Last updated: February 2026

You’re applying for an apartment. Or maybe financing a car. Or trying to get approved for your first credit card. At some point, someone tells you, “You need good credit.” But when you ask what number that actually means, the answers get vague fast.

Here’s the direct answer: a good credit score is not a single magic number. It’s a risk category that lenders use to predict how reliably a borrower will repay debt. Under the most widely used FICO scoring model, a score of 670 or higher is generally classified as “good” [1]. But different lenders set different thresholds, and approval depends on more than just your score.

If you’re new to how borrowing works, start with our complete guide to how credit works before focusing on numbers.

This guide breaks down the exact score ranges, explains what lenders in different industries actually require, and clarifies what score you realistically need for common financial goals in 2026. No hype, no vague promises, just the math behind money and how credit scoring actually works.

TL;DR: What Is a Good Credit Score?

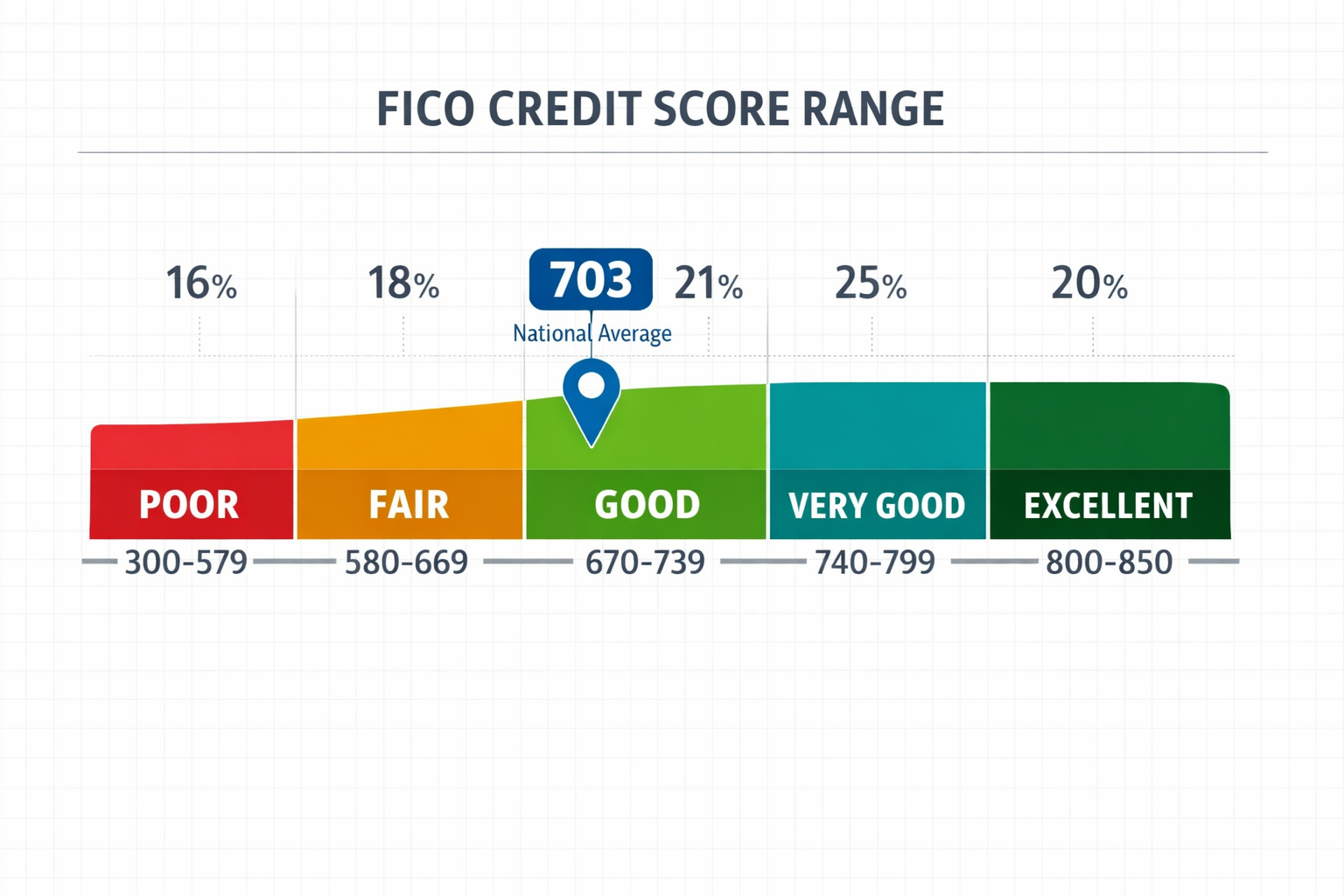

- A FICO score of 670–739 is considered “good.” Scores of 740+ are “very good” or “excellent” [1][3].

- The national average credit score is 703 as of late 2025, which falls in the “good” range [4].

- There is no universal approval number. Mortgage, auto, and credit card lenders all use different minimums.

- A good score gets you lower interest rates, better approval odds, and reduced deposits, but lenders also weigh income, debt ratios, and payment history.

- Building from fair to good credit typically takes 3–9 months of consistent financial behavior.

What Is a Good Credit Score?

A credit score of 670 to 739 is classified as “good” under the FICO scoring model, which is the model used by roughly 90% of top U.S. lenders [1][3]. Scores in this range signal to lenders that a borrower is a relatively low risk, meaning they’re more likely to repay on time and less likely to default.

For context, the national average FICO score stood at 703 as of December 2025, which sits comfortably in the “good” tier [4]. That average has declined slightly from a record high of 718 in 2023 [4], but it still means most Americans carry scores that qualify for reasonable lending terms.

Insight: “Good” is not the top tier. It’s the middle-upper range. Borrowers with scores of 740+ unlock the best interest rates and terms, while those below 670 face higher costs or potential denials.

Credit Score Ranges: The Full FICO Breakdown

Every FICO score falls on a scale from 300 to 850. Both FICO and VantageScore use this same 300–850 range [1], though the boundaries for each category differ slightly between models.

Here is the standard FICO classification:

| Score Range | Rating | What It Means for Borrowers |

|---|---|---|

| 800–850 | Excellent | Best rates, highest approval odds, premium offers |

| 740–799 | Very Good | Near-best rates, strong approval likelihood |

| 670–739 | Good | Competitive rates, solid approval chances |

| 580–669 | Fair | Higher rates, limited options, possible denials |

| 300–579 | Poor | Frequent denials, secured products only, highest rates |

For VantageScore, the “good” range starts slightly lower at 661 and extends up to 780 [1]. Because lenders vary in which scoring model they use, it’s worth confirming which model your specific lender applies [6].

Takeaway: If your score is 670 or above on the FICO scale, you’re in the “good” zone. But the higher within that range, the better your terms will be. Every 20-point improvement can translate into measurably lower interest costs over the life of a loan.

To understand where this number comes from and what factors drive it, see our guide on what a credit score actually is.

Why “What Is a Good Credit Score” Depends on the Lender

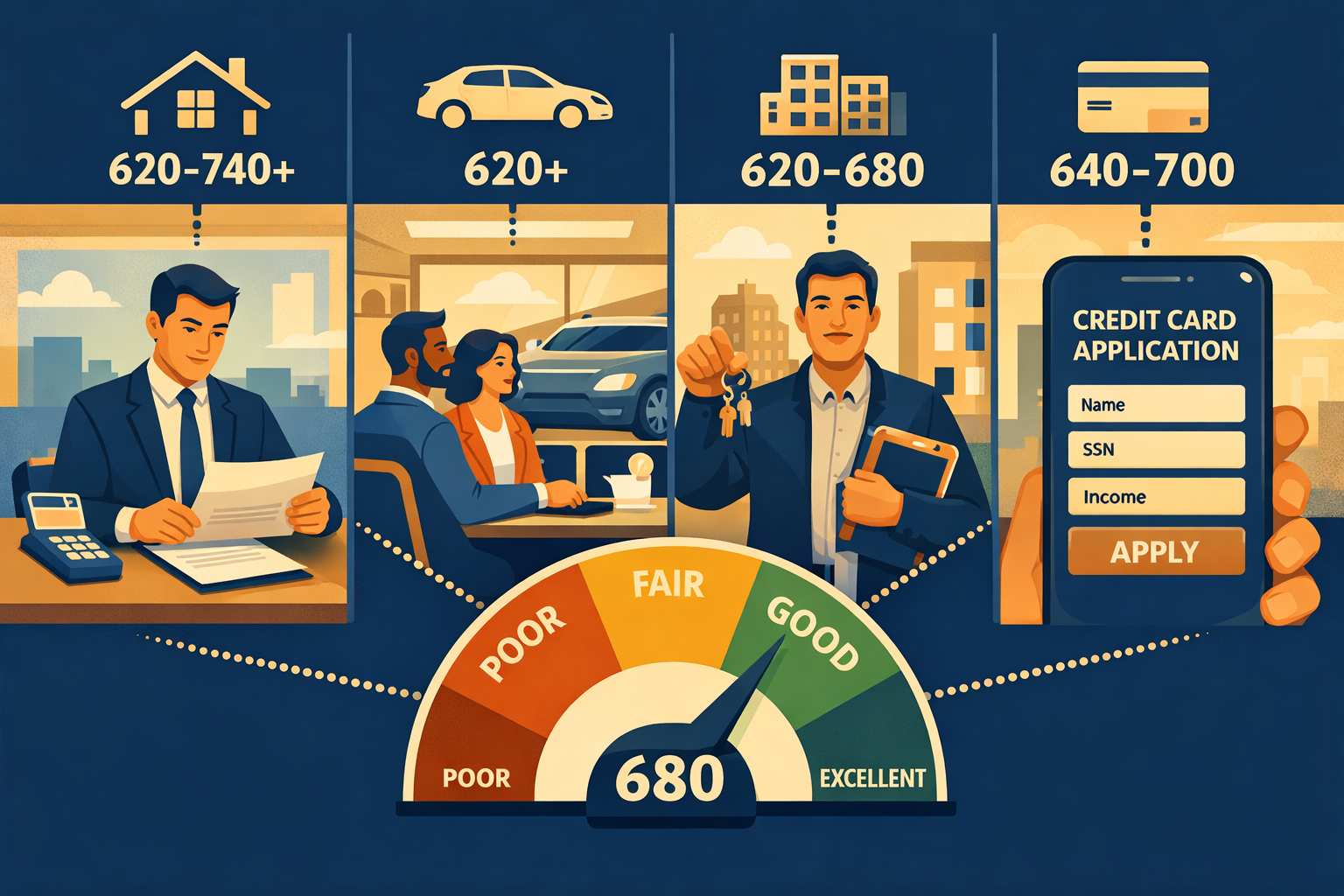

A score of 700 might get you approved for a credit card, but denied for a mortgage with the best rate. That’s because each lending industry, and each lender, sets its own risk thresholds.

Lenders don’t just look at whether your score is “good” in the abstract. They evaluate your score against the specific risk profile of the product they’re offering. A 30-year mortgage carries far more risk exposure than a $2,000 credit card limit, so the standards are different.

Typical Minimum Score Requirements by Product

| Loan or Credit Type | Common Minimum Score | Score for Best Terms |

|---|---|---|

| Conventional mortgage | 620 | 740+ |

| FHA mortgage | 580 (with 3.5% down) | 680+ |

| Auto loan (new car) | 620 | 720+ |

| Auto loan (used car) | 580 | 700+ |

| Credit card (standard) | 640–670 | 720+ |

| Credit card (premium rewards) | 700+ | 750+ |

| Apartment rental | 620–680 | 700+ |

| Personal loan | 600–640 | 700+ |

Sources: General lender guidelines compiled from [1][3][5]

How Risk Tiers Affect Interest Rate Pricing

Lenders use credit score tiers to set interest rates. This is where the math behind money becomes very tangible. A borrower with a 760 score might receive a mortgage rate 0.5–1.0 percentage points lower than someone with a 660 score. On a $300,000 mortgage over 30 years, that difference can equal $30,000–$60,000 in additional interest paid.

The same principle applies to auto loans and credit cards. Higher scores don’t just mean approval; they mean cheaper money.

Common mistake: Assuming that meeting the minimum score guarantees approval. Minimums are floors, not guarantees. Lenders also evaluate income, employment, existing debt, and recent credit activity.

What a Good Credit Score Actually Gets You

The real value of a good credit score isn’t the number itself. It’s the financial outcomes that number unlocks.

Concrete Benefits of a Good Score (670+)

- Lower interest rates on loans and credit cards. This is the single biggest financial benefit. Lower rates mean less money paid to lenders over time, which directly supports wealth building.

- Higher approval odds. Applications for mortgages, auto loans, and credit cards are significantly more likely to be approved.

- Lower security deposits. Utility companies, landlords, and cell phone carriers often reduce or waive deposits for borrowers with good credit.

- Higher credit limits. Lenders extend more available credit, which also helps keep your credit utilization ratio low.

- Better insurance premiums. In many states, auto and home insurers use credit-based insurance scores to set premiums.

- Stronger negotiating position. With a good score, you can shop multiple lenders and negotiate terms, because you have options.

Insight: A good credit score is a financial tool. It reduces the cost of borrowing, which means more of your income goes toward building assets rather than paying interest. That’s the compound growth effect applied to debt management.

A “Good” Score vs an “Approval” Score: Why 720 Can Still Get Denied

This is one of the most misunderstood aspects of credit. A good score improves your odds, but it does not guarantee approval. Lenders evaluate a full financial picture, not just one number.

What Lenders Evaluate Beyond Your Score

- Income and employment stability. Lenders need to see that you can afford the payments. A high score with low income can still result in denial.

- Debt-to-income ratio (DTI). This measures how much of your monthly gross income goes toward existing debt payments. Most mortgage lenders want DTI below 43%, and many prefer below 36%.

- Payment history patterns. Even with a 720 score, a recent 30-day late payment can raise red flags, especially for mortgage underwriters. Learn more about how payment history affects lending decisions.

- Recent credit inquiries and new accounts. Opening several new accounts in a short period signals higher risk, regardless of your overall score.

- Loan-to-value ratio (for mortgages). How much you’re borrowing relative to the property value matters independently of your credit score.

Example: A borrower with a 720 FICO score applies for a mortgage. Their score is solidly “good.” But their DTI is 48% because of student loans and a car payment. The lender denies the application, not because of the score, but because of the debt load.

Takeaway: Your credit score opens the door. Your full financial profile determines whether you walk through it.

How to Move From Fair to Good Credit

If your score currently sits in the 580–669 range (fair), moving into the “good” tier is achievable with consistent, disciplined behavior. There are no shortcuts, but the math is straightforward.

Step-by-Step Actions

- Make every payment on time. Payment history accounts for roughly 35% of your FICO score. Even one missed payment can drop your score significantly. Set up autopay for at least the minimum due on every account.

- Reduce credit utilization below 30%. Credit utilization (the percentage of your available credit you’re using) is the second most influential factor. Below 30% is the standard recommendation; below 10% is ideal. Check your available credit across all accounts.

- Keep older accounts open. The length of your credit history matters. Closing your oldest credit card shortens your average account age, which can lower your score. Learn more about the length of credit history and why it matters.

- Limit hard inquiries. Each hard inquiry (from applying for new credit) can temporarily reduce your score by a few points. Space out applications and only apply when you genuinely need the credit.

- Diversify your credit mix. Having a combination of revolving credit (credit cards) and installment credit (auto loans, student loans) shows lenders you can manage different types of debt.

- Dispute errors on your credit report. Mistakes happen. An incorrect late payment or a collection that isn’t yours can drag your score down unfairly. Review your credit report regularly and dispute inaccuracies.

For a more detailed roadmap, follow our step-by-step plan for how to build credit safely.

Biggest Myths About Good Credit Scores

Misinformation about credit scores is everywhere. Here are the most common myths, corrected with data-driven insights.

Myth 1: “You Need an 800 to Get Approved for Anything Good”

Reality: A score of 740+ qualifies you for nearly the same rates and terms as an 800+. The difference in interest rates between 760 and 820 is often negligible. Chasing a perfect score offers diminishing returns.

Myth 2: “Checking Your Own Score Hurts It”

Reality: Checking your own score is classified as a soft inquiry and has zero impact on your score [5]. Only hard inquiries from lender-initiated credit checks affect your score, and even those have a small, temporary effect.

Myth 3: “Carrying a Balance on Your Credit Card Helps Your Score”

Reality: This is false. Carrying a balance doesn’t help your score; it just costs you interest. What helps is using your credit card and paying it off. Utilization is measured at a point in time (usually your statement closing date), not by whether you carry a balance month to month.

Myth 4: “Closing Old Credit Cards Improves Your Score”

Reality: Closing a credit card reduces your total available credit, which increases your utilization ratio. It can also shorten your average account age. Both effects typically lower your score.

Myth 5: “All Credit Scores Are the Same”

Reality: FICO and VantageScore use different algorithms and category boundaries [1][6]. Your FICO score and VantageScore can differ by 20–40 points or more. Always check which model your lender uses.

How Long Does It Take to Reach a Good Credit Score

Credit improvement isn’t instant, but it follows predictable timelines based on where you’re starting.

| Starting Point | Typical Time to Reach 670+ | Key Actions |

|---|---|---|

| No credit history | 6–12 months | Open a secured card or become an authorized user; make on-time payments |

| Fair credit (580–669) | 3–9 months | Pay down balances, eliminate late payments, reduce utilization |

| Poor credit (below 580) | 12–24 months | Address collections, establish positive payment history, rebuild gradually |

Important Variables

- Negative items like collections or bankruptcies take longer to overcome. Most negative marks stay on your report for 7 years, though their impact fades over time. See our guide on how to remove collections from your credit report.

- Consistent behavior matters more than any single action. Lenders and scoring models reward patterns, not one-time fixes.

- Score recovery after a single late payment typically takes 3–6 months of on-time payments, assuming no other negative activity.

Takeaway: Building good credit is a function of time and consistency. No hack replaces months of responsible financial behavior.

What Lenders Really Care About More Than Your Score

Your credit score is a summary. It’s useful, but lenders making large lending decisions (especially mortgages) dig deeper into the underlying data.

The Factors Behind the Number

- Payment history detail. Not just “on time” or “late,” but how late, how recently, and how frequently. A 90-day late payment from last year is far more damaging than a 30-day late payment from five years ago.

- Debt trajectory. Are your balances going up or down? Lenders prefer borrowers who are actively reducing debt, not accumulating it.

- Account diversity. A borrower with only credit cards looks different from one with a mortgage, auto loan, and credit cards. A healthy credit mix signals broader financial experience.

- Stability indicators. The length of time at the current job, the length of time at the current address, and the consistency of income all factor into manual underwriting decisions.

Lenders review the detailed history inside your credit report, not just the three-digit score on top. Understanding what’s in that report gives you more control over the outcome.

How to Check Your Score Safely

Monitoring your credit score is a basic financial literacy practice. Here’s how to do it without any risk to your score.

Free Options Available in 2026

- AnnualCreditReport.com provides free credit reports from all three major credit bureaus (Equifax, Experian, and TransUnion) every week.

- Bank and credit card apps often include free FICO or VantageScore monitoring as a feature for account holders.

- Credit Karma, Credit Sesame, and similar services offer free VantageScore monitoring with regular updates.

Soft Inquiry vs Hard Inquiry

| Type | When It Happens | Impact on Score |

|---|---|---|

| Soft inquiry | Checking your own score, pre-approval offers, employer background checks | None |

| Hard inquiry | Applying for a credit card, loan, or mortgage | Small, temporary (typically 5–10 points for a few months) |

Key point: Checking your own score is always a soft inquiry and does not hurt your credit [5]. You should check your score at least quarterly, and ideally monthly, to catch errors or signs of fraud early.

Credit Score Range Checker

Enter your score to see your rating and what it means for lenders

Please enter a score between 300 and 850.

703

Good

What This Score Typically Means

Conclusion: A Good Credit Score Is a Result, Not a Goal

A good credit score, 670 or higher on the FICO scale, opens doors to lower interest rates, better approval odds, and reduced borrowing costs. But the score itself is an output. It’s the result of consistent financial behavior: paying on time, keeping balances low, maintaining older accounts, and borrowing responsibly.

Don’t chase a number. Build the habits that produce the number.

Actionable next steps:

- Check your current score using a free service. Know where you stand today.

- Review your credit report for errors or negative items that may be dragging your score down.

- Set up autopay on all credit accounts to protect your payment history.

- Calculate your utilization across all revolving accounts and work to get it below 30%, ideally below 10%.

- Avoid unnecessary new credit applications in the months before a major purchase, like a home or car.

The math behind money is clear on this: every percentage point of interest you avoid through better credit is money that stays in your pocket and compounds in your favor over time.

Related Reading

- What Is a Credit Score? — How scores are calculated and what factors matter most

- What Is a Credit Report? — The detailed record behind your score

- How to Increase Your Credit Score — Step-by-step strategies for improvement

- Credit: The Complete Guide — Understanding how borrowing works from the ground up

- How Long Do Late Payments Stay on Your Credit Report? — Timeline and impact of negative marks

References

[1] What Is A Good Credit Score – https://blog.kikoff.com/posts/what-is-a-good-credit-score

[3] What Credit Score Do Home Buyers Need Buy a House in 2026 – https://www.leaderbank.com/blog/what-credit-score-do-home-buyers-need-buy-house-2026

[4] Why You Need To Get And Keep A Good Credit Score – https://www.neamb.com/personal-finance/why-you-need-to-get-and-keep-a-good-credit-score

[5] What Is A Good Credit Score – https://www.usbank.com/credit-cards/credit-card-insider/building-credit/what-is-a-good-credit-score.html

[6] Your 2026 Credit Score Playbook: The Biggest Changes And What They Mean For You – https://www.pheplefcu.org/blogmain/2026/1/18/your-2026-credit-score-playbook-the-biggest-changes-and-what-they-mean-for-you

Disclaimer

This article is for educational purposes only and does not constitute financial advice. Credit score requirements, lender standards, and interest rates vary by institution, location, and individual circumstances. No specific credit score guarantees approval for any financial product. Consult with a qualified financial professional or lender for advice tailored to your situation.

About the Author

Max Fonji is the founder of The Rich Guy Math, a data-driven financial education platform focused on teaching the math behind money. With a background in financial analysis and personal finance education, Max creates evidence-based content covering credit literacy, investing fundamentals, wealth building, and risk management. Every article is designed to help readers make smarter financial decisions through numbers, logic, and clarity.

Frequently Asked Questions

Is 700 a good credit score?

Yes. A 700 FICO score falls within the “good” range (670–739) and is close to the national average of about 703. It qualifies borrowers for most standard credit products at competitive interest rates, though scores above 740 typically unlock the best loan terms.

Is 750 excellent credit?

Under the FICO scoring model, a 750 score is considered “very good” (740–799), not technically “excellent” (which begins at 800). However, a 750 score usually qualifies for nearly the same interest rates and lending terms as an 800+ score.

What credit score do apartments require?

Most landlords look for credit scores between 620 and 680, though requirements vary by property and location. In competitive rental markets, landlords may prefer 700+. A lower score does not always mean denial, but you may need a larger deposit or a co-signer.

What score is needed for a car loan?

Auto lenders typically require a minimum score between 580 and 620 for approval. Borrowers with scores below 670 often pay significantly higher interest rates. A credit score of 720 or higher usually qualifies for the best auto loan rates.

Can I get a credit card with a 600 credit score?

Yes, but options are limited. A 600 score falls in the “fair” range and generally qualifies for secured credit cards and some basic unsecured cards. Premium rewards cards usually require 700+. Using a secured card responsibly is one of the most effective ways to build toward a good credit score.

Does income affect my credit score?

No. Income is not included in FICO or VantageScore calculations. Credit scores are based on credit behavior such as payment history, credit utilization, length of credit history, credit mix, and new credit inquiries. Lenders do evaluate income separately when deciding loan approval.

How often does my credit score update?

Credit scores typically update every 30–45 days, depending on when lenders report information to the credit bureaus. After paying down balances, it may take one or two billing cycles for the improvement to appear in your score.

Is there one credit score or multiple?

There are multiple credit scores. FICO alone provides many industry-specific versions (such as FICO Auto Score and FICO Bankcard Score), and VantageScore is a separate scoring model. The score shown in free monitoring apps may differ from the score a mortgage lender checks.