing date), and the credit bureaus would only see the $500 balance. Your utilization ratio reflects the lower number.

Tactical approach for score optimization:

- Identify your statement closing date (different from payment due date)

- Make a large payment 2-3 days before the closing date

- This ensures the lower current balance gets reported

- Your credit score reflects the optimized utilization ratio within 30-60 days

This strategy is particularly powerful before applying for a mortgage, auto loan, or new credit card, where even a 20-point score increase can mean better interest rates and thousands in savings.

Understanding credit utilization and available credit mechanics provides the mathematical foundation for strategic credit management.

Common Scenarios (Real-World Examples)

Current balance calculations become clearer through practical examples that mirror everyday financial situations.

Refunds

Scenario: You return a $200 jacket to a retailer on Monday. When does your current balance reflect the refund?

Timeline:

- Day 1 (Monday): You process the return in-store; the merchant initiates the refund

- Day 2-3: Refund shows as “pending credit” in your account (may or may not increase your current balance yet)

- Day 4-7: Refund posts to your account; current balance increases by $200

Banking variation: Some institutions immediately add pending credits to your current balance, while others wait until posting. This inconsistency means your current balance might show $1,000 on Day 2 at Bank A but $1,200 at Bank B, even though the same refund is processing.

Credit card refunds: When you return a purchase made on credit, the refund reduces your current balance (the amount you owe). If your current balance is $1,500 and you receive a $200 refund, your new current balance becomes $1,300. However, if you’ve already paid off that purchase, the refund creates a negative balance (credit), which you can either use for future purchases or request as a cash refund.

Tips at Restaurants

Scenario: You have dinner at a restaurant with a $50 bill and leave a $10 tip. How does this affect your current balance?

Transaction flow:

- Initial authorization (at the table): Restaurant charges $50 to verify funds

- Current balance: May decrease by $50 (institution-dependent)

- Available balance: Decreases by $50

- Tip adjustment (hours later): Server adds your $10 tip to the transaction

- Current balance: Remains at $50 reduction until posting

- Final posting (1-3 days later): Full $60 transaction posts

- Current balance: Decreases by $60 total

- Available balance: Already reflected $50; now shows an additional $10 reduction

The confusion: Between the time you leave the restaurant and the transaction posts, your current balance might only show a $50 reduction while your available balance shows $60 less. This $10 discrepancy represents the pending tip adjustment.

Financial impact: If you’re managing a tight budget, these delayed tip postings can accumulate. Five restaurant visits with $10 tips each mean $50 in “hidden” pending charges not yet reflected in your current balance, enough to trigger an overdraft if you’re not tracking available balance.

Travel Holds

Scenario: You rent a car for $300 and book a hotel for $600. Your current balance shows $2,000 before the trip.

What actually happens:

Car rental hold:

- Rental company authorizes $300 (rental cost) + $200 (security hold) = $500 total hold

- Current balance: May show $2,000 or $1,500 (varies by bank)

- Available balance: $1,500 (hold always reduces available funds)

Hotel hold:

- Hotel authorizes $600 (room cost) + $120 (20% incidental hold) = $720 total hold

- Current balance: May show $2,000, $1,500, or $780 (institution-dependent)

- Available balance: $780

Total holds: $1,220 ($500 + $720), even though your actual expenses are only $900

When holding release:

- Car rental: 3-7 days after vehicle return

- Hotel: 3-10 days after checkout

- Final posted charges: Only the actual $900 spent

During the hold period: Your current balance might show $2,000 (if your bank doesn’t reflect pending holds), but your available balance shows $780. If you rely on current balance for spending decisions, you might attempt a $1,000 purchase and face a declined transaction—or worse, an overdraft if the purchase is processed.

Pro tip: Always check available balance before travel-related purchases, and budget an extra 20-30% cushion for merchant holds that temporarily reduce spending power.

These scenarios illustrate why monitoring both current balance and available balance is essential for accurate financial management and avoiding costly surprises.

Should You Pay Your Current Balance or Statement Balance?

This question determines whether you pay interest on credit card debt, a decision with significant long-term financial consequences.

The Mathematical Reality

Paying statement balance:

- Eliminates all debt from the previous billing cycle

- Preserves your grace period for the next cycle

- Results in zero interest charges on those purchases

- Leaves any new purchases (made after the statement closing date) on your current balance

Paying current balance:

- Eliminates all debt, including recent charges

- Guarantees zero interest on everything

- Resets your current balance to $0

- Provides maximum credit score benefit (0% utilization when reported)

Paying minimum payment:

- Keeps account in good standing (avoids late fees)

- Triggers immediate interest charges on the entire balance

- Costs hundreds or thousands in compound interest over time

- Damages credit score through high utilization

Real-World Comparison

Scenario: Your credit card has a 21.47% APR.

- Statement balance (March 31): $2,000

- New purchases (April 1-24): $500

- Current balance (April 24): $2,500

- Minimum payment: $50

- Payment due date: April 25

Option A: Pay $2,000 (statement balance)

- Interest on March purchases: $0 (grace period preserved)

- Interest on April purchases: $0 (new grace period starts)

- Remaining current balance: $500

- Next month’s interest if unpaid: ~$8.92

Option B: Pay $2,500 (current balance)

- Interest on all purchases: $0

- Remaining current balance: $0

- Credit utilization: 0% (when reported)

- Total cost: $0 in interest

Option C: Pay $50 (minimum payment)

- Interest on $2,000 from March: ~$35.30 (calculated from purchase dates)

- Interest on $500 from April: ~$8.92

- Total interest this month: ~$44.22

- Remaining current balance: $2,494.22 ($2,500 – $50 + $44.22)

- Next month’s interest: Even higher, compounding on $2,494.22

Over 12 months (assuming no new purchases):

- Paying statement balance: $0 in interest

- Paying current balance: $0 in interest

- Paying minimum only: $487+ in interest, taking 6+ years to pay off

The math is unambiguous: Paying at least your full statement balance is essential for avoiding the compound interest trap. Paying your current balance provides additional benefits through improved credit utilization and complete debt elimination.

For those managing multiple debts, understanding debt-to-equity ratio and debt ratio concepts helps prioritize payments strategically.

How to Manage Your Current Balance Like a Pro

Strategic current balance management combines mathematical precision with behavioral discipline, skills that separate wealth builders from perpetual debtors.

Payment Timing Strategies

1. Pay before the statement closing date

Making payments before your statement closes reduces the balance that gets reported to credit bureaus, optimizing your credit utilization ratio.

Example:

- Statement closes: 15th of each month

- Payment due: 10th of the following month

- Strategic payment date: 13th-14th (before closing)

Benefit: A $3,000 current balance paid down to $300 before the 15th results in only $300 being reported to credit bureaus, showing 10% utilization instead of 100% on a $3,000 limit.

2. Make multiple payments per month

Instead of one large payment on the due date, make weekly or bi-weekly payments to continuously reduce your average daily balance.

Mathematical impact:

- Single $1,200 payment on day 25: Average daily balance = $1,200 for 25 days, $0 for 5 days

- Four $300 payments (days 7, 14, 21, 28): Average daily balance significantly lower

Interest savings: The second approach reduces your average daily balance by approximately 40-50%, cutting interest charges proportionally.

3. Align payments with income

Match payment timing to your paycheck schedule:

- Get paid bi-weekly? Make credit card payments bi-weekly

- Receive monthly income? Pay statement balance immediately after payday

This behavioral alignment prevents the “I’ll pay it later” trap that leads to missed payments and interest charges.

Increasing Credit Score Through Balance Management

Tactical approaches:

1. Keep the current balance under 10% of the credit limit

The 10% threshold triggers optimal credit scoring algorithms. On a $5,000 limit, maintain a current balance below $500 when your statement closes.

Implementation:

- Set up balance alerts at 8% utilization

- Make payments when you hit the threshold

- Request credit limit increases to improve the ratio (if you can avoid increased spending)

2. Use multiple cards strategically

Distribute purchases across cards to keep individual utilization low:

- Card A ($10,000 limit): $500 balance = 5% utilization

- Card B ($5,000 limit): $250 balance = 5% utilization

- Total: $750 across $15,000 = 5% overall utilization

This beats carrying a $750 balance on a single $1,500 limit card (50% utilization).

3. Request higher credit limits

A credit limit increase from $5,000 to $10,000 instantly cuts your utilization ratio in half (assuming the same current balance).

Caution: Only effective if you don’t increase spending. The goal is a better ratio of mathematics, not more debt capacity.

Avoiding Interest Traps

Common traps and solutions:

Trap 1: “I’ll pay it off next month.”

Procrastination costs compound interest. A $1,000 balance at 21.47% APR costs $17.89 in interest the first month, then $18.21 the next month (compounding on $1,017.89).

Solution: Treat credit cards as debit cards, only charge what you can pay immediately. Implement the 50/30/20 rule budgeting framework to ensure sufficient cash flow for full payment.

Trap 2: Paying only the minimum

Minimum payments (typically 2-3% the current balance) barely cover interest charges, extending repayment to decades.

Example: $5,000 balance at 21.47% APR

- Minimum payment: $100/month

- Time to pay off: 7.5 years

- Total interest paid: $4,311

- Total cost: $9,311 for $5,000 in purchases

Solution: Always pay at least 3-4× the minimum, or better yet, the full statement balance.

Trap 3: Ignoring the statement closing date

Making a large purchase the day before your statement closes results in high reported utilization, even if you pay it off before the due date.

Solution: Time large purchases for immediately after your statement closes, giving you 30 days to pay before the next reporting date.

Trap 4: Confusing current balance with available balance

Spending based on the current balance without accounting for pending transactions leads to overdrafts.

Solution: Always reference the available balance for spending decisions. Set up low-balance alerts at $200-500 above zero.

Automation and Tracking Tools

1. Set up automatic payments

Configure autopay for at least the minimum payment to avoid late fees, but manually pay the full statement balance for interest avoidance.

2. Use mobile banking apps

Modern banking apps display real-time current balance, available balance, and pending transactions in one view. Enable push notifications for:

- Transactions over $X amount

- Balance drops below threshold

- Payment due date reminders

- Unusual activity alerts

3. Leverage budgeting software

Tools like Mint, YNAB (You Need A Budget), or Personal Capital sync with your accounts to track current balances across all institutions, providing consolidated views and spending analysis.

4. Create balance tracking spreadsheets

For those who prefer manual control, a simple spreadsheet tracking daily current balance, pending transactions, and available balance provides complete visibility:

| Date | Current Balance | Pending Transactions | Available Balance | Notes |

|---|---|---|---|---|

| 4/1 | $2,000 | -$150 (groceries) | $1,850 | Paycheck posted |

| 4/2 | $1,950 | -$75 (gas) | $1,775 | Groceries posted |

This manual approach forces daily financial awareness, building the behavioral discipline that prevents overspending.

Conclusion: Master Your Current Balance, Master Your Finances

Understanding current balance transcends simple account monitoring—it represents a fundamental financial literacy skill that prevents costly mistakes, optimizes credit scores, and builds lasting wealth through disciplined money management.

The math is straightforward: knowing the difference between current balance, available balance, and statement balance prevents $35 overdraft fees, avoids 21%+ credit card interest charges, and maintains the credit utilization ratios that unlock better loan terms and financial opportunities.

Your action plan:

- Check both balances daily: Review current balance for overall position, available balance for spending decisions

- Set up automated alerts: Configure notifications for low balances, large transactions, and payment due dates

- Pay statement balances in full: Eliminate interest charges while preserving cash flow

- Time payments strategically: Pay before statement closing dates to optimize credit utilization reporting

- Track pending transactions: Maintain awareness of holds and pending charges that reduce available funds

- Build a buffer: Keep $200-500 cushion above zero to absorb unexpected fees or holds

The difference between financial stress and financial confidence often comes down to this simple discipline: understanding what your balances actually mean and making decisions based on accurate, real-time data rather than assumptions.

Your current balance is more than a number on a screen—it’s a real-time scorecard of your financial decisions, a predictor of your credit health, and a tool for building the mathematical foundation of lasting wealth.

Start today: Log into your bank and credit card accounts, identify your current balance, available balance, and statement closing dates. This five-minute exercise provides the clarity that prevents years of costly financial mistakes.

The math behind money rewards those who understand it. Current balance mastery is where that understanding begins.

References

[1] Federal Reserve. (2024). “Payment System Improvement – Public Consultation Paper.” Federal Reserve System. https://www.federalreserve.gov/paymentsystems.htm

[2] Consumer Financial Protection Bureau. (2024). “Data Point: Overdraft/NSF Revenue in Q4 2023 down nearly 50% versus pre-pandemic levels.” CFPB Research Reports. https://www.consumerfinance.gov/

[3] Federal Reserve Bank of New York. (2025). “Quarterly Report on Household Debt and Credit.” Center for Microeconomic Data. https://www.newyorkfed.org/microeconomics/hhdc

[4] FICO. (2024). “What’s in my FICO Scores?” MyFICO Consumer Education. https://www.myfico.com/credit-education/whats-in-your-credit-score

[5] Experian. (2024). “What Is a Good Credit Utilization Ratio?” Experian Credit Education. https://www.experian.com/blogs/ask-experian/

Disclaimer

This article provides educational information about current balance concepts for bank accounts and credit cards. It is not personalized financial advice. Banking policies, interest calculation methods, credit reporting practices, and fee structures vary significantly between financial institutions. Always consult your specific bank or credit card issuer’s terms and conditions for precise information about how balances are calculated and reported for your accounts.

Credit score impacts described represent general patterns based on industry research, but individual results vary based on complete credit profiles. For personalized credit or debt management guidance, consult a certified financial planner, credit counselor, or qualified financial advisor.

Interest calculations shown use simplified examples for educational purposes. Actual interest charges may vary based on daily balance fluctuations, promotional rates, penalty APRs, and other factors specific to your account terms.

Author Bio

Max Fonji is the founder of The Rich Guy Math, a data-driven financial education platform that explains the mathematical principles behind wealth building, investing, and personal finance. With a background in financial analysis and a commitment to evidence-based money management, Max translates complex financial concepts into actionable insights for beginner and intermediate investors. His work focuses on helping readers understand the cause-and-effect relationships that drive financial outcomes, empowering them to make informed decisions based on logic, data, and proven frameworks rather than hype or speculation.

FAQs About Current Balance

What’s the difference between current balance and available balance?

Current balance shows the total amount in your account or owed on your credit card based on all posted transactions. Available balance shows how much you can actually spend or withdraw right now, accounting for pending transactions, holds, and restrictions.

Example: $1,000 current balance – $200 pending transactions = $800 available balance. You can only spend the $800, even though your account shows $1,000.

Why is my current balance higher than my available balance?

Your current balance is higher when you have pending transactions, merchant holds, or scheduled payments that haven’t posted yet. These reduce your available funds immediately but don’t update your current balance until they fully process.

Common causes:

- Restaurant tips awaiting final posting

- Gas station holds ($75–$125 typical)

- Hotel or rental car security deposits

- Checks you’ve written that haven’t cleared

- Scheduled automatic payments

Can I spend my current balance?

Not safely. Your available balance represents your true spending power. Attempting to spend your full current balance when pending transactions exist will result in declined purchases or overdraft fees.

Safe practice: Always reference available balance before making purchases and maintain a $100–$200 buffer for unexpected holds or fees.

Does paying my current balance help my credit score?

Yes. Paying your current balance to $0 before your statement closing date maximizes your credit score benefits by showing 0% credit utilization when reported to credit bureaus. However, paying your statement balance in full is sufficient to avoid interest—paying the current balance is optimal but not required for interest-free credit card use.

How often does my current balance update?

Current balance updates in real time as transactions post to your account—typically within 1–3 business days of the transaction. However, the update frequency you see depends on how often you refresh your banking app or website.

The balance itself changes as your bank processes transactions throughout the day, often in batches at specific times (morning, afternoon, evening).

What happens if I only pay the minimum on my current balance?

Paying only the minimum payment keeps your account in good standing and avoids late fees, but triggers interest charges on your entire remaining current balance. At typical credit card APRs (21%+), minimum payments result in years of repayment and hundreds or thousands in interest.

Example: $3,000 balance at 21.47% APR with $75 minimum payments takes 6.5 years to pay off and costs $2,700+ in interest—almost doubling the original debt.

Why does my current balance show a negative number?

A negative current balance means you have a credit on your account—the institution owes you money.

Bank accounts:

- Deposit posted before a check clears

- Refund processed to a zero-balance account

- Bank error in your favor (rare)

Credit cards:

- Return refund exceeds current balance

- Overpayment

- Rewards or statement credits applied

You can typically use negative balances for future purchases or request a refund check from your credit card issuer.

How do I find my statement closing date?

Your statement closing date appears on your monthly credit card or bank statement, typically labeled as “closing date,” “statement date,” or “cycle ending date.”

You can also:

- Log into your online account and check account details

- Call your bank or card issuer

- Check your most recent statement

The closing date is usually the same day each month (e.g., always the 15th) and differs from the payment due date, which usually falls 21–25 days later.

Should I pay my credit card before the statement closes?

Paying before your statement closes reduces the balance reported to credit bureaus, improving your credit utilization ratio and potentially boosting your credit score by 20–40 points.

Optimal timing: Make a large payment 2–3 days before your statement closing date.

Trade-off: You’ll have less cash available during the month, so only use this approach if you have enough liquidity for other expenses.