Most investors overcomplicate wealth building. They chase hot stocks, pay high fees to active managers, and wonder why their returns lag the market.

Vanguard Index Funds offer a different path—one grounded in mathematics, evidence, and a structure designed to keep more money in investor pockets. These funds don’t try to beat the market. They become the market, tracking major indexes like the S&P 500 while charging a fraction of what traditional mutual funds cost.

The numbers tell a clear story: Over 90% of actively managed funds underperform their benchmark indexes over 15-year periods, according to S&P Dow Jones Indices [1]. Meanwhile, Vanguard’s investor-owned structure has enabled expense ratios as low as 0.03%—meaning investors keep 99.97% of their returns instead of paying them to fund managers.

This guide breaks down exactly how Vanguard index funds work, which options align with different investment goals, and the mathematical reasons they’ve become the foundation of evidence-based portfolios. Whether starting with $1,000 or $100,000, understanding these vehicles is essential to building wealth through compound growth and systematic investing.

Key Takeaways

- Vanguard index funds track market indexes (like the S&P 500) instead of trying to beat them, providing instant diversification across hundreds or thousands of securities.

- Expense ratios matter enormously: Vanguard’s 0.03-0.05% fees versus industry averages of 0.50%+ create a 0.45% annual advantage that compounds to six-figure differences over decades.

- Four core fund types cover complete portfolios: Total stock market funds (VTSAX/VTI), S&P 500 funds (VFIAX/VOO), international funds (VTIAX/VXUS), and bond funds (VBTLX/BND) provide building blocks for any allocation strategy.

- Mutual fund vs ETF versions offer flexibility: The same underlying holdings available as traditional mutual funds (requiring $1,000-$3,000 minimums) or ETFs (tradable for the price of one share)

- Passive indexing wins through math: Lower costs + tax efficiency + full market participation = higher net returns than 90%+ of active managers over time.

What Are Vanguard Index Funds?

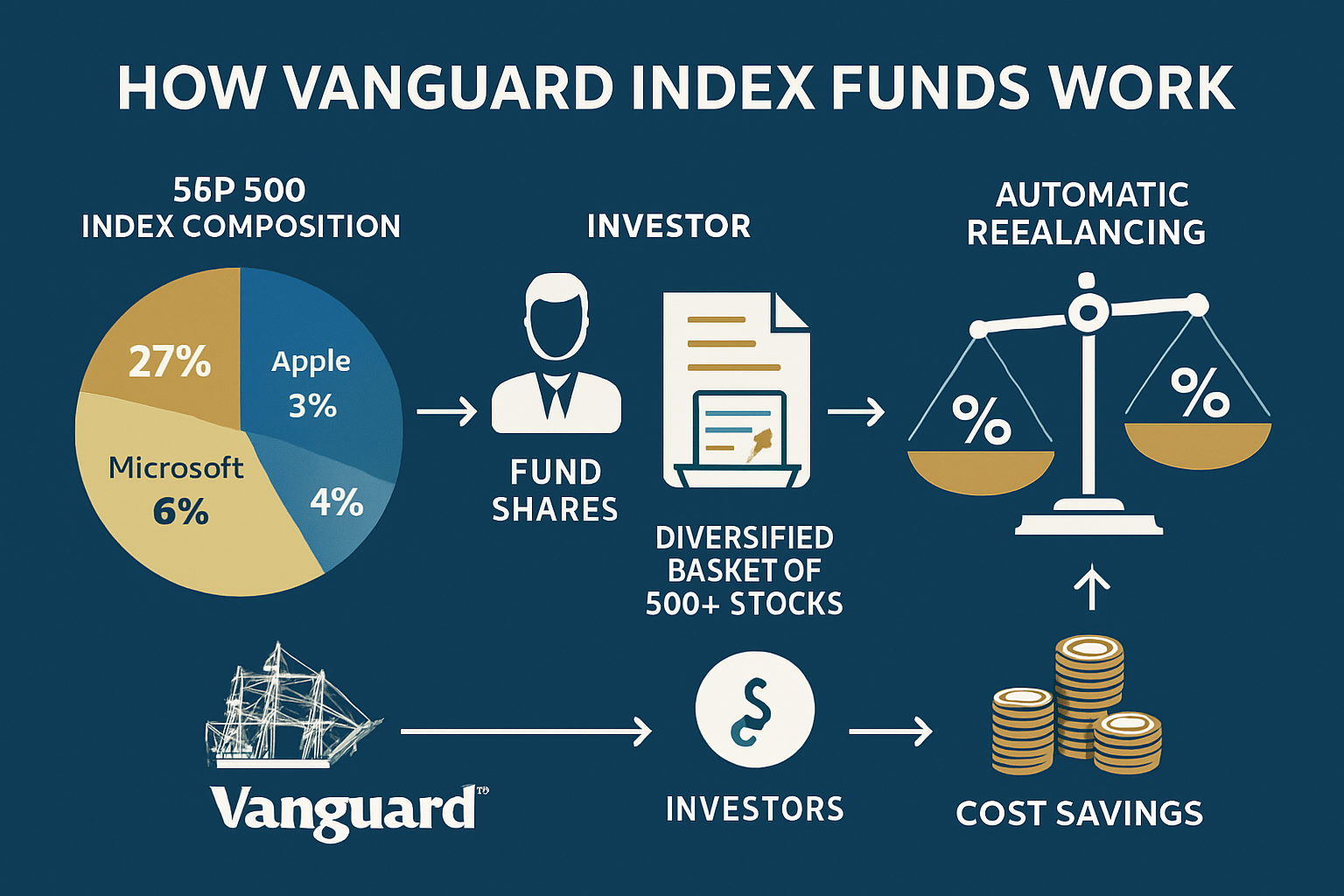

A Vanguard index fund is an investment vehicle that owns a predetermined basket of stocks or bonds designed to mirror the performance of a specific market index.

Instead of employing analysts to pick “winning” securities, these funds use a rules-based approach: If a stock is in the S&P 500, the fund buys it in proportion to its market capitalization. If a company gets removed from the index, the fund sells it. This mechanical process eliminates the need for expensive research teams and active trading.

The fundamental difference from actively managed funds: Active managers attempt to outperform the market through security selection and market timing. Index funds accept market returns as the target, recognizing that market efficiency makes consistent outperformance mathematically improbable after accounting for fees and taxes.

Vanguard pioneered this approach in 1976 when founder John Bogle launched the First Index Investment Trust (now the Vanguard 500 Index Fund). The investment community initially dismissed it as “un-American” for settling for average returns. The math proved otherwise.

Why Index Tracking Matters

Market indexes serve as performance benchmarks representing specific segments of the investment universe. The S&P 500 tracks 500 large U.S. companies. The Total Stock Market Index includes every publicly traded U.S. stock—over 4,000 securities. The Total Bond Market Index covers U.S. investment-grade bonds.

When a fund tracks an index, it provides:

- Transparency: Investors know exactly what they own at all times

- Predictability: Performance will match the index minus small tracking errors

- Diversification: A Single fund purchase provides exposure to hundreds or thousands of securities

- Cost efficiency: Minimal trading and no research expenses

The alternative—active management—requires investors to believe their chosen manager possesses superior skill, will maintain that skill over decades, and will generate excess returns large enough to overcome higher fees. Historical data shows this combination rarely materializes [2].

How Vanguard Index Funds Work

Understanding the mechanics behind index funds reveals why they consistently outperform more complex alternatives.

What Indexes Do They Track?

Vanguard offers index funds covering virtually every investable market segment:

U.S. Stock Market Indexes

- S&P 500: 500 large-cap U.S. companies representing approximately 80% of U.S. market capitalization

- Total Stock Market: Every publicly traded U.S. stock, from mega-cap technology companies to small-cap regional banks

- Extended Market: Mid-cap and small-cap stocks not included in the S&P 500

- Dividend Appreciation: Companies with histories of consistent dividend growth

International Stock Indexes

- Total International Stock: Developed and emerging market stocks outside the United States

- Developed Markets: Europe, Japan, Australia, and other developed economies

- Emerging Markets: China, India, Brazil, and other developing economies

Bond Market Indexes

- Total Bond Market: U.S. investment-grade bonds, including government, corporate, and mortgage-backed securities

- Short-Term Bond: Bonds with 1-5 year maturities

- Intermediate-Term Bond: Bonds with 5-10 year maturities

- Long-Term Bond: Bonds with 10+ year maturities

Each index follows specific rules for inclusion, weighting, and rebalancing. The S&P 500, for example, requires companies to meet profitability criteria, minimum market capitalization thresholds, and liquidity standards. Index providers (like S&P Dow Jones and FTSE Russell) maintain these rules, and Vanguard’s funds mechanically follow them.

How Fund Ownership Works

When purchasing shares of a Vanguard index fund, investors buy proportional ownership in the fund’s entire portfolio.

Net Asset Value (NAV) represents the per-share price, calculated daily:

NAV = (Total Assets – Total Liabilities) / Shares Outstanding

For example, if a fund holds $10 billion in stocks and has 100 million shares outstanding, the NAV equals $100 per share. Investors buying one share at $100 own $100 worth of the fund’s underlying securities.

Mutual fund transactions occur once daily after markets close. All investors buying or selling that day receive the same NAV price, regardless of when during the day they place their order. This differs from ETFs, which trade continuously throughout the day at market-determined prices.

Rebalancing maintains index alignment. When an index adds or removes securities, the fund executes corresponding trades. When market movements cause individual holdings to drift from target weights, the fund adjusts. This happens systematically, minimizing trading costs through careful execution.

The fund continuously reinvests dividends and interest payments unless investors elect cash distributions. This automatic reinvestment accelerates compound growth without requiring manual intervention.

Why Vanguard’s Structure Keeps Costs Low

Vanguard operates under a unique ownership structure that creates inherent cost advantages.

Investor ownership: Vanguard funds own the Vanguard Group. This means fund shareholders collectively own the management company. There are no external shareholders demanding profits, no private equity owners extracting value, and no public market pressures to maximize revenue.

This structure creates a mathematical certainty: Every dollar saved in operating expenses flows directly to investors through lower expense ratios.

Expense ratio comparison (2025 data):

| Fund Type | Industry Average | Vanguard Average | Annual Savings on $100,000 |

|---|---|---|---|

| Stock Index Fund | 0.47% | 0.04% | $430 |

| Bond Index Fund | 0.37% | 0.05% | $320 |

| International Stock Fund | 0.71% | 0.08% | $630 |

These differences compound dramatically over time. A $100,000 investment growing at 8% annually for 30 years becomes:

- At 0.04% expense ratio: $983,000

- At 0.47% expense ratio: $817,000

- Difference: $166,000 (20% more wealth from lower fees alone)

Vanguard achieves these low costs through:

- Economies of scale: $8+ trillion in assets under management spreads fixed costs across massive asset bases

- Index methodology: No expensive research teams, no active trading costs

- Operational efficiency: Automated processes, minimal marketing expenses

- At-cost operation: No profit motive beyond covering operational expenses

This isn’t marketing—it’s structural mathematics. The investor-owned model mathematically guarantees cost advantages that compound into substantial wealth differences over investment lifetimes.

Vanguard Index Funds vs ETFs

Vanguard offers most index strategies in two formats: traditional mutual funds and exchange-traded funds (ETFs). Both track identical indexes and hold the same underlying securities, but they differ in structure and mechanics.

Mutual Funds vs ETFs

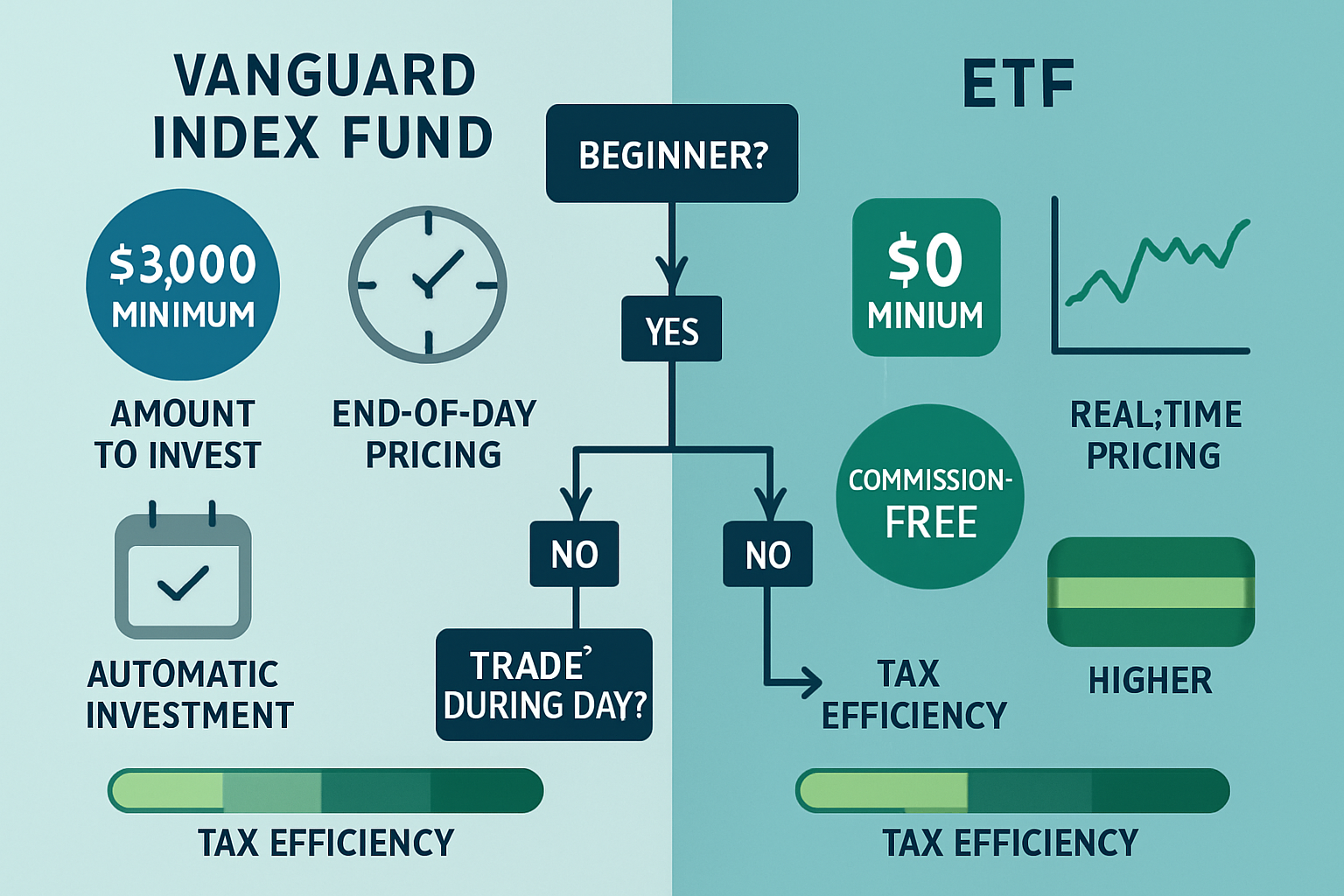

Traditional Index Mutual Funds

- Trading: Execute once daily at NAV after market close (4:00 PM ET)

- Pricing: Single price for all transactions that day

- Minimum investment: Typically $1,000-$3,000 for initial purchase

- Subsequent purchases: Can invest any dollar amount

- Automatic investing: Easy to set up recurring investments

- Fractional shares: Automatically purchased with exact dollar amounts

- Tax efficiency: Highly efficient but slightly less than the ETF structure

Exchange-Traded Funds (ETFs)

- Trading: Continuous throughout market hours, like stocks

- Pricing: Real-time market prices that fluctuate minute-to-minute

- Minimum investment: Price of one share (often $50-$300)

- Subsequent purchases: Must buy whole shares

- Automatic investing: Possible but more complex

- Fractional shares: Not available at most brokerages

- Tax efficiency: Slightly higher due to the in-kind redemption structure

The tax efficiency difference stems from how each structure handles investor redemptions. When mutual fund investors sell shares, the fund may need to sell underlying securities, potentially triggering capital gains distributed to remaining shareholders. ETFs use an “in-kind” redemption process that transfers securities to authorized participants without triggering taxable events [3].

For Vanguard funds specifically, this difference is minimal. Vanguard’s patented structure allows its mutual funds to benefit from ETF tax advantages, making the tax efficiency gap negligible for most investors.

Which Is Better for Beginners?

The optimal choice depends on investment approach and account size:

Choose mutual funds (like VTSAX, VFIAX, VBTLX) if:

- Building wealth through systematic monthly contributions

- Starting with less than $3,000 but planning regular additions

- Preferring the simplicity of dollar-based investing

- Setting up automatic investment plans

- Avoiding the temptation to check prices throughout the day

Choose ETFs (like VTI, VOO, BND) if:

- Starting with smaller initial amounts (under $1,000)

- Comfortable buying whole shares only

- Not planning regular automatic contributions

- Wanting intraday trading flexibility (though rarely beneficial)

- Maximizing tax efficiency in taxable accounts

For most beginner investors following evidence-based strategies, mutual funds offer practical advantages. The ability to invest exact dollar amounts, automate contributions, and avoid intraday price monitoring aligns with disciplined wealth building.

The mathematical impact on returns is negligible. A $10,000 investment in VTSAX (mutual fund) versus VTI (ETF) will produce virtually identical results over time. The 0.03% expense ratio is identical, the holdings are identical, and the performance will track within basis points.

Focus on the behavior enablers rather than microscopic structural differences. The format that makes consistent investing easiest is the format that will generate superior long-term results.

For more detailed analysis, see our guide on the best index funds and best ETFs to buy.

Best Vanguard Index Funds

Vanguard offers dozens of index funds, but four core options provide building blocks for complete portfolios across different investment objectives.

Best for Total Market Exposure

Vanguard Total Stock Market Index Fund

- Mutual Fund: VTSAX (Admiral Shares)

- ETF: VTI

- Expense Ratio: 0.04%

- Minimum Investment: $3,000 (mutual fund), ~$250 (ETF, one share)

- Holdings: 4,000+ U.S. stocks across all capitalizations

This fund owns the entire U.S. stock market in a single investment. Large-cap technology giants like Apple and Microsoft sit alongside mid-cap industrial companies and small-cap regional businesses. Weighting follows market capitalization, meaning larger companies represent larger portfolio percentages.

Who should invest: Investors seeking maximum U.S. stock diversification without making capitalization bets. This serves as a complete U.S. equity allocation in one fund.

Historical performance: 10-year annualized return of approximately 12.5% through 2024 [4]. This matches the overall U.S. stock market because the fund is the overall U.S. stock market.

Risk considerations: Full exposure to U.S. equity market volatility. During the 2020 market decline, VTSAX dropped 34% from peak to trough. During the 2022 bear market, it declined 25%. These drawdowns are features, not bugs—they represent the volatility required to generate long-term equity returns.

Best for S&P 500 Exposure

Vanguard 500 Index Fund

- Mutual Fund: VFIAX (Admiral Shares)

- ETF: VOO

- Expense Ratio: 0.04%

- Minimum Investment: $3,000 (mutual fund), ~$500 (ETF, one share)

- Holdings: 500 large-cap U.S. stocks

The original Vanguard index fund, launched in 1976, remains one of the most popular investment vehicles globally. It tracks the S&P 500, representing approximately 80% of U.S. stock market capitalization.

Who should invest: Investors wanting large-cap U.S. exposure with a 50-year track record. The S&P 500 serves as the benchmark most professional investors fail to beat, making it a logical default equity allocation.

Historical performance: 10-year annualized return of approximately 13.0% through 2024 [5]. Slightly higher than the total market due to large-cap concentration, though differences are minimal over long periods.

VTSAX vs VFIAX: These funds correlate at 0.99+. VTSAX includes mid-cap and small-cap stocks that VFIAX excludes, providing slightly broader diversification. Performance differences over decades are measured in basis points. Choose based on preference, not expected return differences.

Best for International Investing

Vanguard Total International Stock Index Fund

- Mutual Fund: VTIAX (Admiral Shares)

- ETF: VXUS

- Expense Ratio: 0.08%

- Minimum Investment: $3,000 (mutual fund), ~$65 (ETF, one share)

- Holdings: 8,000+ stocks across developed and emerging markets

This fund provides exposure to every significant stock market outside the United States, including Europe, Japan, China, emerging markets, and developed Asia-Pacific countries.

Who should invest: Investors implementing geographic diversification beyond U.S.-only portfolios. International stocks provide different economic exposures, currency diversification, and access to companies dominating industries underrepresented in U.S. markets.

Historical performance: 10-year annualized return of approximately 5.5% through 2024 [6]. International stocks have underperformed U.S. markets over the past decade, but performance leadership rotates over longer periods. From 2000-2010, international stocks significantly outperformed U.S. markets.

Allocation considerations: Common approaches include 60/40 U.S./international, 70/30, or 80/20 splits. The mathematically optimal allocation remains debated, but complete home-country bias (100% U.S.) concentrates geographic and economic risk.

For more on building diversified portfolios, see our guide on diversification investing strategies.

Best for Bonds

Vanguard Total Bond Market Index Fund

- Mutual Fund: VBTLX (Admiral Shares)

- ETF: BND

- Expense Ratio: 0.05%

- Minimum Investment: $3,000 (mutual fund), ~$75 (ETF, one share)

- Holdings: 10,000+ U.S. investment-grade bonds

This fund owns the entire U.S. investment-grade bond market, including government bonds, corporate bonds, and mortgage-backed securities across various maturities.

Who should invest: Investors adding fixed-income allocation for volatility reduction, capital preservation, or portfolio ballast during equity market declines. Bonds provide income and typically decline less than stocks during recessions.

Historical performance: 10-year annualized return of approximately 1.8% through 2024 [7]. Bond returns consist of interest income minus price changes from interest rate movements. Rising rate environments (like 2022-2023) create negative returns; falling rate environments create positive returns beyond yield.

Risk considerations: Bond funds carry interest rate risk (prices fall when rates rise), credit risk (borrowers may default), and inflation risk (fixed payments lose purchasing power). Total bond market funds minimize credit risk through investment-grade requirements and diversification across thousands of issuers.

Allocation framework: Traditional 60/40 stock/bond portfolios allocate 60% to stock funds (VTSAX, VFIAX) and 40% to bond funds (VBTLX). More aggressive investors use 80/20 or 90/10. Conservative investors use 40/60 or 50/50. The optimal allocation depends on time horizon, risk tolerance, and income needs.

Comparison Table: Core Vanguard Index Funds

| Fund | Ticker (MF/ETF) | Expense Ratio | Asset Class | Risk Level | Min Investment | 10-Yr Return* |

|---|---|---|---|---|---|---|

| Total Stock Market | VTSAX / VTI | 0.04% | U.S. Stocks (All Cap) | High | $3,000 / ~$250 | ~12.5% |

| 500 Index | VFIAX / VOO | 0.04% | U.S. Stocks (Large Cap) | High | $3,000 / ~$500 | ~13.0% |

| Total International | VTIAX / VXUS | 0.08% | International Stocks | High | $3,000 / ~$65 | ~5.5% |

| Total Bond Market | VBTLX / BND | 0.05% | U.S. Bonds | Low-Medium | $3,000 / ~$75 | ~1.8% |

*Approximate annualized returns through 2024; past performance doesn’t guarantee future results

Pros and Cons of Vanguard Index Funds

Evidence-based investing requires understanding both advantages and limitations. Vanguard index funds excel in specific dimensions while accepting tradeoffs inherent to passive indexing.

Advantages

1. Mathematically Superior Cost Structure

Expense ratios of 0.03-0.08% versus industry averages of 0.50%+ create compounding advantages. On a $500,000 portfolio over 30 years, this difference equals $200,000+ in additional wealth retained by investors rather than paid to fund managers.

The math is simple: Returns = Market Return – Costs – Taxes. Minimizing costs mathematically increases net returns when market returns and tax efficiency remain constant.

2. Instant Diversification

Single fund purchases provide exposure to thousands of securities. VTSAX owns 4,000+ stocks. VBTLX owns 10,000+ bonds. This diversification eliminates company-specific risk (the risk that individual holdings go bankrupt or underperform).

Diversification doesn’t eliminate market risk—the risk that entire markets decline. It eliminates the unnecessary risk of concentrated positions.

3. Consistent Long-Term Performance

Index funds don’t outperform markets. They match markets minus minimal expenses. This sounds mediocre until recognizing that matching the market means outperforming 90%+ of active managers over 15-year periods [1].

The S&P 500 has delivered approximately 10% annualized returns over the past century. Capturing 9.96% (after 0.04% expenses) beats capturing 8.5% (after 1.5% active management fees and underperformance).

4. Tax Efficiency

Index funds trade infrequently, minimizing capital gains distributions. Active funds average turnover rates of 60-100% annually, triggering taxes on gains. Index funds average 3-5% turnover, occurring only when index composition changes.

In taxable accounts, this creates substantial after-tax return advantages. Tax-deferred accounts (IRAs, 401(k)s) neutralize this benefit since all growth is tax-deferred regardless of turnover.

5. Behavioral Simplicity

Index funds remove the temptation to chase performance, time markets, or second-guess holdings. The investment decision simplifies to allocation (what percentage in stocks vs bonds) rather than selection (which stocks or managers to pick).

This simplicity prevents costly behavioral mistakes. Research shows individual investors underperform the funds they own by 2-3% annually due to poor timing decisions [8]. Index funds reduce opportunities for these mistakes.

Disadvantages & Risks

1. No Downside Protection

Index funds own the market. When markets decline 30%, index funds decline 30%. No manager is making defensive moves, no cash position providing cushion, no tactical allocation reducing exposure.

This is a feature for long-term investors (staying fully invested maximizes compound growth) but a drawback for those needing capital preservation during specific periods.

2. Market Volatility Exposure

Stock index funds experience full equity market volatility. Historical maximum drawdowns:

- 1929-1932: -86%

- 1973-1974: -48%

- 2000-2002: -49%

- 2007-2009: -57%

- 2020: -34%

- 2022: -25%

Investors must possess the psychological capacity to maintain positions through these declines. Those who sell during drawdowns lock in losses and miss recoveries.

3. Not Ideal for Short-Term Goals

Money needed within 3-5 years shouldn’t be invested in stock index funds. Volatility creates unacceptable risk that values will be down when funds are needed.

Bond index funds provide more stability for intermediate-term goals (3-7 years). High-yield savings accounts or short-term bond funds suit goals under 3 years. For recommendations, see our guide on the best high-yield savings accounts.

4. Index Inclusion Inefficiencies

Index funds must buy stocks when they’re added to indexes and sell when they’re removed. This creates predictable trading patterns that other investors exploit, potentially causing index funds to buy high and sell low at reconstitution events.

Research suggests this costs index investors 0.10-0.20% annually [9]. This remains far less than active management fees but represents a real inefficiency.

5. No Outperformance Potential

Index funds will never beat the market. They will match the market minus small expenses. Investors seeking market-beating returns must look elsewhere.

The counterargument: Seeking outperformance is rational only if the probability-weighted expected outcome exceeds passive indexing. Given that 90%+ of active managers underperform over 15 years, the odds favor accepting market returns rather than attempting to beat them.

How to Choose the Right Vanguard Index Fund

Selecting appropriate index funds requires matching investment vehicles to specific financial circumstances rather than chasing past performance or following trends.

Based on Time Horizon

The investment timeline fundamentally determines appropriate asset allocation.

0-3 Years (Short-Term)

- Primary allocation: High-yield savings accounts, money market funds

- Vanguard option: Vanguard Treasury Money Market Fund (VUSXX)

- Rationale: Capital preservation trumps growth for near-term needs

3-7 Years (Intermediate-Term)

- Primary allocation: Short-term or intermediate-term bond funds, conservative balanced funds

- Vanguard options: Vanguard Short-Term Bond Index (VBIRX/BSV), Vanguard Intermediate-Term Bond Index (VBILX/BIV)

- Rationale: Moderate volatility is acceptable, but full equity risk is inappropriate

7-15 Years (Medium-Term)

- Primary allocation: Balanced stock/bond portfolio (60/40 to 80/20)

- Vanguard options: 60% VTSAX + 20% VTIAX + 20% VBTLX

- Rationale: Sufficient time to recover from equity declines while bonds provide ballast

15+ Years (Long-Term)

- Primary allocation: Aggressive stock allocation (80/20 to 100% stocks)

- Vanguard options: 70% VTSAX + 30% VTIAX, or 100% VTSAX

- Rationale: Maximum growth potential, time to weather volatility

The mathematical foundation: Stocks provide higher expected returns with higher volatility. Longer time horizons allow volatility to average out while compound growth accumulates. Shorter horizons create the risk that volatility produces losses when capital is needed.

Based on Risk Tolerance

Risk tolerance represents the psychological capacity to maintain positions during market declines.

Conservative (Cannot tolerate 20%+ declines)

- Allocation: 40/60 or 50/50 stocks/bonds

- Vanguard portfolio: 40% VTSAX + 10% VTIAX + 50% VBTLX

- Expected volatility: 10-12% annual standard deviation

- Historical max drawdown: -25% to -30%

Moderate (Can tolerate 20-35% declines)

- Allocation: 60/40 or 70/30 stocks/bonds

- Vanguard portfolio: 50% VTSAX + 20% VTIAX + 30% VBTLX

- Expected volatility: 12-15% annual standard deviation

- Historical max drawdown: -35% to -45%

Aggressive (Can tolerate 40%+ declines)

- Allocation: 80/20 or 90/10 or 100% stocks

- Vanguard portfolio: 70% VTSAX + 30% VTIAX

- Expected volatility: 15-20% annual standard deviation

- Historical max drawdown: -50% to -60%

Critical insight: Risk tolerance should be tested against actual dollar amounts, not percentages. Seeing a $500,000 portfolio decline to $300,000 creates a different psychological impact than conceptualizing “40% decline.”

Consider this framework: What portfolio decline would cause you to sell in panic? Reduce stock allocation until maximum historical drawdowns fall below that threshold.

For more on managing investment psychology, see our analysis of the cycle of market emotions.

Based on Account Type (IRA vs Brokerage)

Account type influences optimal fund selection due to tax treatment differences.

Tax-Deferred Accounts (Traditional IRA, 401(k), 403(b))

- Tax treatment: Contributions may be tax-deductible; growth is tax-deferred; withdrawals are taxed as ordinary income

- Optimal holdings: Tax-inefficient assets (bonds, REITs, actively managed funds if used)

- Vanguard recommendation: VBTLX (bonds generate ordinary income), dividend-focused funds

- Rationale: Tax-deferred growth shelters interest and dividend income from annual taxation

Tax-Free Accounts (Roth IRA, Roth 401(k))

- Tax treatment: Contributions from after-tax income; growth is tax-free; qualified withdrawals are tax-free

- Optimal holdings: Highest-growth-potential assets

- Vanguard recommendation: VTSAX, VTIAX (maximize tax-free growth on highest-return assets)

- Rationale: Tax-free compounding is most valuable on assets with the highest expected returns

Taxable Brokerage Accounts

- Tax treatment: Dividends and interest are taxed annually; capital gains are taxed when realized

- Optimal holdings: Tax-efficient stock index funds, ETF versions for maximum efficiency

- Vanguard recommendation: VTI, VXUS (ETF versions), tax-managed funds

- Rationale: Minimize annual tax drag through low turnover and qualified dividend treatment

Tax-loss harvesting opportunity: In taxable accounts, market declines create opportunities to sell positions at losses, realize those losses for tax deductions, and immediately repurchase similar (but not identical) funds. For example, selling VTI at a loss and buying VTSAX (or vice versa) maintains market exposure while capturing tax benefits.

This strategy can generate 0.50-1.00% annual tax alpha for high-income investors [10]. For more on tax-efficient investing, see our guide on capital gains tax.

Are Vanguard Index Funds Good for Beginners?

Vanguard index funds represent optimal starting points for most beginning investors due to simplicity, low costs, and alignment with evidence-based investing principles.

Who They’re Best For

Ideal candidates for Vanguard index fund investing:

1. Long-term wealth builders with 10+ year time horizons who can tolerate short-term volatility for long-term growth. Index funds excel at capturing market returns over decades, making them perfect for retirement investing, generational wealth building, and long-term financial independence.

2. Investors seeking simplicity who prefer straightforward portfolios over complex strategies. A three-fund portfolio (U.S. stocks, international stocks, bonds) provides complete diversification without requiring ongoing research, monitoring, or rebalancing beyond annual adjustments.

3. Cost-conscious investors who recognize that minimizing expenses mathematically increases net returns. Vanguard’s expense ratios of 0.03-0.08% versus industry averages of 0.50%+ create compounding advantages worth hundreds of thousands over investment lifetimes.

4. Evidence-based decision makers who accept that markets are largely efficient and that consistent outperformance is statistically improbable. Index investing aligns with academic research, Nobel Prize-winning financial theory, and empirical evidence from decades of performance data.

5. Behavioral investors who benefit from “set and forget” strategies that prevent emotional decision-making. Index funds remove the temptation to chase hot stocks, time markets, or abandon strategies during volatility.

Who Should Avoid Them

Vanguard index funds are suboptimal for:

1. Short-term savers needing money within 3 years. Stock market volatility creates unacceptable risk for near-term goals. High-yield savings accounts, CDs, or money market funds provide appropriate vehicles for short-term capital.

2. Active traders seeking frequent trading opportunities or intraday price movements. Index funds are designed for buy-and-hold investing, not trading. Those seeking trading vehicles should consider individual stocks or leveraged ETFs (though evidence suggests active trading destroys wealth for most participants).

3. Income-focused retirees requiring high current income. While index funds pay dividends, dedicated dividend funds or individual dividend stocks may provide higher yields. However, total return (dividends plus growth) typically matters more than yield alone. For dividend strategies, see our guides on dividend investing and best dividend ETFs.

4. Investors unable to tolerate volatility psychologically. If seeing portfolio declines of 30-50% would cause panic selling, index funds may be inappropriate regardless of time horizon. Conservative balanced funds or stable value options better match risk tolerance.

5. Those seeking outperformance who believe they can identify superior managers or strategies. Index funds will never beat the market. Investors convinced they can achieve above-market returns through selection or timing should pursue those strategies (while recognizing the statistical odds favor passive indexing).

Common Beginner Mistakes

Mistake #1: Chasing recent performance

Investors frequently choose funds based on recent returns, buying what’s performed well and avoiding what’s lagged. This creates a buy-high, sell-low pattern.

Example: International stocks (VTIAX) underperformed U.S. stocks (VTSAX) from 2010-2020, leading many investors to abandon international exposure. From 2000-2010, international stocks significantly outperformed, and performance leadership will likely rotate again.

Solution: Maintain diversified allocations regardless of recent performance. Rebalancing forces buying underperforming assets and selling outperforming assets—the opposite of chasing returns.

Mistake #2: Overcomplicating portfolios

Beginners sometimes build portfolios with 10-15 different index funds, believing that more funds equal better diversification.

Reality: VTSAX alone provides exposure to 4,000+ stocks. Adding multiple overlapping funds (large-cap fund + mid-cap fund + small-cap fund) creates complexity without meaningful diversification benefits.

Solution: Start with 2-4 core funds maximum. A simple portfolio might be: 60% VTSAX + 20% VTIAX + 20% VBTLX. This provides complete diversification with minimal complexity.

Mistake #3: Abandoning strategy during volatility

Market declines trigger fear, leading investors to sell index funds “to avoid further losses.” This locks in losses and misses recoveries.

Historical pattern: Every major market decline in history has been followed by recovery to new highs. Investors who maintained positions recovered. Those who sold often missed rebounds.

Solution: Build portfolios aligned with risk tolerance before volatility occurs. If declines trigger panic, the portfolio was too aggressive. Adjust allocation to enable staying invested through downturns.

Mistake #4: Neglecting tax efficiency

Beginners often place tax-inefficient assets (bonds) in Roth IRAs and tax-efficient assets (stock index funds) in taxable accounts—the opposite of optimal placement.

Solution: Follow the account-type framework outlined earlier. Maximize tax-free growth on the highest-return assets in Roth accounts. Shelter tax-inefficient income in tax-deferred accounts. Use tax-efficient stock index ETFs in taxable accounts.

Mistake #5: Failing to automate

Relying on manual investing creates inconsistency. Some months get skipped. Market volatility causes hesitation. Automation removes these barriers.

Solution: Set up automatic monthly contributions from checking accounts to investment accounts. Use dollar-cost averaging to systematically invest regardless of market conditions. This builds discipline and captures compound growth consistently.

How to Start Investing in Vanguard Index Funds

Converting knowledge into action requires following a systematic implementation process.

Step 1: Open a Vanguard Account

Account types available:

- Individual brokerage account: Taxable account for general investing

- Joint brokerage account: A Taxable account owned by two people

- Traditional IRA: Tax-deferred retirement account (contributions may be deductible)

- Roth IRA: Tax-free retirement account (contributions from after-tax income)

- SEP IRA: Retirement account for self-employed individuals

- Rollover IRA: Account for transferring 401(k) funds from former employers

Opening process:

- Visit Vanguard.com and select “Open an account.”

- Choose an account type based on tax treatment and purpose

- Provide personal information (name, address, Social Security number, employment)

- Answer regulatory questions (investment experience, risk tolerance, time horizon)

- Link bank account for electronic transfers

- Fund account via electronic transfer, check, or rollover

Account minimums: Most Vanguard index funds require $1,000-$3,000 minimum initial investment for mutual fund versions. ETF versions have no minimums beyond the price of one share.

Alternative: Investors can open accounts at other brokerages (Fidelity, Schwab, etc.) and purchase Vanguard ETFs commission-free. This provides access to Vanguard index funds without opening Vanguard accounts, though purchasing Vanguard mutual funds at other brokerages may incur transaction fees.

Step 2: Choose Fund vs ETF

Decision framework:

Choose mutual fund versions (VTSAX, VFIAX, VTIAX, VBTLX) if:

- Meeting minimum investment requirements ($1,000-$3,000)

- Planning systematic monthly contributions

- Preferring dollar-based investing over share-based

- Setting up automatic investment plans

- Avoiding intraday price monitoring

Choose ETF versions (VTI, VOO, VXUS, BND) if:

- Starting with smaller amounts (under the minimum requirements)

- Comfortable buying whole shares only

- Not planning automatic recurring investments

- Wanting maximum tax efficiency in taxable accounts

- Already using a brokerage other than Vanguard

Performance equivalence: VTSAX and VTI track the same index, hold identical securities, and charge identical expense ratios. Long-term returns will be virtually identical. Choose based on practical considerations, not expected performance differences.

Step 3: Automate Contributions

Systematic investing creates discipline and maximizes compound growth.

Setting up automatic investments:

- Log in to your Vanguard account

- Navigate to “Automatic investments” under account settings

- Select source account (bank account or settlement fund)

- Choose destination fund (VTSAX, VFIAX, etc.)

- Set investment amount and frequency (monthly recommended)

- Select start date and end date (if applicable)

Recommended approach: Invest a fixed dollar amount monthly regardless of market conditions. This implements dollar-cost averaging, buying more shares when prices are low and fewer when prices are high.

Contribution amounts: Determine sustainable monthly investment based on budget and goals. Even $100-$500 monthly creates substantial wealth over decades through compound growth.

Example: $500 monthly invested in VTSAX at 10% annual returns for 30 years = $1,028,000

The math behind wealth building is simple: Consistent contributions + time + compound growth = financial independence. For more on systematic wealth building, see our guide on the 4% rule for retirement planning.

Rebalancing: Set a calendar reminder to review portfolio allocation annually. If the target allocation was 70/30 stocks/bonds and market movements have shifted it to 80/20, sell stocks and buy bonds to restore the target. This maintains risk level and forces buying low/selling high.

📊 Vanguard Index Fund Portfolio Builder

Build your personalized Vanguard index fund allocation based on your investment profile

Your Investment Profile

Your Recommended Portfolio

Conclusion

Vanguard index funds represent the mathematical optimization of wealth building: maximum diversification, minimum costs, and alignment with evidence demonstrating that market returns beat 90%+ of active managers over time.

The core insight is simple. Markets are efficient enough that consistent outperformance is statistically improbable after accounting for fees and taxes. Index funds accept this reality and capture market returns at minimal cost. The result: superior net returns for investors who maintain discipline through market cycles.

For beginners, the implementation path is clear:

- Start with core building blocks: VTSAX (or VTI) for U.S. stocks, VTIAX (or VXUS) for international diversification, VBTLX (or BND) for bond allocation

- Match allocation to time horizon and risk tolerance: Longer timelines and higher risk tolerance support higher stock allocations; shorter timelines and lower risk tolerance require more bonds

- Automate monthly contributions: Systematic investing removes emotional decision-making and maximizes compound growth through consistent participation

- Maintain discipline through volatility: Market declines are temporary; abandoning strategy during downturns locks in losses and misses recoveries.

- Minimize costs and taxes: Use tax-advantaged accounts, place assets strategically, and avoid unnecessary trading.

The mathematics of index investing compounds into life-changing wealth differences. A $10,000 initial investment plus $500 monthly contributions over 30 years at 10% annual returns (roughly the historical stock market average) grows to $1,139,000. The same contributions in actively managed funds charging 1.5% total costs grow to $878,000—a $261,000 difference from the cost structure alone.

This isn’t theory. It’s arithmetic. Lower costs + consistent investing + time = wealth building that works.

Start with one fund if necessary. Add international and bond allocations as knowledge and capital grow. The perfect portfolio matters less than starting, maintaining consistency, and allowing compound growth to work over decades.

The math behind money favors those who understand it and act on it. Vanguard index funds provide the vehicle. Time and discipline provide the fuel. The destination—financial independence—becomes mathematically inevitable.

For next steps, explore our guides on best index funds, asset allocation strategies, and compound interest fundamentals.

Educational Disclaimer

This article is provided for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or personalized guidance tailored to individual circumstances.

Investing in index funds involves risk, including potential loss of principal. Past performance does not guarantee future results. Market values fluctuate, and investors may experience losses during market downturns.

Before making investment decisions, consider consulting with qualified financial advisors who can evaluate your specific financial situation, goals, risk tolerance, and time horizon. Tax implications vary based on individual circumstances and account types; consult tax professionals regarding your specific situation.

The Rich Guy Math provides educational content to help readers understand financial concepts and make informed decisions. We do not provide personalized investment advice or manage client assets.

All data, statistics, and performance figures represent historical information and should not be interpreted as predictions of future performance. Index fund returns will vary based on market conditions, and no investment strategy guarantees positive returns.

Author Bio

Max Fonji is the founder of The Rich Guy Math, a data-driven financial education platform dedicated to explaining the mathematical principles behind wealth building, investing, and risk management. With expertise in financial analysis and evidence-based investing strategies, Max translates complex financial concepts into clear, actionable insights for investors at all levels.

Max’s approach combines academic research, empirical data, and practical application to help readers understand how money actually works—through numbers, logic, and cause-and-effect relationships rather than hype or speculation.

The Rich Guy Math has helped thousands of investors build confidence through understanding, applying principles of compound growth, diversification, and evidence-based decision-making to achieve long-term financial goals.

References

[1] S&P Dow Jones Indices. (2024). “SPIVA U.S. Scorecard.” S&P Global. https://www.spglobal.com/spdji/en/research-insights/spiva/

[2] Malkiel, B. G. (2019). “A Random Walk Down Wall Street.” W.W. Norton & Company.

[3] Internal Revenue Service. (2024). “Investment Income and Expenses.” IRS Publication 550. https://www.irs.gov/publications/p550

[4] Vanguard. (2024). “Vanguard Total Stock Market Index Fund Performance.” Vanguard.com. https://investor.vanguard.com/investment-products/mutual-funds/profile/vtsax

[5] Vanguard. (2024). “Vanguard 500 Index Fund Performance.” Vanguard.com. https://investor.vanguard.com/investment-products/mutual-funds/profile/vfiax

[6] Vanguard. (2024). “Vanguard Total International Stock Index Fund Performance.” Vanguard.com. https://investor.vanguard.com/investment-products/mutual-funds/profile/vtiax

[7] Vanguard. (2024). “Vanguard Total Bond Market Index Fund Performance.” Vanguard.com. https://investor.vanguard.com/investment-products/mutual-funds/profile/vbtlx

[8] Dalbar, Inc. (2023). “Quantitative Analysis of Investor Behavior.” Dalbar Research.

[9] Morningstar. (2023). “The Hidden Costs of Index Investing.” Morningstar Investment Research.

[10] Arnott, R., Berkin, A., & Ye, J. (2001). “Loss Harvesting: What’s It Worth to the Taxable Investor?” Journal of Wealth Management, 3(4), 10-18.

Frequently Asked Questions

What is the minimum investment for Vanguard index funds?

Vanguard mutual fund minimums typically range from $1,000 to $3,000 for initial purchases. Admiral Shares, which offer lower expense ratios, generally require a $3,000 minimum.

Vanguard ETF versions have no account minimums. Investors can buy a single share at market price, usually between $50 and $500 depending on the fund.

Are Vanguard index funds good for retirement?

Yes. Vanguard index funds are well-suited for retirement investing due to their low costs, broad diversification, and long-term market-matching performance.

When held in tax-advantaged accounts like IRAs or 401(k)s, index funds allow compound growth to accumulate tax-deferred or tax-free over decades.

How do Vanguard index funds make money for investors?

Vanguard index funds generate returns through two primary mechanisms:

- Dividend and interest income from underlying holdings

- Capital appreciation as the value of securities rises over time

Total return reflects the combined effect of income distributions and price growth.

What is the difference between VTSAX and VTI?

VTSAX and VTI track the same Total Stock Market Index but are structured differently.

- VTSAX: Mutual fund, $3,000 minimum, trades once daily at NAV

- VTI: ETF, no minimum beyond one share, trades intraday

Holdings, expense ratios (0.04%), and long-term performance are effectively identical.

Can you lose money in Vanguard index funds?

Yes. Vanguard index funds offer no downside protection. When markets decline, fund values fall proportionally.

Historical drawdowns have exceeded 50% during severe bear markets. However, every major market decline has eventually recovered to new highs.

How often should I rebalance my Vanguard index fund portfolio?

Annual rebalancing is generally optimal. Review your allocation once per year and rebalance if an asset class drifts more than 5–10 percentage points from its target.

More frequent rebalancing can increase taxes and transaction costs without improving results.

Are Vanguard index funds better than Fidelity or Schwab index funds?

Vanguard, Fidelity, and Schwab all offer excellent low-cost index funds with comparable expense ratios, often ranging from 0.00% to 0.04%.

Performance differences are minimal. Choose based on overall brokerage features, account options, and customer service rather than small expense ratio differences.

Related posts:

Dividend Portfolio: How to Build One for Steady Passive Income

Dividend Portfolio: How to Build One for Steady Passive Income

Why Should You Invest? The Benefits of Long-Term Investing Explained

Why Should You Invest? The Benefits of Long-Term Investing Explained

What Is a Hedge Fund? How It Works, Strategies, and Risks Explained

What Is a Hedge Fund? How It Works, Strategies, and Risks Explained

Best Robo-Advisors in 2026: Top Picks & Comparison

Best Robo-Advisors in 2026: Top Picks & Comparison

Margin Investing: How It Works, Risks, Examples, and Smart Strategies

Margin Investing: How It Works, Risks, Examples, and Smart Strategies

Robinhood vs Fidelity: Which Brokerage Is Better for Investors?

Robinhood vs Fidelity: Which Brokerage Is Better for Investors?