Imagine having access to tens of thousands of dollars sitting right in your home, ready to help you consolidate debt, renovate your kitchen, or pay for your child’s education. That’s the power of a home equity loan, a financial tool that transforms the equity you’ve built in your property into cash you can use today. But before you tap into this resource, understanding exactly how it works, what it costs, and whether it’s the right choice for your situation is crucial to making a smart financial decision.

TL;DR

- A home equity loan is a lump-sum loan secured by your home’s equity, offering fixed interest rates and predictable monthly payments

- You can typically borrow 80-85% of your home’s value minus what you owe, with loan amounts ranging from $10,000 to $500,000+

- Interest rates are generally lower than credit cards or personal loans because your home serves as collateral

- Best uses include home improvements, debt consolidation, and major expenses—not discretionary spending

- Risk warning: Your home serves as collateral, meaning failure to repay could result in foreclosure

What Is a Home Equity Loan?

In simple terms, a home equity loan is a type of loan that allows homeowners to borrow money using the equity in their home as collateral. Also known as a “second mortgage,” it provides a lump sum of cash upfront that you repay over a fixed term with a fixed interest rate.

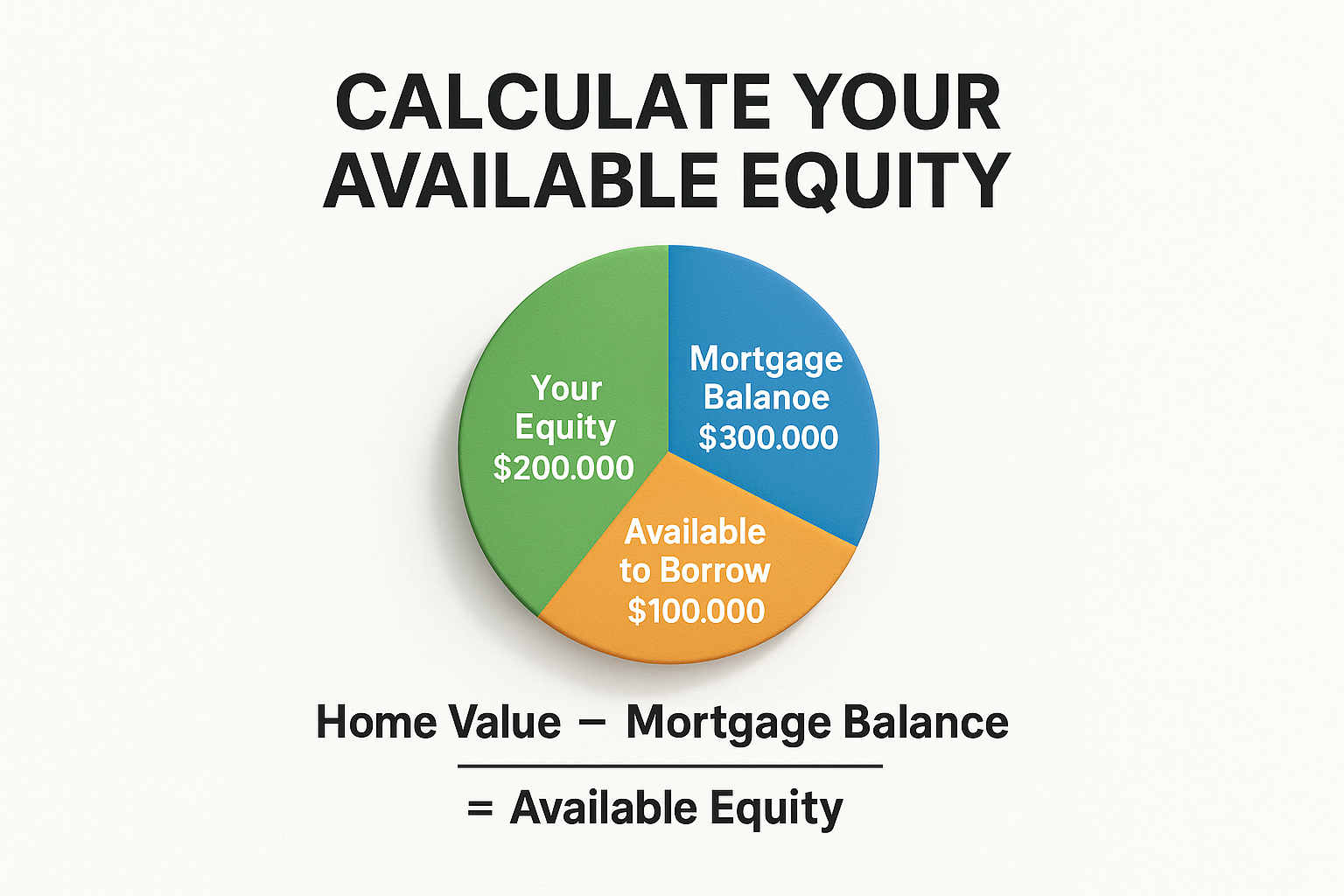

Understanding Home Equity

Before diving deeper, let’s clarify what “equity” means. Home equity is the difference between your home’s current market value and the amount you still owe on your mortgage.

Formula:

Home Equity = Current Home Value - Outstanding Mortgage BalanceExample:

- Your home is worth: $400,000

- You owe on your mortgage: $250,000

- Your home equity: $150,000

This $150,000 represents the portion of your home that you truly “own.” A home equity loan lets you borrow against this value, typically up to 80-85% of it.

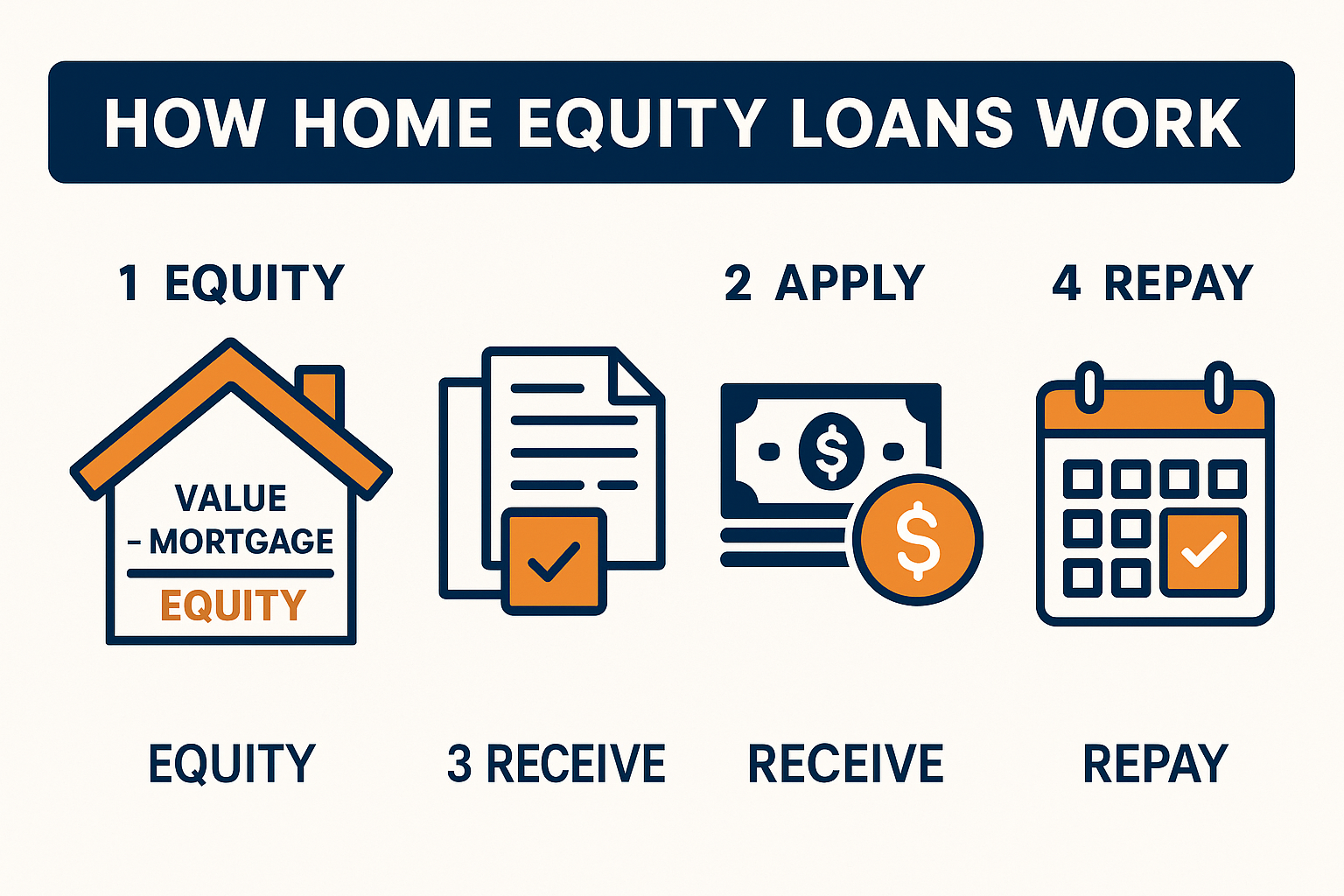

How Does a Home Equity Loan Work?

When you take out a home equity loan, the lender provides you with a single lump sum of money. You then repay this amount over a predetermined period (usually 5-30 years) with fixed monthly payments that include both principal and interest.

Key characteristics:

- Lump sum disbursement – You receive all the money at once

- Fixed interest rate – Your rate stays the same throughout the loan term

- Fixed repayment schedule – Predictable monthly payments

- Secured by your home – Your property serves as collateral

- Second lien position – Sits behind your primary mortgage

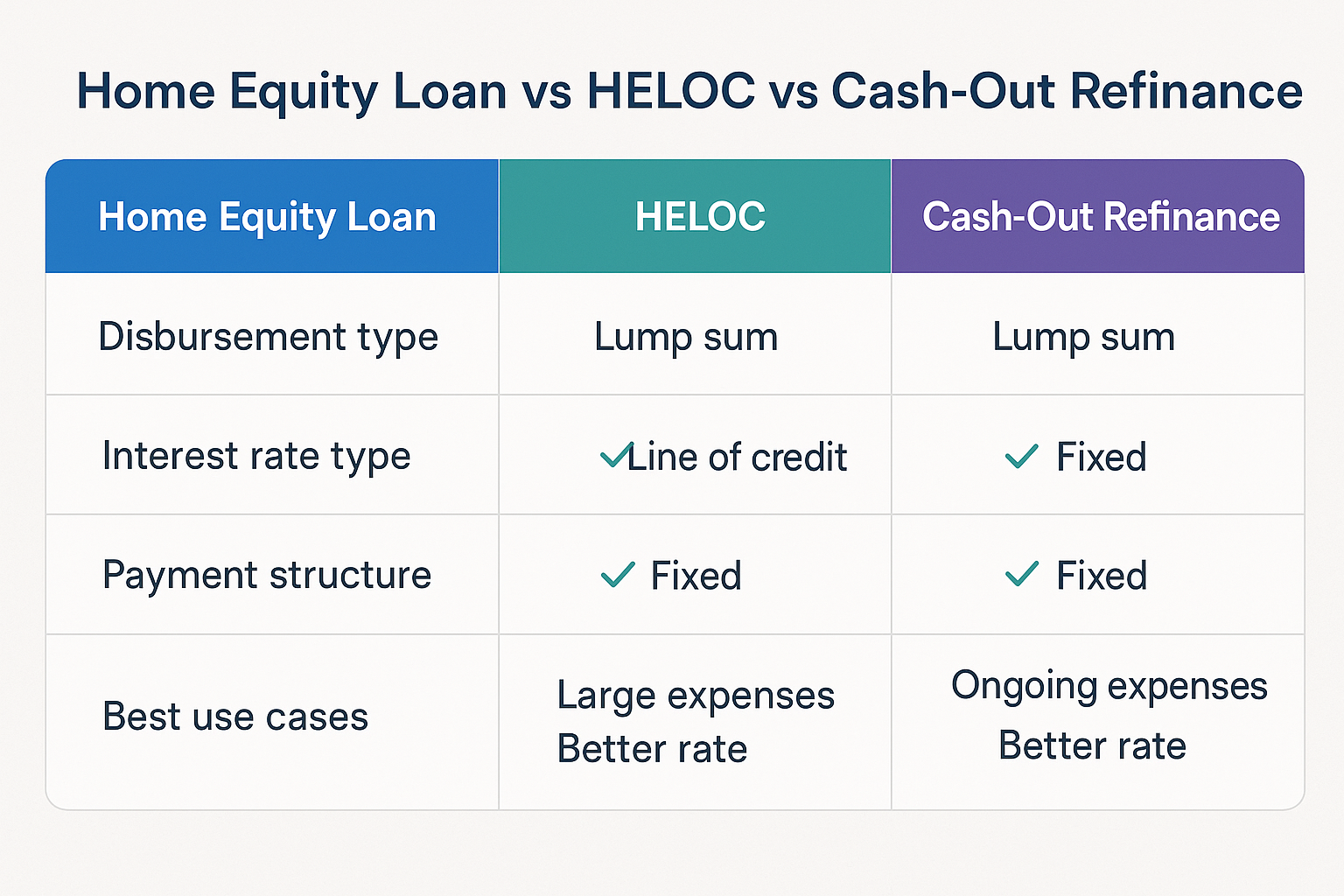

Home Equity Loan vs HELOC vs Cash-Out Refinance

Many homeowners confuse home equity loans with other borrowing options. Here’s a clear comparison:

| Feature | Home Equity Loan | HELOC | Cash-Out Refinance |

|---|---|---|---|

| Type | Lump sum, second mortgage | Revolving credit line | New first mortgage |

| Interest Rate | Fixed | Variable (usually) | Fixed |

| Disbursement | All at once | Draw as needed | All at once |

| Payment | Fixed monthly | Variable (interest-only option) | Fixed monthly |

| Best For | One-time expenses | Ongoing projects | 2-6% of the loan amount |

| Closing Costs | 2-5% of the credit line | Lowering the primary mortgage rate | 2-6% of loan amount |

Bankrate – Home Equity Loan vs. HELOC

When to choose a home equity loan:

- You need a specific amount for a one-time expense

- You prefer predictable payments

- You want protection from rising interest rates

- You’re comfortable with your current mortgage rate

How to Calculate How Much You Can Borrow

Lenders use a metric called the Combined Loan-to-Value ratio (CLTV) to determine how much you can borrow.

The Formula

Maximum Loan Amount = (Home Value × Maximum CLTV) - Current Mortgage BalanceMost lenders cap CLTV at 80-85%, though some may go up to 90% for borrowers with excellent credit.

Real-World Example

Let’s say:

- Your home value: $500,000

- Current mortgage balance: $300,000

- Lender’s maximum CLTV: 85%

Calculation:

- Maximum total debt allowed: $500,000 × 0.85 = $425,000

- Subtract current mortgage: $425,000 – $300,000 = $125,000

You could potentially borrow up to $125,000 with a home equity loan.

Factors That Affect Your Borrowing Limit

Credit score – Higher scores qualify for larger amounts

Debt-to-income ratio – Lower ratios increase borrowing power

Home appraisal value – Higher valuations mean more equity

Employment stability – Steady income improves approval odds

Payment history – A Clean mortgage record helps

The Home Equity Loan Application Process (Step-by-Step)

Getting a home equity loan involves several steps. Here’s what to expect:

Step 1: Assess Your Financial Situation

- Calculate your available equity

- Check your credit score (aim for 620+, ideally 700+)

- Review your debt-to-income ratio (should be below 43%)

- Determine how much you need to borrow

Step 2: Shop Around for Lenders

Compare offers from at least 3-5 lenders:

- Traditional banks

- Credit unions often offer better rates)

- Online lenders

- Your current mortgage lender

Compare these factors:

- Interest rates (APR)

- Loan terms (5, 10, 15, 20, or 30 years)

- Closing costs and fees

- Prepayment penalties

- Customer service reviews

Step 3: Get Pre-Approved

Submit preliminary information to get rate quotes without a hard credit check initially. This helps you:

- Understand what rates you qualify for

- Determine realistic borrowing amounts

- Compare offers side-by-side

Step 4: Formal Application

Once you choose a lender, you’ll submit a full application with:

- Proof of income (pay stubs, tax returns, W-2s)

- Employment verification

- Current mortgage statements

- Homeowners insurance information

- Photo ID and Social Security number

Step 5: Home Appraisal

The lender will order a professional appraisal ($300-$600) to verify your home’s current market value. This determines:

- Your available equity

- Maximum loan amount

- Loan-to-value ratio

Step 6: Underwriting

The lender reviews all documentation to assess risk. This typically takes 2-6 weeks. They’ll verify:

- Your ability to repay

- Property value and condition

- Title search results

- Credit worthiness

Step 7: Closing

Similar to your original mortgage, you’ll:

- Review and sign loan documents

- Pay closing costs (2-5% of loan amount)

- Receive your funds (usually within 3-5 business days)

- Begin your repayment schedule

Timeline: The entire process typically takes 30-45 days from the funding application.

Interest Rates & Costs: What to Expect in 2025

Current Home Equity Loan Rates

As of 2025, home equity loan rates typically range from 7.5% to 11%, depending on:

- Your credit score

- Loan-to-value ratio

- Loan amount and term

- Lender and location

- Current market conditions

Credit Score Impact on Rates:

- 760+: Lowest rates (7.5-8.5%)

- 700-759: Average rates (8.5-9.5%)

- 660-699: Higher rates (9.5-10.5%)

- 620-659: Highest rates (10.5-11%+)

Closing Costs & Fees

Unlike some HELOCs that advertise “no closing costs,” home equity loans typically come with fees:

| Fee Type | Typical Cost |

|---|---|

| Appraisal Fee | $300-$600 |

| Application Fee | $0-$500 |

| Origination Fee | 2-5% of the loan amount |

| Title Search & Insurance | $500-$1,000 |

| Recording Fees | $50-$250 |

| Attorney Fees | $500-$1,500 |

| Credit Report | $25-$50 |

| Total Estimated | 2-5% of loan amount |

Tip: Some lenders offer “no closing cost” options where fees are rolled into your interest rate (typically 0.25-0.5% higher). Consumer Financial Protection Bureau (CFPB)

Tax Deductibility (Important Update)

Under the Tax Cuts and Jobs Act, home equity loan interest is only deductible if the funds are used to “buy, build, or substantially improve” the home that secures the loan.

Deductible uses:

Kitchen renovation

Adding a bedroom

New roof or HVAC system

Building an addition

Non-deductible uses:

Paying off credit cards

Buying a car

Vacation expenses

Wedding costs

Consult with a tax professional to understand your specific situation. Learn more about making smart financial moves that align with your overall wealth-building strategy.

Advantages of Home Equity Loans

1. Lower Interest Rates Than Unsecured Debt

Because your home secures the loan, lenders offer significantly lower rates compared to:

- Credit cards (18-25% APR)

- Personal loans (10-18% APR)

- Payday loans (400%+ APR)

Savings example:

Borrowing $50,000 at 8.5% (home equity) vs. 18% (credit card) over 10 years:

- Home equity loan total interest: $23,739

- Credit card total interest: $54,720

- Savings: $30,981

2. Predictable Fixed Payments

Unlike variable-rate HELOCs or credit cards, you’ll know exactly what you owe each month for the entire loan term. This makes budgeting easier and protects you from rising interest rates.

3. Large Borrowing Amounts

Home equity loans typically offer:

- Minimum: $10,000-$25,000

- Maximum: $500,000+ (depending on equity)

This makes them ideal for major expenses that exceed credit card limits.

4. Flexible Use of Funds

Unlike auto loans or student loans, you can use home equity loan funds for virtually any purpose:

- Home improvements

- Debt consolidation

- Education expenses

- Medical bills

- Business startup costs

- Investment opportunities

5. Potential Tax Benefits

As mentioned earlier, interest may be tax-deductible if used for home improvements (consult your tax advisor).

6. Build Credit History

Making on-time payments on a home equity loan can improve your credit score by demonstrating responsible debt management.

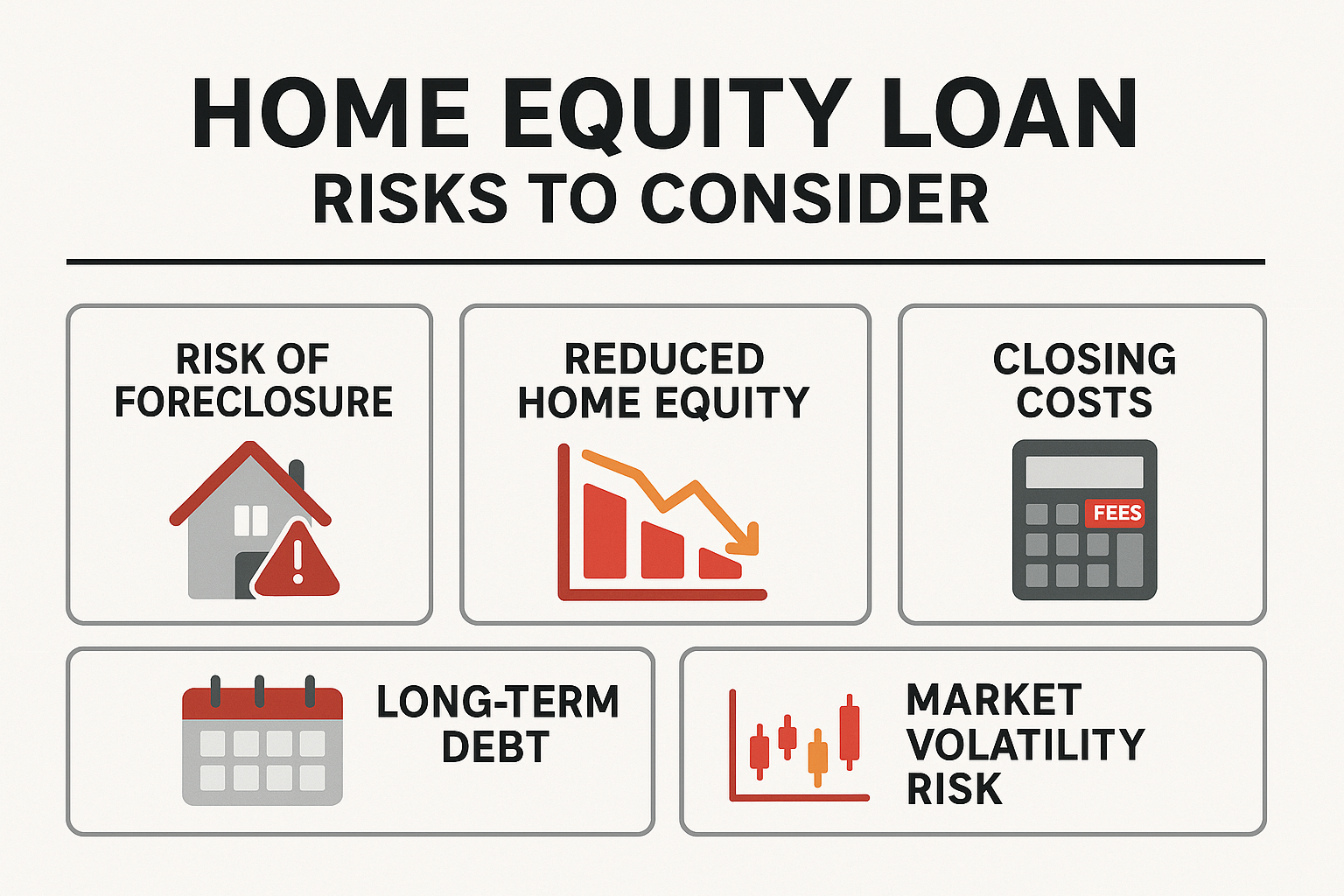

Disadvantages & Risks of Home Equity Loans

1. Your Home Is at Risk

This is the biggest risk: If you default on payments, the lender can foreclose on your home. You could lose your property even if you’re current on your primary mortgage.

Real-world scenario: During the 2008 financial crisis, many homeowners lost their homes because they couldn’t afford both their primary mortgage and home equity loan payments when property values dropped and income declined.

2. Closing Costs Can Be Significant

With 2-5% in closing costs, borrowing $50,000 could cost you $1,000-$2,500 upfront. This reduces the actual amount of usable cash you receive.

3. Reduces Your Home Equity

Every dollar you borrow reduces your ownership stake in your home. This means:

- Less profit when you sell

- Reduced financial cushion in emergencies

- Potential to go “underwater” if home values decline

4. Long-Term Debt Commitment

Taking a 15-20 year home equity loan extends your debt obligations far into the future, potentially limiting your financial flexibility.

5. Prepayment Penalties

Some lenders charge fees if you pay off your loan early (typically within the first 3-5 years). Always read the fine print.

6. Appraisal Risk

If your home appraises for less than expected, you may:

- Qualify for a smaller loan amount

- Face higher interest rates

- Get denied altogether

Best Uses for a Home Equity Loan

Smart Reasons to Borrow

1. Home Improvements with ROI

Investing in your home can increase its value, potentially offsetting the loan amount.

High-ROI projects:

- Kitchen remodel (60-80% ROI)

- Bathroom addition (50-70% ROI)

- Energy-efficient upgrades (varies)

- Curb appeal improvements (50-100% ROI)

2. High-Interest Debt Consolidation

If you’re paying 18-25% on credit cards, consolidating into an 8% home equity loan can save thousands in interest.

Example calculation:

- $30,000 in credit card debt at 20% APR

- Minimum payments: ~$750/month, 15+ years to pay off

- Total interest paid: $105,000+

With a home equity loan at 8% over 10 years:

- Monthly payment: $364

- Total interest paid: $13,680

- Total savings: $91,320+

However, this strategy only works if you address the underlying spending habits that created the credit card debt in the first place.

3. Education Expenses

Home equity loans often offer better rates than private student loans, though federal student loans may still be preferable due to their borrower protections.

4. Medical Expenses

For significant medical bills not covered by insurance, a home equity loan can provide funds at lower rates than medical financing options.

5. Starting or Expanding a Business

Entrepreneurs often use home equity to fund business ventures, though this carries significant risk. Understanding market dynamics and having a solid business plan is crucial before taking this step.

Poor Uses for Home Equity

1. Vacations or Luxury Items

Borrowing against your home for discretionary spending puts your property at risk for temporary enjoyment.

2. Daily Living Expenses

Using home equity to cover regular bills indicates a deeper financial problem that needs addressing through budgeting and income improvement.

3. Risky Investments

While some investors use home equity to invest in stocks or real estate, this strategy is extremely risky. Unlike passive income strategies that build wealth over time, leveraging your home for speculative investments can lead to financial ruin if markets turn.

4. Depreciating Assets

Cars, boats, and electronics lose value rapidly. Financing them with a 15-year home equity loan means you’ll still be paying for them long after they’re worthless.

5. Wedding or Event Costs

Starting married life or celebrating an event with home-secured debt creates unnecessary financial stress.

Home Equity Loan Qualification Requirements

Credit Score Requirements

Minimum scores by lender type:

- Prime lenders: 680-700+

- Subprime lenders: 620-640

- Credit unions: 660-680

- Online lenders: 640-660

Score impact on terms:

- 740+: Best rates, highest loan amounts, lowest fees

- 680-739: Good rates, standard terms

- 620-679: Higher rates, stricter requirements

- Below 620: Very difficult to qualify, extremely high rates

Debt-to-Income Ratio (DTI)

Lenders calculate DTI as:

DTI = (Total Monthly Debt Payments ÷ Gross Monthly Income) × 100DTI requirements:

- Below 36%: Excellent, easily approved

- 36-43%: Acceptable for most lenders

- 43-50%: May qualify with compensating factors

- Above 50%: Very difficult to qualify

Example:

- Gross monthly income: $8,000

- Current mortgage payment: $1,800

- Car payment: $400

- Credit card minimums: $200

- Proposed home equity loan payment: $500

- Total debt: $2,900

- DTI: 36.25% Should qualify

Loan-to-Value Requirements

Most lenders require:

- Maximum CLTV: 80-85% (some go to 90%)

- Minimum equity: 15-20%

Income Verification

You’ll need to prove a stable income through:

- Recent pay stubs (last 2 months)

- W-2 forms (last 2 years)

- Tax returns (last 2 years for self-employed)

- Bank statements (last 2-3 months)

- Employment verification letter

Property Requirements

Your home must:

- Be your primary residence (some lenders allow investment properties)

- Be in good condition (lender may require repairs)

- Have a clear title

- Maintain adequate homeowners’ insurance

- Pass appraisal

How to Use a Home Equity Loan Wisely

1. Borrow Only What You Need

Just because you qualify for $100,000 doesn’t mean you should borrow that much. Calculate your actual need and add a small buffer (10-15%) for unexpected costs.

2. Have a Clear Repayment Plan

Before borrowing, ensure you can comfortably afford the monthly payment. A good rule: Your new total housing payment (mortgage + home equity loan + taxes + insurance) shouldn’t exceed 28% of your gross income.

3. Compare Multiple Lenders

Rate differences of even 0.5% can save thousands over the loan term.

Example: $75,000 loan over 15 years

- At 8.0%: Monthly payment = $717, Total interest = $54,060

- At 8.5%: Monthly payment = $739, Total interest = $58,020

- Savings with lower rate: $3,960

4. Read the Fine Print

Watch for:

- Prepayment penalties

- Variable rate conversion clauses

- Balloon payment requirements

- Hidden fees

- Rate adjustment triggers

5. Maintain an Emergency Fund

Don’t drain your savings to avoid closing costs. Keep 3-6 months of expenses in reserve in case of job loss or emergency.

6. Consider Shorter Loan Terms

While longer terms mean lower monthly payments, they cost significantly more in interest.

Example: $50,000 loan at 8.5%

| Term | Monthly Payment | Total Interest | Total Paid |

|---|---|---|---|

| 10 years | $618 | $24,160 | $74,160 |

| 15 years | $493 | $38,740 | $88,740 |

| 20 years | $432 | $53,680 | $103,680 |

| 30 years | $384 | $88,240 | $138,240 |

Choosing the 10-year term saves $64,080 compared to the 30-year term!

7. Make Extra Payments When Possible

Even small additional payments can significantly reduce interest costs and shorten the loan term.

Strategy: Round up payments or make one extra payment per year. On a $50,000, 15-year loan at 8.5%, adding just $50/month saves $5,700 in interest and pays off the loan 2.5 years earlier.

Common Mistakes to Avoid

1: Treating Your Home Like an ATM

Your home equity isn’t free money—it’s your ownership stake in your property. Repeatedly borrowing against it leaves you vulnerable to market downturns and reduces your net worth.

2: Consolidating Debt Without Changing Spending Habits

Many people consolidate credit card debt with a home equity loan, then run up new credit card balances. This creates a debt spiral that can lead to foreclosure.

Solution: Create a realistic budget, cut unnecessary expenses, and commit to living within your means. Consider resources on making smart financial moves to build better money habits.

3: Ignoring Market Conditions

Borrowing heavily when home values are at peak levels is risky. If the market corrects, you could end up owing more than your home is worth.

Understanding market cycles can help you make more informed borrowing decisions.

4: Skipping the Fine Print

Hidden fees, prepayment penalties, and balloon payments can turn a seemingly good deal into a financial trap.

5: Borrowing for Investments Without Understanding Risk

Using home equity to invest in stocks, cryptocurrency, or speculative real estate is extremely risky. Many people have lost their homes this way, especially during market downturns. Learn about why people lose money in the stock market before considering this strategy.

6: Not Shopping Around

The first lender you contact may not offer the best terms. Comparing at least 3-5 lenders can save thousands.

7: Extending Your Debt Timeline Unnecessarily

If you have 10 years left on your mortgage, taking a 30-year home equity loan means you’ll be in debt for 30 more years. Consider aligning loan terms with your financial goals.

Home Equity Loan Alternatives to Consider

Before committing to a home equity loan, explore these alternatives:

1. HELOC (Home Equity Line of Credit)

Best for: Ongoing projects with variable costs or emergency funds

Advantages:

- Only pay interest on what you use

- Flexibility to borrow, repay, and borrow again during the draw period

- Often, lower initial costs

Disadvantages:

- Variable interest rates (can increase significantly)

- Temptation to overspend

- Payment shock when the repayment period begins

2. Cash-Out Refinance

Best for: When current mortgage rates are lower than your existing rate

Advantages:

- Single monthly payment

- Potentially lower overall interest rate

- May extend the loan term for lower payments

Disadvantages:

- Higher closing costs (2-6% of the total loan)

- Resets your mortgage timeline

- Only beneficial if the new rate is significantly lower

3. Personal Loan

Best for: Smaller amounts ($5,000-$50,000) without risking your home

Advantages:

- No collateral required

- Faster approval (often 1-7 days)

- Lower closing costs or none

Disadvantages:

- Higher interest rates (10-18%)

- Shorter repayment terms (2-7 years)

- Lower borrowing limits

4. 0% Balance Transfer Credit Card

Best for: Debt consolidation with a disciplined repayment plan

Advantages:

- 0% interest for 12-21 months

- No home at risk

- Quick approval

Disadvantages:

- Limited to the available credit limit

- High rates after promotional period (18-25%)

- Balance transfer fees (3-5%)

- Requires excellent credit

5. 401(k) Loan

Best for: Emergencies when no other option exists

Advantages:

- No credit check

- Repay yourself with interest

- Quick access to funds

Disadvantages:

- Reduces retirement savings

- Must repay if you leave your job

- Opportunity cost of lost investment growth

- Not available with all plans

6. Building Passive Income Streams

Instead of borrowing, consider building passive income through dividend investing or other wealth-building strategies. While this takes longer, it creates sustainable financial resources without debt.

Real-World Case Studies

Case Study 1: The Smart Renovation

Situation:

- Sarah owns a home worth $450,000

- Mortgage balance: $280,000

- Available equity: $170,000

- Credit score: 750

Decision:

Sarah took a $60,000 home equity loan at 8.25% for 15 years to renovate her outdated kitchen and bathrooms.

Outcome:

- Monthly payment: $582

- Home value increased to $510,000 (+$60,000)

- Improved quality of life

- Tax-deductible interest (used for home improvement)

- Successfully paid off in 12 years with extra payments

Why it worked: Sarah borrowed for a value-adding improvement, had stable income, and maintained an emergency fund.

Case Study 2: The Debt Consolidation Success

Situation:

- Mike had $45,000 in credit card debt at an average 21% APR

- Monthly minimum payments: $1,125

- Home equity available: $95,000

- Credit score: 680

Decision:

Mike took a $45,000 home equity loan at 9.5% for 10 years to eliminate all credit card debt.

Outcome:

- New monthly payment: $580 (saved $545/month)

- Total interest over 10 years: $24,600 (vs. $180,000+ with credit cards)

- Saved approximately $155,400

- Improved credit score to 740 within 18 months

- Created an automatic savings plan with the $545 monthly savings

Why it worked: Mike addressed his spending habits, cut up his credit cards, created a budget, and committed to never carrying credit card debt again.

Case Study 3: The Cautionary Tale

Situation:

- Jennifer took a $80,000 home equity loan in 2007

- Used funds for: new car ($35,000), vacation ($15,000), paying off credit cards ($30,000)

- Home value: $400,000 at time of loan

Outcome:

- 2008 financial crisis hit

- Home value dropped to $280,000

- Jennifer lost her job

- Couldn’t afford both mortgage and home equity loan payments

- Fell underwater on the property (owed more than it was worth)

- Eventually lost home to foreclosure

Lesson: Never borrow against your home for depreciating assets or discretionary spending. Always maintain emergency reserves and consider economic cycles.

How to Apply for a Home Equity Loan: Actionable Checklist

Ready to move forward? Use this checklist to prepare:

Before You Apply

- [ ] Calculate your available equity

- [ ] Check your credit score (all three bureaus)

- [ ] Review your credit report for errors

- [ ] Calculate your debt-to-income ratio

- [ ] Determine exactly how much you need

- [ ] Create a detailed budget, including the new payment

- [ ] Build or maintain a 3-6 months emergency fund

- [ ] Research current market rates

Shopping for Lenders

- [ ] Contact at least 3-5 lenders

- [ ] Compare APRs (not just interest rates)

- [ ] Review all fees and closing costs

- [ ] Ask about prepayment penalties

- [ ] Check lender reviews and ratings

- [ ] Verify lender credentials and licensing

- [ ] Get all quotes in writing

Documentation to Gather

- [ ] Government-issued photo ID

- [ ] Social Security card

- [ ] Recent pay stubs (last 2 months)

- [ ] W-2 forms (last 2 years)

- [ ] Tax returns (last 2 years if self-employed)

- [ ] Bank statements (last 2-3 months)

- [ ] Current mortgage statement

- [ ] Homeowners insurance policy

- [ ] Property tax statements

- [ ] List of monthly debts and obligations

During the Process

- [ ] Respond promptly to lender requests

- [ ] Don’t make major purchases or open new credit accounts

- [ ] Don’t change jobs if possible

- [ ] Keep documentation organized

- [ ] Ask questions about anything unclear

- [ ] Review all documents before signing

After Closing

- [ ] Set up automatic payments

- [ ] Keep loan documents in a safe place

- [ ] Track payments and interest for tax purposes

- [ ] Consider making extra payments when possible

- [ ] Review statements monthly

- [ ] Maintain homeowners’ insurance

- [ ] Don’t borrow additional home equity unnecessarily

Expert Tips from Financial Advisors

1: The 28/36 Rule

Financial experts recommend keeping your total housing costs (mortgage + home equity loan + taxes + insurance) below 28% of gross income, and total debt payments below 36% of gross income.

Example:

- Gross monthly income: $10,000

- Maximum housing costs: $2,800

- Maximum total debt: $3,600

2: Match Loan Term to Asset Life

If borrowing for home improvements, match your loan term to the improvement’s useful life. For example:

- New roof (20-30 year life): 15-20 year loan

- Kitchen appliances (10-15-year life): 10-year loan

- Vacation (0 years): Don’t use home equity

3: The Investment Return Test

Before borrowing, ask: “Could I earn a higher return investing this money instead of using it for my intended purpose?”

If you’re consolidating 20% credit card debt with an 8% home equity loan, the 12% “return” (savings) makes sense. But if you’re borrowing at 8% to invest in high dividend stocks that might return 6%, the math doesn’t work in your favor.

4: Build in a Safety Margin

When calculating affordability, assume:

- Your income could decrease by 10-20%

- Your expenses might increase by 10-15%

- Interest rates on variable expenses might rise

If you can still afford the payment under these scenarios, you’re in a safer position.

5: Consider Opportunity Cost

Every dollar paid in home equity loan interest is a dollar not invested for your future. Before borrowing, consider whether building passive income streams might better serve your long-term financial goals.

The Bottom Line: Is a Home Equity Loan Right for You?

A home equity loan can be a powerful financial tool when used wisely for value-adding home improvements, high-interest debt consolidation, or essential expenses. The fixed interest rate, predictable payments, and lower rates compared to unsecured debt make it attractive for borrowers with stable income and good credit.

However, the risks are real and significant. Your home serves as collateral, meaning you could lose your property if you can’t make payments. The closing costs, long-term commitment, and reduction in home equity require careful consideration.

You’re a Good Candidate If:

You have a stable income and employment

Your credit score is 680 or higher

You have significant home equity (20%+)

You’re using funds for value-adding purposes

You can comfortably afford the monthly payment

You have emergency savings in place

You understand and accept the risks

You’ve addressed any underlying spending issues

Reconsider If:

Your income is unstable or uncertain

You’re already struggling with debt payments

You want funds for discretionary spending

You don’t have emergency savings

You’re planning to sell your home soon

You haven’t addressed spending habits that created debt

You’re uncomfortable with the risk to your home

Your Next Steps

If you’ve decided a home equity loan makes sense for your situation:

- Calculate your available equity using the formulas provided above

- Check your credit score and review your credit report for errors

- Shop at least 3-5 lenders to compare rates and terms

- Gather required documentation using the checklist above

- Get pre-approved to understand your options

- Review offers carefully and ask questions about anything unclear

- Proceed with the lender offering the best combination of rate, terms, and service

Remember: Borrowing against your home is a serious financial decision that requires careful thought, thorough research, and honest assessment of your financial situation. Take your time, do your homework, and never feel pressured to move faster than you’re comfortable with.

For more insights on building wealth and making smart financial decisions, explore our resources on the stock market and understanding market movements.

Interactive Home Equity Loan Calculator

🏠 Home Equity Loan Calculator

FAQ: Home Equity Loan

A good home equity loan rate in 2025 typically ranges from 7.5% to 9% for borrowers with excellent credit (740+) and strong financial profiles. Rates vary based on credit score, loan-to-value ratio, and lender, so shopping around is essential to find the best deal.

You can typically borrow up to 80-85% of your home’s value minus your existing mortgage balance. For example, if your home is worth $400,000 and you owe $250,000, you could borrow up to $70,000-$90,000, depending on the lender’s maximum CLTV ratio and your qualifications.

Most lenders require a minimum credit score of 620-680 for home equity loan approval. However, to qualify for the best rates and terms, you’ll typically need a score of 700 or higher. Scores above 740 receive the most favorable rates and the highest borrowing limits.

Home equity loan interest is tax-deductible only if you use the funds to “buy, build, or substantially improve” the home securing the loan, according to the Tax Cuts and Jobs Act. Interest on funds used for debt consolidation, education, or other purposes is not deductible. Always consult a tax professional for your specific situation.

If you default on your home equity loan, the lender can foreclose on your home, even if you’re current on your primary mortgage. This is because your home serves as collateral for the loan. Contact your lender immediately if you’re struggling with payments—they may offer forbearance, loan modification, or other hardship options.

The home equity loan process typically takes 30-45 days from the funding application. This includes time for application review (1-3 days), home appraisal (1-2 weeks), underwriting (2-4 weeks), and closing (1 week). Some lenders offer expedited processing for qualified borrowers.

A home equity loan is better if you need a specific lump sum for a one-time expense and prefer fixed, predictable payments. A HELOC is better for ongoing projects or expenses where you need flexibility to borrow and repay multiple times. Home equity loans protect you from rising interest rates, while HELOCs often start with lower rates but can increase over time.

Most home equity loans allow early payoff, but some lenders charge prepayment penalties, especially if you pay off the loan within the first 3-5 years. Review your loan agreement carefully and ask about prepayment terms before signing. Even with a small penalty, early payoff often saves money on interest.

Disclaimer

This article is for educational purposes only and does not constitute financial advice. Home equity loans involve significant financial risk, including the potential loss of your home. Before making any borrowing decision, consult with qualified financial advisors, tax professionals, and legal experts who can evaluate your specific situation. Interest rates, terms, and lending requirements vary by lender and are subject to change. The information presented reflects general market conditions as of 2025 and may not apply to your individual circumstances.

About the Author

Written by Max Fonji — With over a decade of experience in personal finance and investment education, Max is dedicated to helping readers make informed financial decisions. As the founder of TheRichGuyMath.com, Max provides clear, data-backed insights on building wealth, managing debt, and achieving financial independence. His mission is to demystify complex financial concepts and empower individuals to take control of their financial future.

For more educational content on building wealth and making smart money moves, explore our comprehensive blog resources.

Related posts:

What Is SmartPass? Raptor Digital Hall Pass Explained for K-12 Schools

What Is SmartPass? Raptor Digital Hall Pass Explained for K-12 Schools

What Is the 3x Rent Rule & How to Calculate It (With Examples)

What Is the 3x Rent Rule & How to Calculate It (With Examples)

Types of Income: A Complete Guide to Earning and Growing Wealth

Types of Income: A Complete Guide to Earning and Growing Wealth

Tax Filing: A Clear, Step-by-Step Guide for Stress-Free Taxes

Tax Filing: A Clear, Step-by-Step Guide for Stress-Free Taxes

Return on Assets (ROA): Definition, Formula & How to Improve It

Return on Assets (ROA): Definition, Formula & How to Improve It

How to Save Money Fast: A Smart Savings Plan That Actually Works

How to Save Money Fast: A Smart Savings Plan That Actually Works