Missing a single payment deadline can cost you hundreds of dollars in interest charges and tank your credit score by over 100 points. Yet most people don’t fully understand the difference between their statement closing date and their payment due date, a confusion that costs American consumers billions annually in avoidable fees and interest.

Managing due dates becomes much easier once you understand the full credit process lenders use.

The payment due date is the specific deadline by which your credit card issuer must receive your minimum payment to avoid late fees, penalty interest rates, and credit score damage. This isn’t the date you send payment; it’s the date funds must be received. Understanding this critical distinction and the math behind your billing cycle can save you thousands of dollars over your lifetime while building a stronger credit profile.

This guide breaks down the data-driven approach to managing payment due dates, revealing how strategic timing can eliminate interest charges, optimize your credit utilization ratio, and create a cash-flow system that works with your financial goals rather than against them.

Key Takeaways

- Payment due dates are firm deadlines where funds must be received (not just sent) to avoid late fees averaging $32 and potential penalty APRs up to 29.99%

- The grace period (typically 21-25 days after statement closing) allows you to pay your balance in full without accruing interest charges

- Strategic payment timing can lower your reported credit utilization ratio by 30-50 points, directly improving your credit score

- Missing a payment by 30+ days triggers credit bureau reporting and can drop your score by 60-110 points for a single incident

- Multi-card payment scheduling aligned with your income cycle creates a sustainable system that prevents missed payments and maximizes available credit

What Is a Payment Due Date?

A payment due date is the mandatory deadline established by your creditor by which they must receive at least your minimum payment amount. This date represents a contractual obligation with specific financial and legal consequences for non-compliance.

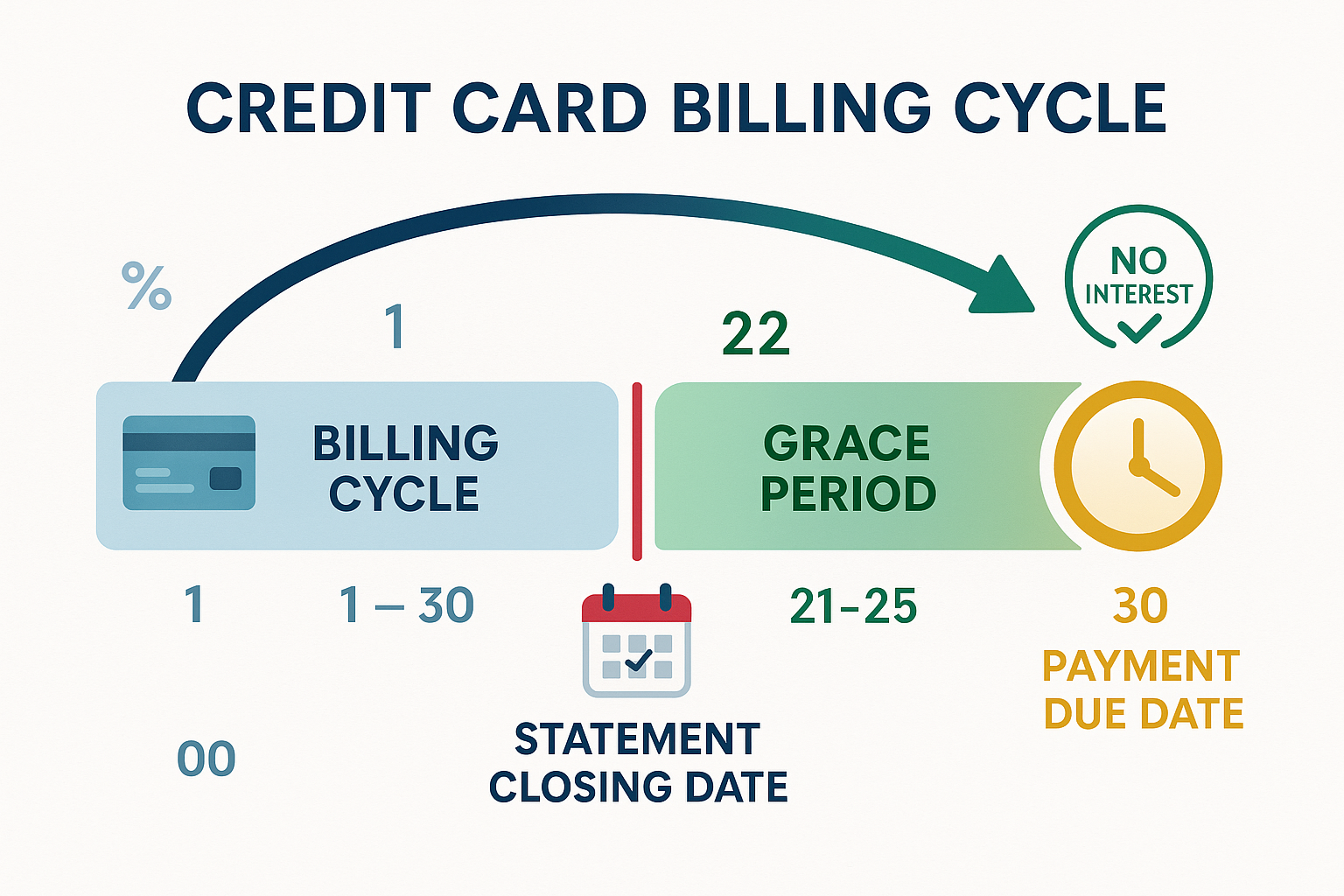

For credit card accounts, the payment due date typically falls 21-25 days after your statement closing date. This period, known as the grace period, represents the window during which you can pay your balance in full without incurring interest charges on new purchases.

The distinction between “sent” and “received” matters significantly. If you mail a check on your due date, the payment arrives late. Card issuers set specific cutoff times (often 5 PM ET for online payments, earlier for phone payments) that determine whether your payment counts as on-time.

Why payment due dates exist: Creditors use these dates to manage their own cash flow cycles, calculate interest charges, assess late fees, and report payment behavior to credit bureaus. From a risk management perspective, your payment history, whether you meet these deadlines, comprises 35% of your FICO credit score calculation.

The math behind the billing cycle creates a predictable pattern:

Billing Cycle Duration (typically 28-31 days) + Grace Period (21-25 days) = Total Time Before Payment Due

This structure gives you approximately 51-56 days between when you make a purchase at the beginning of a billing cycle and when payment is actually due, but only if you understand how to use the system strategically.

Payment Due Date vs Statement Closing Date

These two dates (Payment Due Date vs Statement Closing Date) serve completely different functions in your credit card cycle, yet confusing them represents one of the most common and costly mistakes consumers make.

Statement Closing Date (also called billing cycle end date): The final day of your billing period when the card issuer calculates your total balance, minimum payment, and reports your account information to credit bureaus.

Payment Due Date: The deadline by which you must submit at least the minimum payment to avoid late fees and negative credit reporting.

| Feature | Statement Closing Date | Payment Due Date |

|---|---|---|

| Purpose | Ends billing cycle; calculates balance | Deadline for minimum payment |

| Timing | Last day of billing period | Payment history is reported if missed by 30+ days |

| Credit Reporting | Utilization ratio reported to bureaus | Determines which purchases qualify for the grace period |

| Interest Calculation | Usually fixed by the issuer | Determines if the grace period applies to the next cycle |

| Flexibility | Payments before this date lower the reported utilization | Can often be changed upon request |

| Payment Impact | Payments before this date lower reported utilization | Payments after this date trigger late fees |

The timeline visualization:

Day 1-30: Billing cycle (you make purchases)

↓

Day 30: Statement closing date (balance calculated and reported to credit bureaus)

↓

Day 31-54: Grace period (21-25 days to pay without interest)

↓

Day 54: Payment due date (minimum payment must be received)

Critical insight: Your credit utilization ratio—the percentage of available credit you’re using- gets reported on your statement closing date, not your payment due date. This means making a payment before your statement closes can significantly improve your reported utilization, even if you then charge that amount again before the payment due date.

For example, if you have a $10,000 credit limit and typically carry a $3,000 balance (30% utilization), paying down to $1,000 before your statement closes reports only 10% utilization to the bureaus. You could then spend another $2,000 after the closing date and still have 25 days to pay it off before the due date.

This strategic timing can improve your credit score by 20-40 points without changing your actual spending or payment amounts, just the timing.

How Credit Card Interest Relates to Your Payment Due Date

The relationship between your payment due date and interest charges follows a specific mathematical sequence that most consumers don’t fully understand. This knowledge gap costs billions in avoidable interest annually.

The Grace Period Mechanism

Most credit cards offer a grace period of 21-25 days between your statement closing date and payment due date. During this window, no interest accrues on new purchases if you meet two conditions:

- You paid your previous statement balance in full by its due date

- You pay your current statement balance in full by the current due date

The math: If your APR is 18.99%, the daily periodic rate equals:

18.99% ÷ 365 = 0.052% per day

On a $3,000 balance, each day you carry that balance costs you:

$3,000 × 0.00052 = $1.56 per day in interest

Over a 30-day billing cycle, that’s $46.80 in interest charges, money that compounds if you don’t pay the full balance.

How Missing Your Payment Due Date Triggers Interest

When you miss your payment due date or pay less than the full statement balance, you lose your grace period for the next billing cycle. This means:

- Interest begins accruing on all new purchases from the transaction date (not from the statement closing date)

- Your existing balance continues to accrue interest daily

- You won’t regain the grace period until you pay two consecutive statement balances in full

Cascading cost example:

Month 1: Missed payment due date on $3,000 balance

- Late fee: $32 (industry average)

- Interest for one month: $46.80

- New balance: $3,078.80

Month 2: Make minimum payment only ($92)

- Previous balance: $3,078.80

- New purchases: $1,500

- Interest on previous balance: $48.11

- Interest on new purchases (from transaction date): $11.70

- New balance: $4,546.61

The compounding effect means you’re now paying interest on interest, a mathematical spiral that becomes increasingly difficult to escape.

Late Fee Structures and Penalty APR

Credit card issuers impose late fees according to a tiered structure regulated by the Consumer Financial Protection Bureau:

- First late payment: Up to $32

- Subsequent late payment within 6 billing cycles: Up to $43

- These amounts adjust annually for inflation

More damaging than late fees is the penalty APR, an elevated interest rate that can reach 29.99% and may apply indefinitely until you make six consecutive on-time payments. On a $5,000 balance, the difference between an 18.99% APR and a 29.99% penalty APR equals $45.83 additional interest per month, or $550 annually.

The credit score impact timeline:

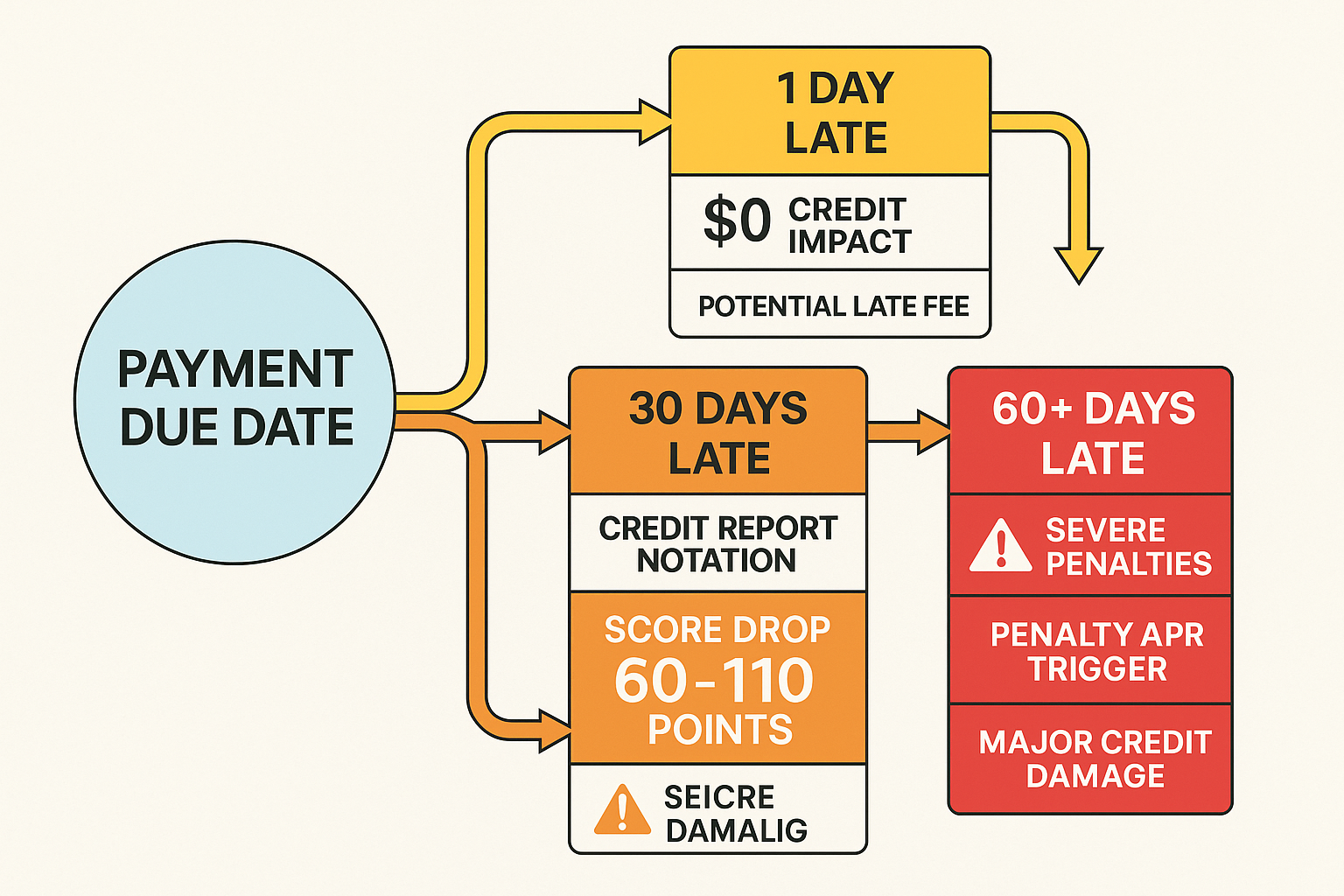

- 1-29 days late: No credit bureau reporting, but a late fee applies

- 30 days late: Reported to all three bureaus; score drops 60-110 points

- 60 days late: Additional negative mark; potential account restrictions

- 90+ days late: Severe delinquency; possible charge-off and collections

Understanding the APY vs APR distinction helps you calculate the true cost of carrying balances across payment cycles.

How to Find Your Payment Due Date

Locating your payment due date requires knowing where to look across different platforms and understanding how issuers communicate this critical information.

Primary Methods to Identify Your Payment Due Date

1. Monthly Statement (Most Reliable)

Your billing statement, whether paper or electronic, displays your payment due date prominently, typically in the top right corner or in a highlighted payment information box. This document also shows:

- Statement closing date

- Minimum payment amount

- Total balance

- Available credit

- Payment address (for mailed payments)

2. Mobile App Dashboard

All major card issuers provide mobile apps with your payment due date displayed on the home screen or account summary. Apps typically include:

- Countdown to due date

- Push notification reminders (customizable)

- One-tap payment functionality

- Payment history

3. Online Account Portal

Logging into your account via a web browser shows your payment information in the account overview section. Online portals often provide additional features:

- Ability to change your due date

- Payment scheduling tools

- Autopay setup options

- Transaction history with dates

4. Customer Service

Calling the number on the back of your card connects you to automated systems or representatives who can confirm your payment due date and accept payments by phone (though phone payment fees may apply).

Issuer-Specific Examples

Chase: Due date appears in the Chase Mobile app under “Account Details” and in the online portal under “Payment & Statements.” Chase allows you to change your due date once per year through the online portal.

American Express: Displays due date prominently in the Amex app home screen and sends customizable payment reminders. Amex allows due date changes online with no frequency restrictions.

Capital One: Shows due date in the app’s “Overview” tab and offers Eno, a virtual assistant that sends payment reminders via text. Due date changes can be requested through the app or by phone.

Discover: Lists due date in the Discover app under “Account Summary” and provides FICO score tracking to monitor payment impact. Due date modifications are available through customer service.

Pro tip: Screenshot your payment due date and set recurring calendar reminders 3-5 days before the deadline. This buffer accounts for payment processing time and prevents last-minute technical issues from causing late payments.

Understanding your accounts payable cycle in your personal finances works similarly to business cash flow management; timing matters as much as the payment amount.

Strategies to Manage Your Payment Due Date for Better Credit

Strategic management of your payment due date transforms it from a passive deadline into an active tool for credit optimization and financial stability. These evidence-based approaches leverage the math behind credit scoring and billing cycles.

Lower Utilization Strategy

Your credit utilization ratio, the percentage of available credit you’re using, accounts for 30% of your FICO score. The timing of when you pay relative to your statement closing date directly impacts this metric.

The mathematical approach:

If your statement closes on the 15th and your payment is due on the 10th of the following month, making a large payment on the 14th (before closing) reports a lower balance to credit bureaus than paying on the 9th (before due date but after closing).

Example calculation:

- Credit limit: $10,000

- Typical monthly spending: $4,000

- Standard utilization is paid on the due date: 40%

Optimized approach:

- Pay $3,500 on the 14th (before statement closes)

- Reported utilization: 5% ($500 remaining balance)

- Pay the remaining $500 by the due date (10th)

- Result: 35-point average credit score improvement

This strategy requires no change in spending or total payment amounts, only a timing adjustment. The cause-and-effect relationship is direct: lower reported utilization triggers algorithmic credit score increases.

Cash-Flow Alignment Strategy

Aligning your payment due dates with your income cycle prevents cash shortfalls that lead to missed payments. Most card issuers allow you to request a due date change once per year (some allow unlimited changes).

Strategic due date selection:

- Biweekly paycheck schedule: Set due dates 3-5 days after payday

- Monthly salary: Set due dates 5-7 days after deposit

- Irregular income: Set due dates for the latest expected income date plus a buffer

Multi-income household optimization:

If you receive income on the 1st and 15th:

- Card 1 due date: 5th (paid from 1st income)

- Card 2 due date: 20th (paid from 15th income)

- Card 3 due date: 5th (paid from 1st income)

This creates a balanced payment schedule that prevents all obligations from clustering around a single date, reducing the risk of insufficient funds.

The 50/30/20 rule budgeting framework helps allocate income across payment cycles systematically.

Avoiding Late Fees & Penalty APR

The mathematical cost of a single late payment extends far beyond the immediate late fee:

Single late payment cost breakdown:

- Late fee: $32

- Lost grace period interest (next cycle): $47

- Potential penalty APR increase: $46/month additional interest

- Credit score drop opportunity cost: Reduced approval odds for better rates

- Total first-year impact: $600-$800

Prevention mechanisms:

1. Autopay Configuration

Set autopay for at least the minimum payment to ensure you never miss the deadline. You can always pay more manually, but autopay provides a safety net.

Autopay options:

- Minimum payment only (safest for avoiding late fees)

- Statement balance (eliminates all interest charges)

- Fixed amount (predictable cash flow impact)

2. Multiple Reminder Systems

- Calendar alerts: 7 days before, 3 days before, 1 day before

- Email notifications from the issuer

- Text message alerts

- Physical calendar notation

3. Buffer Day Strategy

Treat the day before your due date as your actual deadline. This accounts for:

- Weekend/holiday processing delays

- Technical issues with payment platforms

- Bank transfer processing time

- Time zone differences

Multiple-Card Scheduling Plan

Managing several credit cards requires a systematic approach that prevents missed payments while optimizing utilization across all accounts.

The staggered due date method:

Instead of having all cards due around the same date, space them throughout the month:

| Card | Credit Limit | Statement Closes | Payment Due | Primary Use |

|---|---|---|---|---|

| Card A | $10,000 | 5th | 30th | Large purchases |

| Card B | $5,000 | 15th | 10th | Monthly subscriptions |

| Card C | $7,500 | 25th | 20th | Daily spending |

Benefits of staggering:

- Cash flow smoothing: Spreads payment obligations across the month

- Utilization optimization: Allows strategic paydown before each closing date

- Mental load reduction: Only one card requires attention per week

- Error prevention: Less likely to confuse due dates when they’re distinct

The payment priority system:

When cash flow is tight, prioritize payments in this order:

- Cards approaching 30 days late (credit reporting threshold)

- Cards with the highest penalty APR risk

- Cards with the highest current APR

- Cards with the largest balances

- Cards with the lowest balances (for psychological wins)

This evidence-based approach minimizes financial damage during temporary cash flow disruptions.

Your credit score responds predictably to payment timing patterns; consistency matters more than perfection.

Issuer Policies: Chase, Amex, Capital One, Discover

Understanding how major credit card issuers structure their payment due date policies reveals significant differences that can impact your financial strategy. This comparison uses 2025 data from issuer disclosures and cardholder agreements.

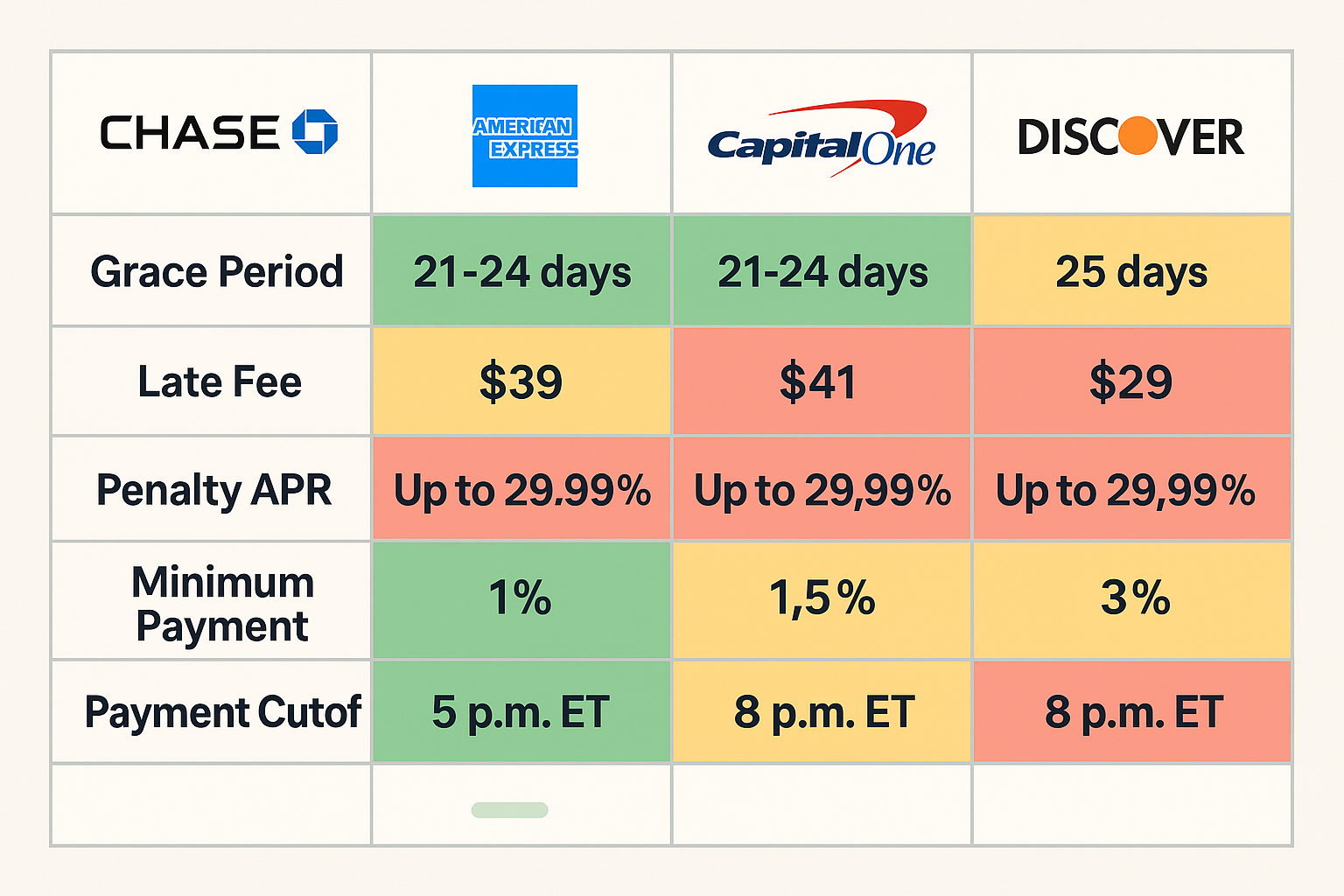

| Policy Feature | Chase | American Express | Capital One | Discover |

|---|---|---|---|---|

| Grace Period | 21 days minimum | 25 days (charge cards: none) | 25 days | 25 days |

| Late Fee (First) | Up to $32 | Up to $32 | Up to $32 | Up to $32 |

| Late Fee (Subsequent) | Up to $43 | Up to $43 | Up to $43 | Up to $43 |

| Penalty APR | Up to 29.99% | Up to 29.99% | Up to 29.99% | Up to 29.99% |

| Penalty APR Trigger | 60+ days late | 60+ days late | 60+ days late | Payment 60+ days late |

| Due Date Change Frequency | Once per year | Unlimited | Unlimited online | Contact customer service |

| Online Payment Cutoff | 5 PM ET | 8 PM ET | 8 PM ET | 5 PM ET |

| Phone Payment Fee | $10 | $0 (Platinum/Gold), $15 others | $10 | $15 |

| Minimum Payment | $40 or 1% + interest/fees | 1-2% + fees | $25 or 1% + interest/fees | $40 or 2% + fees |

| Weekend/Holiday Extension | Next business day | Next business day | Next business day | Next business day |

Key differentiators:

Chase: Restricts due date changes to once annually, requiring strategic planning before requesting modifications. Offers the earliest online payment cutoff, making same-day payments riskier.

American Express: Provides the latest payment cutoff time (8 PM ET) and unlimited due date changes, offering maximum flexibility. Charge cards (Green, Gold, Platinum) have no grace period and require full payment monthly.

Capital One: Allows unlimited due date changes through the online portal without customer service contact. Offers an Eno virtual assistant for payment reminders and fraud monitoring.

Discover: Includes free FICO score tracking, allowing you to monitor how payment timing affects your credit score. Requires customer service contact for due date changes, but typically accommodates requests.

Regulatory framework: The Credit CARD Act of 2009 mandates that payment due dates must:

- Fall on the same day each month

- Provide at least 21 days from statement closing to the due date

- Not fall on weekends/holidays (automatically extends to next business day)

- Allow payments received by 5 PM to count as on-time

Strategic issuer selection: When choosing between issuers, consider:

- Your typical payment timing (morning vs. evening payers benefit from later cutoffs)

- Need for due date flexibility (frequent income changes favor unlimited change policies)

- Preference for phone payments (fee structures vary significantly)

- Desire for integrated credit monitoring (Discover, Capital One offer free FICO tracking)

Understanding these policy differences allows you to select issuers whose systems align with your payment behavior patterns, reducing friction and late payment risk.

Common Mistakes People Make With Payment Due Dates

Despite the straightforward nature of payment deadlines, specific behavioral patterns and misconceptions lead to costly errors. Recognizing these mistakes prevents financial damage.

Mistake 1: Missing Autopay Setup

The error: Relying solely on manual payment reminders without configuring autopay as a backup system.

The cost: A 2024 Consumer Financial Protection Bureau study found that 23% of late payments occurred despite the cardholder intending to pay on time; they simply forgot or encountered technical issues [9].

The math: If you miss one payment annually due to oversight:

- Late fee: $32

- Interest on unpaid balance: ~$40-50

- Potential credit score impact: -30 to -60 points

- Annual cost: $72-82 plus opportunity cost of lower score

The fix: Set autopay for the minimum payment amount. You can always pay more manually, but autopay ensures you never miss the deadline entirely. Configure the payment method to a checking account with sufficient buffer funds.

Mistake 2: Confusing Closing Date vs Due Date

The error: Making payments based on the statement closing date rather than the payment due date, or vice versa.

The scenario: Your statement closes on the 15th, and payment is due on the 10th of the following month. You pay on the 16th, thinking you’ve met the deadline because it’s “after the statement.”

The consequence: You’ve paid 24 days before the actual due date, which is fine, but if you confused it the other way (paying on the 10th, thinking that’s the closing date), you’d be 5 days late.

The fix: Create a simple reference document:

Card: Chase Sapphire

- Statement closes: 15th

- Payment due: 10th (following month)

- Pay-by date for utilization optimization: 14th

- Absolute deadline: 10th

Store this in your phone’s notes app or password manager for instant reference.

Mistake 3: Paying After 5 PM Cutoff

The error: Submitting online payments after the issuer’s cutoff time and assuming they’ll count as same-day.

The reality: Most issuers set cutoffs between 5 PM and 8 PM ET. Payments submitted after this time count as next-day, potentially making an on-time payment late.

Example scenario:

- Payment due: April 10th

- You submit payment: April 10th at 6 PM ET

- Issuer cutoff: 5 PM ET

- Payment posts: April 11th

- Result: Late payment, $32 fee

The fix: Apply the “24-hour buffer rule”, make payments at least one full day before the due date. If your payment is due on the 10th, submit it by the 9th at the latest.

Mistake 4: Assuming Mailed Payments Arrive Instantly

The error: Mailing a check on the due date and expecting it to count as on-time.

The reality: Mailed payments require 3-7 business days for delivery and processing. The payment date is when the issuer receives and processes the payment, not when you mail it.

Cost example:

- Payment due: May 15th

- Check mailed: May 15th

- Check arrives: May 20th

- Check processes: May 21st

- Result: 6 days late, $32 late fee, potential credit reporting if it pushes previous late payment to 30+ days

The fix: Mail payments at least 10 business days before the due date, or switch to electronic payments for same-day processing.

Mistake 5: Ignoring Time Zone Differences

The error: Submitting payments based on your local time zone rather than the issuer’s time zone (typically Eastern Time).

The scenario: You live in California and submit a payment at 4 PM PT on the due date, thinking you’re within the 5 PM deadline. But 4 PM PT equals 7 PM ET, two hours past the cutoff.

The fix: Always convert cutoff times to your local zone:

- 5 PM ET = 2 PM PT = 3 PM MT = 4 PM CT

- 8 PM ET = 5 PM PT = 6 PM MT = 7 PM CT

Set phone reminders using the converted local time to avoid confusion.

Mistake 6: Paying Only the Minimum When Possible to Pay More

The error: Habitually paying only the minimum payment when cash flow allows for larger payments.

The mathematical impact: On a $5,000 balance at 18.99% APR:

- Minimum payment (2% + interest): ~$179

- Time to pay off: 17 years

- Total interest paid: $5,916

versus

- Payment of $300 monthly

- Time to pay off: 20 months

- Total interest paid: $847

The difference: $5,069 in interest savings by paying $121 more monthly.

The fix: Calculate your optimal payment using the formula:

Monthly Payment = (Balance × APR/12) + (Balance × 0.01)

This pays off the balance in approximately 3 years while minimizing interest.

Understanding debt-to-equity ratio principles helps you evaluate whether paying down credit cards or investing surplus cash generates better returns.

Examples: What Happens If You Miss a Payment Due Date?

Real-world scenarios demonstrate the cascading consequences of missed payment due dates across different timeframes. These examples use industry-average rates and fees from 2025 data.

Scenario 1: One Day Late

Initial situation:

- Balance: $3,500

- APR: 18.99%

- Payment due: March 15th

- Payment submitted: March 16th (one day late)

- Payment amount: $100 (minimum was $95)

Immediate consequences:

Late fee: $32 (charged to next statement)

Credit bureau reporting: None (late payments aren’t reported until 30 days past due)

Grace period status: Lost for next billing cycle (interest begins accruing on new purchases immediately)

Interest impact calculation:

Next month’s new purchases: $1,200

Days in billing cycle: 30

Daily periodic rate: 0.052%

Interest on new purchases = $1,200 × 0.00052 × 30 = $18.72

This interest wouldn’t have accrued if the grace period had remained intact.

Total cost of being one day late: $32 + $18.72 = $50.72

Credit score impact: 0 points (not reported to bureaus)

Recovery strategy: Pay the next statement balance in full to restore the grace period for the following cycle. The one-time late fee is a costly lesson, but credit damage is avoided.

Scenario 2: 30 Days Late

Initial situation:

- Balance: $4,200

- APR: 21.99%

- Payment due: April 10th

- Payment submitted: May 10th (30 days late)

- Payment amount: $150 (minimum was $126)

Immediate consequences:

Late fee: $32 (already charged on April statement)

Credit bureau reporting: Late payment reported to Equifax, Experian, and TransUnion as “30 days past due.”

Credit score impact: -60 to -110 points, depending on previous credit history

Account status changes:

- Grace period eliminated until two consecutive full balance payments

- Potential penalty APR trigger (depends on issuer policy)

- Possible credit limit decrease

- The account may be flagged for closure if the pattern continues

Interest accumulation:

Month 1 (April): $4,200 × (0.2199/12) = $76.97

Month 2 (May): $4,276.97 × (0.2199/12) = $78.38

Total interest for 30-day late period: $155.35

Total financial cost: $32 + $155.35 = $187.35

Opportunity cost: The credit score drop may result in:

- Higher interest rates on future credit applications

- Potential denial for premium credit cards

- Increased insurance premiums (credit-based insurance scores)

- Higher security deposits for utilities/rentals

Recovery timeline: The late payment remains on your credit report for 7 years, though its impact diminishes over time. Your score begins recovering immediately with on-time payments, typically regaining 50% of lost points within 6-12 months of consistent payment behavior.

Scenario 3: 60+ Days Late (Severe Delinquency)

Initial situation:

- Balance: $6,800

- APR: 19.99% (standard)

- Payment due: February 15th

- Payment submitted: April 20th (64 days late)

- Payment amount: $200 (minimum was $204)

Immediate consequences:

Late fees: $32 (February) + $43 (March) = $75

Penalty APR triggered: Rate increases to 29.99% (applies to entire balance)

Credit bureau reporting: “60 days past due” notation on all three bureaus

Credit score impact: -100 to -130 points (severe delinquency category)

Account restrictions:

- Card likely suspended (cannot make new purchases)

- Account flagged for potential charge-off at 180 days

- The issuer may demand payment in full

- The account may be sent to the collections department

Interest and fee accumulation:

Month 1 (Feb): $6,800 × (0.1999/12) = $113.27

Month 2 (March): $6,913.27 × (0.1999/12) + $32 late fee = $147.15

Month 3 (April): Penalty APR applies: $7,060.42 × (0.2999/12) = $176.51

Total interest and fees: $436.93

New balance after 64 days: $7,236.93

Long-term consequences:

Credit report damage: The 60-day late notation is more severe than the 30-day and signals a higher risk to future lenders. This may result in:

- Denial for mortgages or auto loans

- Subprime interest rates (8-12% higher than prime rates)

- Difficulty renting apartments

- Potential employment issues (for positions requiring credit checks)

Financial cost over 7 years: If the higher penalty APR remains and you make only minimum payments:

- Time to pay off: 28+ years

- Total interest: $18,400+

- Opportunity cost of damaged credit: $15,000-$50,000 in higher interest rates on other loans

Recovery strategy:

- Immediate: Make payment to bring the account current (pay all past-due amounts)

- Short-term: Contact the issuer to request penalty APR removal after 6 months of on-time payments

- Long-term: Establish perfect payment history for 12-24 months to rebuild score

- Consider: Goodwill letter to issuer requesting late payment removal (low success rate but worth attempting)

Understanding accounts receivable concepts helps you recognize that credit card companies view your payment obligation as their receivable, late payments directly impact their cash flow, and risk assessment.

💳 Payment Due Date Interest Calculator

Calculate the cost of missing your payment due date

📊 Cost of Missing Your Payment Due Date

Conclusion: Mastering Your Payment Due Date for Financial Success

Your payment due date represents more than a deadline; it’s a mathematical leverage point in your financial system. Understanding the precise mechanics of billing cycles, grace periods, and credit reporting timelines transforms this single date into a tool for credit optimization, interest avoidance, and wealth preservation.

The data is clear: Missing a payment due date by even one day costs an average of $51 in immediate fees and interest. Missing by 30 days costs $187 plus 60-110 credit score points. Missing by 60+ days can cost thousands in higher interest rates over the following years and tens of thousands in opportunity costs from damaged credit.

Your action plan:

- Document your due dates: Create a master list of all credit card payment due dates, statement closing dates, and issuer cutoff times

- Align with income: Request due date changes to fall 5-7 days after your regular payday

- Implement autopay: Set minimum payment autopay as a safety net while continuing manual payments

- Optimize utilization: Make payments before statement closing dates to lower reported balances

- Build buffer time: Submit payments 24-48 hours before due dates to account for processing delays

- Monitor consistently: Check accounts 1-2 days after due dates to verify successful payment processing

The math behind payment due dates follows predictable patterns. Master these patterns, and you eliminate billions of dollars in collective consumer waste while building the credit profile that unlocks premium financial products and lower interest rates.

Your payment due date is a fixed point in time. Your strategy for managing it determines whether it serves as an obstacle or an advantage.

Next step: Open your credit card app right now. Verify your next payment due date. Set three calendar reminders: 7 days before, 3 days before, and 1 day before. This five-minute action prevents the average $187 cost of a missed payment.

The difference between financial stability and financial stress often comes down to systematic management of recurring deadlines. Your payment due date is the most predictable, manageable, and consequential of these deadlines.

References

[1] Consumer Financial Protection Bureau. (2023). “Credit Card Payment Processing Requirements.” CFPB Regulatory Guidance.

[2] Fair Isaac Corporation. (2024). “Understanding Your FICO Score: Payment History Components.” MyFICO Consumer Education.

[3] VantageScore Solutions. (2024). “Credit Utilization Impact on Credit Scores: 2024 Analysis.” VantageScore Research.

[4] Federal Reserve. (2024). “Consumer Credit Card Late Fee Survey.” Federal Reserve Consumer Credit Report.

[5] Consumer Financial Protection Bureau. (2025). “Credit Card Late Fee Rule Adjustments.” CFPB Rule 1026.52.

[6] Experian. (2024). “How Late Payments Affect Your Credit Score.” Experian Credit Education.

[7] Credit Karma. (2024). “Credit Utilization Optimization Study: Score Impact Analysis.” Credit Karma Research.

[8] Federal Trade Commission. (2009). “Credit CARD Act of 2009: Payment Due Date Requirements.” FTC Regulatory Summary.

[9] Consumer Financial Protection Bureau. (2024). “Credit Card Payment Behavior Study.” CFPB Consumer Research.

[10] Bankrate. (2024). “Credit Card Minimum Payment Calculator: Long-term Cost Analysis.” Bankrate Financial Tools.

[11] FICO. (2024). “Late Payment Score Impact: Severity and Recovery Timeline.” FICO Score Research.

[12] Equifax. (2024). “Credit Utilization Timing Study: Statement Date vs. Due Date Impact.” Equifax Credit Research.

[13] TransUnion. (2024). “Optimal Credit Utilization Ratios for Score Maximization.” TransUnion Consumer Credit Analysis.

Educational Disclaimer

This article provides educational information about payment due dates, credit card billing cycles, and credit management strategies. It is not financial advice, and individual circumstances vary significantly.

Credit card terms, interest rates, fees, and issuer policies change frequently. Always verify current terms directly with your card issuer before making financial decisions. The examples provided use industry-average figures and may not reflect your specific account terms.

Credit score impacts vary based on individual credit history, existing score, and numerous other factors. The score ranges mentioned represent averages from industry studies and may not predict your specific outcome.

Before implementing any credit management strategy, consider consulting with a certified financial planner or credit counselor who can evaluate your complete financial situation.

The Rich Guy Math provides data-driven financial education but does not offer personalized financial advice. All financial decisions carry risk and should be made based on your individual circumstances, goals, and risk tolerance.

About the Author

Max Fonji is the founder of The Rich Guy Math, a data-driven financial education platform that explains the mathematical principles behind wealth building, investing, and credit management. With a background in financial analysis and a commitment to evidence-based education, Max translates complex financial concepts into actionable strategies backed by research and real-world data.

Max’s approach combines analytical precision with accessible teaching, helping readers understand not just what to do with their money, but why specific strategies work based on mathematical principles and behavioral economics. His work focuses on empowering financial literacy through clarity, logic, and verifiable evidence.

Connect with Max and explore more financial education resources at The Rich Guy Math.

Frequently Asked QuestionsWhy does my payment due date change sometimes?

Your payment due date normally stays the same each month unless you request a change or your billing cycle length varies. Issuers typically assign a fixed due date (e.g., the 15th of every month).

Common reasons it appears to change:

- Weekend/holiday adjustments: If the due date falls on a weekend or federal holiday, it automatically moves to the next business day.

- Billing cycle variation: Different month lengths (28–31 days) can affect how the dates appear.

- Issuer system changes: Rare, but issuers may update billing systems and notify you 45 days in advance.

- Account changes: New accounts, balance transfers, or promo periods can temporarily shift your cycle.

What to do: If your due date changes unexpectedly, contact your issuer—unexplained date shifts are rare and may signal an issue.

Why does my payment due date change sometimes?

Your payment due date normally stays the same each month unless you request a change or your billing cycle length varies. Issuers typically assign a fixed due date (e.g., the 15th of every month).

Common reasons it appears to change:

- Weekend/holiday adjustments: If the due date falls on a weekend or federal holiday, it automatically moves to the next business day.

- Billing cycle variation: Different month lengths (28–31 days) can affect how the dates appear.

- Issuer system changes: Rare, but issuers may update billing systems and notify you 45 days in advance.

- Account changes: New accounts, balance transfers, or promo periods can temporarily shift your cycle.

What to do: If your due date changes unexpectedly, contact your issuer—unexplained date shifts are rare and may signal an issue.

Can I move my payment due date to align with my payday?

Yes. Most major issuers allow you to change your due date.

Issuer policies:

- Chase: Once per year.

- American Express: Unlimited changes online.

- Capital One: Unlimited changes via online account.

- Discover: Customer service must process the request.

How to change your due date:

- Log in to your online account or mobile app.

- Go to “Account Settings” → “Payment Settings.”

- Select “Change Payment Due Date.”

- Choose a date (usually between the 1st–28th).

- Confirm. Changes apply next billing cycle.

Tip: Pick a date 5–7 days after payday for safer cash flow.

Note: Some issuers require the account to be open for 3–6 months before allowing changes.

Do weekends and holidays extend my payment due date?

Yes. Federal rules require that if your due date falls on a weekend or federal holiday, your deadline automatically shifts to the next business day.

Major U.S. federal holidays in 2025 include:

- New Year’s Day — Jan 1

- MLK Day — Jan 20

- Presidents’ Day — Feb 17

- Memorial Day — May 26

- Juneteenth — June 19

- Independence Day — July 4

- Labor Day — Sept 1

- Columbus Day — Oct 13

- Veterans Day — Nov 11

- Thanksgiving — Nov 27

- Christmas Day — Dec 25

Important: While the law protects you, some systems fail to update correctly. Always pay one business day early when possible.

Does autopay count as on-time even if it processes on the due date?

Yes. Autopay payments count as on-time as long as the payment successfully processes and your funding source has enough available funds.

How autopay timing works:

- Most issuers pull funds 1–2 business days before the due date.

- The payment posts to your credit card account on the due date.

Requirements for successful autopay:

- Sufficient bank account funds.

- Valid debit card or bank account.

- Correct autopay setting (minimum, statement balance, or custom amount).

- No bank blocks or holds.

Common failure causes:

- Insufficient funds.

- Expired debit card.

- Closed bank account.

Best practice: Check your account 1–2 days after the due date to confirm autopay processed.

Does paying before my statement closes help my credit score?

Yes. Paying before your statement closing date lowers the balance that gets reported to credit bureaus, reducing your credit utilization ratio—one of the most important credit score factors.

Example:

Credit limit: $8,000

Scenario A (pay after statement closes):

- Reported balance: $4,000

- Utilization: 50%

Scenario B (pay before statement closes):

- Payment before close: $3,200

- Reported balance: $800

- Utilization: 10%

Optimal strategy:

- Know your statement closing date.

- Pay down balance 1–2 days before closing.

- Let $50–$100 report to show activity.

- Pay remaining balance by due date to avoid interest.

Why not report $0? Reporting a very small balance (1–10% utilization) may produce a slightly better score than reporting zero.

Related posts:

Credit Utilization Ratio Explained: What It Is, How It Works, And How To Improve It

Credit Utilization Ratio Explained: What It Is, How It Works, And How To Improve It

How Long Do Late Payments Stay on Credit Report? The Complete 7-Year Timeline Explained

How Long Do Late Payments Stay on Credit Report? The Complete 7-Year Timeline Explained

Statement Balance vs Current Balance: Which One Should You to Pay

Statement Balance vs Current Balance: Which One Should You to Pay

Current Balance vs Available Balance: What’s the Difference?

Current Balance vs Available Balance: What’s the Difference?

Credit Card APR Explained: What It Is And How Interest Really Works

Credit Card APR Explained: What It Is And How Interest Really Works

How Long Does It Take to Build Credit? Real Timeline Explained

How Long Does It Take to Build Credit? Real Timeline Explained