An installment loan is money you borrow once and repay in fixed monthly payments over a set period of time.

Common examples include car loans, student loans, personal loans, and mortgages. Each serves a specific purpose but follows the same fundamental structure.

Many beginners think installment loans and credit cards work the same way. This creates confusion because they are completely different types of borrowing. Credit cards offer revolving credit that replenishes as you pay it down, while installment loans provide a one-time lump sum with a clear payoff date.

If you’re new to borrowing, it helps to first understand how the credit system works overall. This foundation makes installment loan concepts much clearer.

This guide will explain how installment loans work, how lenders evaluate them, and how they affect your credit score. The math behind money becomes clearer when you understand these borrowing fundamentals.

Key Takeaways

Fixed Structure: Installment loans provide a lump sum upfront with predictable monthly payments over a set timeline

Credit Impact: They affect payment history (35% of your score) and credit mix (10%), but don’t impact utilization like credit cards

Lower Rates: Installment loans typically offer lower interest rates than credit cards, especially for borrowers with good credit

Closed-End Debt: Unlike revolving credit, installment loans have a definite end date when the balance reaches zero

Credit Building: Consistent payments help establish a positive payment history, but secured credit cards are usually better for first-time credit building

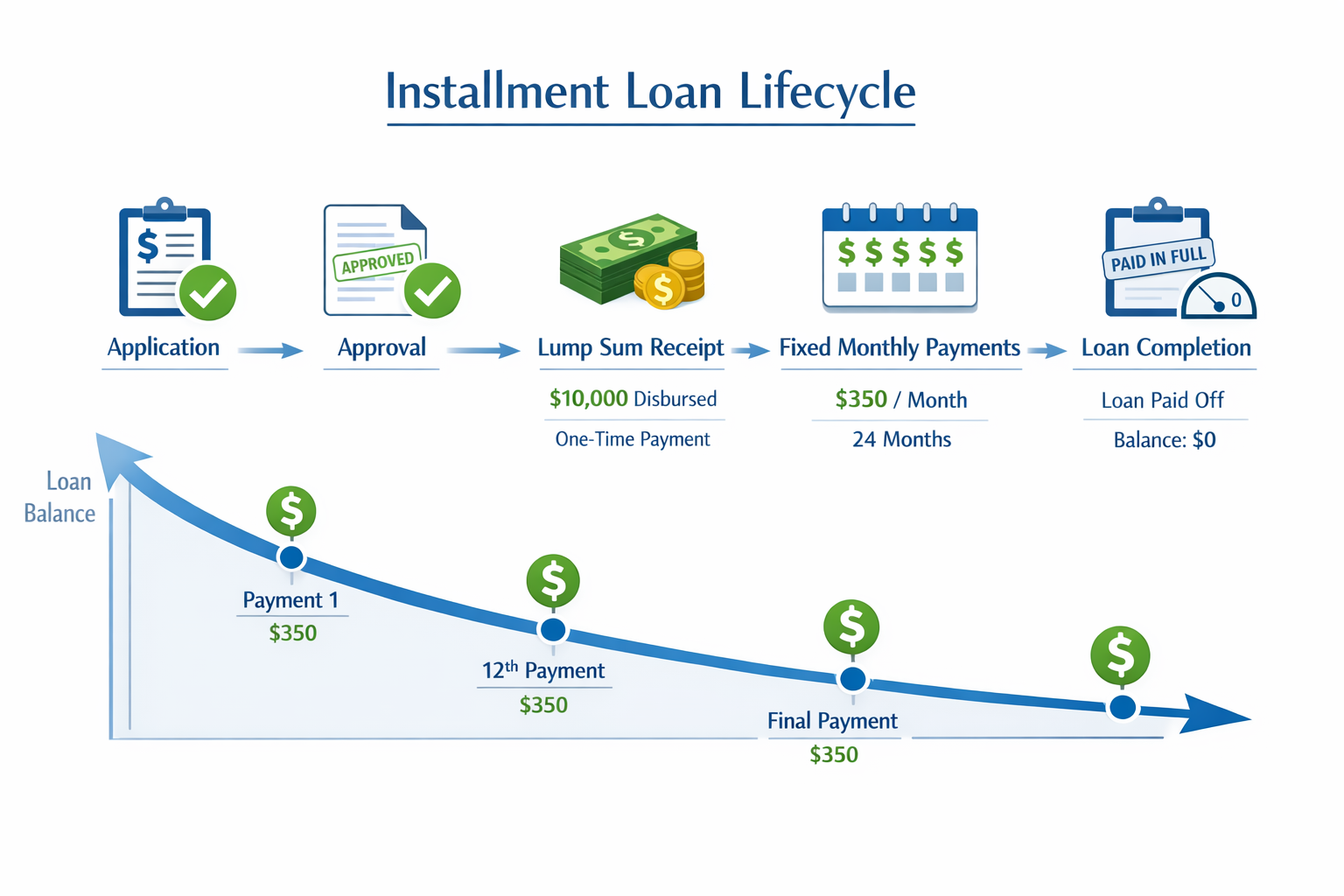

How an Installment Loan Works

The installment loan lifecycle follows five clear steps that create predictable borrowing costs.

Step 1: Application You apply for a specific loan amount and term length. Lenders review your credit score, income, and debt-to-income ratio to determine approval odds.

Step 2: Approval and Terms If approved, the lender sets your interest rate, monthly payment, and repayment schedule. These terms remain fixed throughout the loan.

Step 3: Lump Sum Receipt You receive the full loan amount at once, unlike credit cards, where you access funds gradually.

Step 4: Fixed Monthly Payments You make identical payments each month until the loan is paid off. Each payment includes principal and interest components [1].

Step 5: Loan Completion The loan ends when you make the final payment. The account closes, and your debt obligation ends.

Real-World Example

Borrow $10,000 at 8% interest for 5 years → pay $203 per month for 60 months.

The $203 payment includes both principal repayment and interest charges. Early payments contain more interest, while later payments contain more principal. This amortization schedule ensures the loan balance reaches zero on the final payment date.

Key Insight: Interest is built into each payment, so you always know your total borrowing cost upfront.

Common Types of Installment Loans

Different installment loan types serve specific financial needs with varying terms and qualification requirements.

Auto Loans

Auto loans finance vehicle purchases with the car serving as collateral. Terms typically range from 3-7 years, with interest rates varying by credit score and vehicle age.

Lenders can repossess the vehicle if payments stop, which reduces their risk and keeps interest rates relatively low.

Student Loans

Student loans fund education expenses with extended repayment periods, often 10-25 years. Federal student loans offer fixed rates and income-driven repayment options.

Private student loans require credit checks and may have variable interest rates based on market conditions.

Personal Loans

Personal loans provide unsecured financing for debt consolidation, home improvements, or major purchases. Terms usually range from 2-7 years with no collateral required.

Interest rates depend heavily on credit scores since lenders have no assets to seize if payments stop [3].

Mortgages

Mortgages finance home purchases with repayment terms extending 15-30 years. The property serves as collateral, allowing for lower interest rates despite large loan amounts.

Monthly payments include principal, interest, property taxes, and insurance (PITI) in most cases.

Credit Builder Loans

Credit builder loans help establish payment history for borrowers with limited credit. The loan funds are held in a savings account until the loan is repaid.

These loans prioritize credit building over immediate access to funds.

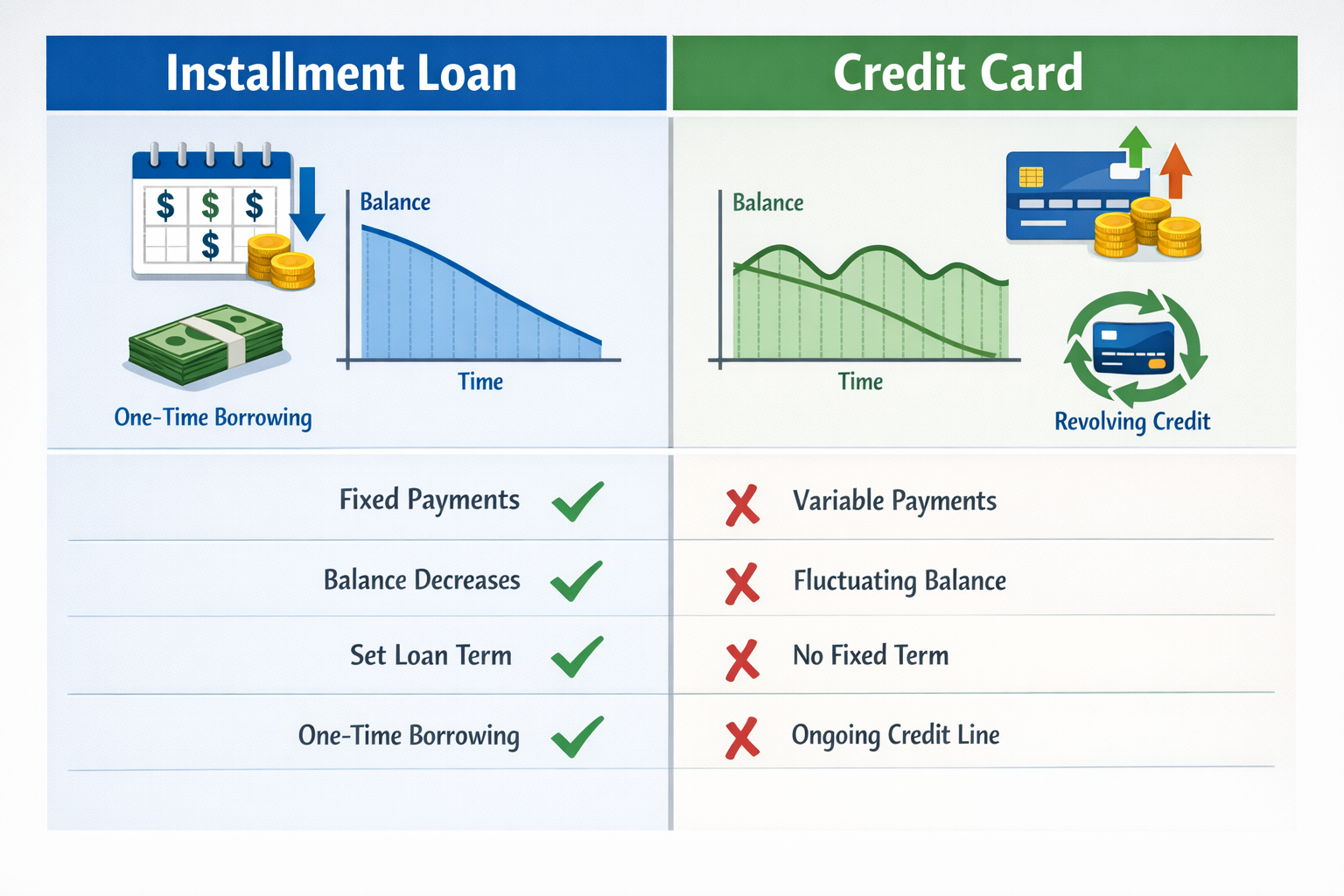

Installment Loan vs Credit Card (Revolving Credit)

Understanding the differences between installment loans and credit cards prevents borrowing mistakes and improves financial planning.

Feature

Installment Loan

Credit Card

Borrowing

One-time lump sum

Reusable credit line

Payments

Fixed amount

Variable minimum

End Date

Definite payoff

No set end

Balance

Decreases only

Fluctuates

Interest

Fixed rate (usually)

Variable rate

Credit Impact

Payment history, mix

Payment history, utilization

Borrowing Structure: Installment loans provide all funds upfront, while credit cards allow ongoing borrowing up to your credit limit.

Payment Predictability: Installment loans require identical monthly payments, making budgeting straightforward. Credit cards have minimum payments that change based on your balance.

Account Lifecycle: Installment loans close when paid off. Credit cards remain open indefinitely unless you or the lender closes them.

Credit cards fall under a different category called revolving accounts, which operate on fundamentally different principles than installment debt.

Takeaway: Choose installment loans for planned purchases with predictable costs. Use credit cards for flexible spending and rewards optimization.

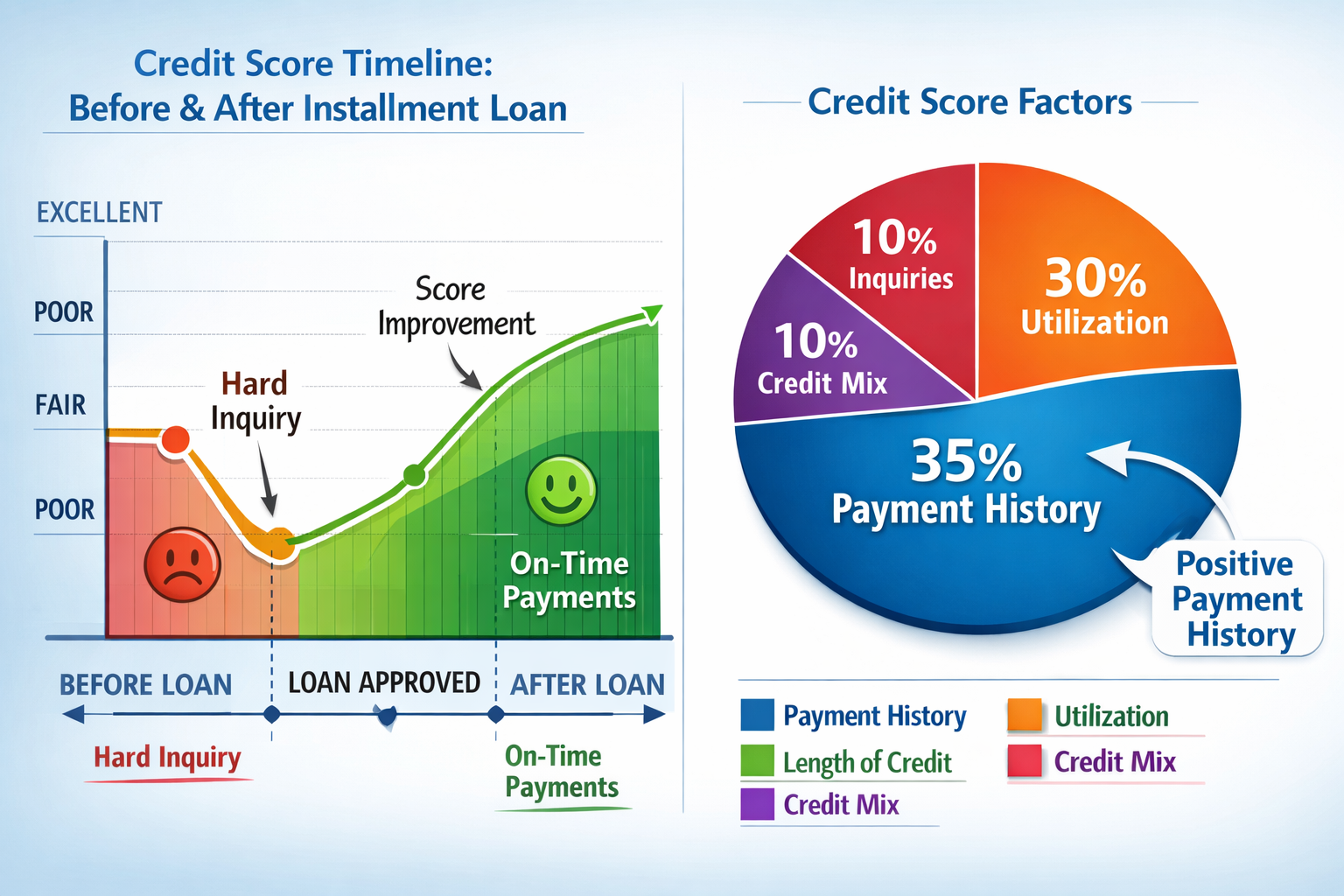

How Installment Loans Affect Your Credit Score

Installment loans impact your credit score through multiple factors, but their effect differs significantly from credit card utilization.

Payment History Impact (35% of Score)

Every monthly payment gets reported to credit bureaus as either on-time or late. Consistent payments build positive history, while missed payments create lasting damage.

Timeline: Payment history begins reporting within 30-60 days of your first payment. Late payments appear after 30+ days past due.

Credit Mix Improvement (10% of Score)

Having both installment loans and revolving accounts demonstrates your ability to manage different credit types. This credit mix diversity slightly improves your score.

Lenders prefer borrowers who successfully handle various credit products because it indicates financial responsibility.

Account Age Contribution

Installment loans contribute to your average account age, which affects 15% of your credit score. A longer credit history generally improves your score over time.

The account continues contributing to your credit age even after you pay off the loan, though closed accounts eventually fall off your report.

No Utilization Impact

Critical difference: Installment loans don’t affect credit utilization ratios like credit cards do. Your $10,000 auto loan doesn’t count as “maxed out credit” even though you owe the full amount.

Credit utilization only applies to revolving accounts, not installment debt [5].

Lenders evaluate these behaviors using the information on your credit report, which tracks all account activity and payment patterns.

Does Taking a Loan Hurt Your Credit?

Taking an installment loan causes a temporary credit score dip, but the long-term impact is typically positive with responsible management.

Initial Score Impact

Hard Inquiry Effect: Applying for a loan triggers a hard credit inquiry, which temporarily lowers your score by 2-5 points. This effect diminishes over 12 months and disappears after 24 months.

New Account Impact: Opening a new installment account slightly reduces your average account age, causing another small temporary dip.

Recovery Timeline

Month 1-3: Score may drop 5-10 points from inquiry and new account Month 4-12: Score stabilizes as payment history begins building Month 13+: Score often improves beyond the original level due to positive payment history and credit mix

Long-Term Benefits

Consistent on-time payments create a positive payment history that outweighs the initial inquiry impact. Many borrowers see net score improvements within 6-12 months of taking an installment loan.

Reassurance: The temporary score drop is normal. Focus on making payments on time rather than worrying about short-term fluctuations.

Benefits of Installment Loans

Installment loans offer several advantages that make them valuable financial tools when used appropriately.

Predictable Payment Structure

Fixed monthly payments eliminate guesswork from budgeting. You know exactly how much you’ll pay each month and when the debt will be eliminated.

This predictability helps with cash flow planning and prevents payment shock from variable interest rates.

Clear Payoff Timeline

Unlike credit cards with no set end date, installment loans have definite payoff schedules. This psychological benefit helps borrowers stay motivated and debt-free.

Example: A 5-year auto loan has exactly 60 payments. After paying 60, you own the car free and clear.

Access to Large Purchase Amounts

Installment loans enable major purchases like homes, cars, and education that would be impossible to buy with cash for most people.

The extended repayment terms make large amounts affordable through manageable monthly payments.

Credit Profile Enhancement

Successfully managing installment debt demonstrates financial responsibility to future lenders. This positive history can improve qualification odds and interest rates on future loans.

The stability that lenders appreciate comes from the predictable payment structure and clear debt reduction timeline.

Risks and Downsides

Understanding installment loan risks helps borrowers make informed decisions and avoid financial problems.

Interest Cost Accumulation

Total Interest Burden: Longer loan terms reduce monthly payments but increase total interest paid over the loan’s life.

Example: A $20,000 car loan at 6% costs $2,000 in interest over 3 years but $3,200 over 5 years.

Payment Default Consequences

Missed payments damage your credit score and stay on your credit report for seven years. This long-term impact affects future borrowing costs and approval odds.

Secured Loan Risk: Missing payments on secured loans (auto, mortgage) can result in asset repossession or foreclosure.

Long-Term Financial Commitment

Installment loans create fixed payment obligations that reduce financial flexibility. Economic changes, job loss, or income reduction can make payments difficult.

Planning Consideration: Ensure you can afford payments even if your income decreases by 10-20%.

Fees and Penalties

Many installment loans include origination fees, prepayment penalties, or late payment charges that increase borrowing costs beyond the stated interest rate.

Due Diligence: Read all loan terms carefully and calculate total borrowing costs, including fees.

Installment Loan vs Payday Loan (Critical Authority Section)

Understanding the difference between installment loans and payday loans protects borrowers from predatory lending practices.

Structural Differences

Installment Loans: Extended repayment terms (months to years) with manageable monthly payments and regulated interest rates.

Payday Loans: Short-term debt (2-4 weeks) with full repayment due on your next payday, often with APRs exceeding 400%.

Cost Comparison

Example: Borrowing $500 for 3 months

Personal installment loan at 15% APR = $172 in payments, $16 in interest

Payday loan rolled over 6 times = $600+ in fees alone

Regulatory Protection

Installment loans from traditional lenders follow federal and state lending regulations that cap interest rates and require clear disclosure of terms.

Payday loans often exploit regulatory loopholes and target financially vulnerable borrowers with unsustainable debt cycles.

Critical Distinction: Payday loans are short-term, high-interest debt, not traditional installment loans. Avoid payday lenders and seek installment loans from banks, credit unions, or licensed online lenders instead.

Should Beginners Use an Installment Loan to Build Credit?

Installment loans can help build credit, but they’re not always the best starting point for credit beginners.

When Installment Loans Make Sense

Necessary Purchase: If you need a car for work or housing, an installment loan serves the dual purpose of financing the purchase and building credit.

Existing Credit: If you already have some credit history, adding an installment loan improves your credit mix.

Better Alternatives for Beginners

Secured Credit Cards: These require a cash deposit but offer more flexibility and faster credit building for first-time borrowers.

Credit Builder Loans: Specifically designed for credit building with lower qualification requirements than traditional installment loans.

Strategic Considerations

Building credit requires a consistent payment history over time. Credit cards offer more opportunities to demonstrate responsible usage through monthly statement cycles.

Balanced Advice: Use installment loans when you need financing for a specific purchase, not solely for credit-building purposes.

What Happens When You Pay Off an Installment Loan

Paying off an installment loan triggers several credit score changes that borrowers should understand and expect.

Immediate Score Effects

Account Closure Impact: Your credit score may dip slightly (5-10 points) when the installment account closes. This happens because you lose an active account contributing to your credit mix.

Utilization Changes: If you used loan proceeds to pay off credit cards, your utilization ratio improves, potentially offsetting the closed account impact.

Long-Term Credit Benefits

Positive History Retention: The paid-off loan remains on your credit report for 10 years, continuing to contribute positive payment history.

Debt-to-Income Improvement: Eliminating the monthly payment improves your debt-to-income ratio for future loan applications.

Score Stabilization Timeline

Month 1-2: Temporary score dip from account closure Month 3-6: Score stabilizes at new baseline Month 6+: Score often improves due to lower debt burden and positive payment history

Key Understanding: The temporary score drop after payoff is normal and doesn’t indicate financial problems. Your credit profile strengthens over time from successful loan management.

How Lenders Evaluate an Installment Loan Application

Lenders use specific criteria to assess installment loan applications, focusing on your ability to repay the debt consistently over time.

Income Verification

Primary Consideration: Lenders verify your gross monthly income through pay stubs, tax returns, or bank statements. They want to ensure you earn enough to cover the new payment plus existing obligations.

Self-Employed Borrowers: May need to provide additional documentation like profit and loss statements or multiple years of tax returns.

Debt-to-Income Ratio Analysis

Calculation: Lenders divide your total monthly debt payments by your gross monthly income. Most prefer ratios below 36-43%, though requirements vary by loan type.

Example: $3,000 monthly income with $1,200 in debt payments = 40% debt-to-income ratio.

Credit History Review

Payment Patterns: Lenders examine your payment history to predict future payment behavior. Recent late payments carry more weight than older issues.

Account Management: They review how you’ve handled previous installment loans and credit cards to assess financial responsibility.

Credit Score Requirements

Score Ranges: Different lenders have varying minimum credit score requirements:

Excellent (740+): Best rates and terms

Good (670-739): Competitive rates

Fair (580-669): Higher rates, stricter terms

Poor (Below 580): Limited options, secured loans

Employment Stability

Job History: Lenders prefer borrowers with a stable employment history, typically requiring 2+ years in the same field or with the same employer.

Income Consistency: Variable income earners may need to demonstrate higher average earnings to qualify for the same loan amounts.

The length of your credit history also influences approval decisions, as longer credit histories provide more data for lenders to assess risk patterns.

Insight: Lenders care most about your ability to make consistent payments. Focus on demonstrating stable income and responsible credit management rather than perfect credit scores.

Installment Loan Payment Calculator

Installment Loan Payment Calculator

Please enter a valid loan amount

Please enter a valid interest rate (0-50%)

Please enter a valid loan term (1-30 years)

Monthly Payment:$0

Total Interest Paid:$0

Total Amount Paid:$0

Payment Breakdown:

Principal per payment: $0

Interest per payment: $0

Conclusion

Installment loans are not good or bad — they are tools that serve specific financial purposes when used strategically.

The Math Behind Smart Borrowing: Installment loans work best for planned purchases where the fixed payment structure supports your budget and the asset or goal justifies the interest cost. They help when used for necessary expenses like transportation, education, or housing — not impulse spending.

Credit Building Reality: While installment loans can improve your credit mix and payment history, they’re most valuable when you need financing for a specific purchase. Use them as part of a broader credit strategy, not as standalone credit-building tools.

Key Decision Framework: Before taking an installment loan, ensure you can afford the payment even if your income drops 10-20%. Calculate the total interest cost and confirm the purchase aligns with your long-term financial goals.

Next Steps: If you’re considering an installment loan, start by checking your credit score and calculating your debt-to-income ratio. Shop rates from multiple lenders and read all terms carefully before signing. Remember that the lowest payment isn’t always the best deal if it extends your repayment timeline significantly.

The data-driven approach to installment loans focuses on total borrowing costs, payment affordability, and strategic credit building rather than just monthly payment amounts.

Author Bio: Max Fonji is a financial educator and analyst who specializes in making complex financial concepts accessible through data-driven insights. He focuses on helping readers understand the math behind money to make informed borrowing and investing decisions.

Educational Disclaimer: This article is for educational purposes only and does not constitute financial advice. Loan terms, interest rates, and qualification requirements vary by lender and individual circumstances. Always consult with qualified financial professionals and read all loan documents carefully before making borrowing decisions.

Frequently Asked Questions

Are installment loans good for credit?

Yes, installment loans can improve your credit score through consistent payment history and by adding credit mix diversity. However, opening a new loan often causes a temporary 5–10 point score drop due to a hard inquiry and the new account. The long-term benefit depends on making every payment on time.

Is a mortgage an installment loan?

Yes. Mortgages are installment loans with long repayment terms, typically 15 to 30 years. You receive a lump sum at closing, make fixed monthly payments, and the loan has a defined payoff date. The home itself acts as collateral for the loan.

Do installment loans have fixed interest rates?

Most installment loans have fixed interest rates, meaning your rate and monthly payment stay the same for the life of the loan. However, some personal loans and certain student loans may offer variable rates that can change over time depending on market conditions.

Can you pay off an installment loan early?

In most cases you can pay off an installment loan early, but you should first check for prepayment penalties. Paying early reduces total interest costs, though your credit score may dip slightly when the account closes. Your positive payment history can remain on your credit report for up to 10 years.

What happens if you miss a payment?

Missing an installment loan payment can trigger late fees, potential interest rate increases, and credit score damage. Payments that are 30 days or more late are reported to the credit bureaus and remain on your credit report for seven years. If you anticipate trouble making a payment, contact your lender immediately to discuss hardship or repayment options.