Building wealth through passive income streams has become a cornerstone of modern financial planning, and dividend ETFs represent one of the most accessible paths for beginners. Imagine receiving quarterly payments simply for owning shares in a diversified basket of dividend-paying companies; this is the fundamental promise of Passive Income with Dividend ETFs.

For a broader perspective on managing investments and choosing the right assets, see our guide on complete investing guide.

These investment vehicles combine the income-generating power of dividend stocks with the diversification benefits of exchange-traded funds, creating a compelling opportunity for investors seeking steady cash flow. Unlike the volatility of growth stocks or the complexity of real estate investing, dividend ETFs offer a straightforward approach to generating passive income while building long-term wealth.

Key Takeaways

- Dividend ETFs provide instant diversification across dozens or hundreds of dividend-paying companies, reducing single-stock risk while generating regular income

- Compound growth accelerates wealth building when dividends are reinvested, with the math behind money showing exponential growth over time

- Lower costs and tax efficiency make ETFs superior to mutual funds for most dividend investors, with expense ratios often below 0.20%

- Dollar-cost averaging into dividend ETFs smooths market volatility while building positions systematically

- Starting with $1,000-$5,000 provides sufficient capital to begin building meaningful passive income streams through dividend ETFs

Understanding the Math Behind Dividend ETFs

Dividend ETFs operate on a simple yet powerful mathematical principle: they collect dividends from underlying holdings and distribute them proportionally to shareholders. When an investor owns 100 shares of a dividend ETF yielding 3.5%, and the ETF trades at $50 per share, the annual dividend income equals $175 ($5,000 × 0.035).

The compound growth potential emerges when these dividends are reinvested. A $10,000 investment in a dividend ETF yielding 4% annually, with dividend growth of 6% per year, grows to approximately $43,200 over 20 years through reinvestment alone.

The Power of Dividend Reinvestment:

- Year 1: $10,000 × 4% = $400 in dividends

- Year 5: $12,625, generating $531 in dividends

- Year 10: $17,90,8 generating $895 in dividends

- Year 20: $43,200 generating $2,304 in dividends

This exponential growth demonstrates why compound interest forms the foundation of wealth building through dividend investing.

Risk Management Through Diversification

Individual dividend stocks carry company-specific risks; a single firm might cut or eliminate its dividend during economic downturns. Dividend ETFs mitigate this risk by holding 50-500 different companies across various sectors and industries.

Consider the 2008 financial crisis: while individual bank stocks like Citigroup eliminated dividends, diversified dividend ETFs maintained distributions by offsetting losses with stable performers in utilities, consumer staples, and healthcare sectors.

Key Risk Metrics to Monitor:

- Standard deviation: Measures price volatility (lower is better for income investors)

- Maximum drawdown: Largest peak-to-trough decline during market stress

- Beta: Sensitivity to market movements (dividend ETFs typically have a beta below 1.0)

- Sector concentration: Percentage allocated to any single industry

Building Your Passive Income with Dividend ETFs Strategy

Creating sustainable passive income requires a systematic approach that balances yield, growth, and risk management. The most successful dividend ETF strategies focus on total return rather than chasing the highest current yields.

The Total Return Framework

Total return combines dividend income with capital appreciation. A dividend ETF yielding 2.5% with 8% annual price appreciation delivers 10.5% total return, superior to a 6% yielding ETF with flat price performance.

Total Return = Dividend Yield + Capital Appreciation + Dividend Growth

This framework explains why dividend growth stocks often outperform high-yield investments over long periods. Companies that consistently increase dividends typically demonstrate strong fundamentals, leading to both rising share prices and growing income streams.

Portfolio Allocation Strategies

The optimal allocation to dividend ETFs depends on age, risk tolerance, and income needs. Financial advisors commonly recommend the following frameworks:

Conservative Approach (Age 50+):

- 40-60% dividend ETFs

- 20-30% bond ETFs

- 10-20% growth ETFs

- 5-10% international exposure

Balanced Approach (Age 30-50):

- 30-40% dividend ETFs

- 40-50% growth investments

- 10-20% bonds

- 10-15% international

Aggressive Growth (Age 20-30):

- 20-30% dividend ETFs

- 60-70% growth investments

- 5-10% bonds

- 10-15% international

These allocations should align with your overall budgeting strategy and emergency fund requirements.

💰 Dividend ETF Income Calculator

Top Dividend ETFs for Passive Income Generation

Selecting the right dividend ETFs requires analyzing multiple factors beyond just yield. The best dividend ETFs combine sustainable yields, low costs, and consistent performance across market cycles.

Core Dividend ETF Categories

Broad Market Dividend ETFs provide exposure to hundreds of dividend-paying companies across all sectors. These funds typically yield 2-4% while offering moderate growth potential.

High Dividend Yield ETFs focus on companies paying above-average dividends, often yielding 4-8%. However, higher yields may indicate financial stress or unsustainable payout ratios.

Dividend Growth ETFs target companies with histories of increasing dividends annually. These funds often start with lower yields (2-3%) but provide inflation protection through growing income streams.

Dividend Aristocrat ETFs hold S&P 500 companies that have increased dividends for 25+ consecutive years. This elite group demonstrates exceptional dividend reliability.

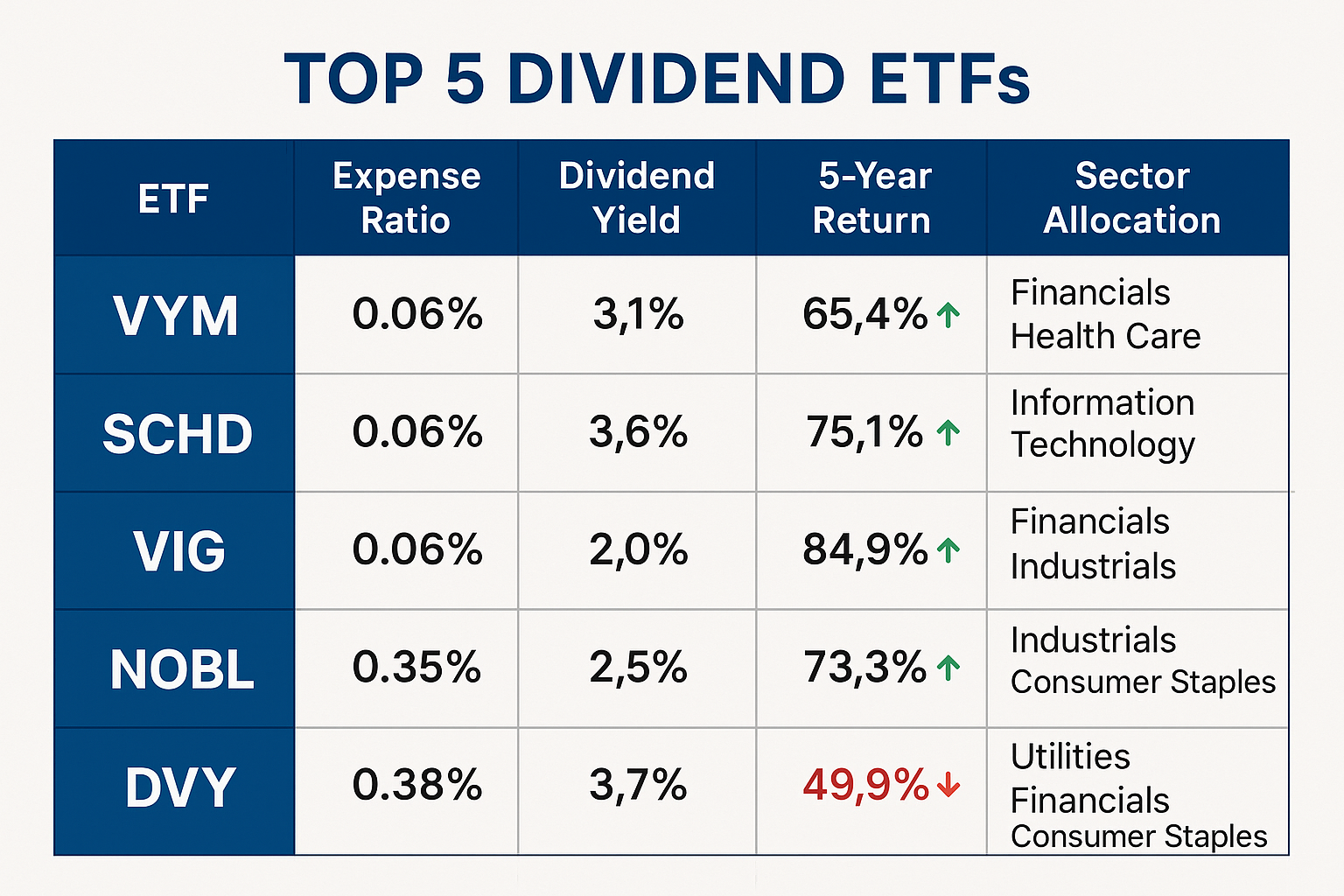

Performance Comparison: Top 5 Dividend ETFs

| ETF Symbol | Fund Name | Yield | Expense Ratio | 5-Year Return | Holdings |

|---|---|---|---|---|---|

| VYM | Vanguard High Dividend Yield | 3.1% | 0.06% | 9.2% | 440+ |

| SCHD | Schwab US Dividend Equity | 3.6% | 0.06% | 11.8% | 100+ |

| VIG | Vanguard Dividend Appreciation | 1.9% | 0.06% | 10.4% | 290+ |

| NOBL | ProShares S&P 500 Dividend Aristocrats | 1.8% | 0.35% | 9.8% | 65+ |

| DVY | iShares Select Dividend | 3.4% | 0.38% | 8.1% | 100+ |

SCHD emerges as the standout performer, combining attractive yield with superior total returns. Its focus on quality companies with sustainable dividend policies explains its outperformance during volatile markets.

Sector Diversification Analysis

Dividend ETFs typically overweight certain sectors due to their dividend-paying characteristics:

Utilities (15-25%): Stable, regulated businesses with predictable cash flows

Financials (15-20%): Banks and insurance companies with strong capital positions

Consumer Staples (10-15%): Companies selling essential goods with pricing power

Healthcare (8-12%): Pharmaceutical and medical device companies with patent protection

Technology (5-15%): Mature tech companies transitioning from growth to income

This sector concentration provides stability but may underperform during growth phases when technology and discretionary sectors lead markets.

Implementation Strategies for Maximum Returns

Building passive income through dividend ETFs requires systematic execution rather than market timing. The most successful investors follow disciplined approaches that prioritize consistency over perfection.

Dollar-Cost Averaging Approach

Dollar-cost averaging involves investing fixed amounts regularly regardless of market conditions. This strategy reduces the impact of volatility while building positions systematically.

Example: $500 Monthly Investment in SCHD

- Month 1: SCHD at $80 = 6.25 shares purchased

- Month 2: SCHD at $75 = 6.67 shares purchased

- Month 3: SCHD at $85 = 5.88 shares purchased

- Average cost: $79.86 vs. average price: $80.00

Over time, dollar-cost averaging typically results in lower average purchase prices compared to lump-sum investing at random intervals.

Tax-Efficient Implementation

Dividend income faces different tax treatment depending on account type and dividend classification. Qualified dividends from most ETFs receive favorable tax rates (0%, 15%, or 20% based on income), while non-qualified dividends face ordinary income tax rates.

Tax-Advantaged Account Strategy:

- 401(k)/403(b): Hold dividend ETFs in employer plans for tax-deferred growth

- Roth IRA: Ideal for dividend growth ETFs, allowing tax-free income in retirement

- Traditional IRA: Suitable for high-yield ETFs when current tax rates exceed future rates

- Taxable Accounts: Focus on tax-efficient, broad-market dividend ETFs

The 4% rule suggests retirees can withdraw 4% annually from portfolios without depleting principal. Dividend ETFs yielding 3-4% provide most of this income without selling shares.

Rebalancing and Monitoring

Successful dividend investing requires periodic portfolio review and rebalancing. Key metrics to monitor quarterly include:

Performance Metrics:

- Total return vs. benchmark indices

- Dividend growth rate vs. inflation

- Yield on cost (original investment basis)

- Maximum drawdown during market stress

Fundamental Changes:

- Expense ratio increases

- Strategy drift or holdings changes

- Dividend coverage ratios

- Sector concentration shifts

Rebalancing should occur when allocations drift more than 5-10% from target weights or annually at a minimum.

Advanced Strategies and Considerations

As dividend ETF portfolios mature, investors can implement more sophisticated strategies to optimize returns and manage risk. These advanced approaches require a deeper understanding but can significantly enhance long-term outcomes.

International Dividend Diversification

Global dividend ETFs provide exposure to international dividend-paying companies, offering currency diversification and access to different economic cycles. Developed market dividend ETFs typically yield 3-5%, while emerging market options may yield 4-7% with higher volatility.

Benefits of International Exposure:

- Currency hedging against dollar weakness

- Access to sectors underrepresented domestically (European utilities, Asian telecoms)

- Different dividend payment schedules (some markets pay annually vs. quarterly)

- Valuation arbitrage opportunities

However, international dividends often face higher tax rates, and foreign tax credits may apply. Consult tax professionals before significant international allocations.

Covered Call Enhancement

Some dividend ETFs employ covered call strategies to generate additional income beyond dividends. These funds sell call options on their holdings, collecting option premiums in exchange for capping upside potential.

Covered Call ETF Examples:

- JEPI (JPMorgan Equity Premium Income): 7-9% distribution yield

- QYLD (Global X NASDAQ 100 Covered Call): 8-12% distribution yield

- XYLD (Global X S&P 500 Covered Call): 7-10% distribution yield

While these strategies boost current income, they typically underperform in strong bull markets due to upside limitations.

REIT Integration

Real Estate Investment Trusts (REITs) complement dividend ETF portfolios by providing real estate exposure and typically higher yields (4-8%). REIT dividends receive different tax treatment, with most classified as ordinary income rather than qualified dividends.

REIT Allocation Guidelines:

- 5-15% of the total portfolio for diversification

- Focus on diversified REIT ETFs rather than sector-specific funds

- Consider REITs’ interest rate sensitivity when building allocations

- Monitor correlation with dividend ETFs during market stress

Common Mistakes and How to Avoid Them

Even experienced investors make costly errors when building dividend ETF portfolios. Understanding these pitfalls helps preserve capital and optimize returns over time.

Yield Chasing Trap

The biggest mistake involves chasing the highest-yielding ETFs without considering sustainability. Extremely high yields (8%+) often signal:

- Companies in financial distress

- Unsustainable payout ratios

- Recent price declines are inflating yield calculations

- Return of capital rather than true income

Solution: Focus on total return and dividend growth rather than current yield alone. A 2.5% yielding ETF growing dividends at 8% annually outperforms a static 5% yielder over time.

Inadequate Diversification

Concentrating too heavily in dividend ETFs creates sector bias and reduces growth potential. Many dividend-focused portfolios become overweight in utilities, REITs, and mature industries while underweighting technology and growth sectors.

Balanced Approach:

- Limit dividend ETFs to 30-50% of equity allocation

- Include growth ETFs for capital appreciation

- Maintain international exposure (20-30%)

- Consider small-cap and mid-cap allocations

Ignoring Expense Ratios

High expense ratios compound over time, significantly reducing returns. A 0.75% expense ratio costs $750 annually on a $100,000 investment, compared to $60 for a 0.06% low-cost alternative.

Cost-Conscious Selection:

- Target expense ratios below 0.20% for broad market funds

- Avoid actively managed dividend funds with ratios above 0.50%

- Consider fund size and liquidity when comparing costs

- Factor in bid-ask spreads for smaller ETFs

Timing the Market

Attempting to time dividend ETF purchases around ex-dividend dates or market cycles typically reduces returns. Studies show consistent investing outperforms market timing strategies over long periods.

Disciplined Approach:

- Maintain regular investment schedules regardless of market conditions

- Focus on time in market rather than timing the market

- Use volatility as an opportunity to purchase additional shares

- Avoid emotional decisions during market stress

Building Your Action Plan

Creating sustainable passive income through dividend ETFs requires a structured implementation plan tailored to individual circumstances and goals. This systematic approach ensures consistent progress toward financial independence.

Step 1: Assess Current Financial Position

Before investing in dividend ETFs, establish a solid financial foundation:

Emergency Fund: Maintain 3-6 months of expenses in high-yield savings accounts

Debt Management: Pay off high-interest debt (credit cards, personal loans) before investing

Cash Flow Analysis: Ensure sufficient income to support regular investments

Risk Tolerance: Determine comfort level with market volatility and potential losses

Use the emergency fund guide to establish appropriate cash reserves before beginning dividend investing.

Step 2: Define Investment Goals and Timeline

Clear objectives guide ETF selection and allocation decisions:

Income Goals: Target monthly or annual passive income requirements

Time Horizon: Investment period before needing income (retirement, financial independence)

Growth Expectations: Balance between current income and future growth

Tax Considerations: Account type selection and tax-efficient strategies

Step 3: Select Core Holdings

Build a foundation with 2-3 high-quality dividend ETFs:

Primary Holding (40-50% of dividend allocation):

- SCHD or VYM for broad market exposure

- Low expense ratios and strong track records

- Consistent dividend growth and reasonable yields

Secondary Holding (30-40%):

- VIG for dividend growth focus

- International dividend ETF for geographic diversification

- Sector-specific ETF is underweighted in core holdings

Satellite Holdings (10-20%):

- REIT ETF for real estate exposure

- High-yield ETF for additional income

- Covered call ETF for enhanced distributions

Step 4: Implement Investment Schedule

Consistency trumps perfection in dividend investing:

Monthly Investment Schedule:

- Automate transfers from checking to investment accounts

- Set specific dates (1st, 15th) for purchases

- Start with affordable amounts ($100-500) and increase gradually

- Reinvest all dividends automatically

Quarterly Review Process:

- Monitor performance vs. benchmarks

- Check for significant holdings or strategy changes

- Rebalance if allocations drift significantly

- Assess progress toward income goals

Tax Optimization Strategies

Maximizing after-tax returns requires understanding dividend taxation and implementing appropriate strategies. Tax-efficient investing can significantly impact long-term wealth accumulation.

Account Type Optimization

Different account types offer varying tax advantages for dividend investors:

Tax-Deferred Accounts (401k, Traditional IRA):

- Immediate tax deduction for contributions

- Dividends grow tax-free until withdrawal

- Ordinary income tax rates apply to withdrawals

- Required minimum distributions begin at age 73

Tax-Free Accounts (Roth IRA, Roth 401k):

- No immediate tax deduction

- Dividends and growth are completely tax-free

- No required distributions during the owner’s lifetime

- Ideal for young investors and dividend growth strategies

Taxable Accounts:

- No contribution limits or withdrawal restrictions

- Qualified dividends taxed at favorable rates (0%, 15%, 20%)

- Tax-loss harvesting opportunities

- Step-up in basis for inherited assets

Tax-Loss Harvesting

Dividend ETF investors can harvest tax losses to offset gains and reduce tax liability:

Harvesting Strategy:

- Sell losing positions to realize capital losses

- Offset gains from other investments or dividends

- Carry forward unused losses to future tax years

- Avoid wash sale rules by waiting 31 days or buying similar (not identical) ETFs

Example: An investor with $5,000 in dividend income can offset this with $5,000 in realized capital losses, eliminating current-year tax liability on the dividends.

Monitoring and Adjusting Your Portfolio

Successful dividend investing requires ongoing monitoring and periodic adjustments. Market conditions, personal circumstances, and fund changes necessitate portfolio evolution over time.

Key Performance Indicators

Track these metrics to assess dividend ETF portfolio health:

Income Metrics:

- Total annual dividend income

- Dividend growth rate vs. inflation

- Yield on cost (dividends/original investment)

- Distribution consistency and reliability

Performance Metrics:

- Total return vs. relevant benchmarks

- Risk-adjusted returns (Sharpe ratio)

- Maximum drawdown during market stress

- Correlation with the overall portfolio

Cost and Efficiency Metrics:

- Weighted average expense ratio

- Tax efficiency (after-tax returns)

- Trading costs and bid-ask spreads

- Account maintenance fees

When to Make Changes

Portfolio adjustments should be deliberate and based on fundamental changes rather than short-term market movements:

Fund-Level Changes:

- Significant expense ratio increases

- Strategy drift or management changes

- Persistent underperformance vs. peers

- Merger or liquidation announcements

Allocation Changes:

- Major life events (marriage, children, career changes)

- Shifting risk tolerance with age

- Achievement of financial milestones

- Significant market valuation changes

Income Adjustments:

- Dividend cuts by underlying holdings

- Changes in tax law affecting dividend treatment

- Inflation significantly exceeds dividend growth

- Need for increased current income

Building Long-Term Wealth Through Compound Growth

The true power of Passive Income with Dividend ETFs emerges through decades of compound growth. Understanding this mathematical principle helps investors maintain discipline during market volatility and focus on long-term objectives.

The Compound Growth Formula

Compound growth occurs when dividends are reinvested to purchase additional shares, which then generate their own dividends. This creates exponential rather than linear growth over time.

Future Value = Present Value × (1 + Growth Rate)^Number of Periods

For dividend ETFs, growth rate includes both dividend yield and dividend growth:

- 3.5% current yield + 5% annual dividend growth = 8.5% compound growth rate

- $10,000 investment growing at 8.5% annually reaches $66,200 after 20 years

- Annual dividend income grows from $350 to $2,317 over the same period

Real-World Example: 30-Year Journey

Consider Sarah, a 35-year-old professional who invests $500 monthly in dividend ETFs:

Years 1-10: Building the Foundation

- Monthly investment: $500 ($6,000 annually)

- Average yield: 3.5%

- Portfolio value at year 10: $85,000

- Annual dividend income: $2,975

Years 11-20: Acceleration Phase

- Monthly investment: $500 (increased with inflation)

- Yield on cost: 5.2% (due to dividend growth)

- Portfolio value at year 20: $245,000

- Annual dividend income: $12,740

Years 21-30: Wealth Accumulation

- Monthly investment: $500 (inflation-adjusted)

- Yield on cost: 7.8%

- Portfolio value at year 30: $580,000

- Annual dividend income: $45,240

By age 65, Sarah’s dividend income alone exceeds her original salary, demonstrating the power of patient, consistent investing in quality dividend ETFs.

Inflation Protection Through Dividend Growth

Unlike fixed-income investments, dividend-growing companies typically increase payments faster than inflation. This provides real purchasing power protection over time.

Historical Dividend Growth vs. Inflation:

- Average S&P 500 dividend growth (1960-2020): 5.8% annually

- Average inflation rate (same period): 3.9% annually

- Real dividend growth: 1.9% annually above inflation

This inflation protection explains why dividend growth stocks often outperform bonds and fixed-income investments during inflationary periods.

Conclusion: Your Path to Financial Freedom

Building Passive Income with Dividend ETFs represents one of the most accessible and reliable paths to financial independence. The combination of professional management, instant diversification, and low costs makes dividend ETFs ideal for beginners seeking steady income streams.

The math behind dividend investing is compelling: a $10,000 initial investment with $500 monthly additions, earning 8% annually through dividend yield and growth, grows to over $800,000 in 30 years while generating $28,000+ in annual passive income.

Success requires patience, consistency, and focus on total return rather than chasing yields. Start with high-quality, low-cost dividend ETFs like SCHD or VYM, implement systematic investment schedules, and reinvest dividends automatically for compound growth.

Your Action Steps:

- Establish an emergency fund and pay off high-interest debt before investing

- Open tax-advantaged accounts (IRA, 401k) to maximize after-tax returns

- Select 2-3 core dividend ETFs with expense ratios below 0.20%

- Automate monthly investments of $100-500 to build consistency

- Monitor quarterly, but avoid frequent changes based on market volatility

- Increase contributions annually with salary growth and inflation

- Stay disciplined during market downturns when yields become more attractive

The journey to financial independence through dividend ETFs requires time, but the destination—receiving substantial passive income without working—makes the patience worthwhile. Begin today with whatever amount you can afford, and let compound growth work its mathematical magic over the coming decades.

Remember: time in the market beats timing the market, especially when building wealth through the steady, reliable income streams that quality dividend ETFs provide.

Sources

[1] Morningstar Direct Database – ETF Performance and Holdings Data, 2025

[2] S&P Dow Jones Indices – S&P 500 Dividend Aristocrats Historical Performance

[3] Federal Reserve Economic Data (FRED) – Historical Inflation and Interest Rates

[4] Securities and Exchange Commission – ETF Investor Guidance and Regulations

[5] CFA Institute Research Foundation – Dividend Growth Investing Studies

[6] Vanguard Investment Strategy Group – Asset Allocation and Retirement Research

[7] Internal Revenue Service – Publication 550, Investment Income and Expenses