Statement balance is the total amount you owed at the end of your last billing cycle. It includes all posted transactions, but not new or pending charges. This number matters because interest is usually charged on this balance if you don’t pay it in full by the due date.

Your statement balance becomes part of your permanent borrowing record, which is reported to the credit bureaus and included in your complete credit report history.

Every month, millions of credit card holders receive statements showing a number that determines whether they’ll pay interest or avoid it entirely. That number is the statement balance, and understanding it can save you hundreds or even thousands of dollars in unnecessary interest charges. Yet most people confuse it with their current balance, leading to costly mistakes that compound over time.

The difference between these two balance types isn’t just semantics; it’s the mathematical line between building credit efficiently and falling into a debt spiral. In 2025, with average credit card APRs hovering above 20%, knowing exactly which number to pay has never been more financially critical.

This guide breaks down the math behind statement balances, explains how they’re calculated, and shows you the precise strategies to use them for optimal financial management.

Key Takeaways

- Statement balance is the total amount owed at the end of your billing cycle, frozen on your statement closing date

- Paying your full statement balance by the due date eliminates interest charges and maintains your grace period

- Current balance updates in real-time and includes all transactions after the statement closes

- Your statement balance directly impacts your credit utilization ratio reported to credit bureaus

- Understanding the difference between these balances prevents overdraft fees, interest charges, and credit score damage

What Is Your Statement Balance?

Statement balance is the total amount you owe on your credit card account at the moment your billing cycle closes. This figure represents a snapshot in time, specifically, the exact balance on your statement closing date.

Think of it as a financial photograph. Once the billing cycle ends (typically after 28-31 days), your card issuer calculates everything you’ve charged, any fees incurred, interest applied, and payments made during that period. The resulting number becomes your statement balance.

Where to Find Your Statement Balance

Your statement balance appears in multiple locations:

- Monthly credit card statement (paper or digital)

- Card issuer’s mobile app under account summary

- Online banking portal in the statements section

- Email notifications are sent when statements are generated

Most major issuers like Chase, Capital One, American Express, and Discover display this prominently on the first page of your statement, usually near the top in bold text.

Why Statement Balance Matters

This number determines three critical financial outcomes:

- Interest avoidance: Pay this amount in full by the due date to avoid interest charges

- Credit reporting: This balance is typically reported to credit bureaus, affecting your credit utilization ratio

- Minimum payment calculation: Your minimum payment is usually a percentage of this balance

The statement balance remains unchanged from the closing date until your next billing cycle ends, even if you make new purchases or payments. This stability makes it the most reliable target for payment planning.

Statement Balance vs Current Balance: The Critical Difference

The confusion between statement balance and current balance causes more financial mistakes than almost any other banking terminology mix-up. These two numbers serve completely different purposes and are updated on different schedules.

How They Differ

| Feature | Statement Balance | Current Balance |

|---|---|---|

| Update frequency | Once per billing cycle | Real-time, after every transaction |

| What it includes | Changes after the statement closes | All transactions up to this moment |

| Changes after statement closes | No, remains fixed | Yes, updates continuously |

| Used for interest calculation | Yes, if unpaid | No |

| Reported to credit bureaus | Typically yes | Sometimes, depending on timing |

| Includes pending transactions | No | Yes |

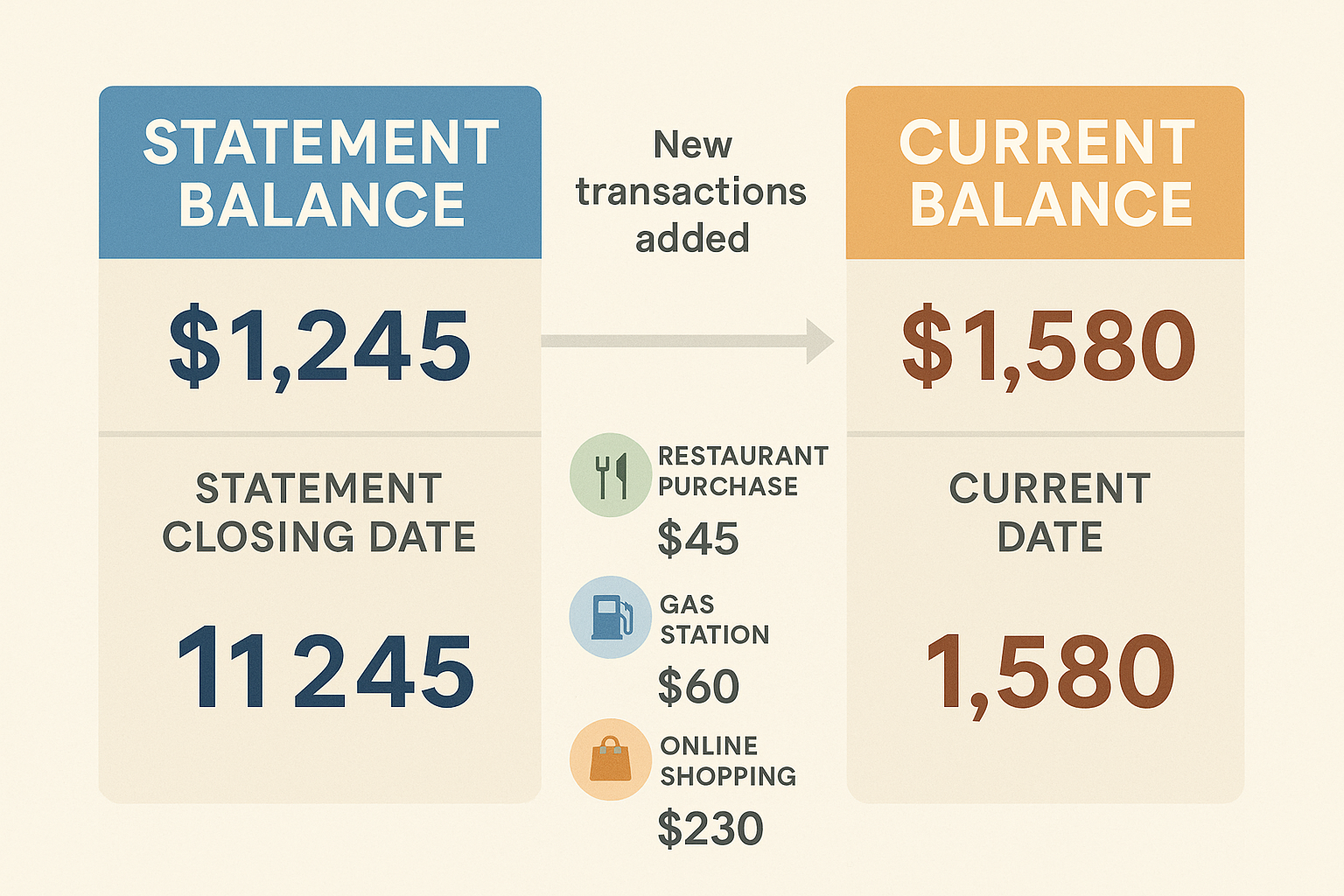

Real Example Breakdown

Here’s how these balances diverge in practice:

Scenario: Your billing cycle closes on March 15th.

| Transaction | Date | Amount | Impact |

|---|---|---|---|

| Starting balance | March 1 | $0 | Both balances |

| Restaurant | March 5 | $85 | Both balances |

| Gas station | March 10 | $60 | Both balances |

| Online shopping | March 14 | $200 | Both balances |

| Statement closes | March 15 | $345 | Statement balance = $345 |

| Grocery store | March 18 | $120 | Current balance only |

| Coffee shop | March 20 | $15 | Current balance only |

| Streaming service | March 22 | $18 | Current balance only |

| Current date | March 23 | $498 | Current balance = $498 |

On March 23rd:

- Statement balance: $345 (frozen since March 15)

- Current balance: $498 (includes all new transactions)

The Payment Decision

If you pay $345 (the statement balance) by the due date, you’ll:

Avoid all interest charges

Maintain your grace period

Keep your account in good standing

You’ll still owe the additional $153 from new purchases, but those will appear on your next statement and won’t accrue interest if you continue paying statement balances in full.

Suppose you only check your current balance and pay $498, you’re essentially prepaying for purchases that haven’t even appeared on a statement yet, not harmful, but financially inefficient since that money could earn interest in a high-yield savings account until the payment is actually due.

How Your Statement Balance Is Calculated

Understanding the mathematical components of your statement balance reveals exactly how credit card companies track your debt and calculate what you owe.

The Statement Balance Formula

Statement Balance = Previous Balance + New Purchases + Fees + Interest – Payments – Credits

Let’s break down each component:

1. Previous Unpaid Balance

Any amount you didn’t pay from last month’s statement carries forward. This is where interest begins accumulating if you don’t pay in full.

2. New Purchases

Every transaction processed during the billing cycle:

- Retail purchases

- Online shopping

- Subscription services

- Recurring charges

Important: Only transactions that were posted (not just pending) before the statement closing date count. A purchase made on the last day of your cycle might not post until the next cycle.

3. Fees

Common fees that increase your statement balance:

- Annual fees (charged once yearly)

- Late payment fees ($30-$40 typically)

- Foreign transaction fees (usually 3% of the purchase)

- Balance transfer fees (typically 3-5%)

- Cash advance fees (usually 5% or $10 minimum)

- Returned payment fees ($25-$40)

4. Interest Charges

If you carried a balance from the previous month, interest accrues daily based on your APR:

Daily Interest = (APR ÷ 365) × Current Balance

These compounds are used throughout the billing cycle. With a 20% APR on a $1,000 balance, you’d pay approximately $16.44 in interest over a 30-day cycle.

5. Payments

Any payments you made during the billing cycle reduce your statement balance. Payments must post (not just be initiated) before the closing date to affect that statement.

6. Credits

- Merchant refunds

- Rewards redemptions applied as statement credits

- Promotional credits

- Dispute resolutions in your favor

Example Calculation

Let’s walk through a complete billing cycle:

Starting point (April 1): Previous unpaid balance = $500

During the April 1-30 billing cycle:

- Purchases posted: $850

- Payment made April 10: -$500

- Annual fee charged: +$95

- Refund from returned item: -$45

- Interest on previous balance: +$8.22

Statement Balance (April 30) = $500 + $850 – $500 + $95 – $45 + $8.22 = $908.22

This $908.22 becomes your statement balance, and paying it in full by the due date (typically May 25) prevents any interest on the $850 in new purchases.

When Balances Are Calculated

Statement balance: Calculated once, at 11:59 PM on your statement closing date

Current balance: Calculated continuously, updating within minutes to hours of each transaction

This timing difference explains why your current balance can be lower than your statement balance if you’ve made payments after the statement closed but haven’t made new purchases.

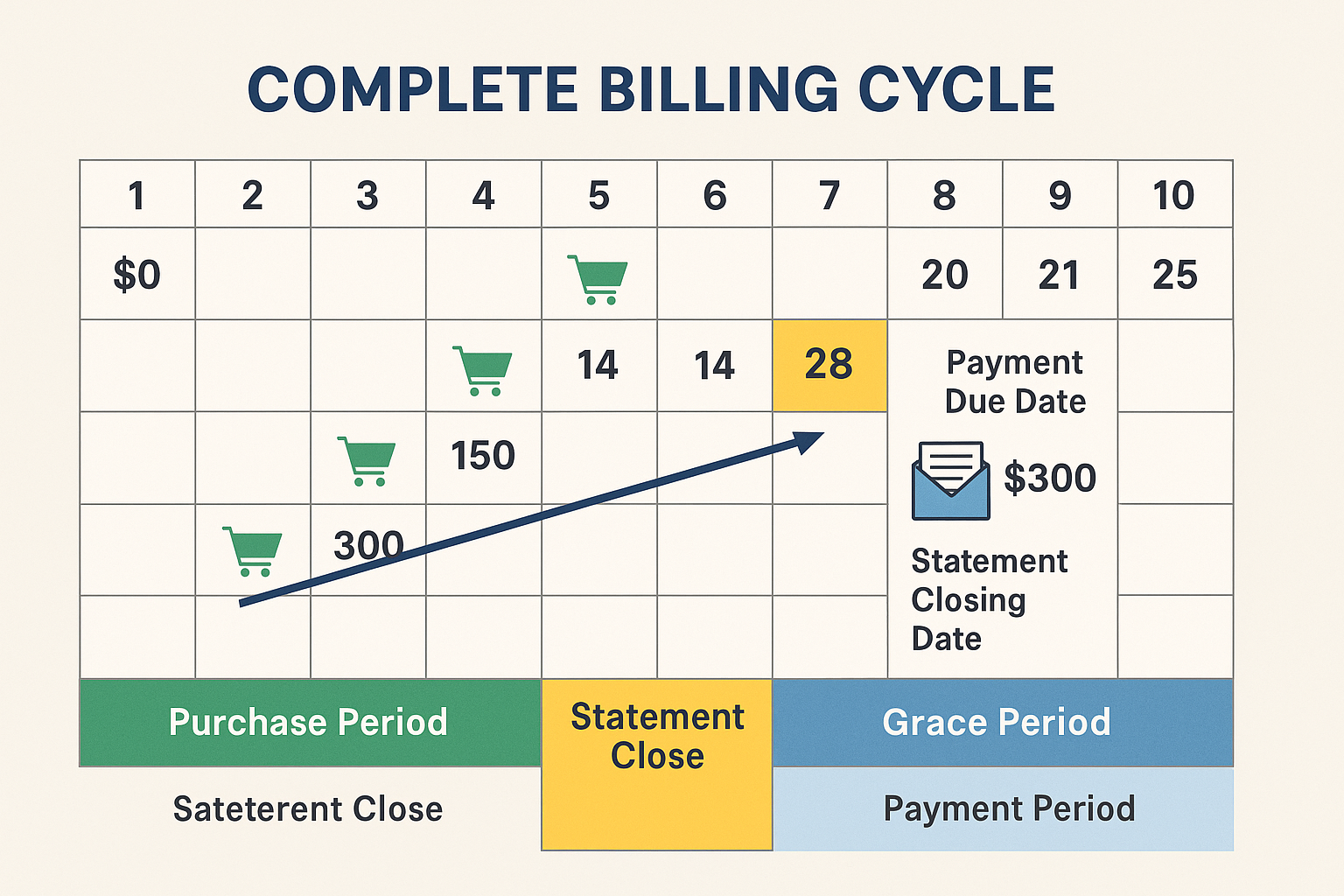

The Billing Cycle Timeline: When Everything Happens

The relationship between your statement balance and payment obligations follows a precise timeline that repeats every month. Understanding this cycle prevents missed payments and optimizes your cash flow management.

Standard Billing Cycle Structure

Phase 1: Billing Cycle (Days 1-30)

- Duration: 28-31 days typically

- Activity: All purchases, payments, and fees are tracked

- Balance type: Current balance updates in real-time

Phase 2: Statement Closing Date (Day 30)

- Timing: Usually the same calendar day each month (e.g., 15th)

- Event: Statement balance is calculated and frozen

- Generation: Statement is produced and made available within 1-2 days

Phase 3: Grace Period (Days 31-55)

- Duration: Minimum 21 days by federal law

- Purpose: Time to pay the statement balance without interest

- Condition: Only applies if you paid the previous statement in full

Phase 4: Payment Due Date (Day 55)

- Timing: At least 21 days after statement closing date

- Requirement: Minimum payment must be posted by this date

- Impact: Late payments trigger fees and potential APR increases

Visual Timeline Example

Day 1 (March 1): Billing cycle begins

↓

Days 1-30: Make purchases, payments tracked

↓

Day 30 (March 30): Statement closes

→ Statement Balance: $1,245

→ Statement generated March 31

↓

Days 31-55: Grace period (21+ days)

→ New purchases begin next cycle

→ Current balance continues updating

↓

Day 55 (April 20): Payment due date

→ Pay $1,245 to avoid interest

→ Pay minimum ($37) to avoid late feeCritical Date Distinctions

Statement Closing Date ≠ Payment Due Date

Many people confuse these, but they serve different purposes:

- Closing date: When your balance is calculated and reported

- Due date: Deadline to make payment without penalties

The gap between them (your grace period) is your interest-free loan period, but only if you pay the full statement balance.

How This Affects Credit Reporting

Most credit card issuers report your balance to credit bureaus on or shortly after your statement closing date. This means your statement balance is usually what appears on your credit report, not your current balance.

Strategic implication: If you have a large purchase that will increase your credit utilization ratio, consider making a payment before your statement closes to reduce the reported balance, even though the payment isn’t due yet.

How Statement Balance Affects Interest Charges

The relationship between your statement balance and interest charges follows precise mathematical rules that determine whether you pay zero interest or hundreds of dollars annually.

The Grace Period Mechanism

Credit cards offer a grace period, a window of time during which no interest accrues on new purchases. However, this benefit has strict conditions:

Grace Period Rules:

- Only applies to new purchases (not cash advances or balance transfers)

- Only available if you paid your previous statement balance in full

- Typically lasts 21-25 days from statement closing date

- Lost immediately if you carry any balance from the previous cycle

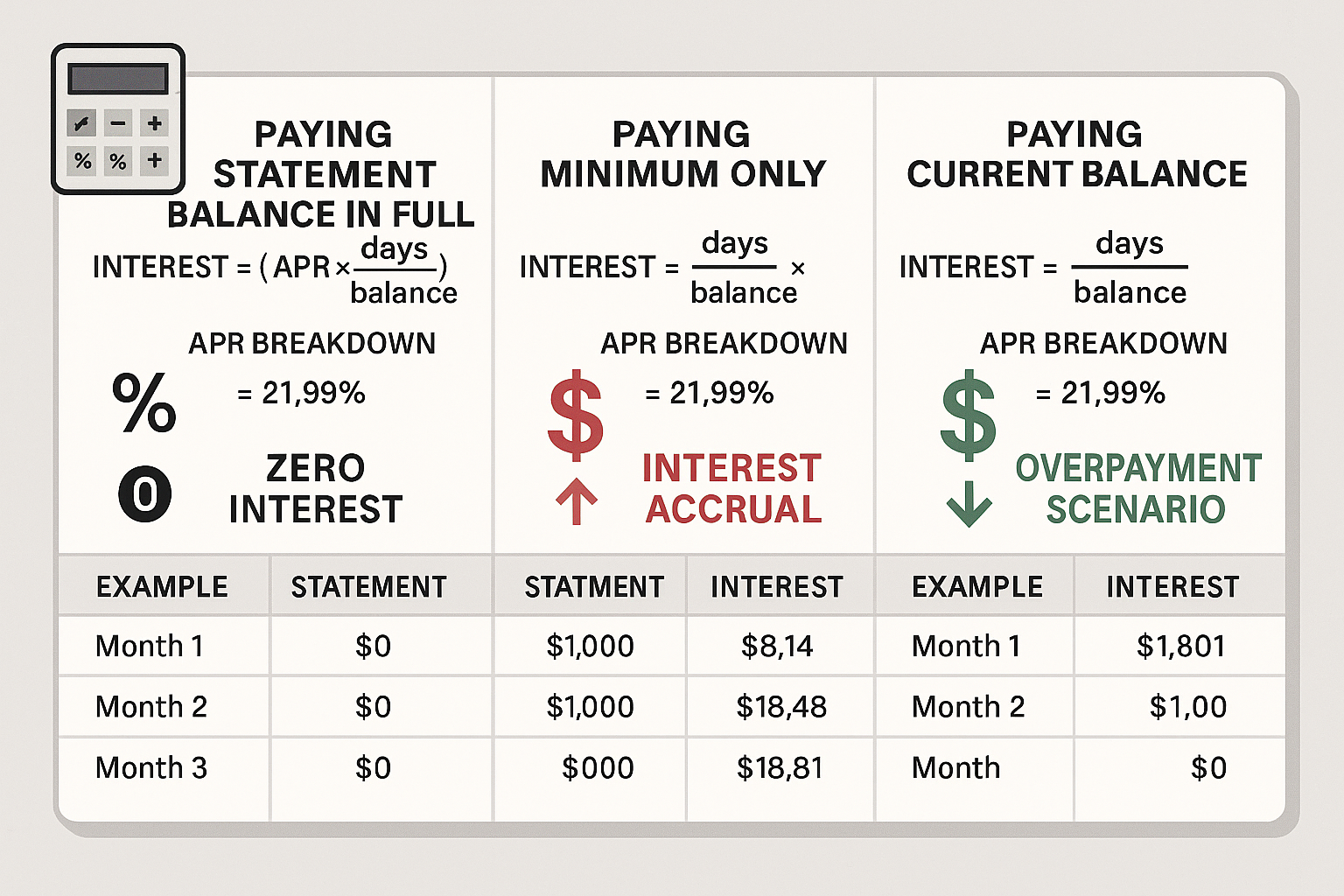

Interest Calculation on Unpaid Statement Balances

When you don’t pay your full statement balance, interest accrues using the average daily balance method:

Step 1: Calculate the daily balance for each day in the billing cycle

Step 2: Add all daily balances together

Step 3: Divide by the number of days in the cycle = Average Daily Balance

Step 4: Multiply by daily periodic rate (APR ÷ 365)

Step 5: Multiply by the number of days in the cycle = Interest charged

Real Example: The Cost of Partial Payment

Scenario: Statement balance = $2,000, APR = 20%, billing cycle = 30 days

Option A: Pay statement balance in full ($2,000)

- Interest charged: $0

- Grace period: Maintained

- Cost over 12 months: $0

Option B: Pay minimum only ($60)

- Average daily balance: ~$1,940

- Daily periodic rate: 20% ÷ 365 = 0.0548%

- Interest charged: $1,940 × 0.000548 × 30 = $31.88

- Next statement balance: $1,940 + $31.88 + new purchases

- Cost over 12 months: ~$400+ (assuming no new purchases)

The difference: $400 in interest charges simply for not paying the statement balance in full.

How New Purchases Are Treated

The treatment of new purchases depends entirely on whether you paid your previous statement balance:

If you paid the previous statement in full:

- New purchases have a grace period

- No interest until the next statement due date

- Can avoid interest indefinitely by continuing to pay in full

If you carried any balance:

- Grace period lost

- New purchases begin accruing interest immediately from the purchase date

- Must pay two consecutive statement balances in full to restore the grace period

The Minimum Payment Trap

Credit card issuers calculate minimum payments as a small percentage of your statement balance; typically 1-3% or $25-$35, whichever is greater.

Example minimum payment calculation:

Statement Balance: $3,000

Minimum: 2% of balance or $35, whichever is greater

Required minimum: $60

Paying only the minimum creates a debt spiral:

- Month 1: $3,000 balance, pay $60, charged $49.32 interest

- Month 2: $2,989.32 balance, paid $59.79, charged $49.15 interest

- Month 3: $2,978.68 balance…

At this rate, it would take approximately 15 years to pay off the original $3,000, and you’d pay over $3,800 in interest, more than the original purchase [5].

How to Pay Zero Interest Using the Statement Balance

The formula is mathematically simple:

Zero Interest Formula:

Pay ≥ Statement Balance by Due Date every month

This strategy:

- Maintains perpetual grace period

- Eliminates all interest charges on purchases

- Maximizes the interest-free loan period (up to 55 days on some purchases)

- Allows you to keep money in savings accounts, earning interest until payment is due

This approach aligns with broader budgeting strategies that prioritize eliminating high-interest debt.

Statement Balance and Your Credit Score

Your statement balance plays a direct role in determining your credit score through one of the most heavily weighted factors: the credit utilization ratio.

How Statement Balance Affects Credit Utilization

Credit utilization is the percentage of available credit you’re using:

Utilization Ratio = (Statement Balance ÷ Credit Limit) × 100

This ratio accounts for approximately 30% of your FICO credit score.

Example Calculation

Single card scenario:

- Credit limit: $5,000

- Statement balance: $1,500

- Utilization: ($1,500 ÷ $5,000) × 100 = 30%

Multiple cards scenario:

- Card 1: $3,000 limit, $900 balance

- Card 2: $7,000 limit, $2,100 balance

- Total limits: $10,000

- Total balances: $3,000

- Overall utilization: ($3,000 ÷ $10,000) × 100 = 30%

Optimal Utilization Targets

Credit scoring models prefer low utilization:

- Under 10%: Excellent—maximizes credit score benefit

- 10-30%: Good—minimal negative impact

- 30-50%: Fair—begins reducing score

- 50-70%: Poor—significant score reduction

- Over 70%: Very poor—major score damage

Important: Credit bureaus typically receive your statement balance, not your current balance, which is why the statement closing date matters so much for credit score optimization.

Strategic Timing for Large Purchases

If you need to make a large purchase that will spike your utilization above 30%, consider this strategy:

Option 1: Pre-statement payment

- Make a large purchase

- Make payment before the statement closing date

- Lower balance gets reported to bureaus

- Credit score impact minimized

Option 2: Split across cards

- Distribute a large purchase across multiple cards

- Keep each card under 30% utilization

- Overall utilization stays lower

- Better score impact

When Statement Balance Is Reported

Most issuers report to credit bureaus on a predictable schedule:

- Primary reporting date: Statement closing date (most common)

- Alternative timing: A few days after the closing date

- Frequency: Once per month per account

Verification tip: Check your credit report to see which balance was reported, then count backward to identify your reporting date. Most issuers maintain consistent reporting schedules.

The Zero Balance Reporting Strategy

Some credit scoring models penalize accounts that consistently report zero balances, interpreting this as “inactive” credit. The optimal strategy:

Allow small statement balance to report → Pay in full by due date

This approach:

- Shows active credit usage

- Maintains low utilization

- Demonstrates responsible payment behavior

- Avoids all interest charges

Example: Let one card report a $50 statement balance (1% utilization on a $5,000 limit), then pay it in full. This signals activity without utilization concerns.

How to Use Statement Balance to Avoid Interest and Fees

Mastering statement balance management transforms your credit card from a potential debt trap into a powerful financial tool that provides free short-term loans and rewards.

Strategy 1: The Full Payment Method

Implementation:

- Wait for the statement to generate after the closing date

- Note the statement balance amount

- Set up payment for the full statement balance

- Schedule payment to arrive 2-3 days before the due date

- Verify payment posted before the due date

Result: Zero interest, maintained grace period, optimal credit card usage

Strategy 2: Automated Statement Balance Payment

Most card issuers offer automatic payment options:

Autopay settings:

- Minimum payment: Avoids late fees but accrues interest (not recommended)

- Statement balance: Pays in full automatically (recommended)

- Current balance: Overpays by including next cycle’s charges (inefficient)

- Fixed amount: Pays a set dollar amount (useful for planned paydown)

Best practice: Set autopay to “statement balance” and maintain sufficient funds in your linked checking account. This eliminates the risk of missed payments while preserving your grace period.

Strategy 3: The Pre-Statement Payment Approach

For those managing tight budgets or high utilization:

Process:

- Make purchases throughout the billing cycle

- Make payment before the statement closing date

- Reduce the balance that will be reported

- The lower statement balance appears on the statement

- Pay the remaining statement balance by the due date

Benefits:

- Lower reported balance to credit bureaus

- Reduced credit utilization impact

- Smaller payment due at the statement due date

- Spreads payments across the month for cash flow management

Strategy 4: The Multiple Payment Method

Scenario: You have a $2,000 statement balance but want to improve cash flow

Implementation:

- Payment 1 (April 5): $700

- Payment 2 (April 15): $700

- Payment 3 (April 20, before due date): $600

- Total: $2,000 (full statement balance paid)

Advantages:

- Aligns with multiple paychecks

- Reduces the psychological burden of a large single payment

- Maintains zero interest status

- Improves budgeting flexibility

Common Mistakes to Avoid

Paying only the current balance: May overpay or underpay the statement amount

Paying day of due date: Risks of processing delays causing late payment

Paying minimum to “build credit”: Costs hundreds in interest; full payment builds credit better

Ignoring statement closing date: Misses the opportunity to optimize the reported balance

Confusing statement date with due date: Causes payment timing errors

Setting Up Payment Alerts

Configure these notifications to never miss a payment:

- Statement generated alert: Know when the statement balance is set

- Payment due reminder: 7 days before due date

- Payment received confirmation: Verify payment posted

- Unusual activity alert: Catch unauthorized charges before the statement closes

Most issuers offer these through their mobile apps, email, or SMS.

The 2-3 Day Payment Buffer Rule

Always schedule payments to arrive 2-3 business days before your due date:

- ACH transfers: Can take 1-3 business days

- Weekends/holidays: Don’t count as business days

- Processing cutoff times: Payments after the cutoff process the next day

- Bank delays: Occasional technical issues cause delays

Example: If your payment is due April 20th (Friday), schedule it to arrive by April 17th (Tuesday) to account for potential delays.

Statement Balance Across Different Card Types

Statement balance mechanics vary slightly depending on your credit card type and issuer policies.

Credit Cards vs Charge Cards

Traditional Credit Cards (Visa, Mastercard, Discover):

- Allow carrying balances month-to-month

- Charge interest on unpaid statement balances

- Require minimum payment only

- Grace period conditional on full payment

Charge Cards (American Express traditional charge cards):

- Require a full statement balance payment monthly

- No preset spending limit on some cards

- No interest charges (balance must be paid in full)

- Late fees and penalties for non-payment

Issuer-Specific Variations

Chase:

- Reports the statement balance on the closing date

- Offers “Pay Yourself Back” redemption that reduces the statement balance

- Autopay processes 2 days before the due date

Capital One:

- May report mid-cycle balances in addition to the statement balance

- Offers flexible payment date selection

- Real-time balance updates in the mobile app

American Express:

- Charge cards require full statement balance payment

- Credit cards function like traditional cards

- Early payment can reduce the reported balance

Discover:

- Reports on statement closing date

- Offers payment date flexibility (can change due date)

- Cashback rewards can be applied to reduce the statement balance

Business Credit Cards

Business cards follow the same statement balance principles, but with different implications:

- Higher credit limits: Often 2-5x personal card limits

- Separate reporting: May not appear on personal credit report

- Payment responsibility: The Business owner is typically personally liable

- Expense tracking: Statement balance includes employee card charges

Store Cards and Retail Credit

Store-specific cards often have:

- Promotional financing: “No interest if paid in full within X months”

- Deferred interest: Full interest charged retroactively if the statement balance is not paid by the promotion end

- Higher APRs: Often 25-30% on unpaid statement balances

Critical: With deferred interest promotions, you must pay the entire promotional purchase amount (which may span multiple statement balances) by the promotion end date, not just each month’s statement balance.

Advanced Statement Balance Strategies

Once you master basic statement balance management, these advanced techniques optimize your financial position.

The Credit Utilization Timing Strategy

Goal: Minimize reported utilization while maximizing credit card usage

Method:

- Identify your statement closing date

- Make large purchases immediately after the closing date

- Pay them off before the next closing date

- Low balance reports to bureaus despite high spending

Example timeline:

- March 15: Statement closes, $100 balance reports

- March 16: Make $3,000 purchase

- April 10: Pay $3,000

- April 15: Statement closes, $100 balance reports again

- Result: Used $3,000+ in credit, only $100 reported each month

The Multiple Card Rotation Method

Strategy: Rotate which cards carry statement balances to optimize rewards and utilization

Implementation:

- Card 1 (Q1): Use for all purchases, pay in full, 5% utilization reports

- Card 2 (Q2): Primary card, pay in full, 5% utilization reports

- Card 3 (Q3): Primary card, pay in full, 5% utilization reports

- Rotate based on category bonuses and promotional offers

Benefits:

- Maximizes rewards in bonus categories

- Keeps all cards active

- Maintains low utilization across all accounts

- Builds a diverse credit history

The Statement Balance Arbitrage Approach

Concept: Use the grace period to keep money in interest-bearing accounts longer

Process:

- Make $5,000 in purchases during the billing cycle

- Keep $5,000 in high-yield savings (earning 4.5% APY)

- Wait until 2 days before the due date (day 53 of 55)

- Transfer $5,000 to pay the statement balance

- Earn interest for 53 days instead of throughout the month

Annual benefit calculation:

- Average float: $5,000 for ~26 extra days per statement

- Interest rate: 4.5% APY

- Additional annual interest: $5,000 × 0.045 × (26/365) × 12 = ~$39

While modest, this strategy compounds across multiple cards and scales with spending. For someone floating $20,000 monthly across cards, this generates $150+ annually in additional interest income.

The Balance Transfer Statement Strategy

When transferring balances, understanding statement mechanics is crucial:

Optimal timing:

- Request a balance transfer immediately after the statement closes

- Transfer posts to the new card in the next billing cycle

- Maximizes 0% APR promotional period

- Minimizes interest on the old card

Statement balance impact:

- Old card: Statement balance reduced by transfer amount

- New card: Transfer appears as a purchase on the next statement

- Pay the old card’s remaining statement balance in full

- Begin systematic paydown of the transfer balance

📊 Statement Balance Calculator

Calculate your statement balance and see how payments affect interest charges

Your Statement Balance

Calculation Breakdown

Minimum Payment (2% or $25)

Conclusion

Understanding your statement balance is fundamental to mastering credit card management and avoiding the interest trap that costs Americans over $120 billion annually in credit card interest. The math is straightforward: pay your full statement balance by the due date every month, and you’ll never pay a cent in interest while building excellent credit.

The distinction between statement balance and current balance isn’t just banking jargon; it’s the difference between using credit cards as powerful financial tools and falling into expensive debt spirals. Your statement balance represents your actual payment obligation, frozen at your statement closing date, while your current balance is simply a real-time snapshot that includes transactions not yet due.

Your Action Plan

- Locate your statement closing date in your most recent credit card statement or mobile app

- Set up autopay for your full statement balance to eliminate missed payment risk

- Configure payment alerts for statement generation and upcoming due dates

- Review your credit utilization and consider making pre-statement payments if above 30%

- Track both balances to understand your spending patterns and upcoming obligations

- Implement the 2-3 day buffer rule by scheduling payments to arrive before your due date

The compound effect of these practices extends beyond avoiding interest charges. Consistent statement balance management improves your credit score through low utilization and perfect payment history, qualifies you for better interest rates on mortgages and auto loans, and builds the financial discipline that underlies all wealth accumulation.

Remember: credit cards offer an interest-free loan of up to 55 days when used properly. That’s free money, but only if you understand and respect the statement balance deadline. Master this concept, and you’ve mastered one of the most important tools in modern personal finance.

For more guidance on optimizing your overall financial strategy, explore our comprehensive guides on budgeting frameworks, credit utilization optimization, and building financial literacy.

Author Bio

Max Fonji is a data-driven financial educator and the voice behind The Rich Guy Math. With a background in financial analysis and a passion for translating complex money concepts into actionable strategies, Max helps readers understand the mathematical principles that drive wealth building. His evidence-based approach combines academic research, industry data, and practical experience to demystify personal finance topics from credit management to investment strategies.

Disclaimer

This article is provided for educational and informational purposes only and should not be construed as financial advice. Credit card terms, interest rates, fees, and policies vary by issuer and are subject to change. Statement balance mechanics and billing cycle structures may differ based on your specific card agreement. Always review your cardholder agreement and consult with a qualified financial advisor before making financial decisions. The Rich Guy Math is not responsible for any financial decisions made based on this content. Credit card usage involves financial risk, and failure to pay balances as agreed can result in interest charges, fees, and credit score.

References

[1] Federal Reserve Bank of St. Louis. (2025). “Credit Card Interest Rates and Consumer Debt Statistics.” Economic Research Division.

[2] Consumer Financial Protection Bureau. (2025). “Understanding Your Credit Card Statement.” CFPB Consumer Education.

[3] Truth in Lending Act, Regulation Z. 12 CFR § 1026.5(b)(2)(ii). “Timing of Statement Mailing and Grace Period Requirements.”

[4] Fair Credit Reporting Act. 15 U.S.C. § 1681. “Credit Bureau Reporting Standards and Practices.”

[5] Federal Reserve Board. (2024). “Report on the Economic Well-Being of U.S. Households: Credit Card Debt and Minimum Payment Analysis.”

[6] Fair Isaac Corporation (FICO). (2025). “Understanding FICO Scores: Credit Utilization Impact Analysis.”

[7] Federal Reserve Consumer Credit Statistical Release. (2025). “G.19 Consumer Credit Report: Revolving Credit Interest Calculations.”

Statement Balance FAQs

Should I pay my statement balance or current balance?

Pay your statement balance in full by the due date. This eliminates all interest charges while maintaining your grace period on new purchases. Paying the current balance means overpaying for purchases that aren’t due yet, which is financially inefficient since that money could earn interest elsewhere until the payment is actually required.

What happens if I only pay the minimum instead of the statement balance?

Paying only the minimum triggers several negative consequences: (1) You’ll be charged interest on the unpaid portion of your statement balance, (2) You’ll lose your grace period on new purchases, which will immediately begin accruing interest, (3) It can take years to pay off the balance while accumulating hundreds or thousands in interest charges, and (4) Your credit utilization ratio increases, potentially lowering your credit score.

Can my statement balance be higher than my credit limit?

Yes, your statement balance can exceed your credit limit due to interest charges, fees, or transactions that posted after you reached your limit. This creates an “over-limit” situation. While the CARD Act of 2009 prohibits over-limit fees unless you opt in, exceeding your limit can trigger account restrictions, APR increases, and significant damage to your credit score due to extremely high utilization.

Why is my statement balance different from what I see in my app?

Your statement balance is frozen at your statement closing date and doesn’t change until the next cycle closes. Your app shows your current balance, which updates in real-time with every transaction, payment, and charge. Any purchases, payments, or fees that occurred after your statement closed will cause these numbers to differ. This is normal and expected.

Does paying before the statement closing date help my credit score?

Yes, making a payment before your statement closes reduces the balance that gets reported to credit bureaus, lowering your credit utilization ratio. Since utilization accounts for about 30% of your credit score, this strategy can improve your score, especially if you’re currently above 30% utilization. However, you still need to pay the remaining statement balance by the due date to avoid interest.

What if I accidentally pay less than my statement balance?

If you pay less than your full statement balance but more than the minimum, you’ll be charged interest on the unpaid portion and lose your grace period on new purchases. Contact your card issuer immediately—some may allow you to make an additional payment before the due date to avoid interest if it’s a genuine error. Set up payment alerts and autopay to prevent this situation.

How long do I have to pay my statement balance?

You have until your payment due date, which must be at least 21 days after your statement closing date per federal law. The exact number of days (your grace period) varies by issuer but typically ranges from 21-25 days. Check your statement for the specific due date, and schedule payment to arrive 2-3 days early to account for processing time.

Will paying my statement balance in full hurt my credit score?

No, paying your statement balance in full helps your credit score. It demonstrates responsible credit usage, maintains low utilization, and establishes positive payment history—the most important factor in credit scoring. The myth that carrying a balance “builds credit” is false and costly. Paying in full builds credit just as effectively while avoiding interest charges entirely.

Can I change my statement closing date?

Most major credit card issuers allow you to request a statement closing date change, though policies vary. Chase, Capital One, Discover, and American Express typically accommodate these requests. Changing your closing date can help align your payment due date with your paycheck schedule or optimize credit reporting timing. Contact your issuer’s customer service to request a change—it’s usually processed within 1-2 billing cycles.

What’s included in my statement balance besides purchases?

Your statement balance includes: (1) All purchases that posted during the billing cycle, (2) Interest charges on any previous unpaid balance, (3) Annual fees, late fees, foreign transaction fees, and other charges, (4) Cash advance fees and balance transfer fees, (5) Any adjustments or credits from returns or disputes. It excludes: transactions still pending, purchases made after the statement closing date, and payments made after the closing date.

Related posts:

Credit Utilization Ratio Explained: What It Is, How It Works, And How To Improve It

Credit Utilization Ratio Explained: What It Is, How It Works, And How To Improve It

How Long Do Late Payments Stay on Credit Report? The Complete 7-Year Timeline Explained

How Long Do Late Payments Stay on Credit Report? The Complete 7-Year Timeline Explained

Statement Balance vs Current Balance: Which One Should You to Pay

Statement Balance vs Current Balance: Which One Should You to Pay

Current Balance vs Available Balance: What’s the Difference?

Current Balance vs Available Balance: What’s the Difference?

Credit Card APR Explained: What It Is And How Interest Really Works

Credit Card APR Explained: What It Is And How Interest Really Works

How Long Does It Take to Build Credit? Real Timeline Explained

How Long Does It Take to Build Credit? Real Timeline Explained