A single missed payment can haunt your credit report for seven years. That’s 84 months of reduced borrowing power, higher interest rates, and denied applications, all because of one financial misstep.

Understanding how long do late payments stay on credit report records isn’t just about knowing the timeline. It’s about grasping the math behind credit scoring, the legal framework that governs reporting, and the strategic actions that accelerate recovery. The Fair Credit Reporting Act (FCRA) establishes clear rules, but most consumers never learn how to work within this system to minimize damage and rebuild faster.

A credit report is one piece of the broader credit system lenders use to evaluate trustworthiness. For a beginner-friendly overview, see our complete credit guide.

This guide breaks down the exact timeline, the scoring impact at each delinquency stage, and the data-driven strategies that separate those who recover in 18 months from those who struggle for years.

Key Takeaways

- Late payments remain on credit reports for exactly 7 years from the original delinquency date, as mandated by FCRA §605(a)

- Payment history accounts for 35% of FICO scores, making late payments the single most damaging credit factor

- Severity escalates in 30-day increments: 30, 60, 90, 120, and 150+ day delinquencies each trigger progressively larger score drops

- Score impact diminishes over time—a 2-year-old late payment affects scores roughly 60% less than a recent one

- Only legitimate disputes and creditor goodwill can remove accurate late payments before the 7-year mark; “pay for delete” violates FCRA reporting standards

What Counts as a Late Payment? (Definition + FCRA Rules)

A late payment becomes a credit report entry when an account reaches 30 days past the due date. Payments made 1-29 days late typically generate late fees but don’t appear on credit reports.

The reporting threshold exists because of industry standards established by the major credit bureaus, Experian, Equifax, and TransUnion. Creditors report account status monthly, and they classify accounts using standardized codes: current, 30 days late, 60 days late, 90 days late, 120 days late, and charge-off.

The Legal Framework: FCRA §605(a)

The Fair Credit Reporting Act establishes the 7-year reporting period for delinquent accounts. Specifically, FCRA §605(a)(4) states that consumer reporting agencies may not report accounts placed for collection or charged off “which antedate the report by more than seven years.”

The countdown begins from the date of the first delinquency that led to the collection or charge-off, not from the date you eventually paid the account. This original delinquency date remains fixed even if the account changes hands or gets sold to collection agencies.

How Lenders Report to Credit Bureaus

Creditors typically report account information on a monthly cycle, usually aligned with statement closing dates. When an account crosses the 30-day threshold, the creditor updates the payment status code in their next reporting cycle.

This creates a permanent record that includes:

- The date the account became delinquent

- The severity level (30, 60, 90, 120+ days)

- The account balance at the time

- Whether the account was eventually paid or charged off

Most creditors report to all three major bureaus, but reporting isn’t legally required. Some smaller lenders or credit unions may only report to one or two bureaus, creating inconsistencies across your credit files.

Insight: The 30-day reporting threshold means you have a narrow window to catch up on missed payments before credit damage occurs. Setting up automatic payments or payment reminders at least 5-7 days before due dates creates a buffer against accidental late payments.

How Long Do Late Payments Stay on Your Credit Report? (Timeline Breakdown)

Late payments remain on credit reports for exactly 7 years from the original delinquency date, regardless of when you eventually pay the account. This timeline applies uniformly across all three major credit bureaus under FCRA regulations.

The 30-60-90-120 Day Escalation Ladder

Late payment severity increases in 30-day increments, and each level triggers a separate credit report entry:

| Days Late | Credit Report Status | Typical Score Impact | Recovery Difficulty |

|---|---|---|---|

| 1-29 days | Not reported | None (late fee only) | Immediate |

| 30 days | First delinquency | 60-110 points | Moderate |

| 60 days | Second delinquency | 70-130 points | Challenging |

| 90 days | Third delinquency | 80-150 points | Severe |

| 120 days | Pre-charge-off | 90-160 points | Very severe |

| 150+ days | Charge-off/Collections | 100-180+ points | Extreme |

Each escalation creates a new negative entry on your credit report. An account that reaches 90 days late will show three separate delinquency markers: 30 days, 60 days, and 90 days late.

The 7-Year Countdown Mechanism

The clock starts ticking from the date of initial delinquency—the first missed payment that you never caught up on. If you missed a payment in March 2025 and never brought the account current, that March 2025 date becomes the anchor point. The late payment entry will automatically fall off your credit report in March 2032.

This date remains fixed even if:

- You make a partial payment later

- The account gets sold to a collection agency

- The creditor updates other account information

- You dispute the entry unsuccessfully

Paying the account doesn’t restart the clock or extend the reporting period. The 7-year timeline is absolute.

Visual Timeline Example

Scenario: Credit card payment due January 15, 2025

- January 15-February 13, 2025: Account 1-29 days late (not reported)

- February 14, 2025: Account hits 30 days late (reported to bureaus)

- March 14, 2025: Account reaches 60 days late (second delinquency reported)

- April 14, 2025: Account reaches 90 days late (third delinquency reported)

- February 14, 2032: All late payment entries automatically removed (7 years from first 30-day mark)

Understanding credit score fundamentals helps contextualize why these timelines matter so significantly for borrowing power.

Takeaway: The 7-year period is non-negotiable and automatic. Credit bureaus use sophisticated systems to track original delinquency dates and remove entries precisely when the statute expires. Manual intervention isn’t required; the entries disappear automatically.

How Late Payments Affect Your Credit Score (The Math Behind the Damage)

Payment history represents 35% of your FICO score, the largest single factor in credit scoring algorithms. A single late payment can trigger score drops ranging from 60 to 180+ points, depending on your starting profile and the severity of the delinquency.

FICO vs VantageScore: Different Approaches to Late Payments

The two dominant scoring models treat late payments similarly but with subtle differences:

| Factor | FICO Score | VantageScore |

|---|---|---|

| Payment history weight | 35% of total score | “Extremely Influential” (highest category) |

| Recency emphasis | Strong—recent lates hurt more | Very strong—recent behavior heavily weighted |

| Single late payment impact | 60-110 point drop (good credit) | 70-120 point drop (good credit) |

| Multiple late payments | Compounding damage | Severe compounding damage |

| Recovery timeline | 18-36 months to baseline | 18-30 months to baseline |

Both models use time-based decay; older late payments have progressively less impact as they age. A 30-day late payment from 6 years ago might reduce your score by only 5-10 points, while the same delinquency from last month could drop it by 90+ points.

Score Drop Ranges by Starting Profile

The credit score impact varies dramatically based on your profile before the late payment:

Excellent Credit (750-850):

- 30 days late: 90-110 point drop

- 60 days late: 110-130 point drop

- 90+ days late: 130-150 point drop

Good Credit (680-749):

- 30 days late: 70-90 point drop

- 60 days late: 90-110 point drop

- 90+ days late: 110-130 point drop

Fair Credit (620-679):

- 30 days late: 60-80 point drop

- 60 days late: 80-100 point drop

- 90+ days late: 100-120 point drop

Consumers with higher starting scores experience larger absolute drops because they have further to fall. Someone with a 780 score might drop to 680 from a single 30-day late payment, while someone at 650 might only drop to 590.

The Compounding Effect of Multiple Late Payments

Multiple late payments create exponential damage rather than additive damage. Two late payments don’t simply double the impact; they signal a pattern of financial distress that scoring models penalize heavily.

Example calculation:

- First 30-day late payment: -90 points (780 → 690)

- Second 30-day late payment (different account): -70 additional points (690 → 620)

- Third 30-day late payment: -50 additional points (620 → 570)

The same account escalating through multiple delinquency stages creates similar compounding effects. An account that reaches 90 days late doesn’t just accumulate three separate 30-point penalties—it triggers algorithm flags for severe financial distress.

Impact Decay Over Time

Late payment impact follows a logarithmic decay curve rather than a linear reduction:

- Months 0-6: Maximum impact (100% weight)

- Months 6-12: 85-90% of original impact

- Year 1-2: 60-75% of original impact

- Year 2-3: 40-55% of original impact

- Year 3-5: 20-35% of original impact

- Year 5-7: 5-15% of original impact

This decay pattern explains why consumers often see significant score improvements around the 24-month mark without taking any specific action. The late payment remains on the report, but its algorithmic weight diminishes substantially.

Managing credit utilization alongside payment history creates the fastest path to score recovery, as utilization represents the second-largest FICO factor at 30%.

Insight: The mathematical relationship between payment history and credit scores illustrates why prevention is more important than remediation. Avoiding a single late payment preserves more score points than any recovery strategy can rebuild in under 18 months.

Can You Remove a Late Payment Early? (What Actually Works)

Removing accurate late payments before the 7-year mark requires navigating a complex landscape of consumer rights, creditor policies, and legal limitations. Most removal strategies fail because consumers misunderstand what’s legally permissible versus what’s marketed online.

Disputing Factual Errors (The Only Guaranteed Path)

The Fair Credit Reporting Act grants consumers the right to dispute inaccurate or incomplete information in their credit reports. If a late payment was reported incorrectly, you can initiate a dispute through:

- Direct bureau disputes: File online, by mail, or by phone with Experian, Equifax, and TransUnion

- Creditor disputes: Contact the original lender’s customer service or credit reporting department

- CFPB complaints: File complaints through the Consumer Financial Protection Bureau for unresolved disputes[2]

Legitimate grounds for disputes include:

- Payment was made on time, but reported late

- Late payment belongs to someone else (identity error)

- The account was in deferment or forbearance

- Creditor violated notification requirements

- Duplicate late payment entries for the same delinquency

Credit bureaus have 30 days to investigate disputes under FCRA §611. They contact the creditor to verify the information, and if the creditor can’t substantiate the late payment, the bureau must remove it.

What doesn’t qualify for disputes:

- “I forgot to pay” (accurate reporting)

- “I was going through a hard time” (doesn’t change accuracy)

- “The late fee was too high” (separate from reporting accuracy)

- “I paid it eventually” (doesn’t erase the original delinquency)

Goodwill Adjustment Requests (Low Success Rate, Worth Trying)

A goodwill letter asks the creditor to remove an accurate late payment as a courtesy gesture. This approach works best when:

- You have a long positive history with the creditor (5+ years)

- The late payment was an isolated incident (first in 12+ months)

- You’ve already brought the account current

- You can demonstrate extenuating circumstances (medical emergency, natural disaster)

Effective goodwill letter structure:

- Opening: Acknowledge that the late payment was accurate

- Context: Briefly explain the unusual circumstance

- History: Highlight your positive payment record

- Request: Politely ask for removal as a one-time courtesy

- Commitment: Emphasize your ongoing reliability

Success rates hover around 15-25% based on consumer reports, with higher success for customers who have significant relationship value (multiple accounts, high balances, long tenure). Credit unions and smaller regional banks typically show more flexibility than large national creditors.

Send goodwill letters to the creditor’s executive customer service or credit reporting department, not general customer service. Include your account number, contact information, and a clear subject line.

Why “Pay for Delete” Violates FCRA Standards

“Pay for delete” arrangements—where creditors agree to remove accurate late payments in exchange for payment—technically violate the accuracy requirements of the Fair Credit Reporting Act. Creditors who furnish information to credit bureaus must report complete and accurate information.

The Metro 2 format (the industry standard for credit reporting) requires creditors to report actual account history, not negotiated versions. Major creditors with compliance departments rarely engage in pay-for-delete because it exposes them to regulatory risk.

Some collection agencies still offer informal pay-for-delete arrangements, but these create several problems:

- No legal enforcement mechanism if they don’t follow through

- Potential re-reporting if the account gets sold again

- Inconsistent removal across all three bureaus

- Risk of the deletion being reversed during bureau audits

Rapid Rescore: Only for Correcting Errors

Rapid rescore is a lender-initiated process that updates credit reports within 3-7 days instead of the standard 30-45 days. It’s used primarily during mortgage applications when borrowers need quick score improvements.

Critical limitations:

- Only available through lenders (you can’t initiate it directly)

- Only works for correcting errors or updating newly paid balances

- Costs $25-50 per bureau per correction

- Cannot remove accurate late payments

Lenders use rapid rescore when borrowers pay down high credit utilization or correct reporting errors that are preventing loan approval. It’s a timing tool, not a removal strategy.

When Disputes Can Backfire

Frivolous disputes—challenging accurate information without legitimate grounds- can create several problems:

- Creditor verification: The creditor may add detailed notes to your file documenting the accuracy

- Bureau flags: Repeated frivolous disputes may result in bureaus flagging your file

- Wasted time: The 30-day investigation period delays other recovery strategies

- Relationship damage: Creditors may view you as difficult, reducing goodwill letters success

The Consumer Financial Protection Bureau has documented cases where consumers filed dozens of disputes on accurate information, resulting in the bureau’s requiring notarized documentation for future disputes.

Takeaway: Focus removal efforts on legitimate errors and isolated goodwill requests. Accurate late payments will remain for the full 7-year period in most cases; energy is better spent on recovery strategies that work within this reality.

How to Recover After a Late Payment (Step-by-Step Plan)

Credit score recovery after a late payment follows predictable mathematical patterns. The strategies that work fastest combine immediate damage control with long-term rebuilding tactics that leverage how scoring algorithms weight different factors.

Step 1: Stop the Bleeding (Prevent Further Delinquency)

The priority is preventing the account from escalating to 60, 90, or 120+ days late. Each additional 30-day increment compounds the damage exponentially.

Immediate actions:

- Bring the account current within 24-48 hours if possible

- Set up automatic payments for at least the minimum due

- Contact the creditor to discuss hardship programs if you can’t pay immediately

- Request a payment plan that prevents further delinquency reporting

Many creditors offer forbearance or deferment programs that temporarily pause payment requirements without additional late payment reporting. These programs typically require proactive contact before the account reaches 60 days late.

Step 2: Optimize Credit Utilization (The Fastest Score Booster)

Credit utilization—the percentage of available credit you’re using—represents 30% of FICO scores and updates monthly. Reducing utilization creates measurable score improvements within 30-45 days.

Target utilization levels:

- Under 30%: Good (prevents score penalties)

- Under 10%: Excellent (maximizes score benefit)

- Under 5%: Optimal (used by consumers with 800+ scores)

Utilization optimization strategies:

- Pay down balances before statement closing dates (not just due dates)

- Request credit limit increases on accounts with good standing

- Distribute balances across multiple cards to avoid high per-card utilization

- Make mid-cycle payments to keep reported balances low

A consumer with a 680 score and 60% utilization who reduces to 10% utilization can see 40-60 point improvements within two months—partially offsetting the late payment damage.

Understanding the 50/30/20 rule budgeting framework helps allocate income toward strategic debt paydown while maintaining emergency reserves.

Step 3: Build an On-Time Payment Streak

Payment history improvement comes from accumulating positive payment data that gradually outweighs the late payment. Each month of on-time payments adds positive weight to your credit file.

The mathematical progression:

- 6 months on-time: Late payment impact reduced by ~15%

- 12 months on-time: Late payment impact reduced by ~30%

- 24 months on-time: Late payment impact reduced by ~50%

- 36 months on-time: Late payment impact reduced by ~70%

This doesn’t mean the late payment disappears; it remains visible for 7 years. But the scoring algorithm progressively reduces its weight as positive payment history accumulates.

Automation strategies:

- Link payments to a checking account with a 5-7 day buffer before due dates

- Use credit card autopay for recurring subscriptions

- Set up calendar alerts 10 days before due dates for manual review

- Monitor accounts weekly through credit card apps or aggregators

Step 4: Add Positive Credit Accounts Strategically

New positive accounts dilute the impact of the late payment by increasing the ratio of good accounts to bad. However, this strategy requires careful timing to avoid hard inquiry damage.

Effective account additions:

Secured credit cards: Require a deposit, guaranteed approval, rand eport to all three bureaus. Ideal for rebuilding because they function identically to regular cards in scoring algorithms.

Credit builder loans: Small installment loans (typically $300-1,000) where the lender holds funds in a savings account while you make payments. Creates a positive installment history that diversifies your credit mix.

Authorized user positions: Being added to someone else’s account with a perfect payment history can add positive data to your file. Choose accounts that are 5+ years old with utilization under 10%.

Retail store cards: Easier approval standards, but should be used sparingly. Only valuable if you can maintain 0% utilization and a perfect payment history.

Timing consideration: Wait 3-6 months after a late payment before applying for new credit. The hard inquiry from applications temporarily reduces scores, and approval odds are lower immediately after delinquencies.

Step 5: Monitor All Three Credit Reports

Credit bureaus don’t share information, creating reporting inconsistencies. A late payment might appear on Experian but not Equifax, or might show different dates across bureaus.

Free monitoring resources:

- AnnualCreditReport.com: Official FCRA-mandated free reports (one per bureau per year)

- Credit card issuer monitoring: Many cards offer free FICO or VantageScore tracking

- Credit Karma: Free VantageScore 3.0 monitoring (Equifax and TransUnion)

- Experian free account: Free Experian FICO Score 8 with monthly updates

Review reports every 3-4 months to catch:

- Errors in late payment dates or severity

- Accounts that should have aged off but didn’t

- Fraudulent accounts or identity theft

- Opportunities to dispute legitimate errors

Step 6: Build Emergency Reserves (Prevent Future Late Payments)

The most effective late payment recovery strategy is preventing the next one. Emergency funds create a buffer that prevents temporary cash flow problems from becoming credit disasters.

Reserve building framework:

- Month 1-3: Accumulate $500-1,000 starter emergency fund

- Month 4-9: Build to one month of essential expenses

- Month 10-18: Expand to three months of expenses

- Month 19+: Target six months for complete stability

Park emergency funds in high-yield savings accounts or best compound interest accounts that provide liquidity with competitive returns.

Insight: Recovery speed depends more on consistent execution of fundamentals than on clever tactics. Consumers who automate payments, maintain low utilization, and avoid new delinquencies typically recover 70-80% of lost score points within 18-24 months.

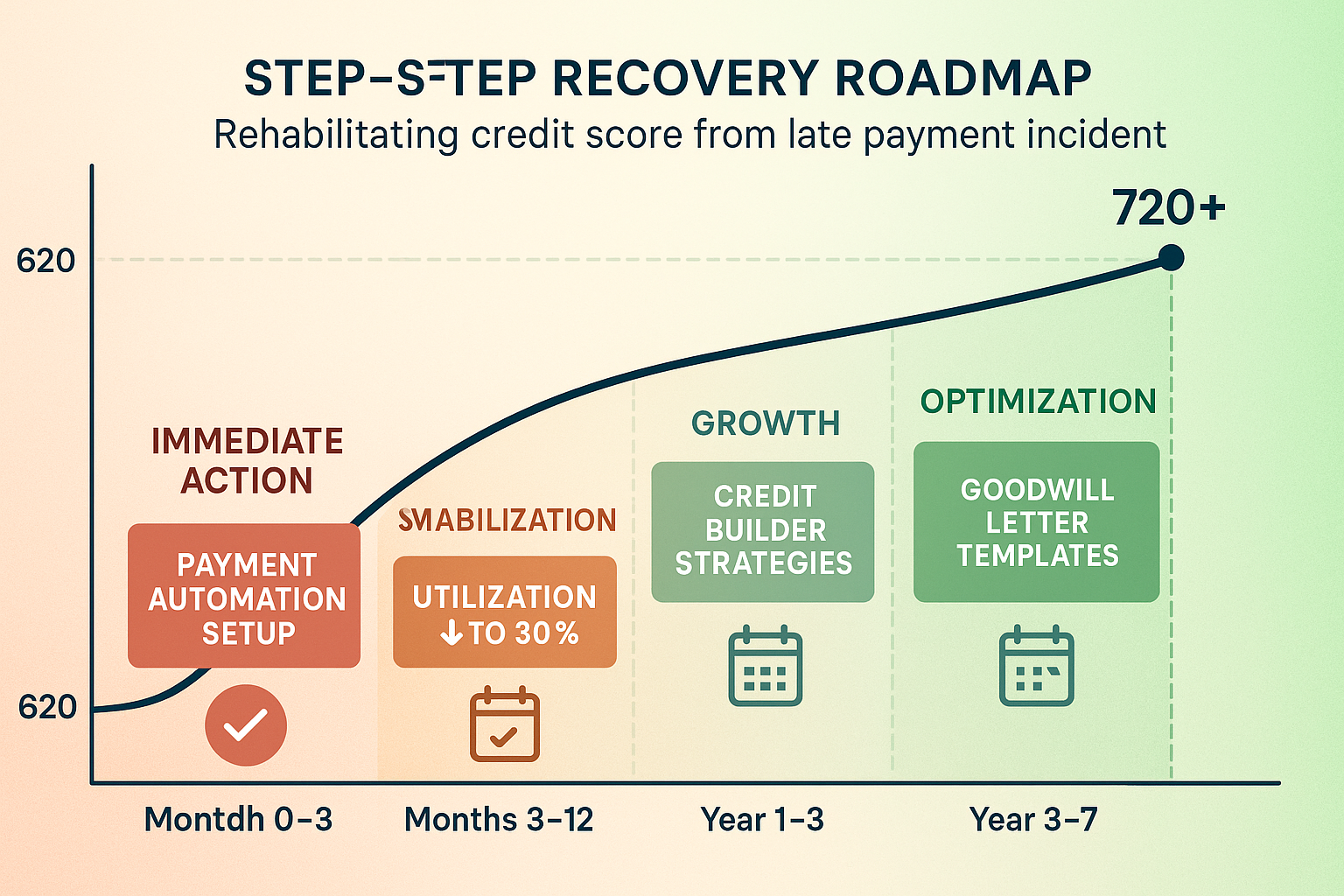

How Long Does It Take Your Score to Recover? (Real Timeline Expectations)

Credit score recovery follows predictable patterns based on the severity of the late payment, your starting profile, and the consistency of your rebuilding efforts. Understanding realistic timelines prevents frustration and helps set appropriate expectations.

Case Study: The 670 → 720 Recovery Curve

Starting profile (March 2025):

- Credit score: 750 (excellent)

- Payment history: Perfect (8 years)

- Utilization: 15%

- Credit age: 8 years

- Recent inquiries: 1

Event: Single 30-day late payment on credit card

Immediate impact (April 2025):

- Score drops to 670 (-80 points)

- Utilization remains at 15%

- No other negative changes

Recovery timeline with optimization:

Month 1-3 (April-June 2025):

- Reduced utilization from 15% to 5%

- Maintained perfect payments on all accounts

- No new credit applications

- Score: 685 (+15 points from utilization improvement)

Month 4-6 (July-September 2025):

- Continued perfect payment history

- Added authorized user position on the parent’s 15-year-old card

- Utilization maintained at 5%

- Score: 700 (+15 points from positive data accumulation)

Month 7-12 (October 2025-March 2026):

- Six months of perfect payments post-late payment

- Late payment impact begins algorithmic decay

- Credit age increases

- Score: 715 (+15 points from time-based decay)

Month 13-24 (April 2026-March 2027):

- Late payment is now 12-24 months old

- Continued perfect payment streak

- Opened secured credit card for additional positive tradeline

- Score: 735 (+20 points from significant time decay)

Month 25-36 (April 2027-March 2028):

- Late payment is now 24-36 months old

- Impact reduced to ~40% of the original weight

- Score: 745 (+10 points from continued aging)

Total recovery time to exceed original score: Approximately 36-42 months

This timeline assumes perfect execution of recovery strategies. Any additional late payments, high utilization spikes, or collections would significantly extend the recovery period.

Recovery Timeline Variables

Several factors accelerate or delay recovery:

Accelerating factors:

- A thick credit file (10+ accounts) dilutes the single late payment impact

- A long credit history (10+ years) demonstrates established reliability

- Low utilization (under 10%) maximizes the second-largest FICO factor

- A diverse credit mix (revolving + installment) shows broader experience

- No additional negative events during the recovery period

Delaying factors:

- Thin credit file (3-5 accounts) magnifies single late payment weight

- Short credit history (under 3 years) lacks a positive data foundation

- High utilization (over 30%) compounds negative scoring factors

- Additional late payments or collections during recovery

- Recent hard inquiries from multiple credit applications

Expected Recovery by Late Payment Severity

Different delinquency levels require different recovery timelines:

| Delinquency Type | Initial Score Drop | 50% Recovery Time | 90% Recovery Time | Full Recovery Time |

|---|---|---|---|---|

| 30 days late | 60-110 points | 12-18 months | 24-30 months | 36-48 months |

| 60 days late | 70-130 points | 18-24 months | 30-36 months | 48-60 months |

| 90 days late | 80-150 points | 24-30 months | 36-48 months | 60-72 months |

| Charge-off | 100-180 points | 30-42 months | 48-60 months | 72-84 months |

“Full recovery” means returning to your pre-late payment score or higher. “90% recovery” represents the point where most consumers regain access to prime lending rates and approval odds.

The Plateau Effect at 24 Months

Most consumers experience a recovery plateau around the 24-month mark. Initial improvements come quickly from utilization optimization and positive payment accumulation, but the final 10-20 points require additional time for the late payment to age further.

This plateau occurs because:

- Utilization benefits max out once you’re consistently under 10%

- Payment history improvements slow as you approach the algorithm’s positive ceiling

- Late payment weight reduction follows a logarithmic curve (rapid early decay, slower later decay)

- Credit age improvements happen gradually and can’t be accelerated

Consumers who understand this plateau avoid frustration and maintain consistent habits rather than searching for quick fixes that don’t exist.

Takeaway: Recovery to “good” credit (680-720) typically takes 12-24 months with disciplined execution. Recovery to “excellent” credit (740+) requires 30-48 months because scoring algorithms maintain some late payment weight throughout the 7-year reporting period.

Strategic Insights: Advanced Recovery Tactics

Beyond the fundamental recovery strategies, several advanced tactics can accelerate score rebuilding for consumers who understand credit scoring nuances.

The Credit Age Rehabilitation Curve

The average age of accounts (AAoA) represents approximately 15% of FICO scores. Late payments can’t be removed early, but you can dilute their impact by strategically managing account age.

Optimal approach:

- Keep old accounts open even with zero balances

- Avoid closing your oldest credit card

- Become an authorized user on accounts older than your oldest account

- Limit new account openings to 1-2 per year, maximum

Each month that passes increases your AAoA by a small amount. A consumer with a 5-year average who avoids new accounts for 24 months will have a 7-year average, which provides meaningful score benefits that partially offset late payment damage.

The Utilization Micro-Optimization Strategy

Most consumers track overall utilization, but FICO also evaluates per-card utilization. Having one card at 80% utilization hurts more than having four cards at 20% utilization, even if the total utilization percentage is identical.

Advanced utilization tactics:

- Pay down highest-utilization cards first (not highest-balance cards)

- Request credit limit increases on low-utilization cards

- Use cards with small balances to keep accounts active

- Make payments before statement closing dates to control reported balances

A consumer with $10,000 total credit limit and $3,000 debt (30% overall) scores better by distributing the debt across multiple cards ($750 each on four cards = 30% card) than concentrating it ($3,000 on one card = 100% on that card, 0% on others).

The Inquiry Timing Strategy

Hard inquiries reduce scores by 5-10 points each and remain on reports for 24 months (though they only affect scores for 12 months). After a late payment, timing new credit applications strategically prevents compounding damage.

Optimal inquiry timing:

- Wait 6-12 months after late payment before applying for new credit

- Use pre-qualification tools that perform soft pulls

- Consolidate applications within 14-45 day windows (FICO treats multiple inquiries for the same loan type as a single inquiry)

- Target creditors known for approving consumers with recent late payments

This approach ensures you’re not adding inquiry-based score reductions on top of late payment damage during the critical first 12 months when recovery efforts matter most.

The Statement Balance Gaming Technique

Credit card issuers report balances to bureaus on statement closing dates, not payment due dates. This creates an opportunity to manipulate reported utilization without changing spending patterns.

Implementation:

- Identify statement closing dates for all cards (usually 21-25 days before the due date)

- Make payments 2-3 days before the closing date

- Allow regular spending to occur after the closing date

- The reported balance stays low even with normal monthly spending

Example:

- Statement closes: 1st of each month

- Payment due: 25th of each month

- Strategy: Pay balance to $0 on the 28th-30th of the previous month

- Result: The Bureau sees $0 balance even though you spend $2,000/month on the card

This technique requires careful tracking but can maintain 0-5% reported utilization while still using credit cards for rewards and convenience.

📊 Credit Score Recovery Timeline Calculator

Conclusion: The Math Behind Credit Recovery

Late payments create measurable, predictable damage that follows mathematical decay curves over 7 years. Understanding how long do late payments stay on credit report files—and more importantly, how their impact diminishes over time- transforms recovery from guesswork into a data-driven process.

The evidence is clear: payment history represents 35% of FICO scores, making it the single most influential factor in credit scoring algorithms. A late payment can drop scores by 60-180 points, depending on severity and starting profile, but the damage isn’t permanent in its intensity. Time-based decay reduces impact by approximately 50% after 24 months and 70% after 36 months, even though the entry remains visible for the full 7 years.

Recovery speed depends on execution consistency across multiple variables: maintaining utilization below 10%, building uninterrupted payment streaks, strategically adding positive tradelines, and avoiding compounding damage from additional delinquencies. Consumers who optimize these factors typically recover 70-80% of lost score points within 18-24 months.

The FCRA’s 7-year reporting period is absolute; accurate late payments cannot be removed early through legitimate means. Energy spent disputing accurate information or pursuing “pay for delete” schemes yields lower returns than focusing on the proven recovery strategies outlined in this guide.

Your Next Steps

- Pull all three credit reports from AnnualCreditReport.com to verify late payment accuracy and dates

- Calculate your current utilization across all revolving accounts and create a paydown plan targeting under 10%

- Automate all payments with 5-7 day buffers before due dates to prevent future delinquencies

- Set calendar reminders to review credit reports every 90 days for errors or unauthorized accounts

- Build emergency reserves equivalent to 3-6 months of expenses to prevent cash flow problems from becoming credit disasters

The math behind credit recovery is straightforward: consistent positive behavior compounds over time, gradually outweighing isolated negative events. Late payments create temporary setbacks, not permanent obstacles, for consumers who understand the system and execute disciplined recovery strategies.

Understanding broader financial principles like the 50/30/20 rule budgeting framework helps allocate income toward strategic goals while maintaining the payment consistency that drives credit recovery. Similarly, applying risk management principles to personal finance creates the stability that prevents future credit damage.

Credit scores measure financial reliability through mathematical models. Late payments temporarily reduce that measured reliability, but they don’t define your long-term financial trajectory. The data shows that disciplined recovery efforts produce predictable results, and those results compound faster than most consumers expect when they understand the underlying mechanisms.

References

[1] Fair Credit Reporting Act, 15 U.S.C. § 1681c(a)(4) – https://www.ftc.gov/legal-library/browse/statutes/fair-credit-reporting-act

[2] Consumer Financial Protection Bureau – Submit a Complaint – https://www.consumerfinance.gov/complaint/

[3] Consumer Financial Protection Bureau – Credit Reporting Dispute Process – https://www.consumerfinance.gov/ask-cfpb/what-should-i-do-when-a-credit-reporting-company-says-they-cant-find-the-information-i-am-disputing-en-314/

Educational Disclaimer

This article provides educational information about credit reporting timelines and recovery strategies. It does not constitute financial advice, credit repair services, or legal counsel. Credit scoring models use proprietary algorithms that may produce results different from the estimates provided in this guide.

Individual credit situations vary based on numerous factors, including credit history length, account mix, utilization patterns, and recent credit activity. The timelines and score projections presented represent typical scenarios based on industry research and scoring model documentation, but actual results may differ.

Readers should verify information with the three major credit bureaus (Experian, Equifax, TransUnion) and consult qualified financial advisors for personalized guidance. The strategies discussed comply with Fair Credit Reporting Act regulations as of 2025, but credit reporting laws and industry practices may change.

The Rich Guy Math provides data-driven financial education to help readers understand the mathematical principles underlying personal finance decisions. We do not offer credit repair services, dispute filing assistance, or individualized credit counseling.

Author Bio

Max Fonji is the founder of The Rich Guy Math, where he translates complex financial concepts into clear, data-driven insights. With a background in financial analysis and a passion for evidence-based investing education, Max helps readers understand the mathematical principles that drive wealth building, credit scoring, and long-term financial success.

His approach combines analytical rigor with accessible teaching, breaking down topics like compound interest, valuation principles, and credit mechanics into actionable frameworks. Max believes financial literacy stems from understanding cause-and-effect relationships in money systems, not from following generic advice.

Through The Rich Guy Math, Max has helped thousands of readers build stronger financial foundations by teaching them to think like analysts rather than consumers. His work emphasizes the importance of understanding the numbers behind financial decisions, from credit score algorithms to investment return calculations.

Frequently Asked Questions

Does paying off a late payment remove it from my credit report?

No. Paying a late payment updates the account status to “paid,” but it does not remove the delinquency. The late payment stays on your credit report for the full 7 years from the original delinquency date. Under the FCRA, credit bureaus must report accurate historical data even after the account is brought current.

Can I have different late payment information on each credit bureau?

Yes. Creditors are not required to report to all three credit bureaus, and reporting frequency varies. It’s common to see a late payment on Experian but not on Equifax or TransUnion. Errors can also cause inconsistencies. Always review all three reports and dispute errors with the specific bureau where they appear.

Will a late payment from 6 years ago prevent me from getting a mortgage?

Probably not. Late payments lose most of their impact after 2–3 years. Mortgage lenders typically focus on the last 12–24 months of payment history. A single 6-year-old late payment with perfect history since then rarely blocks mortgage approval, though it may have a slight effect on your interest rate. Recent late payments are far more damaging.

Do late payments on closed accounts still affect my score?

Yes. Closed accounts remain on your credit report, and late payments tied to them stay for 7 years from the original delinquency date. Closing the account does not change how long the late payment remains or how it affects your score.

Can medical bills create late payments on my credit report?

Medical debt follows special rules. As of 2023, credit bureaus:

- Remove paid medical collections

- Exclude medical collections under $500

- Wait 12 months before reporting unpaid medical collections

If your medical bill goes to collections after 12 months and exceeds $500, it can appear on your report and hurt your score similar to other collections. Paying or negotiating medical bills before the 12-month window prevents them from appearing at all.

Will disputing a late payment hurt my credit score?

No. Disputing a late payment does not lower your score. Your report may temporarily show the account as “in dispute,” but this is neutral. If the creditor verifies the late payment as accurate, it stays on your report with the same score impact. Investigations typically take about 30 days.

How many points will my score drop from a single late payment?

The drop varies widely:

- Excellent credit (750+): −90 to −110 points

- Fair credit (620–680): −60 to −80 points

Severity also matters. A 90-day late payment can cause up to 30–40% more damage than a 30-day late payment.

Can I get a late payment removed by switching to autopay?

No. Autopay only prevents future late payments. It does not remove past delinquencies. Some creditors may grant a goodwill adjustment if you request one and show responsible behavior (such as enabling autopay), but they are not obligated to remove accurate late payment history.

Related posts:

Credit Utilization Ratio Explained: What It Is, How It Works, And How To Improve It

Credit Utilization Ratio Explained: What It Is, How It Works, And How To Improve It

Statement Closing Date: What It Is & How It Affects Your Credit Score

Statement Closing Date: What It Is & How It Affects Your Credit Score

Statement Balance vs Current Balance: Which One Should You to Pay

Statement Balance vs Current Balance: Which One Should You to Pay

Current Balance vs Available Balance: What’s the Difference?

Current Balance vs Available Balance: What’s the Difference?

Credit Card APR Explained: What It Is And How Interest Really Works

Credit Card APR Explained: What It Is And How Interest Really Works

How Long Does It Take to Build Credit? Real Timeline Explained

How Long Does It Take to Build Credit? Real Timeline Explained