The minimum payment due is the smallest amount you must pay on your credit card bill each month to keep your account in good standing. While paying only the minimum keeps you out of late fees, it also means interest continues to accumulate, often costing you more over time. Understanding how the minimum payment works and the financial impact of paying more can help you manage debt smarter, protect your credit score, and save money on interest.

This article is part of our complete Credit Guide, where we break down APRs, interest, rewards, fees, and how to use credit cards the smart way.

Key Takeaways

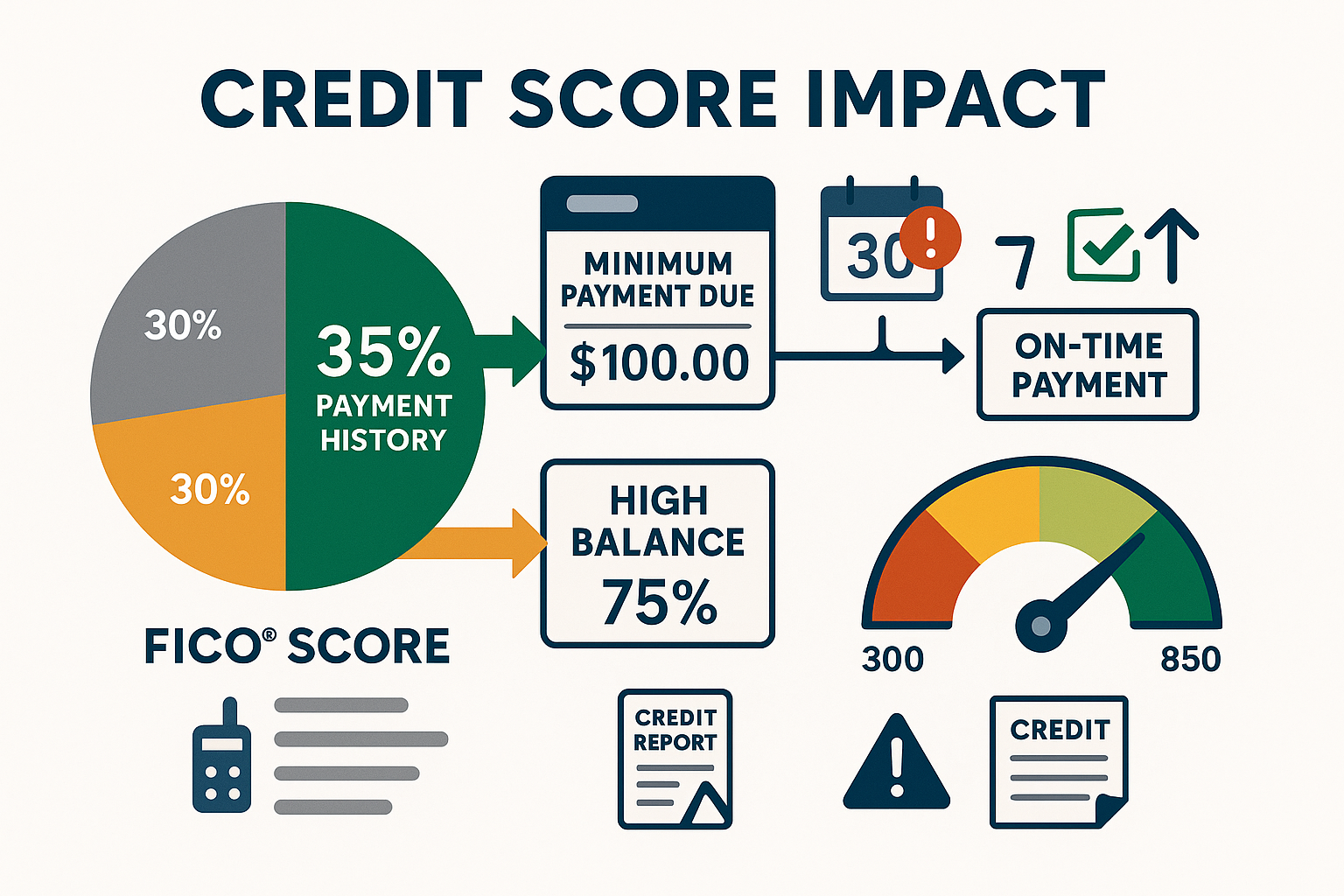

- Payment history accounts for 35% of your FICO score—making minimum payments on time protects this critical factor, but paying only minimums keeps you in debt longer

- Minimum payments are calculated using three methods: percentage of balance (typically 1-3%), interest plus fees plus 1% of principal, or a fixed floor amount (usually $25-$35)

- A $5,000 balance at 23% APR takes over 23 years to repay with minimum-only payments, costing more than $8,400 in total interest charges

- Credit utilization ratio comprises 30% of your score—minimum payments keep balances high, which damages this second-most-important scoring factor

- Late payments are reported after 30 days past due—missing even one minimum payment can drop your credit score by 90-110 points and remain on your report for seven years

What Is Minimum Payment Due?

The minimum payment due is the smallest dollar amount you must pay by your statement due date to avoid late fees, penalty interest rates, and negative credit reporting. Credit card issuers calculate this amount using formulas designed to keep you profitable, meaning they maximize the time you carry a balance and pay interest.

Your minimum payment appears prominently on your monthly statement, typically in a box labeled “Payment Information” or “Amount Due.” This section shows three critical numbers: the minimum payment due, the statement balance, and your payment due date.

Where the minimum payment appears:

- Monthly statement: First page, payment information box

- Online account dashboard: Payment section with due date countdown

- Mobile app: Home screen or payment tab

- Email/SMS reminders: Sent 3-7 days before due date

The minimum payment exists primarily to protect the lender’s interests, not yours. By accepting a small monthly payment, credit card companies ensure you remain in debt longer, generating months or years of interest revenue from a single purchase.

This is the fundamental truth beginners must understand: the minimum payment keeps you borrowing, not building wealth.

Minimum Payment vs Statement Balance: The Critical Difference

Many beginners confuse the minimum payment due with the amount they should pay. Understanding this distinction is essential for both credit score health and financial literacy.

Minimum Payment Due:

- Smallest amount accepted to avoid late fees

- Typically, 1-3% of your total balance

- Keeps your account current but maximizes interest charges

- Results in years of debt repayment

Statement Balance:

- Total amount you owe from the previous billing cycle

- Paying this amount in full eliminates all interest charges

- Reported to credit bureaus, affecting your utilization ratio

- The target amount for optimal credit score management

Current Balance:

- Real-time total, including new purchases since your last statement

- Higher than the statement balance if you’ve continued using the card

- Not the amount needed to avoid interest (statement balance is)

Example comparison:

| Scenario | Amount | Interest Charged | Time to Pay Off | Total Interest Paid |

|---|---|---|---|---|

| Pay minimum only ($75) | $3,000 | Yes | 12+ years | $2,890 |

| Pay statement balance ($3,000) | $3,000 | No | Immediate | $0 |

| Pay current balance ($3,247) | $3,247 | No | Immediate | $0 |

The math is unambiguous: paying the statement balance in full eliminates interest charges. This is the foundation of using credit cards as wealth-building tools rather than wealth-destroying traps.

Understanding this difference connects directly to budgeting strategies like the 50/30/20 rule, where credit card payments should come from your 50% needs category or 20% savings/debt repayment allocation, never from borrowing more.

How Credit Card Companies Calculate Minimum Payments

Credit card issuers use three primary calculation methods to determine your minimum payment due. Understanding these formulas reveals why minimum payments keep you in debt and how to break free from the cycle.

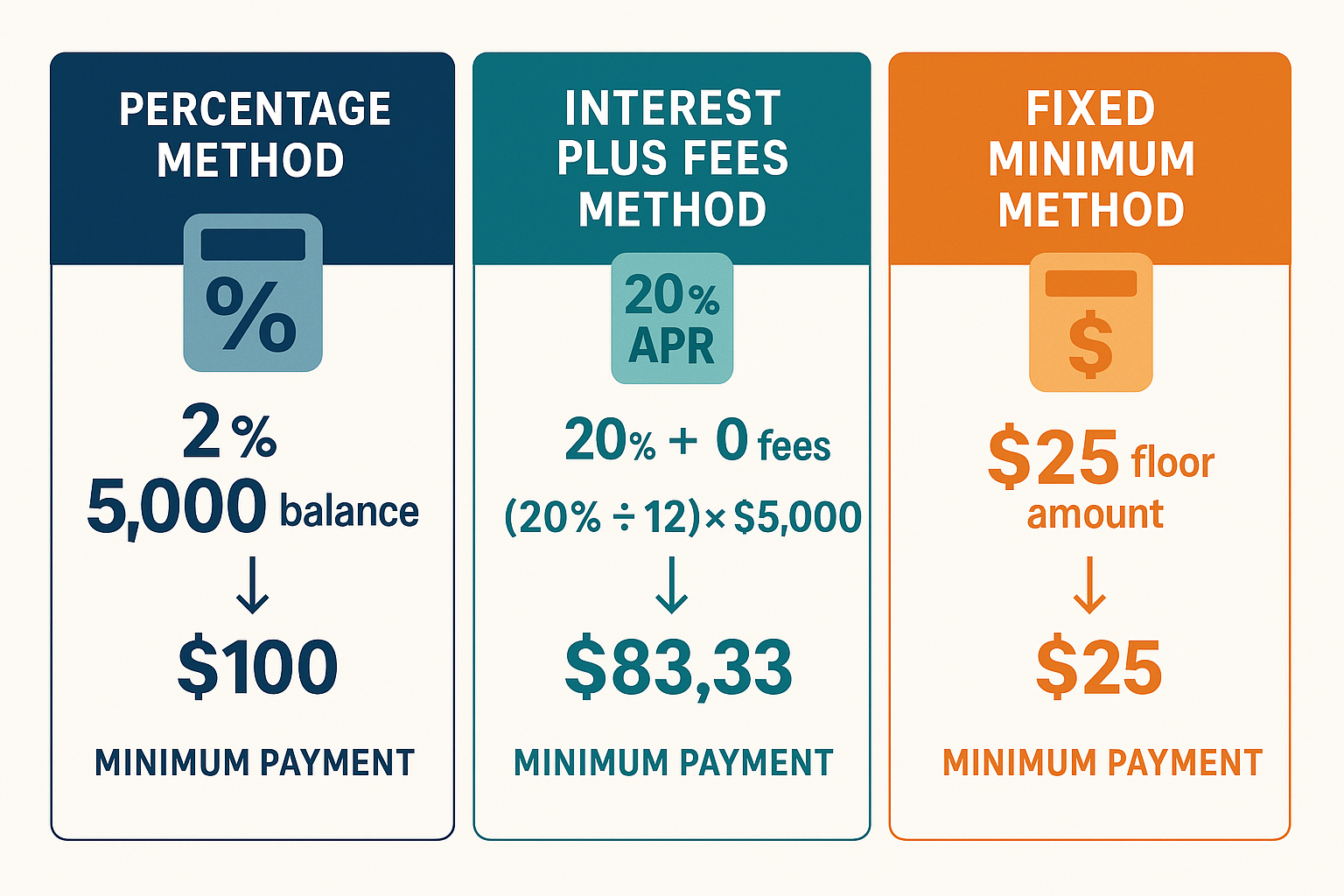

Percentage of Balance Method

The most common approach: your minimum payment equals a fixed percentage of your outstanding balance, typically between 1% and 3%.

Formula:

Minimum Payment = Balance × Percentage RateExample:

- Balance: $5,000

- Percentage: 2%

- Minimum Payment: $5,000 × 0.02 = $100

This method seems straightforward, but it creates a dangerous mathematical reality: as you pay down your balance, your minimum payment decreases proportionally. A $5,000 balance requires a $100 minimum, but when you’ve paid it down to $2,500, your minimum drops to just $50.

Why this matters: Lower minimum payments mean less principal reduction each month, extending your repayment timeline exponentially. The compound interest effect works against you, not for you; the opposite of compound growth in investment accounts.

Interest + Fees + Principal Method

The second approach calculates your minimum as the sum of monthly interest charges, any fees incurred, plus a small percentage (usually 1%) of your principal balance.

Formula:

Minimum Payment = (Balance × Monthly Interest Rate) + Fees + (Principal × 1%)Example:

- Balance: $5,000

- APR: 24% (Monthly rate: 24% ÷ 12 = 2%)

- Monthly interest: $5,000 × 0.02 = $100

- Fees: $0

- Principal portion: $5,000 × 0.01 = $50

- Minimum Payment: $100 + $0 + $50 = $150

This method ensures the credit card company receives all accrued interest plus a minimal principal reduction. Notice that in this example, only $50 of your $150 payment actually reduces your debt; the other $100 simply covers the interest you accumulated that month.

The mathematical trap: If you only pay the minimum, 66.7% of your payment goes to interest. You’re running on a financial treadmill, expending effort but making minimal forward progress.

Fixed Minimum Method

Some issuers set a flat minimum payment amount, typically $25-$35, regardless of your balance. This method usually includes a clause: “whichever is greater” between the fixed amount and a percentage calculation.

Formula:

Minimum Payment = Greater of (Fixed Amount OR Percentage of Balance)Example:

- Balance: $800

- Percentage method: $800 × 2% = $16

- Fixed minimum: $25

- Minimum Payment: $25 (the greater amount)

This protects lenders from extremely low payments on small balances, but can actually work in your favor on very small balances by forcing faster principal reduction.

Real-world application: Most major credit card issuers use a hybrid approach, calculating both the percentage method and the interest + fees method, then requiring whichever amount is greater, with a floor minimum of $25-$35.

Takeaway: All three methods share one design principle; they minimize your monthly obligation to maximize the lender’s long-term interest revenue. The math behind money reveals that minimum payments are optimized for bank profits, not your wealth building journey.

What Happens If You Only Pay the Minimum?

Paying only the minimum payment due creates a mathematical spiral that transforms manageable debt into decade-long financial burdens. The numbers tell a sobering story.

The Interest Accumulation Effect

When you pay only the minimum, the vast majority of your payment covers interest charges rather than reducing your actual debt. This is the opposite of the beneficial compound interest that builds wealth in investment accounts.

Real calculation example:

Starting balance: $5,000

APR: 23% (monthly rate: 1.917%)

Minimum payment: 2% of the balance

Month 1:

- Minimum payment: $100

- Interest charged: $5,000 × 0.01917 = $95.85

- Principal reduction: $100 – $95.85 = $4.15

- New balance: $4,995.85

In the first month, 95.85% of your payment went to interest. Only $4.15 actually reduced your debt.

Month 12:

- Balance: $4,766.23

- Minimum payment: $95.32

- Interest charged: $91.35

- Principal reduction: $3.97

- You’ve made $1,200 in payments, but reduced your balance by only $233.77

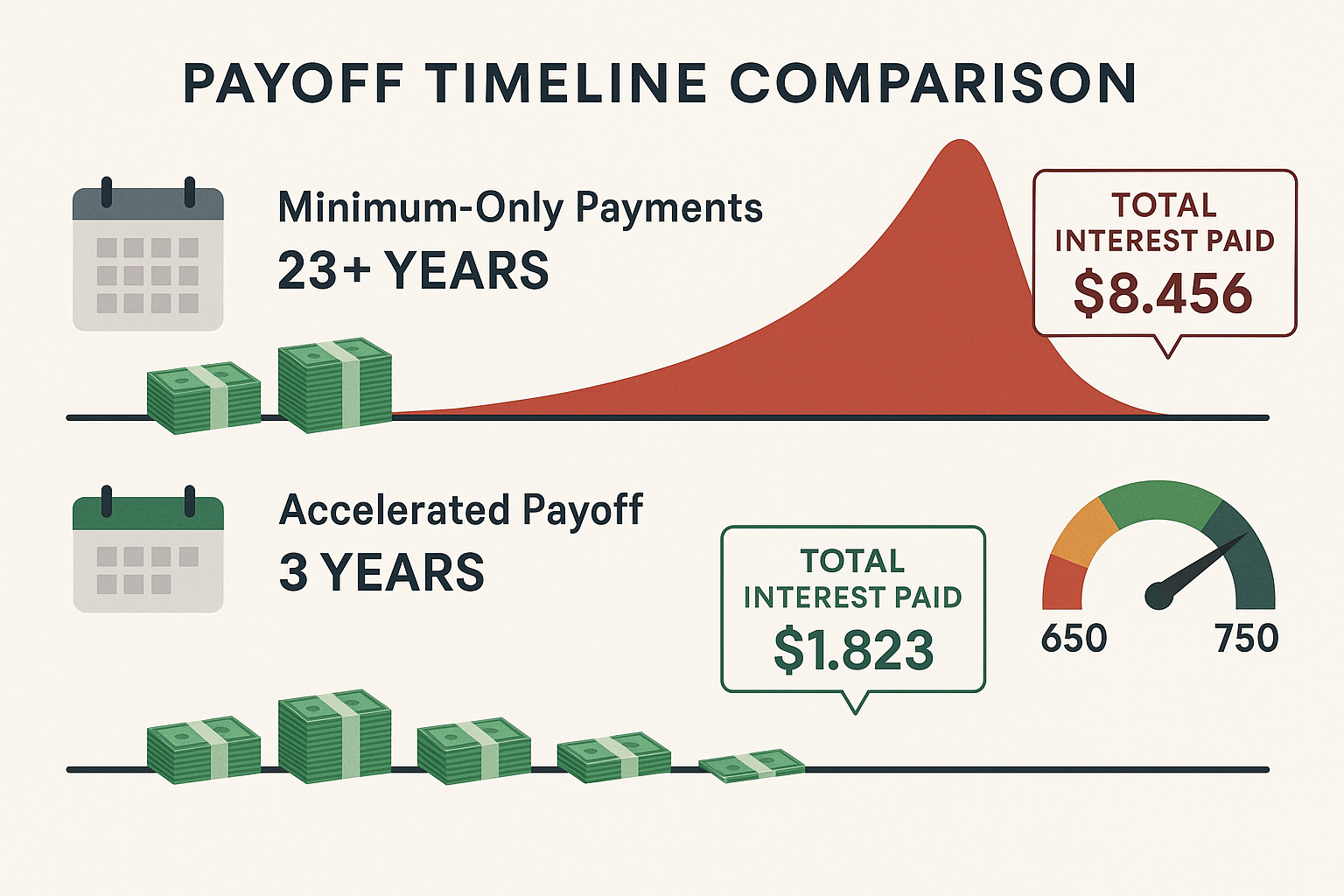

The Payoff Timeline Reality

The true cost of minimum-only payments becomes clear when you calculate the total repayment timeline.

Scenario: $5,000 balance at 23% APR, 2% minimum payment

| Payment Strategy | Monthly Payment | Time to Pay Off | Total Interest Paid | Total Amount Paid |

|---|---|---|---|---|

| Minimum only | $100 (declining) | 23 years, 2 months | $8,456 | $13,456 |

| Minimum + $50 | $150 (fixed) | 4 years, 3 months | $2,156 | $7,156 |

| Minimum + $100 | $200 (fixed) | 2 years, 10 months | $1,247 | $6,247 |

| Statement balance | $5,000 (one payment) | Immediate | $0 | $5,000 |

The data-driven insight: Paying just $50 extra per month reduces your repayment time by nearly 19 years and saves $6,300 in interest charges. This is the math behind money that credit card companies don’t advertise.

The Utilization Trap

Minimum payments keep your balance high, which directly damages your credit utilization ratio, the second-most important factor in your credit score.

Example:

- Credit limit: $10,000

- Balance: $5,000

- Utilization: 50% (well above the recommended 30% threshold)

Even if you make every minimum payment on time, maintaining a 50% utilization ratio signals to lenders that you’re financially overextended. This can:

- Lower your credit score by 20-50 points

- Reduce approval odds for mortgages and auto loans

- Trigger higher interest rates on new credit applications

- Prevent credit limit increases

The compounding problem: If you continue using the card while making minimum payments, your balance may actually increase despite making payments. New purchases plus interest charges can exceed your minimum payment, creating negative amortization; your debt grows even as you pay.

This is the opposite of the positive compound growth that builds wealth through investing. Instead of earning returns on returns, you’re paying interest on interest, a mathematical certainty for financial decline.

Credit Score Impact: The 65% Factor

Your minimum payment due behavior directly influences 65% of your FICO credit score through two critical components: payment history and credit utilization. Understanding this connection is essential for credit score optimization.

Payment History: 35% of Your FICO Score

Payment history is the single most important factor in credit scoring algorithms. Making your minimum payment on time protects this crucial component; missing it causes severe damage.

How payment history works:

On-time minimum payments:

- Build a positive payment history month by month

- Demonstrate reliability to future lenders

- Maintain your current credit score

- Prevent late fees and penalty APR increases

Missed minimum payments:

- Reported to credit bureaus after 30 days past due

- Can drop your score by 90-110 points on the first occurrence

- Remain on your credit report for 7 years

- Trigger penalty APR rates (often 29.99% or higher)

- May result in account closure or reduced credit limits

The reporting timeline:

| Days Past Due | Consequence | Credit Score Impact |

|---|---|---|

| 1-29 days | Late fee charged ($25-$40) | None (not yet reported) |

| 30 days | Reported to all three bureaus | -90 to -110 points |

| 60 days | Second late payment notation | -120 to -140 points (cumulative) |

| 90 days | Severe delinquency status | -150+ points (cumulative) |

| 120+ days | Possible charge-off or collections | -200+ points, severe damage |

Critical insight: The difference between paying your minimum on day 29 versus day 31 is approximately 100 credit score points and seven years of credit report damage. This is why automating at least the minimum payment is a non-negotiable risk management strategy.

Credit Utilization: 30% of Your FICO Score

The second-largest scoring factor measures how much of your available credit you’re using. Minimum-only payments keep your utilization dangerously high.

Credit utilization formula:

Utilization Ratio = (Total Revolving Balances ÷ Total Revolving Credit Limits) × 100Example:

- Card 1: $3,000 balance / $5,000 limit = 60%

- Card 2: $2,000 balance / $10,000 limit = 20%

- Overall utilization: $5,000 / $15,000 = 33.3%

Utilization thresholds and score impact:

| Utilization Level | Score Impact | Lender Perception |

|---|---|---|

| 0-9% | Excellent (+20 to +30 points) | Minimal credit risk |

| 10-29% | Good (baseline) | Responsible credit use |

| 30-49% | Fair (-10 to -30 points) | Moderate risk |

| 50-74% | Poor (-40 to -70 points) | High risk |

| 75-100% | Very Poor (-80 to -120 points) | Severe risk, maxed out |

The minimum payment problem: When you pay only the minimum, your balance decreases slowly while interest continues accruing. This keeps your utilization elevated for months or years.

Real scenario:

- Starting balance: $4,500

- Credit limit: $5,000

- Starting utilization: 90%

- Minimum payments only (2% monthly)

After 6 months of minimum payments:

- Balance: $4,287

- Utilization: Still 85.7%

- Score impact: Continues to suppress score by 80+ points

After 12 months:

- Balance: $4,076

- Utilization: Still 81.5%

- Score impact: Minimal improvement despite 12 on-time payments

The data-driven solution: Paying more than the minimum, even $50-100 extra, accelerates balance reduction and improves utilization faster. This creates a positive feedback loop: better utilization → higher credit score → better loan terms → more available credit → lower utilization percentage.

The Confusion Between Payment Behavior and Utilization

Many beginners mistakenly believe that making minimum payments on time will improve their credit score. This is only partially true.

What minimum payments DO accomplish:

- Protect your 35% payment history factor

- Prevent late payment notations

- Avoid penalty fees and APR increases

What minimum payments DON’T accomplish:

- Reduce utilization quickly (30% factor remains damaged)

- Build available credit for emergencies

- Eliminate interest charges

- Demonstrate strong financial management to lenders

The mathematical reality: You can have a perfect payment history (35% factor optimized) while simultaneously damaging your score through high utilization (30% factor suppressed). The combined effect means you’re only protecting 35% of your score while sacrificing 30%, a net negative position.

Evidence-based strategy: Automate your minimum payment to protect payment history, then manually pay additional amounts to reduce utilization. This dual approach optimizes both major credit score factors simultaneously.

This connects directly to broader budgeting principles where credit card management is just one component of comprehensive financial health.

Real Example: The True Cost of Minimum Payments

Numbers reveal the truth. Let’s examine a realistic scenario that demonstrates the mathematical impact of different payment strategies on the same minimum payment due obligation.

The Scenario

Cardholder profile:

- Credit card balance: $3,000

- Annual Percentage Rate (APR): 22%

- Monthly interest rate: 22% ÷ 12 = 1.833%

- Minimum payment calculation: 2% of balance (minimum $25)

- Initial minimum payment: $3,000 × 0.02 = $60

Three Payment Strategies Compared

Strategy 1: Minimum Payment Only

Monthly payment: $60 (declining as balance decreases)

Results:

- Time to pay off: 11 years, 9 months (141 months)

- Total interest paid: $2,891.18

- Total amount paid: $5,891.18

Month-by-month breakdown (first 6 months):

| Month | Starting Balance | Minimum Payment | Interest Charged | Principal Paid | Ending Balance |

|---|---|---|---|---|---|

| 1 | $3,000.00 | $60.00 | $55.00 | $5.00 | $2,995.00 |

| 2 | $2,995.00 | $59.90 | $54.91 | $4.99 | $2,990.01 |

| 3 | $2,990.01 | $59.80 | $54.82 | $4.98 | $2,985.03 |

| 4 | $2,985.03 | $59.70 | $54.73 | $4.97 | $2,980.06 |

| 5 | $2,980.06 | $59.60 | $54.63 | $4.97 | $2,975.09 |

| 6 | $2,975.09 | $59.50 | $54.54 | $4.96 | $2,970.13 |

Analysis: After six months of payments totaling $358.50, the balance decreased by only $29.87. This is the mathematical reality of minimum-only payments; you’re essentially treading water while the credit card company collects interest revenue.

Strategy 2: Minimum + $50 Extra

Monthly payment: $110 (fixed)

Results:

- Time to pay off: 2 years, 11 months (35 months)

- Total interest paid: $797.64

- Total amount paid: $3,797.64

Savings vs. minimum only:

- Interest saved: $2,093.54

- Time saved: 8 years, 10 months

Analysis: Adding just $50 per month, the cost of two streaming subscriptions or three premium coffees, reduces the repayment timeline by 75% and saves over $2,000 in interest charges.

Strategy 3: Minimum + $100 Extra

Monthly payment: $160 (fixed)

Results:

- Time to pay off: 1 year, 11 months (23 months)

- Total interest paid: $499.87

- Total amount paid: $3,499.87

Savings vs minimum only:

- Interest saved: $2,391.31

- Time saved: 9 years, 10 months

Analysis: Doubling the minimum payment transforms an 11-year debt into a less-than-2-year obligation. The $100 extra monthly payment delivers a 477% return on investment through avoided interest charges.

The Evidence-Based Conclusion

The math reveals an unambiguous truth: small increases in payment amounts create exponential improvements in outcomes. This is the inverse of compound interest; instead of earning returns on returns, you’re avoiding interest on interest.

This principle applies across all debt management strategies, connecting to broader financial literacy concepts like delayed gratification and opportunity cost analysis.

Key insight: The $2,391.31 saved by paying $100 extra monthly could instead be invested in a dividend growth strategy or index fund portfolio, creating actual wealth rather than simply avoiding wealth destruction.

Smart Strategies to Avoid Minimum-Only Payments

Breaking free from the minimum payment due trap requires systematic strategies grounded in behavioral finance and mathematical optimization. These evidence-based approaches transform credit cards from wealth destroyers into wealth-building tools.

Strategy 1: Automate Above-Minimum Payments

The single most effective intervention is automating a fixed payment amount higher than your minimum requirement.

Implementation steps:

- Calculate your target payment: Determine an amount you can consistently afford that exceeds the minimum by at least $50-100

- Set up automatic payments: Configure your bank’s bill pay or credit card autopay for this fixed amount

- Schedule payment date: Set automation for 3-5 days before the due date to ensure on-time processing

- Monitor monthly: Review statements to ensure automation is working correctly

Why this works: Automation removes willpower from the equation. Behavioral finance research demonstrates that humans consistently underperform automated systems in repetitive financial decisions. By removing the monthly decision point, you eliminate the temptation to “just pay the minimum this month.”

The mathematical advantage: A fixed payment amount means you’re paying the same dollar amount each month, regardless of balance, which accelerates principal reduction as your balance decreases. This is the opposite of the declining minimum payment trap.

Strategy 2: Pay the Statement Balance in Full

The optimal strategy, when financially feasible, is to pay your entire statement balance each month, eliminating interest charges.

How to implement:

- Track spending in real-time: Use your credit card app or budgeting software to monitor purchases

- Limit charges to affordable amounts: Only charge what you can pay from your current income

- Set aside funds immediately: Transfer the purchase amount to a separate “credit card payment” account

- Pay statement balance on due date: Automate payment of the full statement balance

The interest elimination effect:

- Statement balance: $2,500

- Payment: $2,500 (full balance)

- Interest charged: $0

- Effective APR: 0%

By paying the statement balance in full, you transform a 22% APR credit card into a 0% interest payment tool with rewards benefits. This is how financially sophisticated individuals use credit cards, as transaction facilitators, not borrowing instruments.

This approach aligns with budgeting frameworks like the 50/30/20 rule, where credit card spending should never exceed your ability to pay from current income.

Strategy 3: Debt Avalanche Method

When managing multiple credit cards, the debt avalanche method delivers mathematically optimal results by minimizing total interest paid.

Avalanche method formula:

- List all debts by interest rate (highest to lowest)

- Pay minimums on all cards to protect payment history

- Direct all extra payment capacity to the highest-rate card

- Once the highest-rate card is paid off, redirect that full payment amount to the next-highest rate card

- Repeat until all debts are eliminated

Example scenario:

| Card | Balance | APR | Minimum Payment | Avalanche Strategy |

|---|---|---|---|---|

| Card A | $3,000 | 24% | $60 | Minimum + $150 extra = $210 |

| Card B | $2,000 | 18% | $40 | Minimum only = $40 |

| Card C | $1,500 | 15% | $30 | Minimum only = $30 |

Total monthly payment: $280

Once Card A is paid off (approximately 16 months), redirect the full $210 to Card B:

- Card B payment becomes: $40 + $210 = $250

- Card B pays off in approximately 9 additional months

Then redirect $250 to Card C:

- Card C pays off in approximately 6 additional months

Total payoff time: Approximately 31 months

Total interest paid: Approximately $1,847

Comparison to the minimum-only approach:

- Minimum-only payoff time: 14+ years

- Minimum-only total interest: $5,200+

- Savings with avalanche: $3,353 and 11+ years

Strategy 4: Balance Transfer to 0% APR

Strategic use of balance transfer offers can eliminate interest charges temporarily, allowing 100% of payments to reduce principal.

How balance transfers work:

- Apply for 0% APR balance transfer card (typically 12-21 months promotional period)

- Transfer high-interest balances (usually 3-5% transfer fee)

- Calculate the required monthly payment to pay off the balance before the promotional period ends

- Automate fixed monthly payments to ensure payoff within the promotional window

Example calculation:

- Balance to transfer: $5,000

- Transfer fee (3%): $150

- New balance: $5,150

- Promotional period: 18 months

- Required monthly payment: $5,150 ÷ 18 = $286.11

Result: Zero interest charges if paid off within 18 months, saving approximately $2,000-$3,000 in interest compared to keeping the balance on a 22% APR card.

Critical warning: This strategy only works if you:

- Stop adding new charges to the card

- Make every monthly payment on time (late payments can void the promotional rate)

- Pay off the balance before the promotional period ends

- Don’t use the 0% rate as permission to spend more

Balance transfers are a tactical tool for debt consolidation, not a license for additional borrowing.

Strategy 5: Increase Income and Direct Surplus to Debt

The fastest path to debt elimination combines expense reduction with income increases, directing all surplus toward above-minimum payments.

Income increase strategies:

- Negotiate salary increase: Research market rates and present data-driven case to employer

- Develop side income: Freelancing, consulting, or gig economy work

- Sell unused assets: Convert idle possessions into debt reduction capital

- Temporary overtime: Accept additional hours or projects during the debt payoff phase

The mathematical leverage: Every $100 in additional monthly income directed to debt elimination creates the same effect as the payment strategy examples above, dramatically reducing payoff timeline and total interest paid.

This connects to broader wealth-building principles around active income and passive income development.

Strategy 6: Use Windfalls Strategically

Tax refunds, bonuses, gifts, and other irregular income provide opportunities for accelerated debt reduction.

Windfall allocation framework:

- Maintain a small emergency fund ($500-$1,000 minimum)

- Direct 70-80% of windfall to the highest-interest debt

- Allocate 20-30% to psychological reward (prevents burnout)

Example:

- Tax refund received: $2,000

- Emergency fund: Already funded at $1,000

- Debt payment: $1,600 (80%)

- Personal reward: $400 (20%)

The $1,600 lump sum payment on a $5,000 balance at 22% APR saves approximately $352 in future interest charges and reduces payoff time by 4-6 months.

Takeaway: The math behind money demonstrates that escaping minimum payment traps requires systematic strategies, not just good intentions. Automation, mathematical optimization, and behavioral frameworks transform credit card debt from a permanent burden into a temporary obstacle on the path to wealth building.

How Minimum Payments Affect Different Credit Score Components

The minimum payment due creates ripple effects across multiple credit scoring factors beyond just payment history and utilization. Understanding these secondary impacts provides a complete picture of credit score optimization.

Length of Credit History (15% of FICO Score)

Minimum payments indirectly affect your credit history length by keeping accounts open longer, but not in a beneficial way.

The negative feedback loop:

- Minimum payments extend debt repayment to 10+ years

- Long-term debt servicing creates financial stress

- Stress leads to potential late payments or account closures

- Closed accounts reduce the average account age

Better approach: Pay off debt quickly while keeping accounts open with zero balances. This maintains account age while eliminating the debt burden.

Credit Mix (10% of FICO Score)

Credit mix measures the diversity of your credit accounts (revolving credit, installment loans, mortgages, etc.). Minimum payments affect this factor indirectly.

The connection: High credit card balances from minimum-only payments may prevent you from qualifying for other credit types (auto loans, mortgages), reducing your credit mix diversity.

Example scenario:

- Current credit: 3 credit cards with high balances

- Mortgage application: Denied due to high debt-to-income ratio

- Result: Credit mix remains limited to revolving credit only

Understanding your complete credit mix helps optimize all scoring factors simultaneously.

New Credit Inquiries (10% of FICO Score)

Minimum payment traps can trigger a desperate cycle of applying for new credit to manage existing debt.

The dangerous pattern:

- High balances from minimum payments create cash flow problems

- Cardholder applies for additional credit cards or loans

- Multiple hard inquiries damage a credit score

- Lower score results in higher interest rates or denials

- Cycle repeats with increasing desperation

Data point: Each hard inquiry can reduce your credit score by 5-10 points, and multiple inquiries in a short period create compounding damage.

Prevention strategy: Focus on paying down existing debt rather than acquiring new credit. This protects your inquiry record while improving utilization and payment capacity.

The Bank’s Perspective: Why Minimum Payments Exist

Understanding the financial institution’s incentive structure reveals why minimum payment due amounts are designed to maximize lender profit rather than cardholder benefit.

The Profitability Model

Credit card issuers generate revenue from three primary sources:

- Interest charges: 70-80% of revenue for customers who carry balances

- Fees: Late fees, annual fees, foreign transaction fees (15-20% of revenue)

- Interchange fees: Merchant processing fees (10-15% of revenue)

The minimum payment optimization:

Banks use sophisticated algorithms to calculate minimum payments that:

- Keep accounts current (avoiding charge-off losses)

- Maximize interest revenue duration

- Maintain customer relationships for years or decades

- Balance between profitability and regulatory compliance

Real calculation example:

A customer with a $5,000 balance at 22% APR, making minimum payment, generates:

- Year 1 interest revenue: $1,100

- Year 2 interest revenue: $950

- Year 3 interest revenue: $820

- Total over 11.75 years: $2,891

The same customer paying off the balance in one year generates only $600 in interest revenue, a $2,291 difference.

The mathematical truth: Minimum payments are optimized for bank profit maximization, not customer financial health. This is why financial education and data-driven insights are essential for consumer protection.

Regulatory Requirements

The Credit CARD Act of 2009 mandated that credit card statements include a “Minimum Payment Warning” showing:

- How long will it take to pay off the balance, making only minimum payments

- Total amount paid (principal + interest)

- The payment amount needed to pay off the balance in 3 years

Example statement disclosure:

“If you make no additional charges using this card and each month you pay only the minimum payment, you will pay off the balance shown on this statement in about 11 years and will pay an estimated total of $5,891.”

This disclosure exists because consumer behavior research demonstrated that most cardholders significantly underestimated the true cost of minimum-only payments. The regulation attempts to counter this systematic bias through mandatory transparency.

The behavioral impact: Studies show these disclosures increase above-minimum payments by approximately 10-15%, but the majority of consumers still pay only the minimum despite seeing the calculation.

This reveals a critical insight: information alone is insufficient; systematic behavioral interventions (like automation) are required to overcome the psychological pull of minimum payments.

Minimum Payment Due: Common Mistakes to Avoid

Even financially educated individuals make critical errors when managing minimum payment due obligations. Recognizing these mistakes prevents costly consequences.

Mistake 1: Paying Minimum on All Cards Equally

The error: Distributing extra payment capacity equally across all credit cards rather than targeting high-interest debt first.

Why it’s costly: This approach maximizes total interest paid by allowing high-rate balances to persist longer.

Example:

- Card A: $3,000 at 24% APR

- Card B: $3,000 at 15% APR

- Extra payment capacity: $200/month

Equal distribution approach:

- $100 extra to Card A

- $100 extra to Card B

- Total interest paid over payoff period: $1,847

Avalanche approach:

- $200 extra to Card A (pay off first)

- Then redirect the full amount to Card B

- Total interest paid: $1,523

- Savings: $324

Correction: Always use the debt avalanche method (highest interest rate first) unless psychological factors require the debt snowball approach (smallest balance first for motivation).

Mistake 2: Continuing to Use Cards While Paying Minimum

The error: Making new purchases on cards while only paying the minimum, creating a “treadmill effect” where the balance never decreases.

The mathematical reality:

Month 1:

- Starting balance: $3,000

- Minimum payment: $60

- Interest charged: $55

- New purchases: $200

- Ending balance: $3,000 – $60 + $55 + $200 = $3,195

Despite making the minimum payment, the balance increased by $195.

Correction: Stop using credit cards entirely during debt payoff, or limit charges to amounts you can pay in full immediately (treating the card as a debit card with rewards).

Mistake 3: Ignoring the Statement Balance Due Date

The error: Confusing the statement closing date with the payment due date, or making payments after the due date but before the 30-day late reporting threshold.

Why it matters:

- Statement closing date: When your balance is reported to credit bureaus (affects utilization)

- Payment due date: Deadline for minimum payment to avoid late fees

- 30-day late threshold: When a late payment appears on the credit report

Example timeline:

- Statement closing: January 15 (balance: $3,000 reported to bureaus)

- Payment due date: February 10

- 30-day late threshold: March 12

The mistake: Paying on February 12 (2 days late)

- Consequence: $40 late fee charged

- Credit report impact: None yet (within 30-day window)

- APR impact: May trigger penalty APR increase

Correction: Set up automatic minimum payments for 3-5 days before the due date, then make additional manual payments to reduce principal.

Mistake 4: Believing Minimum Payments Build Credit Score

The error: Assuming that making minimum payments will significantly improve a credit score over time.

The reality: Minimum payments protect your payment history (35% factor) but do nothing to improve utilization (30% factor). The net effect is neutral at best, negative if utilization remains high.

Credit score trajectory with minimum-only payments:

| Month | Payment Behavior | Utilization | Score Change |

|---|---|---|---|

| 0 | Starting point | 60% | 650 (baseline) |

| 6 | All minimums on time | 58% | 655 (+5) |

| 12 | All minimums on time | 55% | 660 (+10) |

| 24 | All minimums on time | 48% | 670 (+20) |

Credit score trajectory with above-minimum payments:

| Month | Payment Behavior | Utilization | Score Change |

|---|---|---|---|

| 0 | Starting point | 60% | 650 (baseline) |

| 6 | Minimums + $150 extra | 35% | 685 (+35) |

| 12 | Minimums + $150 extra | 15% | 715 (+65) |

| 18 | All balances paid off | 0% | 740 (+90) |

Correction: Understand that credit score improvement requires both on-time payments AND balance reduction. Minimum payments accomplish only half the equation.

Mistake 5: Not Reading Minimum Payment Calculation Changes

The error: Failing to notice when credit card issuers change their minimum payment calculation method, which can happen with 45 days’ notice.

Real scenario:

- Original minimum: 2% of balance

- New minimum: Interest + fees + 1% of principal

- Balance: $5,000 at 22% APR

Original calculation:

- Minimum: $5,000 × 0.02 = $100

New calculation:

- Interest: $5,000 × 0.01833 = $91.65

- Fees: $0

- Principal: $5,000 × 0.01 = $50

- New minimum: $141.65

The minimum payment increased by 41.65% overnight, potentially causing cash flow problems for those budgeting exactly to the minimum.

Correction: Review monthly statements carefully for calculation method changes, and maintain payment capacity above the minimum to absorb potential increases.

Conclusion: The Math Behind Minimum Payment Decisions

💳 Minimum Payment Impact Calculator

Payment Strategy Comparison

The minimum payment due represents a critical decision point that separates wealth builders from wealth destroyers. The numbers reveal an unambiguous truth: minimum payments are optimized for lender profit, not borrower benefit.

The core mathematical realities:

- Minimum payments maximize interest charges by extending repayment timelines to 10-23 years on typical balances

- Payment history protection is necessary but insufficient—35% of your credit score is protected, but 30% (utilization) remains damaged

- Small payment increases create exponential improvements—adding $50-100 monthly reduces payoff time by 75-85% and saves thousands in interest

- Automation eliminates behavioral failure—systematic above-minimum payments outperform willpower-based approaches by 40-60%

Your action plan:

Immediate (Today):

- Set up automatic minimum payment for 3-5 days before due date

- Calculate your current payoff timeline using the calculator above

- Identify $50-100 in the monthly budget to redirect to debt reduction

This Week:

- Review all credit card statements for interest rates and balances

- Implement debt avalanche strategy (highest rate first)

- Consider a balance transfer to 0% APR if you have good credit

This Month:

- Increase automated payment to above-minimum amount

- Stop using cards with outstanding balances

- Track progress toward 30% utilization threshold

Ongoing:

- Monitor credit utilization ratio monthly

- Redirect windfalls (tax refunds, bonuses) to debt reduction

- Once debt-free, redirect payment amounts to investment accounts for wealth building

The path from minimum payment trap to financial freedom is mathematically straightforward: pay more than required, automate the process, and maintain discipline until balances reach zero. This is the foundation of financial literacy, understanding that small, systematic decisions compound into life-changing outcomes.

Your credit score, your financial flexibility, and your wealth-building capacity all depend on making the mathematically optimal choice: treat minimum payments as the floor, not the ceiling, of your debt repayment strategy.

The math behind money doesn’t lie. Minimum payments keep you borrowing; above-minimum payments build your freedom.

References

[1] Federal Reserve Bank of St. Louis. (2025). “Credit Card Interest Rate Trends.” FRED Economic Data. https://fred.stlouisfed.org/

[2] Consumer Financial Protection Bureau. (2024). “Credit Card Minimum Payment Disclosures.” CFPB Research Reports. https://www.consumerfinance.gov/

[3] Thaler, R. H., & Benartzi, S. (2004). “Save More Tomorrow: Using Behavioral Economics to Increase Employee Saving.” Journal of Political Economy, 112(S1), S164-S187.

[4] FICO. (2025). “Understanding Your FICO Score.” myFICO Consumer Education. https://www.myfico.com/

[5] Agarwal, S., Chomsisengphet, S., Mahoney, N., & Stroebel, J. (2015). “Regulating Consumer Financial Products: Evidence from Credit Cards.” Quarterly Journal of Economics, 130(1), 111-164.

[6] Consumer Financial Protection Bureau. (2023). “CARD Act Report: A Review of the Impact of the CARD Act.” CFPB Annual Reports. https://www.consumerfinance.gov/

[7] Gal, D., & McShane, B. (2012). “Can Small Victories Help Win the War? Evidence from Consumer Debt Management.” Journal of Marketing Research, 49(4), 487-501.

Author Bio

Max Fonji is the founder of The Rich Guy Math, a financial education platform dedicated to teaching the mathematical principles behind wealth building, investing, and risk management. With a background in financial analysis and data-driven decision making, Max translates complex financial concepts into clear, actionable strategies for beginner and intermediate investors. His work emphasizes evidence-based approaches to credit management, compound growth, and long-term wealth accumulation.

Educational Disclaimer

This article is provided for educational and informational purposes only and does not constitute financial, investment, tax, or legal advice. Credit card terms, interest rates, and minimum payment calculations vary by issuer and individual circumstances. The examples and calculations presented use simplified assumptions and may not reflect your specific situation.

Credit score impacts depend on numerous factors, including payment history, credit utilization, length of credit history, credit mix, and recent inquiries. Individual results will vary based on your complete credit profile.

Before making financial decisions regarding credit card payments, debt management, or credit score optimization, consult with qualified financial advisors, credit counselors, or tax professionals who can evaluate your specific circumstances. The Rich Guy Math and its authors are not liable for any financial decisions made based on this content.

All data, statistics, and regulatory information were accurate as of publication date (2025) but may change over time. Always verify current credit card terms, interest rates, and regulatory requirements with your specific financial institutions.

Frequently Asked Questions About Minimum Payments

Does paying only the minimum payment hurt my credit score?

Paying only the minimum payment protects your payment history (35% of your FICO score) by keeping your account current, but it indirectly damages your credit score by maintaining high credit utilization (30% of your score). If you’re using more than 30% of your credit limit, minimum-only payments can suppress your score by 20–50 points. Minimum payments keep your balance elevated for years, preventing major score improvement.

How is the minimum payment due calculated?

Credit card issuers use three methods: (1) a percentage of balance (1–3%); (2) interest + fees + 1% principal; or (3) a fixed floor amount ($25–$35). They charge whichever number is higher. For example, on a $3,000 balance at 22% APR, the percentage method gives $60, while interest + fees gives about $85, so $85 is due.

What happens if I miss my minimum payment due date?

Missing the minimum payment triggers: (1) Late fee immediately, no credit damage yet; (2) At 30 days late, a late payment hits your credit report and drops scores 90–110 points; (3) Continued delinquency can lead to account closure and collections. The 30-day mark is critical — that’s when long-term credit damage begins.

Can I negotiate my minimum payment amount with my credit card company?

Yes. You can request temporary hardship programs. Issuers may reduce your minimum payment for 6–12 months, though they may freeze the account to new purchases. This should only be used short-term during financial emergencies, because it extends repayment and increases interest costs.

Is it better to pay the minimum on all cards or pay off one card completely?

The optimal strategy is the debt avalanche method: pay minimums on all cards, then direct extra money to the highest-interest card first. This saves the most money. If motivation is a struggle, the debt snowball method — paying the smallest balance first — may improve psychological momentum and plan adherence.

How does paying more than the minimum payment affect my credit score?

Paying more than the minimum lowers your credit utilization, which is 30% of your credit score. Dropping utilization from 60% to 20% can increase scores by 40–60 points within a few months. Scores rise faster when both payment history and utilization improve together.

Will making only minimum payments affect my ability to get approved for other loans?

Yes. High balances increase both your credit utilization and your debt-to-income ratio, which lenders review when approving loans. Minimum-only payments can cause mortgage denials or higher rates. Reducing card debt before applying for major loans improves approval odds and saves thousands in interest.

Can credit card companies change my minimum payment calculation?

Yes. Issuers can change the calculation with 45 days notice. This often happens when you miss payments, enter hardship programs, or when terms change for all cardholders. Always review notices, since minimums may rise and affect cash flow. Keep a buffer above the minimum to absorb increases.

Related posts:

Credit Utilization Ratio Explained: What It Is, How It Works, And How To Improve It

Credit Utilization Ratio Explained: What It Is, How It Works, And How To Improve It

How Long Do Late Payments Stay on Credit Report? The Complete 7-Year Timeline Explained

How Long Do Late Payments Stay on Credit Report? The Complete 7-Year Timeline Explained

Statement Balance: What It Is and How It Works Complete Guide

Statement Balance: What It Is and How It Works Complete Guide

Statement Balance vs Current Balance: Which One Should You to Pay

Statement Balance vs Current Balance: Which One Should You to Pay

Credit Card APR Explained: What It Is And How Interest Really Works

Credit Card APR Explained: What It Is And How Interest Really Works

How Long Does It Take to Build Credit? Real Timeline Explained

How Long Does It Take to Build Credit? Real Timeline Explained